")

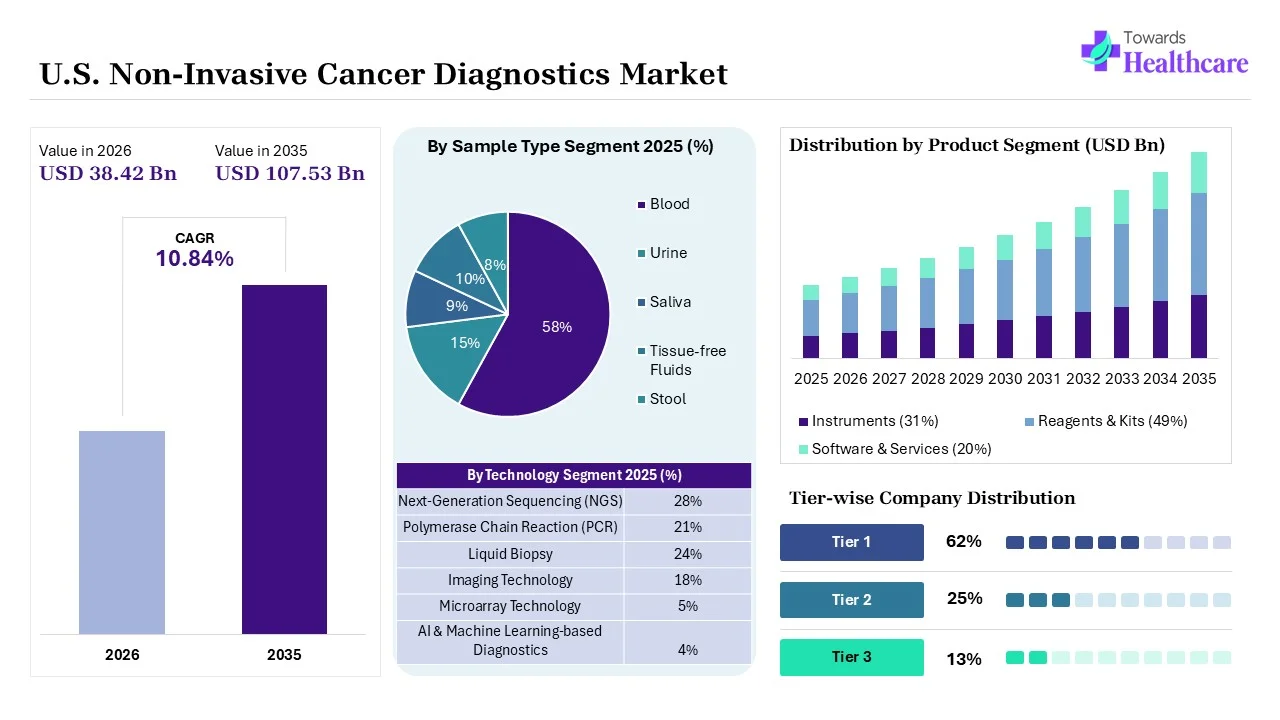

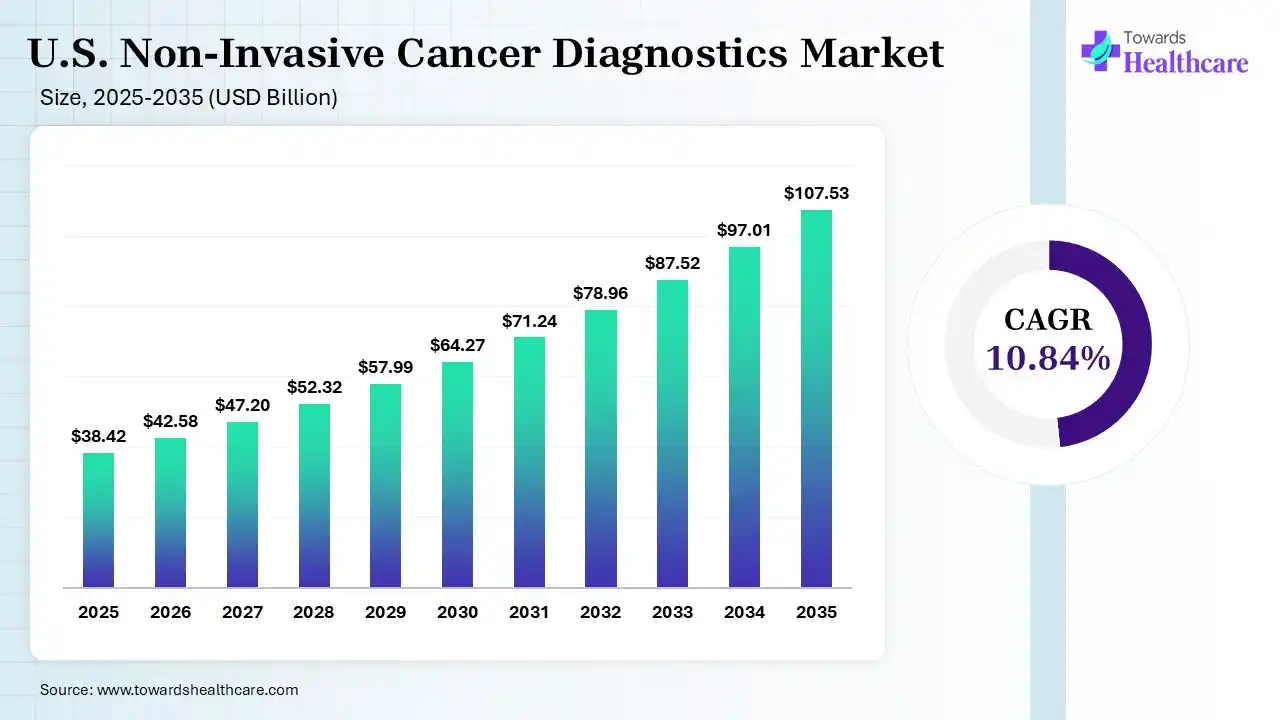

The U.S. non-invasive cancer diagnostics market size was estimated at USD 38.42 billion in 2025 and is predicted to increase from USD 42.58 billion in 2026 to approximately USD 107.53 billion by 2035, expanding at a CAGR of 10.84% from 2026 to 2035. The U.S. non-invasive cancer diagnostics market is increasing due to non-invasive cancer screening, with liquid biopsy, which detects cancer DNA from a simple blood test, allowing early detection.

")

Non-invasive diagnostic technology that detects cancer by analysing biomarkers such as ctDNA and CTCs in blood or various fluids. Non-invasive diagnostic technology includes processes that assess the body’s internal condition without penetrating the skin or entering the body surgically. They influence advanced imaging, digital technologies, and spectroscopy to offer clear and precise insights into the physiological or pathological conditions. In the cancer diagnosis, non-invasive imaging processes involving PET, MRI, and CT are critical. With the applications of radioactive tracers, PET scans diagnose cancers and track the efficiency of treatment by identifying metabolic activity. Non-invasive imaging allows real-time tracking of cancer response to medicines, enabling medical personnel to promptly adapt and enhance treatment plans.

AI-powered technology in non-invasive cancer diagnostics has demonstrated up to 90 % precision in challenges identificantion via non-invasive processes. AI-based technology is helping to enhance the speed, correctness, and reliability of various cancer screening and identification processes. AI-driven image analysis enhances cancer identification, biomarker discovery, and diagnostic consistency. Multimodal AI strategy integrates data from radiology, pathology, and genomics to offer inclusive diagnostic insights. This technology enhances diagnostic precision in radiology, pathology, dermatology, and ophthalmology by analysing images using applications of deep learning algorithms.

| Table | Scope |

| Market Size in 2026 | USD 42.58 Billion |

| Projected Market Size in 2035 | USD 107.53 Billion |

| CAGR (2026 - 2035) | 10.84% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Therapeutic Area, By End User, By Sample Type, By Application, By End User |

| Top Key Players | Illumina, Inc., Exact Sciences Corporation, Guardant Health, Inc., F. Hoffmann-La Roche Ltd. |

")

| Segment | Share 2025 (%) |

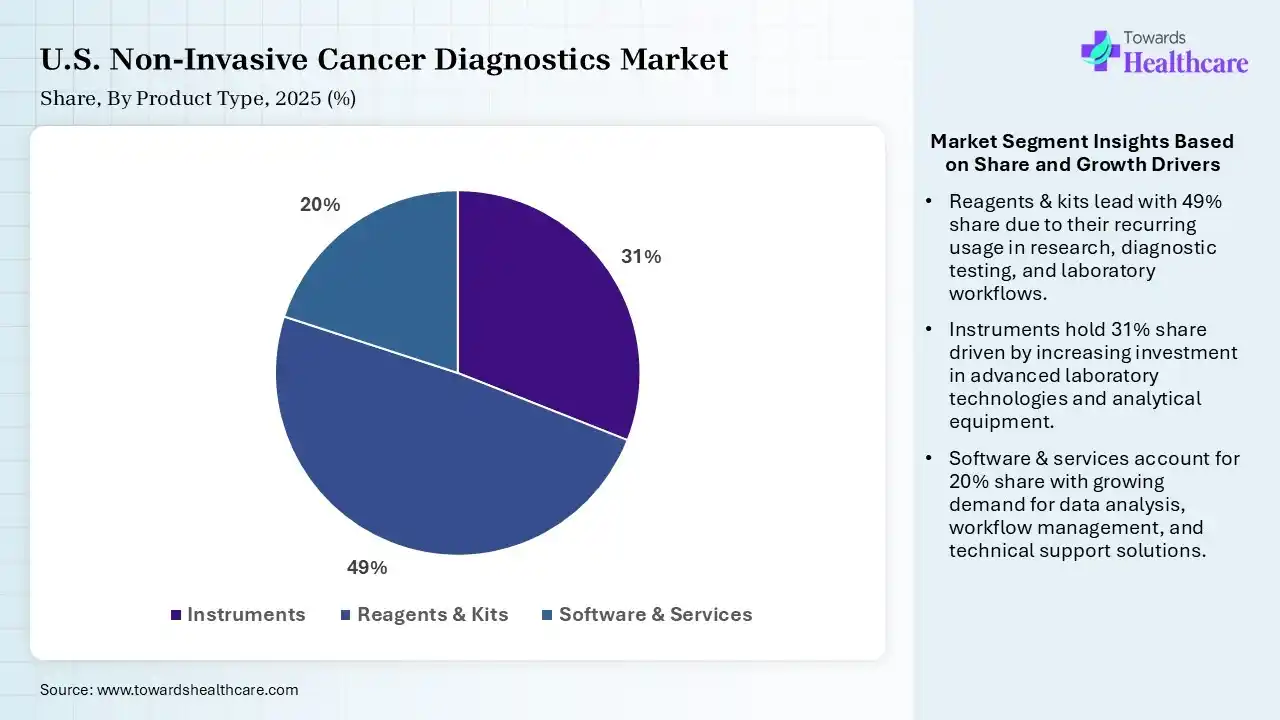

| Instruments | 31% |

| Reagents & Kits | 49% |

| Software & Services | 20% |

The Reagents & Kits Segment Led the U.S. Non-Invasive Cancer Diagnostics Market in 2025

The reagents & kits segment contributed the largest market share of 49% in 2025, as diagnostic reagents and kits identify diseases at an initial stage, and enhance treatment results. Molecular diagnosis determines the type of cancer and treatment approaches by detecting gene mutations in cancer cells.

The instruments segment held a significant share of 31% in the market, as instruments and analytical devices in cancer diagnostics transform oncology by allowing earlier identification, mapping exact cancer locations, and analysing tumors at the molecular level. Advanced tools detect ultra-low concentrations of tumor biomarkers from a single drop of blood or non-invasive fluid.

The software & services segment held a significant share of 20% in the market and is expected to grow at the fastest CAGR during the forecast period, as computing software plays a significant role in handling cancer big data by offering significant processing, infinite storage, accessibility, scalability, and affordability of computational resources. This software supports enhancing the speed, precision, and reliability of various cancer screening and detection methods.

")

| Segment | Share 2025 (%) |

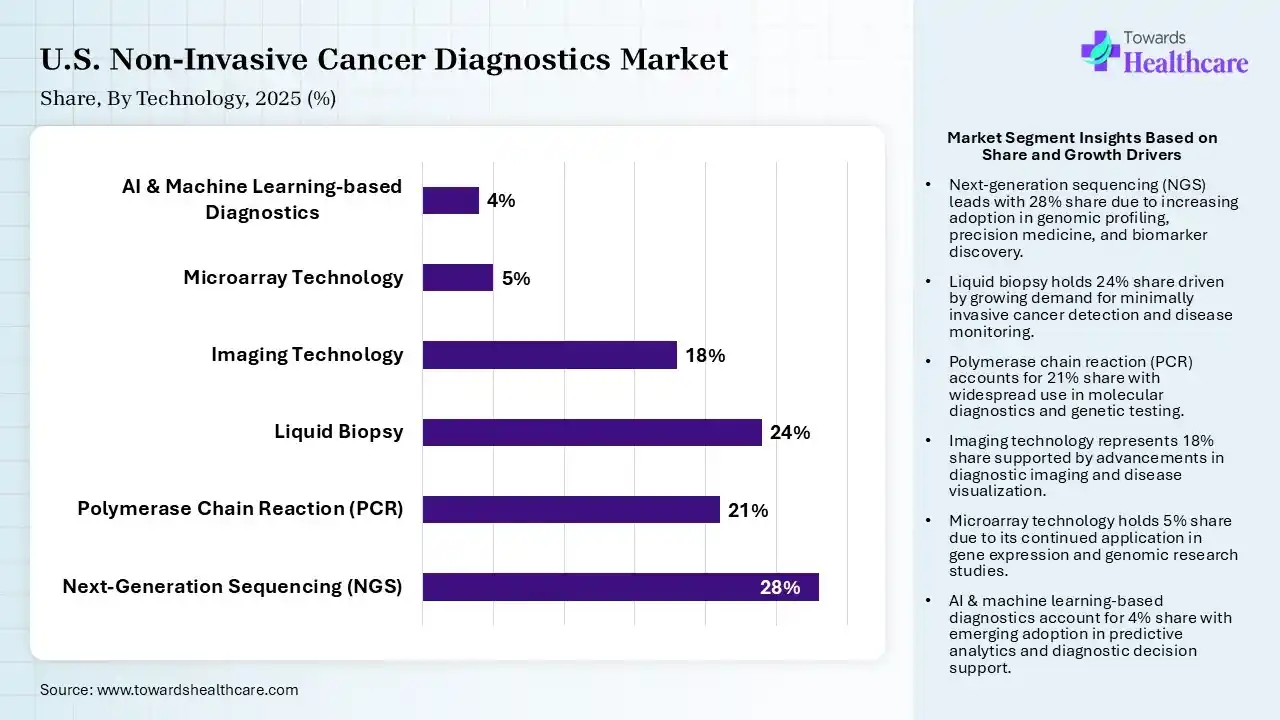

| Next-Generation Sequencing (NGS) | 28% |

| Polymerase Chain Reaction (PCR) | 21% |

| Liquid Biopsy | 24% |

| Imaging Technology | 18% |

| Microarray Technology | 5% |

| AI & Machine Learning-based Diagnostics | 4% |

Next-Generation Sequencing (NGS) Segment Led the U.S. Non-Invasive Cancer Diagnostics Market in 2025

The next-generation sequencing (NGS) segment contributed the largest market share of 28%, as next-generation sequencing (NGS) has evolved as a significant technology in the sector of oncology. NGS allows detailed genomic profiling of cancer, classifying genetic modifications that drive cancer progression and driving targeted treatment plans targeting particular mutations, therefore improving patient outcomes.

The liquid biopsy segment held a significant share of 24% of the market, and is expected to grow at the fastest CAGR during the forecast period, as liquid biopsies provides significant insights into tumor heterogeneity, treatment response, minimum residual disease identification, and targeted treatment of cancer via the analysis of circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), microRNAs, and extracellular vesicles.

The polymerase chain reaction (PCR) segment held a significant share of 21% of the U.S. non-invasive cancer diagnostics market, as PCR identifies cancer marker-expressing cells that are otherwise undetectable by other methods in patients with localized or metastatic cancer. These tests allow physicians to research mutations resulting from a certain type of cancer. PCR classifies mutations and genetic markers that inform cancer diagnostics.

The imaging technology segment held a significant share of 18% of the market. These technologies improved healthcare imaging by enabling more precise cancer localization, staging, and treatment response monitoring, eventually enhancing patient outcomes, particularly in oncology. It also helps physicians find cancer, determine how far a cancer has spread, and guide the delivery of particular treatments.

")

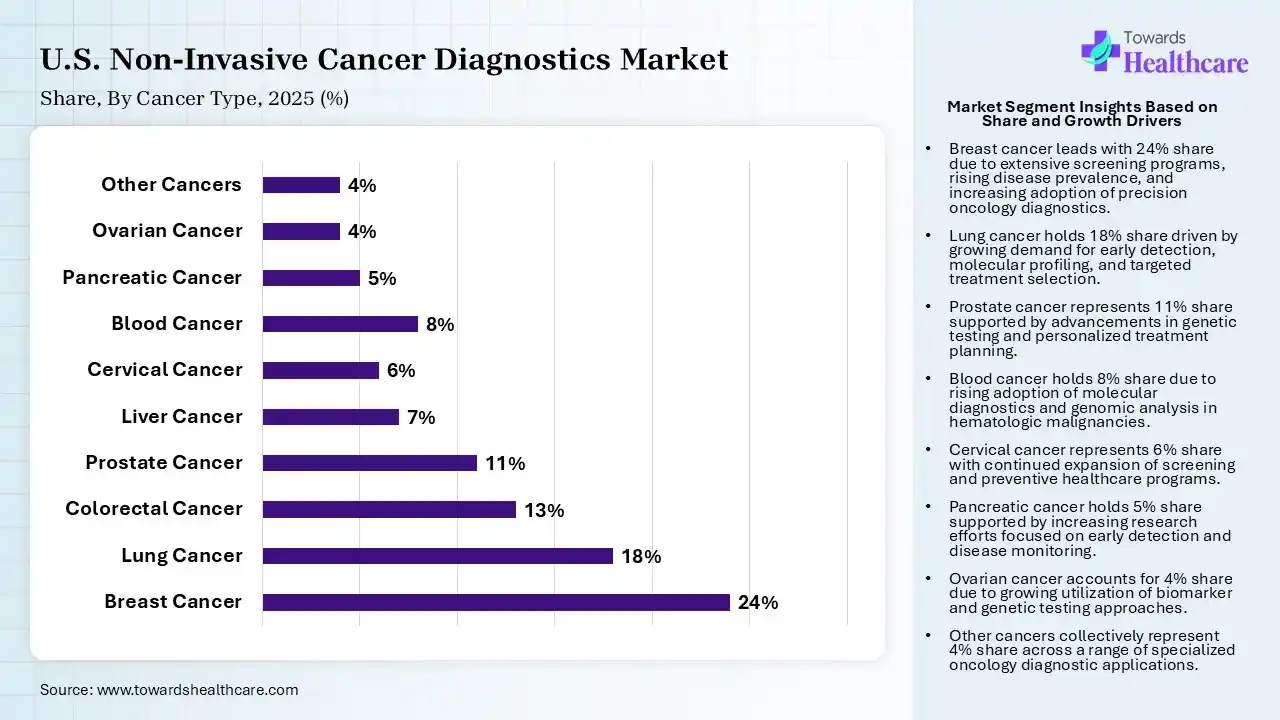

| Segment | Share 2025 (%) |

| Breast Cancer | 24% |

| Lung Cancer | 18% |

| Colorectal Cancer | 13% |

| Prostate Cancer | 11% |

| Liver Cancer | 7% |

| Cervical Cancer | 6% |

| Blood Cancer | 8% |

| Pancreatic Cancer | 5% |

| Ovarian Cancer | 4% |

| Other Cancers | 4% |

The Breast Cancer Segment led the U.S. Non-Invasive Cancer Diagnostics Market in 2025

The breast cancer segment held a significant share of 24% in the market. Non-invasive biomarkers like ctDNA, CTCs, and EVs hold significant promise for early identification and monitoring of breast cancer recurrence. It improves the accuracy of diagnosis. Timely screening improves treatment success, survival rates, and long-term health outcomes. By improving early diagnosis, liquid biopsy improves patient outcomes while lowering overall healthcare expenses.

The lung cancer segment contributed the largest market share of 18%, and is expected to grow at the fastest CAGR during the forecast period, as non-blood fluids provide a new, non-invasive choice for diagnosing lung cancer. Lung cancer patients could obtain more accurate treatment, and their development could be better tracked, using a novel high-tech process of non-invasive medical imaging analysis.

The colorectal cancer segment held a significant 13% share of the U.S. non-invasive cancer diagnostics market, as a non-invasive screening choice to make CRC detection rapid and easier. Innovative technologies, like the fecal occult blood test (FOBT), stool DNA testing, and blood-related biomarker assays, improve early identification and enhance patient results.

The prostate cancer segment held a significant share of 11% in the market, as the non-invasive tests renovate prostate cancer diagnosis by lowering technology and targeting biopsies to the highest-risk patients. Recent developments in biomarker tests show high specificity and negative prognostic value.

")

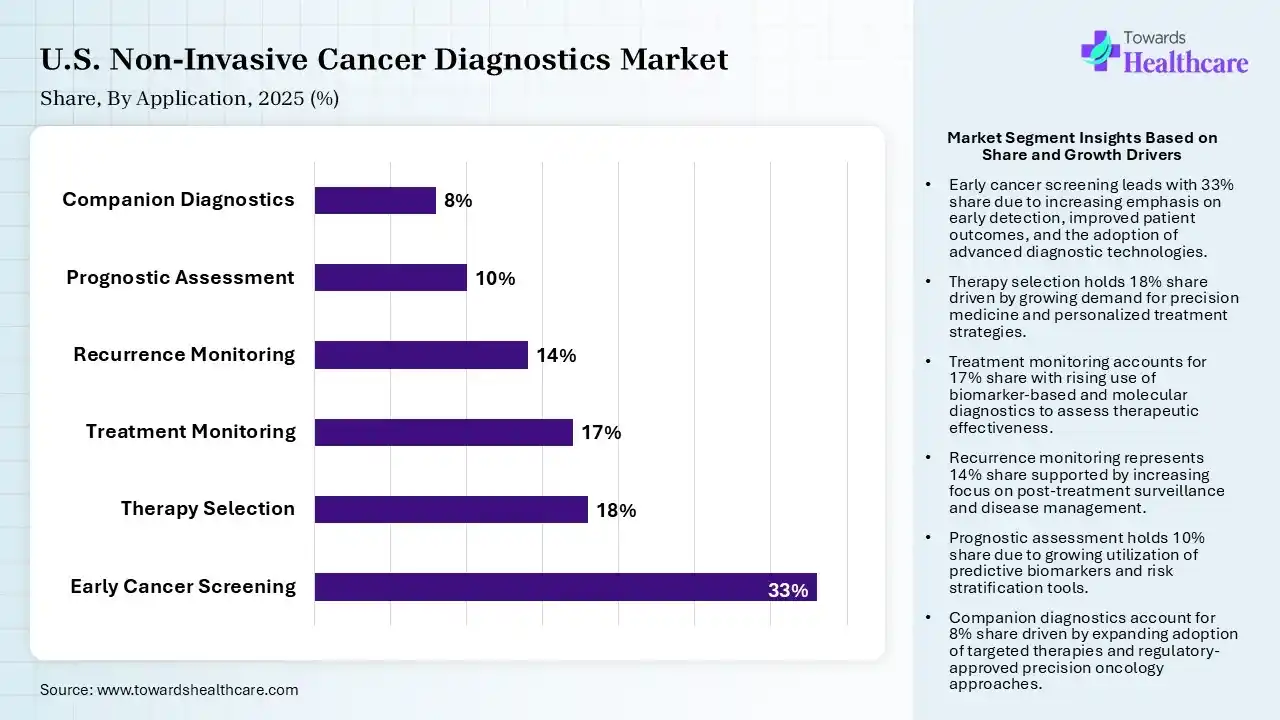

| Segment | Share 2025 (%) |

| Early Cancer Screening | 33% |

| Therapy Selection | 18% |

| Treatment Monitoring | 17% |

| Recurrence Monitoring | 14% |

| Prognostic Assessment | 10% |

| Companion Diagnostics | 8% |

The Early Cancer Screening Segment led the U.S. Non-Invasive Cancer Diagnostics Market in 2025

The early cancer screening segment contributed the largest market share of 33%, as early cancer detection is significant for efficient therapeutic intervention. Improves the capability to diagnose conditions at an early and treatable stage. Non-invasive technology is making cancer diagnostics less invasive and more effective.

The therapy selection segment held a significant share of 18% in the market, as non-invasive diagnostics offer actionable, highly accurate molecular and structural information without surgical incisions or tissue deletion. These safe, pain-free processes empower clinicians to pinpoint disease subtypes and track treatment effectiveness.

The treatment monitoring segment held a significant share of 17% in the U.S. non-invasive cancer diagnostics market, as non-invasive testing has evolved as a safer, more effective strategy for diagnostics, providing patients and medical care providers with alternatives to invasive procedures. These processes offer precise data related to the internal structures and organs of the body.

The recurrence monitoring segment held a significant share of 14% in the market, and is expected to grow at the fastest CAGR during the forecast period as non-invasive diagnostics lower complications, enable continuing monitoring, and more efficiently identify signs of treatment resistance and disease reappearance. It tracks disease dynamics with zero surgical trauma, allowing targeted therapy adjustments.

")

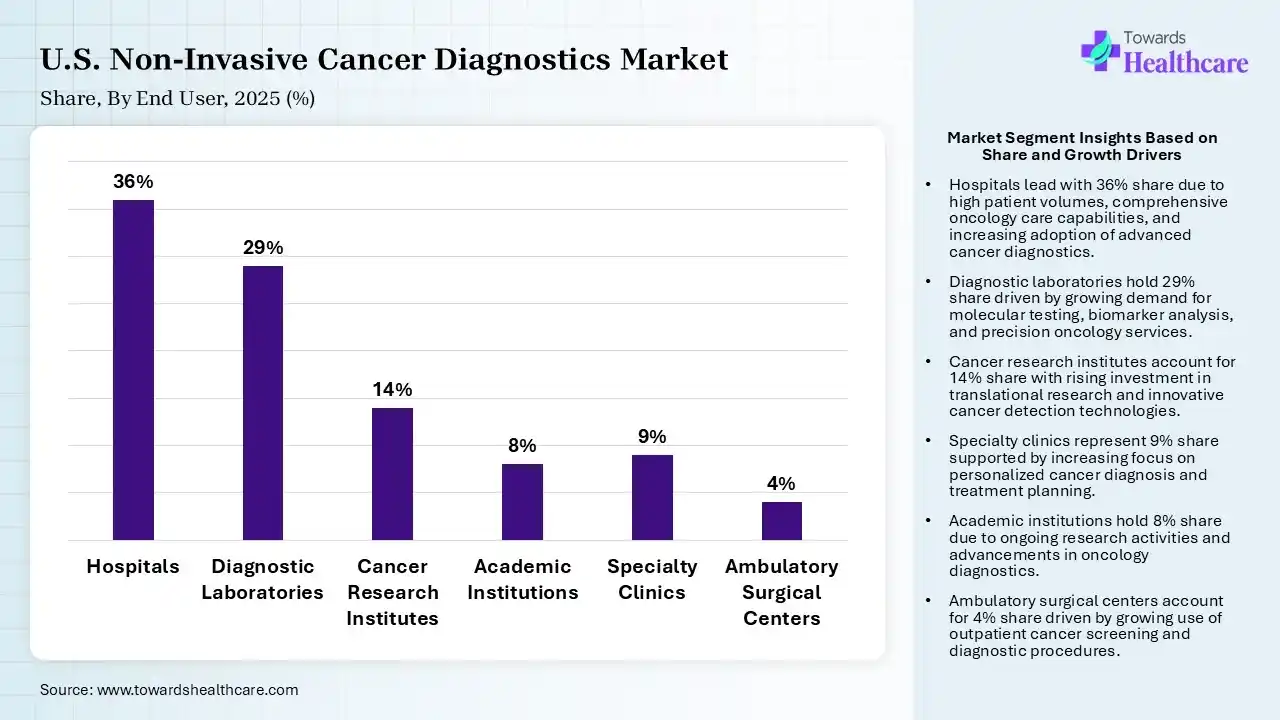

| Segment | Share 2025 (%) |

| Hospitals | 36% |

| Diagnostic Laboratories | 29% |

| Cancer Research Institutes | 14% |

| Academic Institutions | 8% |

| Specialty Clinics | 9% |

| Ambulatory Surgical Centers | 4% |

The Hospitals Segment led the U.S. Non-Invasive Cancer Diagnostics Market in 2025

The hospitals segment contributed the largest market share of 36%, non-invasive tests provide various benefits over invasive practices, involving lower challenges of complications, reducing discomfort, and shortening recovery times. Doctors perform these tests externally or via minimally invasive processes.

The diagnostic laboratories segment held a significant share of 29% in the market, and is expected to grow at the fastest CAGR during the forecast period, due to the use of non-invasive processes for early cancer detection. Early identification is significant for efficient therapeutic intervention, and non-invasive processes have emerged as promising tools to improve diagnostic accuracy and enhance patient outcomes.

The cancer research institutes segment held a significant share of 14% in the U.S. non-invasive cancer diagnostics market, due to non-invasive processes for early cancer identification. Early detection is significant for efficient therapeutic intervention, and non-invasive technology evolves as a promising tool to improve diagnostic precision and improve patient outcomes.

The academic institutions segment held a significant share of 8% in the market, as non-invasive imaging provides a visual image of the tumor's size, type, and location, which is one of its significant benefits. This technology enhances screening and diagnostic effectiveness, and liquid biopsy supports enhance diagnostic precision and lower healthcare expenses.

R&D

Clinical Trials & Regulatory Approvals

| Company | Headquarters | Latest Update |

| Illumina, Inc. | United States | This company leader in DNA sequencing and array-based technologies. Their platforms are foundational for detecting genetic mutations linked to cancer. |

| Exact Sciences Corporation | United States | Pioneers in non-invasive colorectal cancer screenings, a standard known for its stool-DNA test. |

| Guardant Health, Inc. | United States | Precision oncology leader specializing in liquid biopsies and inclusive genomic profiling. |

| F. Hoffmann-La Roche Ltd | United States | This product provides a comprehensive portfolio of cancer tissue diagnostics and molecular testing solutions. |

Strengths

Weakness

Opportunities

Threat

By Product Type

By Therapeutic Area

By Cancer User

By Sample Type

By Application

By End User

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar