Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

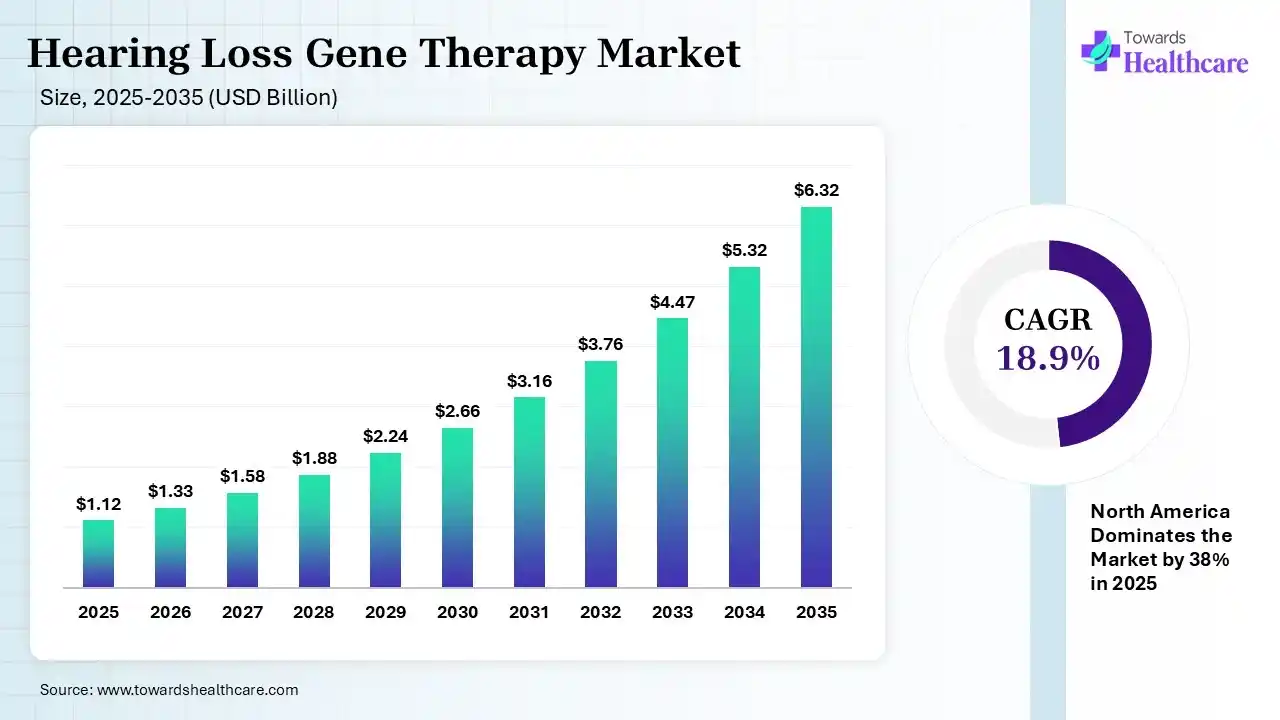

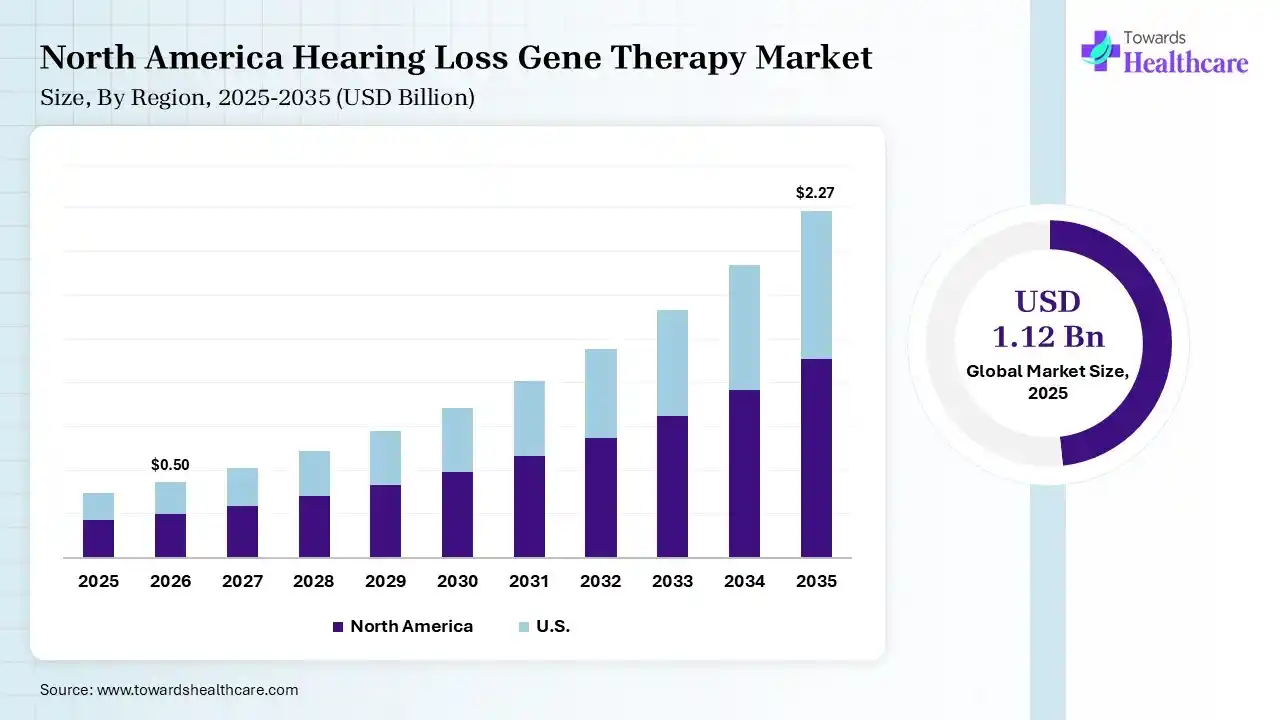

The global hearing loss gene therapy market size was estimated at USD 1.12 billion in 2025 and is predicted to increase from USD 1.33 billion in 2026 to approximately USD 6.32 billion by 2035, expanding at a CAGR of 18.9% from 2026 to 2035. A huge rise in the geriatric population, who are highly susceptible to hearing loss conditions, & rising funding in R&D and clinical trials, drive the overall market development. Eventually, the market will adopt gene editing approaches, like CRISPR Cas9, which fosters innovations in the hearing loss issues.

")

Beyond regulatory approvals, the industry is shifting from traditional management devices like cochlear implants to permanent biological cures. Breakthroughs in adeno-associated virus vectors allow scientists to inject healthy gene copies directly into the delicate inner ear cochlea. This method successfully targets specific genetic mutations, such as the OTOF gene responsible for congenital deafness, restoring natural sound transmission to the brain. Consequently, large pharmaceutical firms are aggressively expanding their pipelines to include treatments for adult-onset and noise-induced hearing loss. However, high development costs, precise surgical delivery requirements, and the need for early genetic screening remain major operational challenges. Overcoming these hurdles creates significant opportunities for specialized audiology clinics and innovative biotech partnerships worldwide, driving the next generation of standard patient care.

Primarily, the hearing loss gene therapy market is defined as the emergence of novel approved treatments to treat genetic issues that lead to deafness by employing functional genes into the inner ear. Whereas the global market progression is propelled by the massive rise in congenital, noise-induced, & age-related impairment, with increasing clinical trials success & FDA authorizations. Alongside, the development of targeted gene therapies to reach the main cause of inherited deafness is impacting the overall demand.

Specifically, the use of machine learning algorithms assists in estimating hereditary hearing loss from specific gene variants, including GJB2 & SLC26A4. Besides this, AI solutions support designing adeno-associated viruses (AAVs) for the efficient delivery of functional genes into inner ear hair cells. However, emerging new AI tools are facilitating deeper, 3D views of hair cell stereocilia, enabling researchers to assess how effectively gene therapy rescues damaged auditory structures.

Immersive Clinical Advances

Particularly, the market is emphasizing treatment for OTOF-related congenital deafness, while the FDA has approved Otarmeni, which enables a dual AAV vector to deliver a functional OTOF gene, resulting in a major enhancement in speech & hearing.

Fostering Vector Technology & Delivery

Nowadays, researchers are preferring recombinant Adeno-associated virus (rAAV) due to its safety, efficiency, & ability to be delivered directly into the inner ear via the round window membrane.

Spurring Non-Viral Vector Progression

Eventual studies are seeking into non-viral alternatives, such as nanoparticles or cationic lipids that enable repeated dosing.

| Table | Scope |

| Market Size in 2026 | USD 1.33 Billion |

| Projected Market Size in 2035 | USD 6.32 Billion |

| CAGR (2026 - 2035) | 18.9% |

| Leading Region | North America by 38% |

| Key Applications | OTOF-related deafness, sensorineural hearing loss, congenital hearing loss, syndromic hearing loss, acquired hearing loss |

| Primary End Users | Hospitals, ENT Clinics, Academic Medical Centers, Research Institutes, Biotechnology Companies |

| Key Growth Drivers | Rising prevalence of genetic hearing disorders, advances in AAV vectors, CRISPR technologies, regulatory support, increasing clinical trial success rates |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapy Type, By Vector Type, By Hearing Loss Type, By Delivery Method, By End User, By Region |

| Top Key Players | Regeneron Pharmaceuticals, Akouos (Eli Lilly), Sensorion, Fudan University, Otovia Therapeutics, Astellas Pharma, BridgeBio Pharma |

")

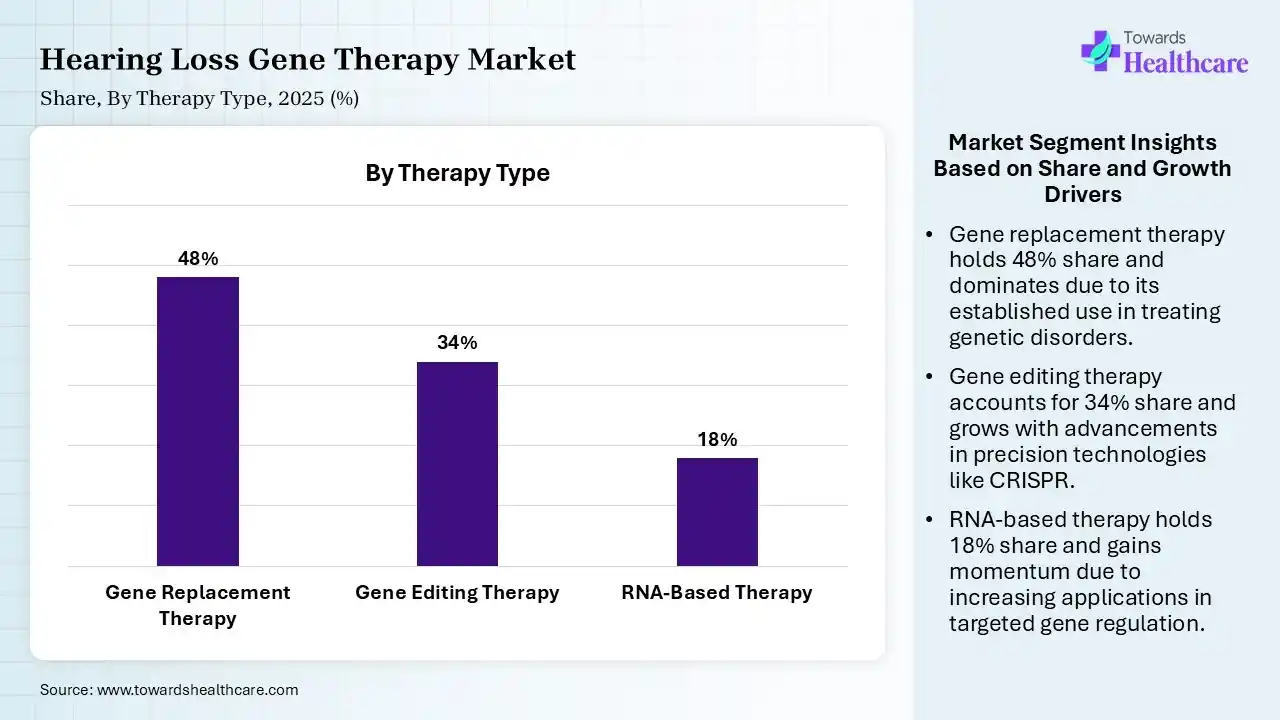

| Segment | Share 2025 (%) |

| Gene Replacement Therapy | 48% |

| Gene Editing Therapy | 34% |

| RNA-Based Therapy | 18% |

The Gene Replacement Therapy Segment Dominated the Market in 2025

In 2025, the gene replacement therapy segment held a dominant share of 48% of the hearing loss gene therapy market. Prominent catalysts include successful pre-clinical restoration of hearing in animal models and the ongoing evolution of safe AAV vectors for inner ear delivery. Whereas biological restoration offers extensive frequency resolution & pitch discrimination.

Moreover, the gene editing therapy segment captured the second largest share of a 34% in 2025 & is predicted to expand fastest. Globally surging cases of monogenic causes, breakthroughs in CRISPR/Cas9 technologies, & the inner ear’s accessibility for local, targeted delivery, fuel the demand for this therapy type. The latest study has shown the efficiency of CRISPR-based editing to treat DFNA41, which restores both hearing & balance in preclinical models.

The RNA-based therapy segment held 18% share of the hearing loss gene therapy market, as they facilitate reversible modulation of gene expression. Moreover, expanded research activities in antisense technologies & strengthened clinical trials are bolstering the therapeutic purposes of this type.

")

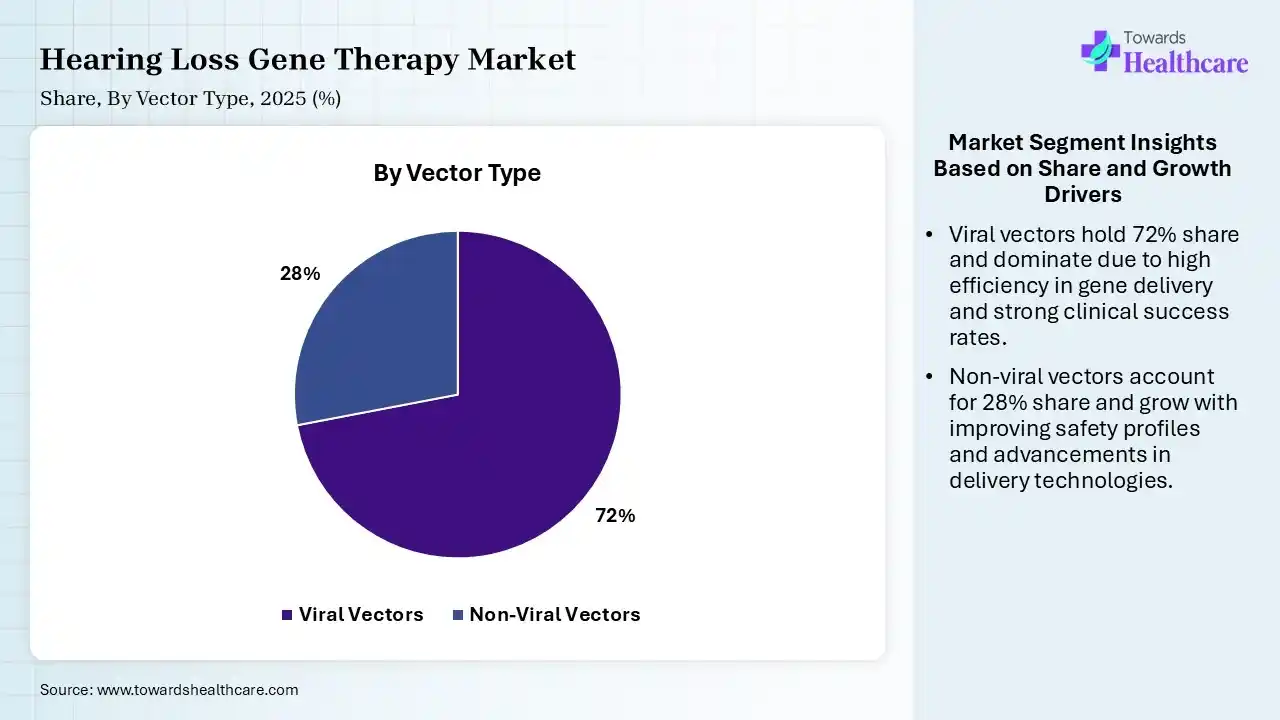

| Segment | Share 2025 (%) |

| Viral Vectors | 72% |

| Non-Viral Vectors | 28% |

The Viral Vectors Segment Led the Market in 2025

The viral vectors segment captured the largest share of a 72% of the market in 2025. Its dominance is propelled by its low immunogenicity, safety, & ability to transduce both dividing & non-dividing cells. Alongside, these vectors have a pivotal role in treating genetic sensorineural hearing loss, with Anc80L65, AAV1, & AAV2/9 being significant serotypes for targeting hair cells & assisting cells.

On the other hand, the non-viral vectors segment is anticipated to witness rapid expansion in the hearing loss gene therapy market. They have a high safety profile, with specialized carriers, such as lipid nanoparticles (LNPs) & polymeric carriers. The market is shifting towards breakthroughs in silica & gold nanoparticles, enabling non-invasive, targeted delivery of genetic materials.

")

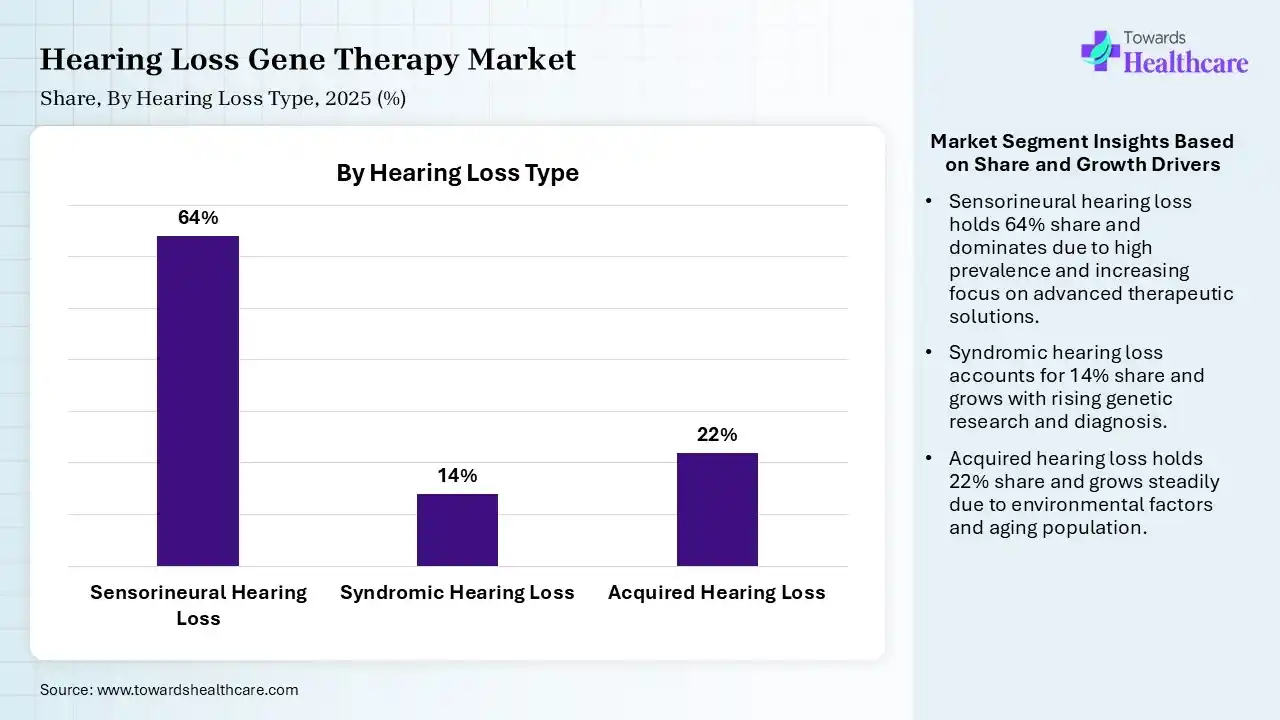

| Segment | Share 2025 (%) |

| Sensorineural Hearing Loss | 64% |

| Syndromic Hearing Loss | 14% |

| Acquired Hearing Loss | 22% |

The Sensorineural Hearing Loss Segment Was Dominant in the Market in 2025

In 2025, the sensorineural hearing loss segment led with a 64% share of the market. This kind is a permanent one, which also develops from genetic factors, head trauma, tumors, or autoimmune diseases. Researchers are investigating novel targeted therapies for various kinds of hereditary deafness, like Usher syndrome type 1C (USH1C) & connexin 26 (GJB2).

The acquired hearing loss segment held a 22% share in 2025 & is estimated to expand rapidly in the hearing loss gene therapy market. This type is fueled by higher exposure to sound greater than 85 dB, with side effects of ototoxic drugs, & viral infections/issues, like meningitis, mumps, & measles, can cause damage, especially in children.

In 2025, the syndromic hearing loss segment accounted for 14% share, due to the notable genetic mutations, such as autosomal dominant, recessive, or mitochondrial, connected with abnormalities in other body systems. Researchers are highly focused on Usher Syndrome by employing AAV vectors to deliver healthy genetic material to the inner ear.

")

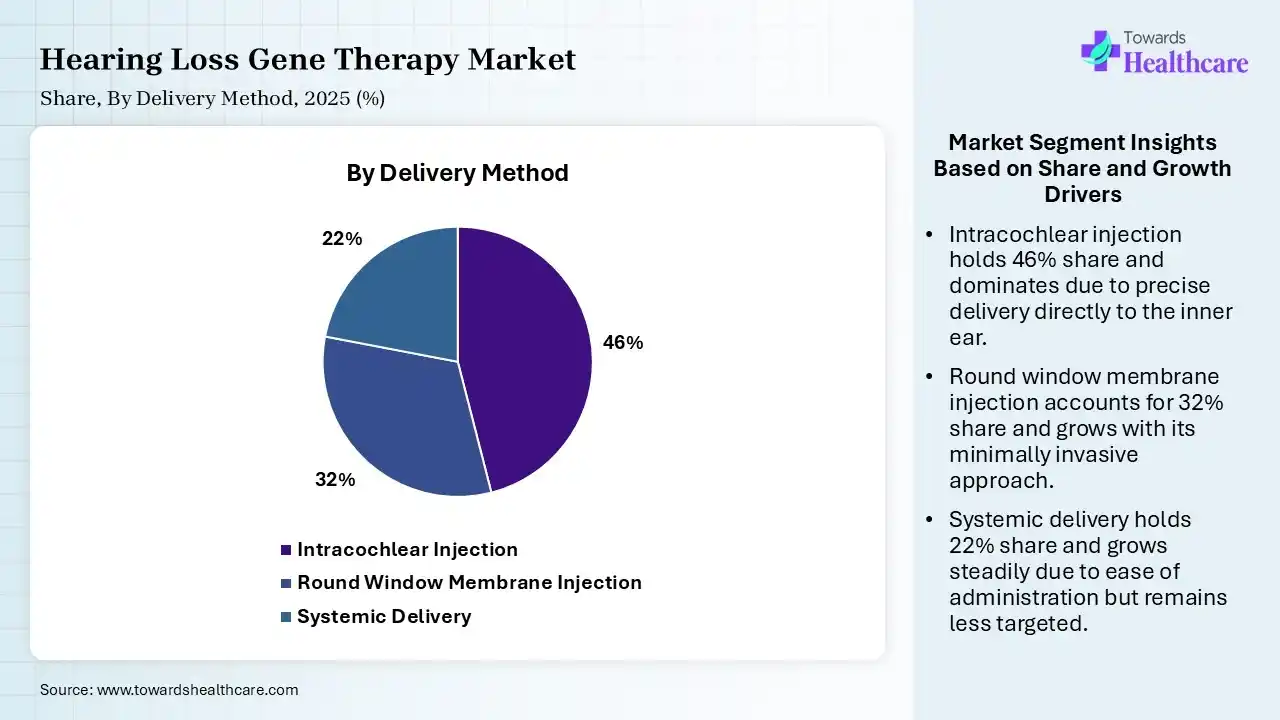

| Segment | Share 2025 (%) |

| Intracochlear Injection | 46% |

| Round Window Membrane Injection | 32% |

| Systemic Delivery | 22% |

The Intracochlear Injection Segment Dominated the Market in 2025

The intracochlear injection segment captured a 46% share of the hearing loss gene therapy market in 2025. Their dominance is driven by a direct, localised approach to restoring biological hearing & also targets the cellular roots of deafness. The leading organizations are using this method to treat hereditary sensorineural hearing loss (SNHL), which delivers viral vectors directly into the fluid-filled cochlea.

The round window membrane injection segment accounted for 32% share in 2025 & is anticipated to show the fastest growth. This is a minimally invasive approach, which improves patient safety, coupled with the emergence of delivery techniques, drives the overall adoption. This method is often unified with posterior semicircular canal fenestration (RWM+CF) to boost transduction in adult models, & enable wider expression.

However, the systemic delivery segment held a 22% share of the hearing loss gene therapy market. Respective expansion is fueled by its offerings, including a non-invasive option for gene therapy, with advances in targeting mechanisms to enhance specificity.

")

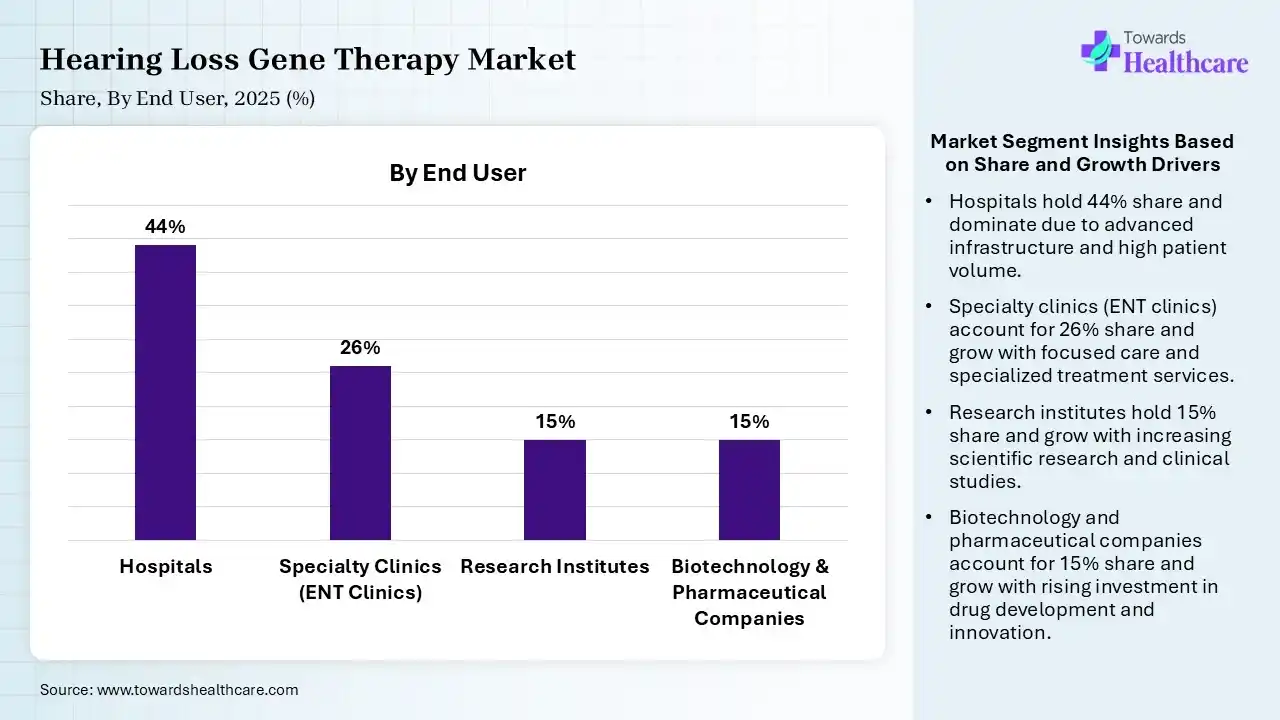

| Segment | Share 2025 (%) |

| Hospitals | 44% |

| Specialty Clinics (ENT Clinics) | 26% |

| Research Institutes | 15% |

| Biotechnology & Pharmaceutical Companies | 15% |

The Hospitals Segment Led the Market in 2025

In 2025, the hospitals segment dominated with a 44% share of the market. Primarily, hospitals provide rigorous ENT specialists, audiologists, & more sophisticated diagnostics. Besides this, hospitals offer robust diagnosis, cochlear implant surgery, hearing aid fitting, & rehabilitative therapy to boost quality of life & communication. They widely facilitate surgical, in vivo, round-window membrane injections.

The specialty clinics (ENT clinics) segment held the second-largest share of 26% of the hearing loss gene therapy market in 2025. These clinics are increasingly offering specialized, multi-disciplinary, & highly tailored care necessary for delicate inner ear treatments. They have a key role in finding genetic causes, accurate surgical delivery of therapeutics, & long-term monitoring.

However, the research institutes segment held 15% of the market share and is estimated to grow fastest in the market. Their expansion is promoting the transformation of viral vectors for precise gene delivery, performing vital preclinical trials on animal models, & exploring clinical trials to test safety & effectiveness. Many research institutes are working on CRISPR Cas9, gene editing approaches, optogenetics & gene therapy.

The biotechnology & pharmaceutical companies segment held a 15% share in 2025, due to the robust investment in R&D. Also, these companies are bolstering strategic alliances to raise commercialization, and emphasizing the progression of the biotech hub.

")

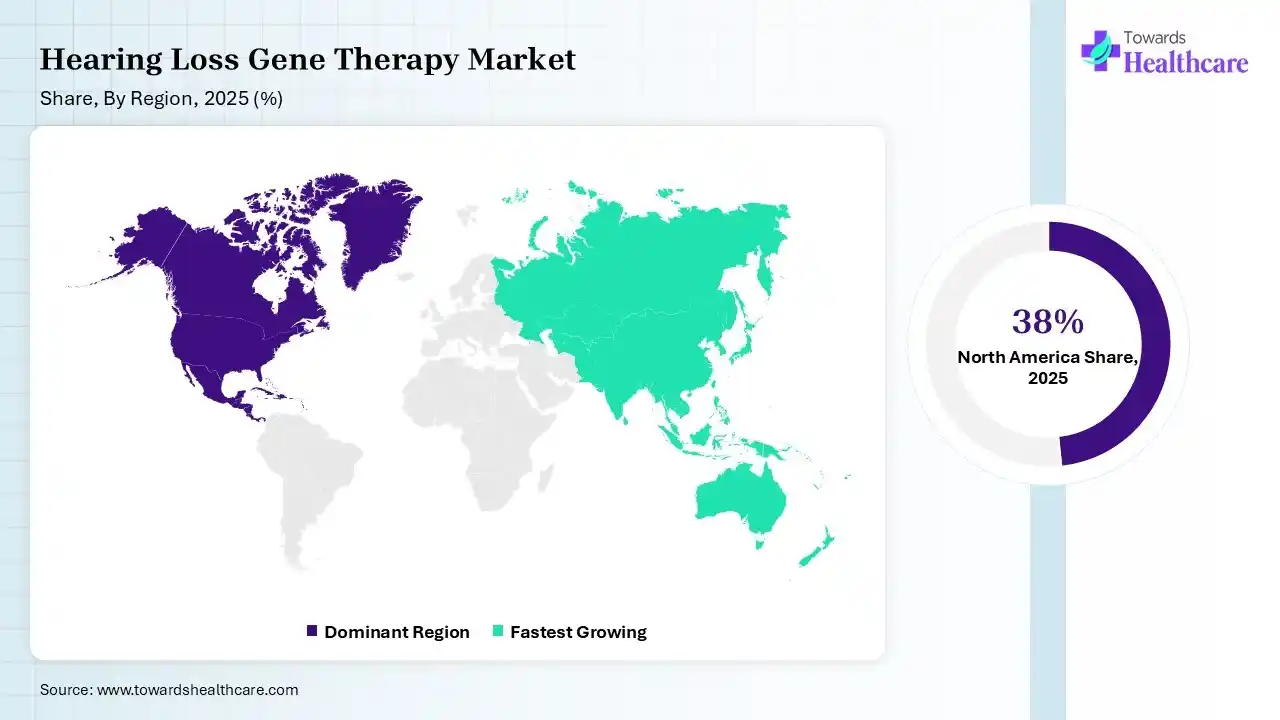

In 2025, North America led with a 38% share of the hearing loss gene therapy market, due to the strong presence of biotech leaders, which surges innovation. Also, the region has a well-nurtured healthcare infrastructure, which supports the broader adoption of these therapies. Additionally, the regional major private & public funding is spurring clinical trials for therapies, with a focus on restoration of hair cell function.

U.S. Market Trends

In the U.S., ongoing clinical trials are often targeting DFNB9, a specific form of congenital auditory neuropathy, coupled with prospective research activities on other genes, like TMPRSS3, PCDH15, & TMC1. Moreover, the respective market is demonstrating early studies, which show successful improvements in hearing & speech in children.

Canada Market Trends

Canada is establishing a strong footprint through integrated public healthcare initiatives. Recent population-based health metrics reveal that 19.2% of Canadian adults live with a measured form of hearing loss, while pediatric data indicate a 7.7% prevalence among children aged 6 to 19. Local biotechnology startups are leveraging these demographics to coordinate clinical trial recruitments, actively partnering with universal healthcare infrastructure to ensure widespread, long-term therapeutic access.

Mexico Market Trends

Mexico serves as a vital location for international testing due to distinct demographic trends. Out of the nation's total population, over 7.2 million citizens live with disabilities, and 33.5% of those cases involve severe hearing impairments. Recent international surveys indicate that Mexico exhibits some of the highest regional hearing loss rates alongside low rehabilitation uptake. This extensive, untreated patient population offers significant opportunities for global developers evaluating therapeutic efficacy.

Asia Pacific held 23% of the market share and is predicted to expand rapidly in the hearing loss gene therapy market. Major drivers involved in the upcoming progress are the vast geriatric population, mainly in China & Japan, which are highly prone to sensorineural hearing loss. This population is increasingly demanding the latest solutions for this type of concern. Many governments are heavily investing in biotechnology & gene therapy research by offering grants & easy approval measures.

China Market Trends

Moreover, China is estimated to grow at a rapid CAGR in the coming era. Specifically, teams from Fudan University's Eye & ENT Hospital are expanding globally in OTOF-related deafness (DFNB9) gene therapy. Numerous large-scale Chinese trials are developing rapidly to assess infants, children, & adults, with 90% of participants having substantial hearing optimization.

China is accelerating into a dominant market force owing to massive clinical numbers. The country faces an immense public health challenge, with a staggering 426.5 million people affected by varying degrees of hearing impairment. Over 50% of adults aged 50–54 report notable hearing issues, skyrocketing to 80% among older cohorts. This profound clinical burden is driving heavily funded domestic enterprises to rapidly deploy targeted inner-ear gene therapies nationwide.

Japan Market Trends

Japan leads in advanced precision healthcare due to an incredibly rapid population aging trend. Audiometric research reveals that 25% of men in their late 50s and 25% of women in their early 60s experience measurable hearing impairment, which escalates to 75% by their late 70s. Despite high clinical prevalence, only 14% of affected individuals utilize hearing aids, prompting specialized government frameworks to fast-track permanent biological gene therapy alternatives.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Regeneron Pharmaceuticals, Eli Lilly (Akouos), Sensorion, Astellas Pharma | Develop gene therapy platforms, vectors, and delivery technologies |

| Product Manufacturers | Regeneron, Eli Lilly, Sensorion, BridgeBio Pharma | Develop and commercialize hearing loss gene therapies |

| Service Providers | Boston Children's Hospital, Mayo Clinic, Mass Eye and Ear | Clinical administration, patient management, hearing restoration programs |

| Platform Providers | Regeneron, Eli Lilly, Astellas Pharma | AAV platforms, gene delivery systems, genetic medicine technologies |

| CROs/CDMOs | Charles River Laboratories, Catalent, Thermo Fisher Scientific, Lonza | Clinical development, manufacturing, viral vector production |

| Software Vendors | Illumina, SOPHiA GENETICS, QIAGEN Digital Insights | Genomic analysis and patient stratification tools |

| Research Institutions | Harvard Medical School, Fudan University, Institut Pasteur, Stanford University, University College London | Discovery research and translational studies |

| End-User Industries | Biotechnology, Pharmaceuticals, Hospitals, Academic Research Centers | Adoption and commercialization of therapies |

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 68% | 24% | 8% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Regeneron Pharmaceuticals | Tarrytown, New York, USA | USA | First FDA-approved hearing loss gene therapy; market leader | Otarmeni (lunsotogene parvec), OTOF gene therapy |

| Eli Lilly and Company (Akouos) | Indianapolis, Indiana, USA | USA | Major hearing gene therapy developer following Akouos acquisition | AK-OTOF, inner ear AAV gene therapy |

| Astellas Pharma Inc. | Tokyo, Japan | Japan | Active investor in regenerative medicine and gene therapy platforms | Auditory regenerative and gene therapy programs |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Sensorion | Montpellier, France | France | Leading deafness-focused biotech with clinical-stage assets | SENS-501, SENS-601 |

| Otovia Therapeutics | Shanghai, China | China | Focused on genetic hearing restoration technologies | OTOF-targeted gene therapies |

| Decibel Therapeutics* | Boston, Massachusetts, USA | USA | Pioneer in hearing therapeutics; technology integrated into Regeneron programs | DB-OTO platform origins |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Seamless Therapeutics | Dresden, Germany | Germany | Developing programmable genetic medicines for hearing loss | Recombinase-based gene editing platform |

| Audina Hearing Instruments | Orlando, Florida, USA | USA | Exploring advanced hearing restoration technologies | Hearing loss treatment solutions |

| Rinri Therapeutics | Sheffield, England, UK | United Kingdom | Developing regenerative therapies for sensorineural hearing loss | Auditory neuron replacement programs |

Strengths

Weaknesses

Opportunities

Threats

By Therapy Type

By Vector Type

By Hearing Loss Type

By Delivery Method

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar