Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

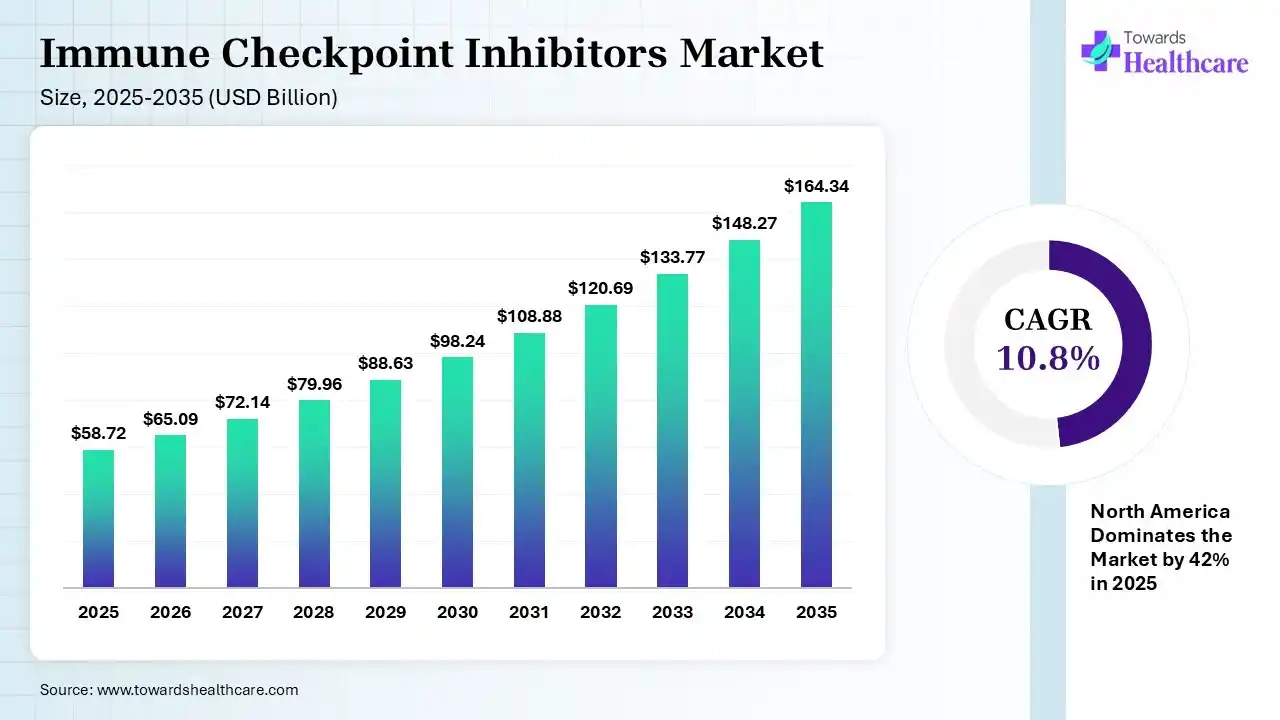

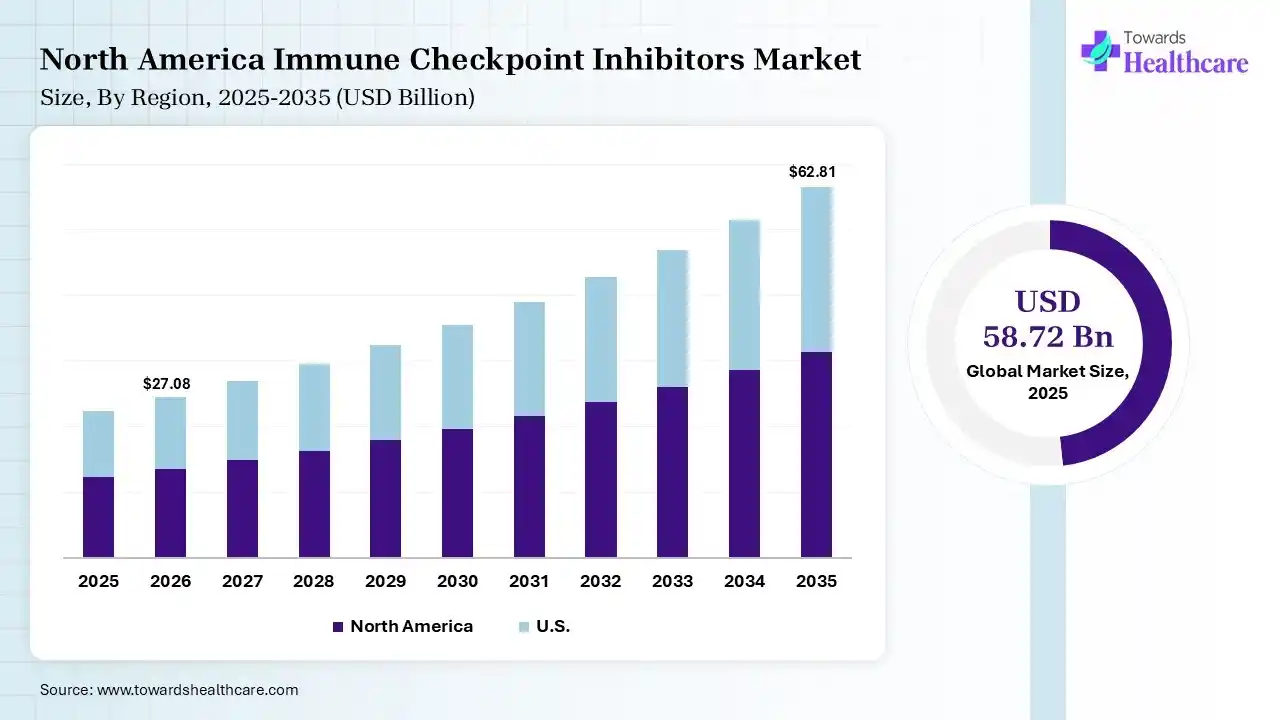

The global immune checkpoint inhibitors market size was estimated at USD 58.72 billion in 2025 and is predicted to increase from USD 65.09 billion in 2026 to approximately USD 164.34 billion by 2035, expanding at a CAGR of 10.84% from 2026 to 2035. A rise in the cancer burden globally is increasing the adoption of the immune checkpoint inhibitors. Their expanding applications, innovations, approvals, and launch of new products are also enhancing the market growth.

")

The immune checkpoint inhibitors market is driven by growing cancer incidences, increasing demand for combination therapies, and expansion of treatment into earlier-stage adjuvant settings. The immune checkpoint inhibitors refer to a class of cancer immunotherapy drugs responsible for enhancing the immune system for recognition and attack cancer cells. They are used for the treatment of multiple cancer types, advanced or metastatic cancers, and long-term disease control.

The immune checkpoint inhibitors market is expanding due to growing global cancer cases. Doctors use these innovative immunotherapy medicines to target advanced or metastatic tumors. These therapies work by blocking specific checkpoint proteins like PD1, PDL1, and CTLA4. These hidden proteins normally stop the body from fighting cancer cells. By unblocking them, the drugs reawaken immune cells to attack tumors. This market includes treatments for multiple malignancies like lung cancer, breast cancer, bladder cancer, and melanoma.

Growth in the immune checkpoint inhibitors market is fueled by new regulatory approvals. Hospitals and oncology clinics increasingly adopt these medications as preferred initial therapies. Furthermore, combining these inhibitors with traditional chemotherapy provides excellent patient outcomes. Researchers are heavily investing in finding next-generation treatments to prevent drug resistance. New delivery methods like quick skin injections also support easy outpatient care models. Ultimately, these treatments offer long-term disease control and improve patient survival.

The use of AI is increasing in the development of immune checkpoint inhibitors as they are being used for the identification of new checkpoint targets, biomarker discovery, and treatment optimization. It is also used for the analysis of tumor response, the prediction of immune-related side effects, and forecasting treatment outcomes. AI is also being used to offer personalized immunotherapy decisions and clinical trial design.

Blooming Combination Therapies

To enhance response rates, survival benefits, and overcome resistance, there is a rise in the development of new combination therapies. This, in turn, is driving the combinations of immune checkpoint inhibitors with chemotherapy, radiotherapy, and targeted therapies.

Emerging Next-Generation Checkpoint Targets

Growing R&D activities are driving the discovery of new immune targets such as LAG-3, TIM-3, and TIGIT. This is promoting the development of next-generation immune checkpoint inhibitors.

Expanding Clinical Applications

Increasing applications of the immune checkpoint inhibitors are driving their adoption beyond the treatment of advanced cancers. This is increasing their use for early-stage cancers and to prevent their recurrences.

| Table | Scope |

| Market Size in 2026 | USD 65.09 Billion |

| Projected Market Size in 2035 | USD 164.34 Billion |

| CAGR (2026 - 2035) | 10.84% |

| Leading Region | North America by 42% |

| Key Applications | Lung Cancer, Melanoma, Renal Cell Carcinoma, Head & Neck Cancer, Bladder Cancer, Hodgkin Lymphoma, Gastric Cancer, Liver Cancer |

| Primary End Users | Hospitals, Cancer Centers, Oncology Clinics, Academic Research Institutes |

| Key Challenges | High treatment costs, immune-related adverse events, patent expirations, reimbursement constraints, variable patient response rates |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Type, By Indication, By End User, By Distribution Channel, By Therapy Type, By Region |

| Top Key Players | Merck & Co., Pfizer, Bristol Myers Squibb, Sanofi, Roche (Genentech), BeiGene, AstraZeneca, Junshi Biosciences, Regeneron, GSK (GlaxoSmithKline) |

")

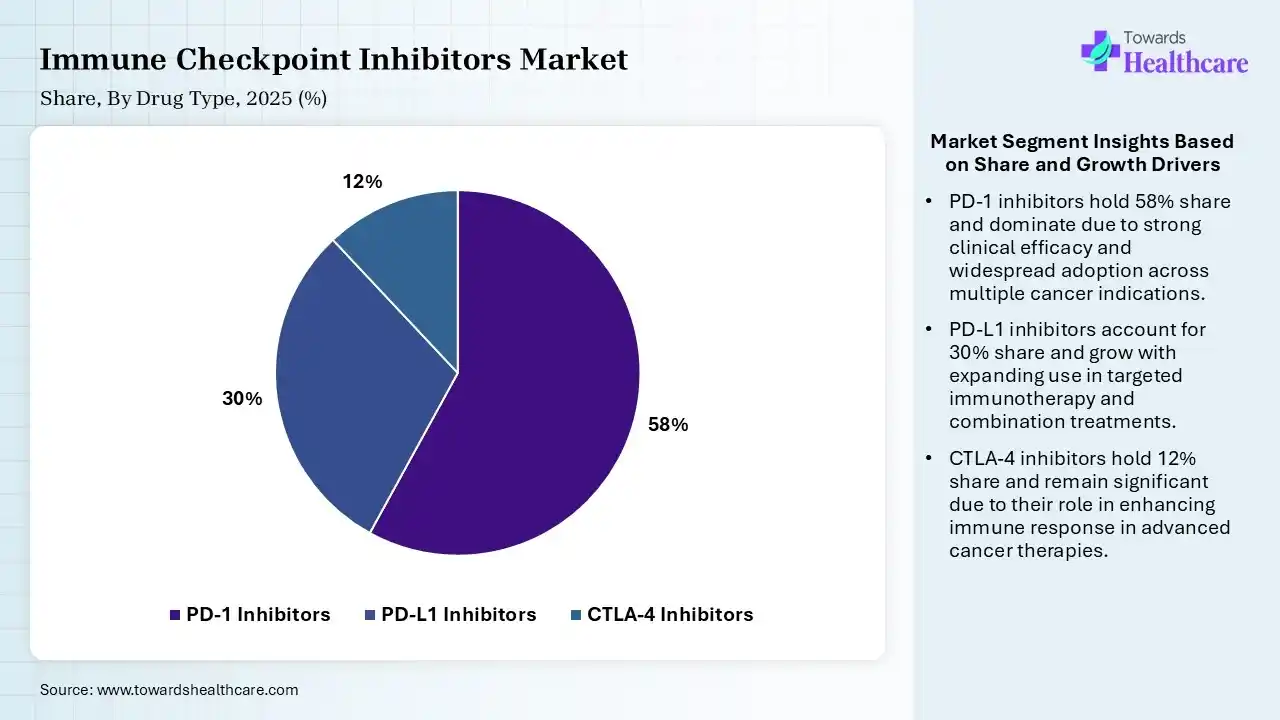

| Segment | Share 2025 (%) |

| PD-1 Inhibitors | 58% |

| PD-L1 Inhibitors | 30% |

| CTLA-4 Inhibitors | 12% |

The PD-1 Inhibitors Segment Dominated the Market With 58% in 2025

The PD-1 inhibitors segment led the immune checkpoint inhibitors market with 58% share in 2025 and is expected to witness the fastest growth with a CAGR of 11.20% during the forecast period, due to growth in their approval rates for multiple cancers. Strong clinical efficacy is responsible for improved survival outcomes, also increasing their use. Physicians also preferred PD-1 due to better safety profiles.

The PD-L1 inhibitors segment held the second-largest share of 30% of the market in 2025, driven by the increasing use in combination regimens, which boosts their demand. Broader pipeline expansion also supports growth. Favorable reimbursement policies also improve their access.

The CTLA-4 inhibitors segment held 12% of the immune checkpoint inhibitors market share in 2025, due to their use in combination therapies. Improved dosing strategies reduce toxicity concerns, increasing their use. Growing clinical trials continue exploring new indications.

")

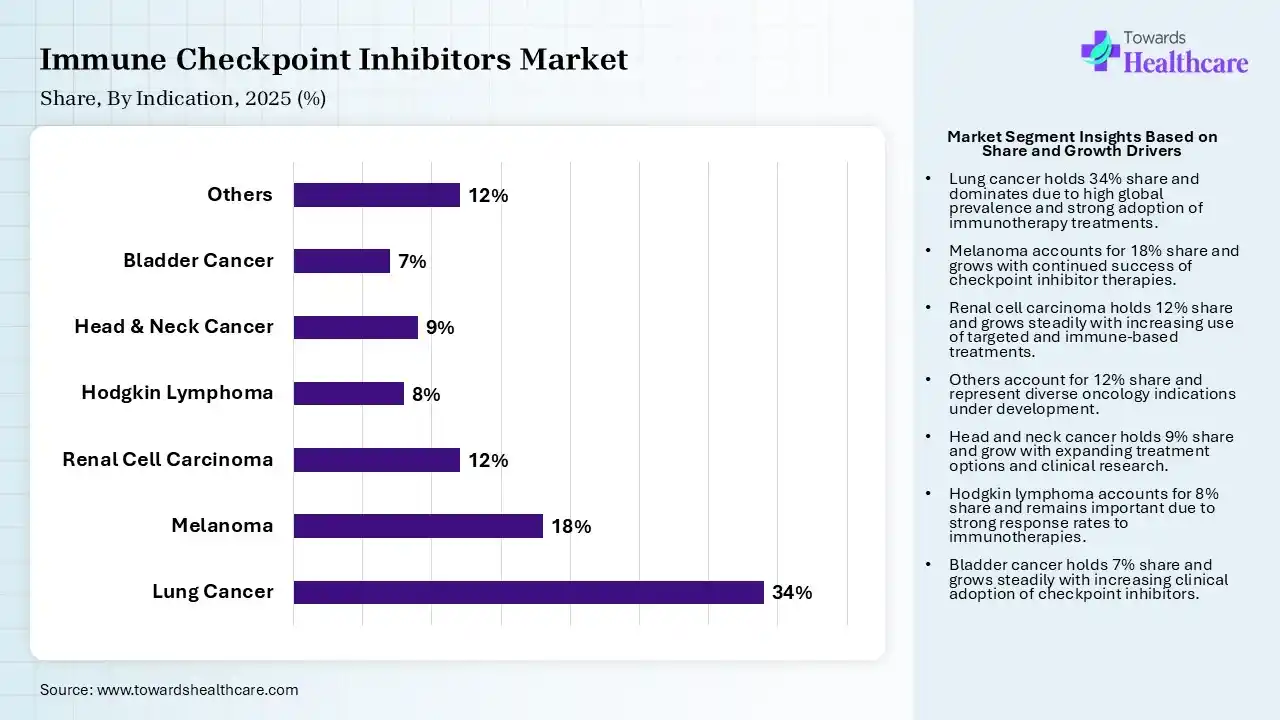

| Segment | Share 2025 (%) |

| Lung Cancer | 34% |

| Melanoma | 18% |

| Renal Cell Carcinoma | 12% |

| Hodgkin Lymphoma | 8% |

| Head & Neck Cancer | 9% |

| Bladder Cancer | 7% |

| Others | 12% |

The Lung Cancer Segment Dominated the Market With 34% in 2025

The lung cancer segment accounted for the highest revenue share of 34% of the immune checkpoint inhibitors market in 2025, driven by high global incidence, which increased the demand for immunotherapy. Strong clinical outcomes in NSCLC also encouraged their adoption. Combination regimens also expanded their treatment scope.

The melanoma segment held the second-largest share of 18% of the market in 2025, due to the early success of checkpoint inhibitors sustaining usage. Their high response rates improve treatment preference. Continued innovation also enhances outcomes.

The others segment held 12% of the immune checkpoint inhibitors market share in 2025 and is expected to show the highest growth with a CAGR of 12.40% during the forecast period, driven by the expanding use of immune checkpoint inhibitors in emerging cancer types. Ongoing trials are unlocking new indications. Precision oncology also supports targeted treatment adoption.

The renal cell carcinoma segment held 12% of the market share in 2025, due to the rising use of combination therapies. Increasing diagnosis rates expand the patient pool, driving the demand for immune checkpoint inhibitors. Favorable survival benefits also drive their adoption.

")

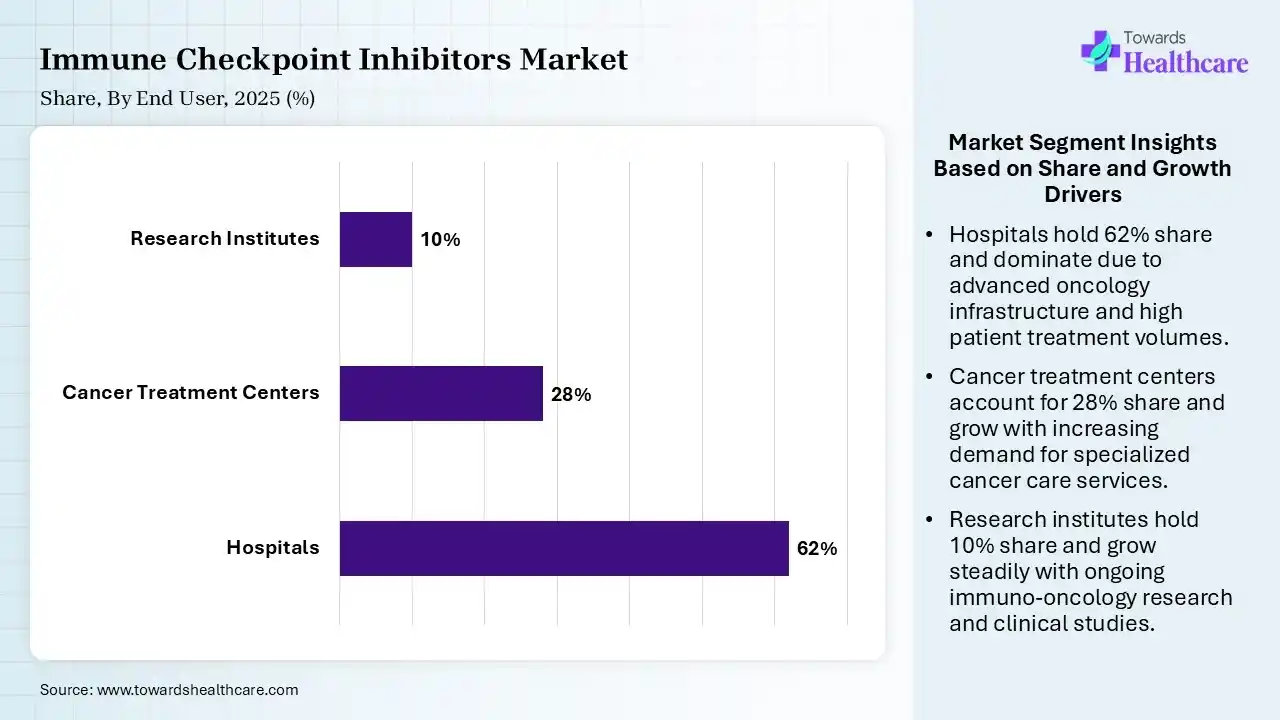

| Segment | Share 2025 (%) |

| Hospitals | 62% |

| Cancer Treatment Centers | 28% |

| Research Institutes | 10% |

The Hospitals Segment Dominated the Market With 62% in 2025

The hospitals segment held a major revenue share of 62% of the immune checkpoint inhibitors market in 2025, due to the presence of advanced infrastructure that supported complex immunotherapy delivery. Higher patient inflow also increased the demand for immune checkpoint inhibitors. The availability of oncology specialists also increased their usage.

The cancer treatment centers segment held the second-largest share of 28% of the market in 2025 and is expected to expand rapidly with a CAGR of 11.6% during the forecast period, driven by their specialized oncology care, which enhances treatment outcomes. A rising number of dedicated centers also supports their growth. Increasing preference for targeted care also drives their demand.

The research institutes segment held 10% of the immune checkpoint inhibitors market share in 2025, due to growing clinical trials, which expand the use of immune checkpoint inhibitors. Academic collaborations also boost their innovation. Government funding also supports their research activities.

")

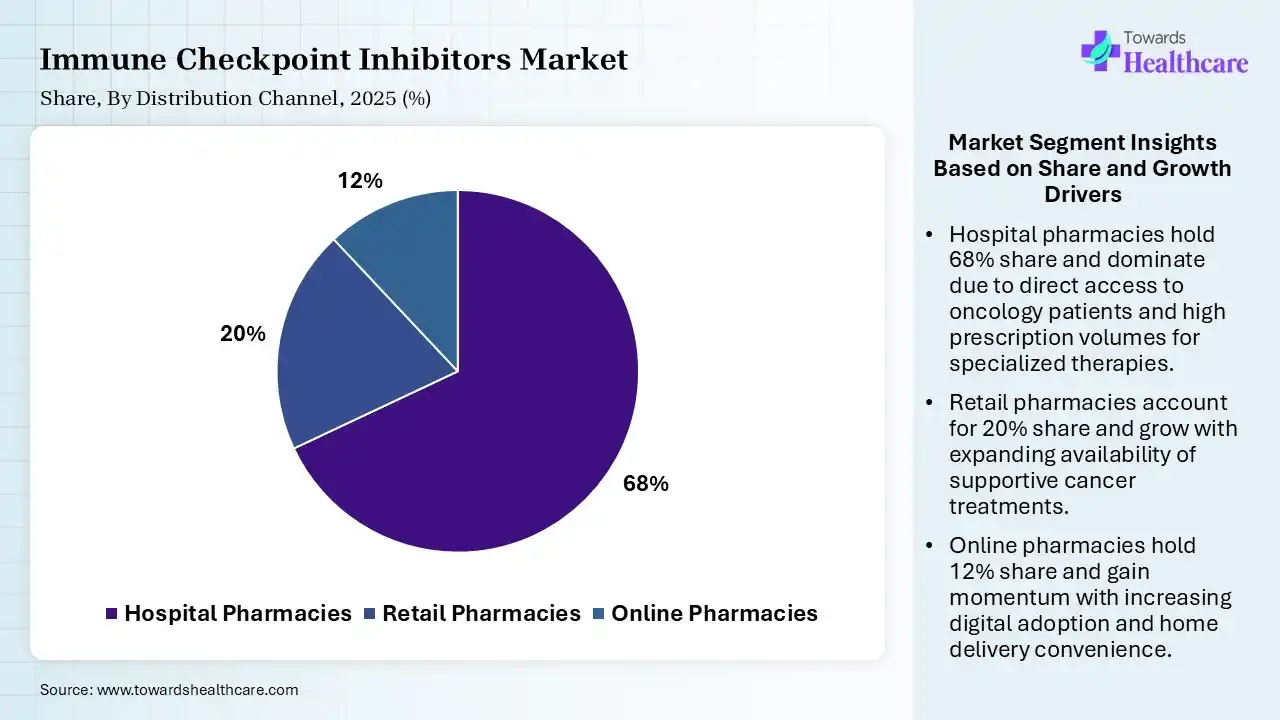

| Segment | Share 2025 (%) |

| Hospital Pharmacies | 68% |

| Retail Pharmacies | 20% |

| Online Pharmacies | 12% |

The Hospital Pharmacies Segment Dominated the Market With 68% in 2025

The hospital pharmacies segment held the largest revenue share of 68% of the immune checkpoint inhibitors market in 2025, driven by direct administration in hospitals, which contributed to their distribution dominance. Their specialized handling also increased their use. Additionally, the availability of oncology treatments also increased their use.

The retail pharmacies segment held the second-largest share of 20% of the market in 2025, due to increasing outpatient treatment, which is supporting the growth of retail pharmacies. Improved availability also enhances their access. Increasing specialty pharmacy services and distribution networks are also attracting patients.

The online pharmacies segment held 12% of the immune checkpoint inhibitors market share in 2025 and is expected to grow with the fastest CAGR of 12.10% during the forecast period, due to digital healthcare adoption. Enhanced convenience and accessibility also drive their usage. Expanding telemedicine platforms also supports their growth.

")

| Segment | Share 2025 (%) |

| Monotherapy | 46% |

| Combination Therapy | 54% |

The Combination Therapy Segment Dominated the Market With 54% in 2025

The combination therapy segment contributed the biggest revenue share of 54% of the immune checkpoint inhibitors market in 2025 and is expected to gain the highest share with a CAGR of 12.30% during the forecast period, due to their superior clinical outcomes, which promoted their rapid adoption. Synergistic effects improved response rates, increasing their demand. Ongoing trials also contributed to the expansion of the combination options.

The monotherapy segment held the second-largest share of 46% of the market in 2025, driven by its simpler treatment regimens, which drive adoption. Lower toxicity compared to combinations also supports its usage. Established efficacy also sustains their demand.

")

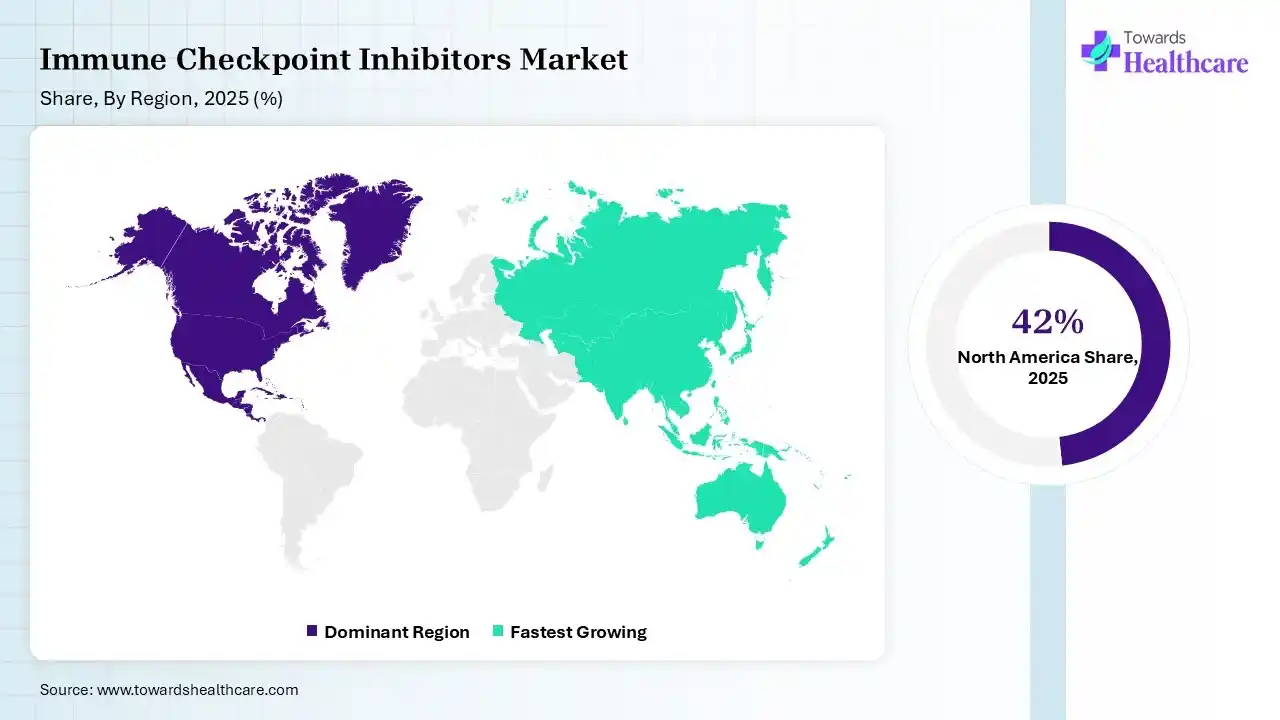

North America dominated the immune checkpoint inhibitors market with 42% in 2025, due to strong regulatory approvals, which accelerated the adoption of immune checkpoint inhibitors. High healthcare spending also supported the use of advanced therapies. The presence of key players enhanced innovations, which contributed to the market growth.

U.S. Market Trends

High cancer prevalence across the U.S. is increasing the adoption of the immune checkpoint inhibitors. Favorable reimbursement policies are enhancing the accessibility of these products. Moreover, extensive clinical trials are also driving the development of new immune checkpoint inhibitors for a wide range of indications.

Canada Market Trends

The immune checkpoint inhibitors market in Canada is growing due to strong government support. The country has a publicly funded universal healthcare system. This system ensures easy patient access to vital new cancer treatments. Health Canada is accelerating its approvals for advanced immunotherapy options. Leading oncology clinics across provinces quickly adopt these medicines for complex tumors. Strong academic research collaborations also drive therapy innovation throughout the nation.

Mexico Market Trends

The immune checkpoint inhibitors market in Mexico is expanding because of rising cancer cases. Public health institutions are actively working to include these modern therapies in standard care packages. Medical tourism is also driving increased investments in advanced private oncology centers. Private clinics frequently purchase these innovative drugs for international patients. Local awareness campaigns are helping patients understand the benefits of early immunotherapy options.

Asia Pacific held 22% share of the immune checkpoint inhibitors market in 2025 and is expected to grow at the fastest CAGR of 12.60% during the forecast period, due to a large patient pool, which drives rapid expansion of immune checkpoint inhibitors. Improving healthcare infrastructure also boosts their access. Rising investments in oncology also support their growth, enhancing the market growth.

India Market Trends

Expanding oncology infrastructure across India is driving the adoption of the immune checkpoint inhibitors. Rising health awareness is increasing the diagnosis rates and early cancer detection, ultimately increasing the demand for immune checkpoint inhibitors. Increasing affordability also drives their growth.

China Market Trends

The immune checkpoint inhibitors market in China is expanding very rapidly. The government is introducing fast-track approval policies for urgent oncology medications. Local biotech companies are successfully producing affordable domestic immunotherapy alternatives. This domestic production significantly lowers treatment costs for patients nationwide. Hospitals are including these treatments in the national reimbursement drug list. Consequently, millions of citizens gain immediate access to lifesaving cancer therapies.

Japan Market Trends

The immune checkpoint inhibitors market in Japan is expanding due to a rapidly aging population. Elderly citizens experience higher cancer risks, increasing the demand for advanced treatments. Japan has an excellent universal health insurance system covering expensive modern medicines. Regulatory bodies prioritize the swift evaluation of new oncology products. Leading Japanese pharmaceutical companies are heavily investing in clinical trials for complex combination therapies.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Bristol Myers Squibb, Merck & Co., Roche, AstraZeneca | Develop checkpoint inhibition platforms and novel immunotherapy technologies |

| Product Manufacturers | Merck & Co., Bristol Myers Squibb, Roche, AstraZeneca, Regeneron | Commercial production and global supply of checkpoint inhibitors |

| Service Providers | McKesson, Cardinal Health, Cencora | Oncology distribution, specialty pharmacy support, patient access programs |

| Platform Providers | BeiGene, GSK, Junshi Biosciences | Immuno-oncology development platforms and clinical expansion |

| CROs | ICON plc, IQVIA, Syneos Health, Parexel | Clinical trial management and regulatory support |

| CDMOs | Lonza, Samsung Biologics, WuXi Biologics | Biologics manufacturing and commercial-scale production |

| Software Vendors | IQVIA, Oracle Health, Medidata | Clinical data management and oncology trial analytics |

| Research Institutions | National Cancer Institute (NCI), MD Anderson Cancer Center, Dana-Farber Cancer Institute | Immunotherapy research and clinical validation |

| End-User Industries | Hospitals, Cancer Treatment Centers, Oncology Networks | Administration and monitoring of checkpoint inhibitor therapies |

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 72% | 22% | 6% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Merck & Co. | Rahway, New Jersey | USA | Market leader with the highest-selling checkpoint inhibitor globally | Keytruda (Pembrolizumab) |

| Bristol Myers Squibb | Princeton, New Jersey | USA | Pioneer in checkpoint inhibition and broad immuno-oncology portfolio | Opdivo, Yervoy, Opdualag |

| Roche | Basel | Switzerland | Strong PD-L1 franchise and extensive oncology footprint | Tecentriq |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| GSK | London, England | United Kingdom | Expanding oncology business through checkpoint inhibitor assets | Jemperli |

| Sanofi | Paris | France | Commercial immuno-oncology presence and strategic oncology investments | Libtayo (co-commercialization) |

| BeiGene | Beijing | China | Fast-growing oncology innovator with expanding international presence | Tevimbra (Tislelizumab) |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Junshi Biosciences | Shanghai | China | Commercialized PD-1 inhibitor with international expansion strategy | Tuoyi (Toripalimab) |

| Innovent Biologics | Suzhou, Jiangsu | China | Strong oncology pipeline and approved checkpoint inhibitors | Tyvyt (Sintilimab) |

| Coherus BioSciences | Redwood City, California | USA | Commercial immuno-oncology expansion through checkpoint inhibitor assets | Loqtorzi (Toripalimab) |

In February 2026, “We’re pleased to partner with two of the largest healthcare and distribution companies to launch ANKTIVA to patients in Saudi Arabia and across the broader Middle East and North Africa region,” said Richard Adcock, President and CEO of ImmunityBio. “Their combined world-class commercial infrastructure and proven track record in bringing innovative therapies to patients with serious diseases will help accelerate access to ANKTIVA and support our commitment to serving physicians and health systems throughout the region, including Saudi Arabia, United Arab Emirates, Qatar, and Egypt.”

Strengths

Weaknesses

Opportunities

Threats

By Drug Type

By Indication

By End User

By Distribution Channel

By Therapy Type

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar