Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

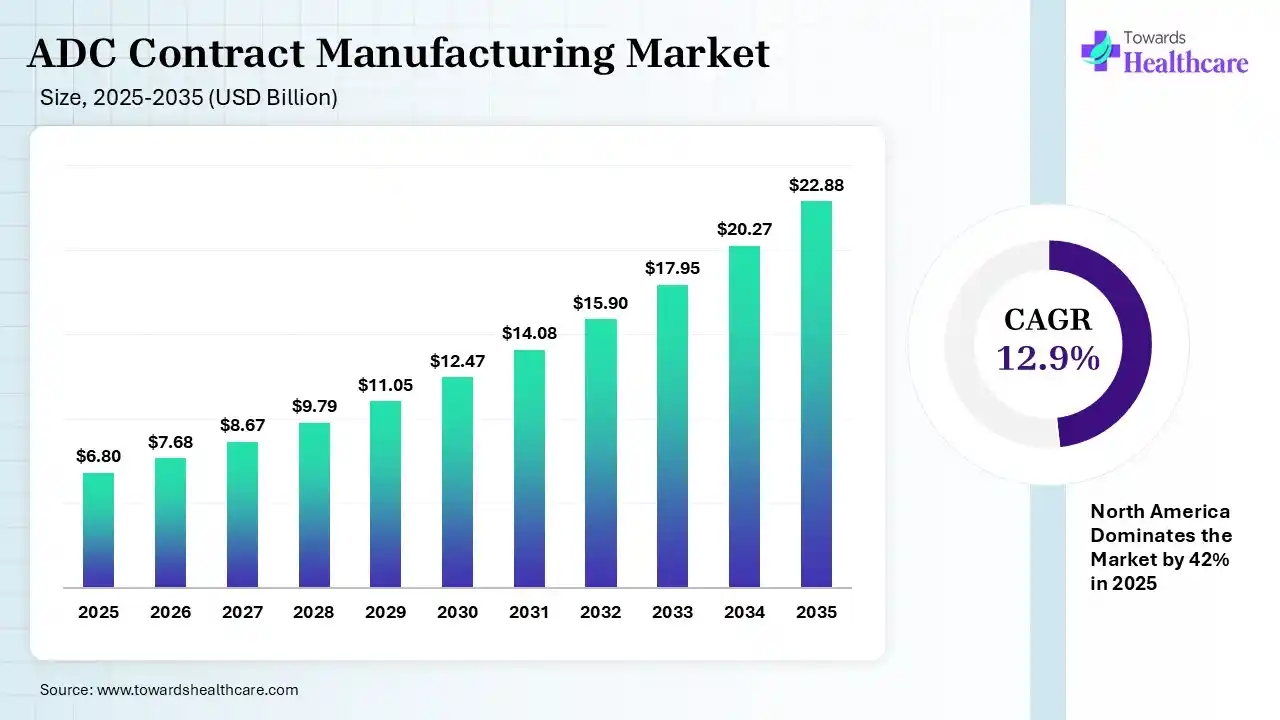

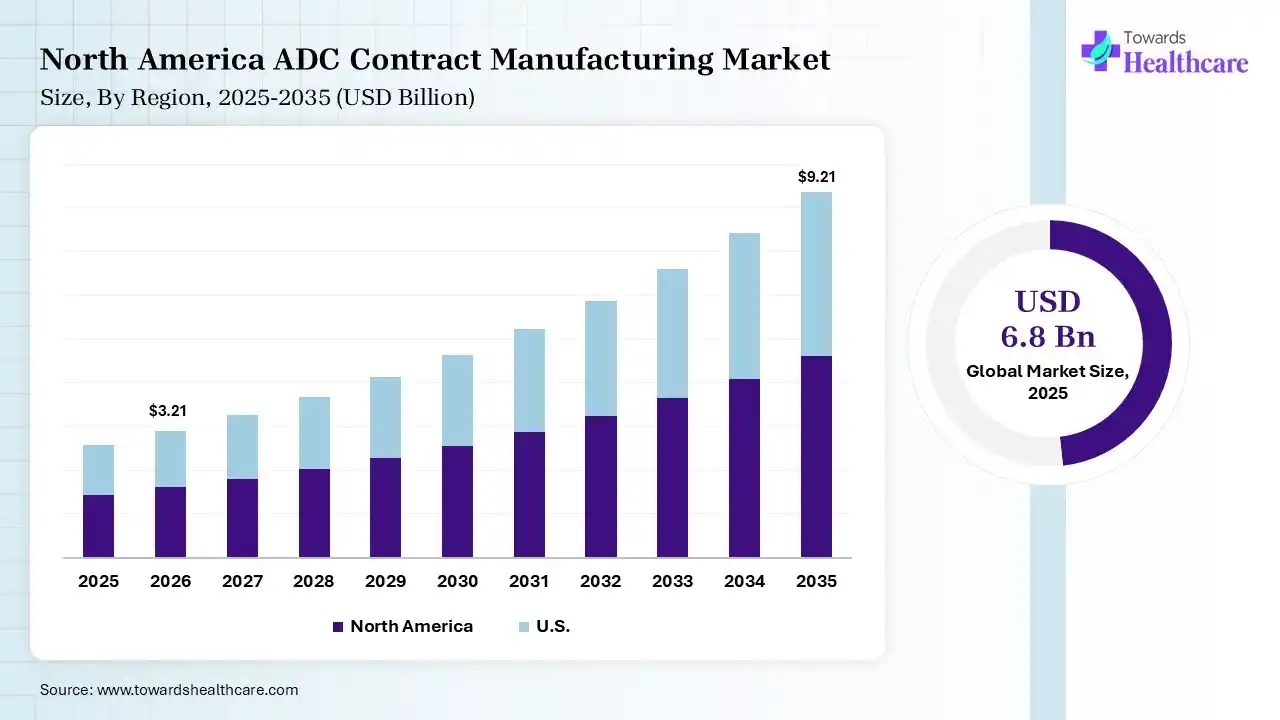

The global ADC contract manufacturing market size was estimated at USD 6.8 billion in 2025 and is predicted to increase from USD 7.68 billion in 2026 to approximately USD 22.88 billion by 2035, expanding at a CAGR of 12.9% from 2026 to 2035. The growing cancer burden globally is increasing the demand for ADC products, driving the adoption of ADC contract manufacturing. Growing R&D activities, funding, government support, outsourcing trends, technological advancements, and collaborations are enhancing the market growth.

The ADC contract manufacturing market is driven by growing technical complexity and extreme capital requirements. The ADC contract manufacturing refers to the antibody-drug conjugate outsourcing to the specialized third-party companies for their development and production. They offer various services such as ADC production, commercial manufacturing, quality testing, formulation optimization, management of cytotoxic payloads, and clinical trial support.

The ADC contract manufacturing market is growing as pharmaceutical companies increase investments in targeted cancer therapies and outsource complex production processes. Demand for specialized manufacturing, process development, and fill-finish services continues to rise. Manufacturers are expanding facilities, improving automation, and adopting advanced quality control systems to meet strict regulatory standards. Opportunities are increasing through partnerships between biotechnology firms and contract development and manufacturing organizations that accelerate product development and commercial production. Continuous innovation in linker technologies, monoclonal antibodies, and cytotoxic payloads is creating demand for highly skilled manufacturing partners. The competitive landscape includes global CDMOs, specialized biologics manufacturers, and regional companies focusing on capacity expansion, technology upgrades, strategic collaborations, and integrated services that support clients from early research through commercial manufacturing.

AI offers a wide range of applications in the market, including process optimization and predictive analytics, reducing the chances of product or batch failures. It also helps in maintaining a consistent drug antibody ratio, which also helps in detecting any anomalies, ensuring quality control. AI also helps in the development of personalized ADC products and offers automation, reducing the chances of human errors and accelerating product development.

Blooming Outsourcing Trends

A rise in the ADC drug pipeline is increasing the outsourcing trends, promoting the use of ADC contract manufacturing services. They are being preferred to avoid the use of expensive facilities and complex technologies and promote faster, higher-quality, and safety products development.

Rising Adoption of End-To-End Services

The lack of manufacturing capacities and skilled personnel is increasing the shift towards ADC contract manufacturing to leverage their end-to-end services. Their one-stop solution offering antibody production, conjugations, payload synthesis, and fill-finish solutions is also attracting the client.

Technological Advancements

Growing technological advancements are increasing the adoption of new technologies, driving collaborations with ADC contract manufacturing organizations. Their site-specific conjugation technologies, improved linker chemistry, and continuous and automated manufacturing are also increasing their demand.

| Table | Scope |

| Market Size in 2026 | USD 7.68 Billion |

| Projected Market Size in 2035 | USD 22.88 Billion |

| CAGR (2026 - 2035) | 12.9% |

| Leading Region | North America by 42% |

| Key Applications | Oncology drugs, targeted cancer therapies, HER2 ADCs, solid tumors, hematological cancers, clinical trial material manufacturing, commercial ADC production |

| Primary End Users | Pharmaceutical companies, biotechnology companies, oncology drug developers, research organizations |

| Key Challenges | Complex manufacturing processes, high capital investment requirements, regulatory complexity, payload toxicity handling, limited specialized capacity |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Payload Type, By Linker Type, By Conjugation Technology, By Scale of Operation, By End User, By Region |

| Top Key Players | Lonza Group, Axplora (Novasep), WuXi Biologics, MilliporeSigma (Merck KGaA), Samsung Biologics, Cambrex, Catalent, Inc., Sterling Pharma Solutions, Piramal Pharma Solutions, Abzena |

")

| Segment | Share 2025 (%) |

| Process Development | 28% |

| Analytical & QC Services | 22% |

| cGMP Manufacturing | 32% |

| Fill-Finish Services | 10% |

| Packaging & Labeling | 8% |

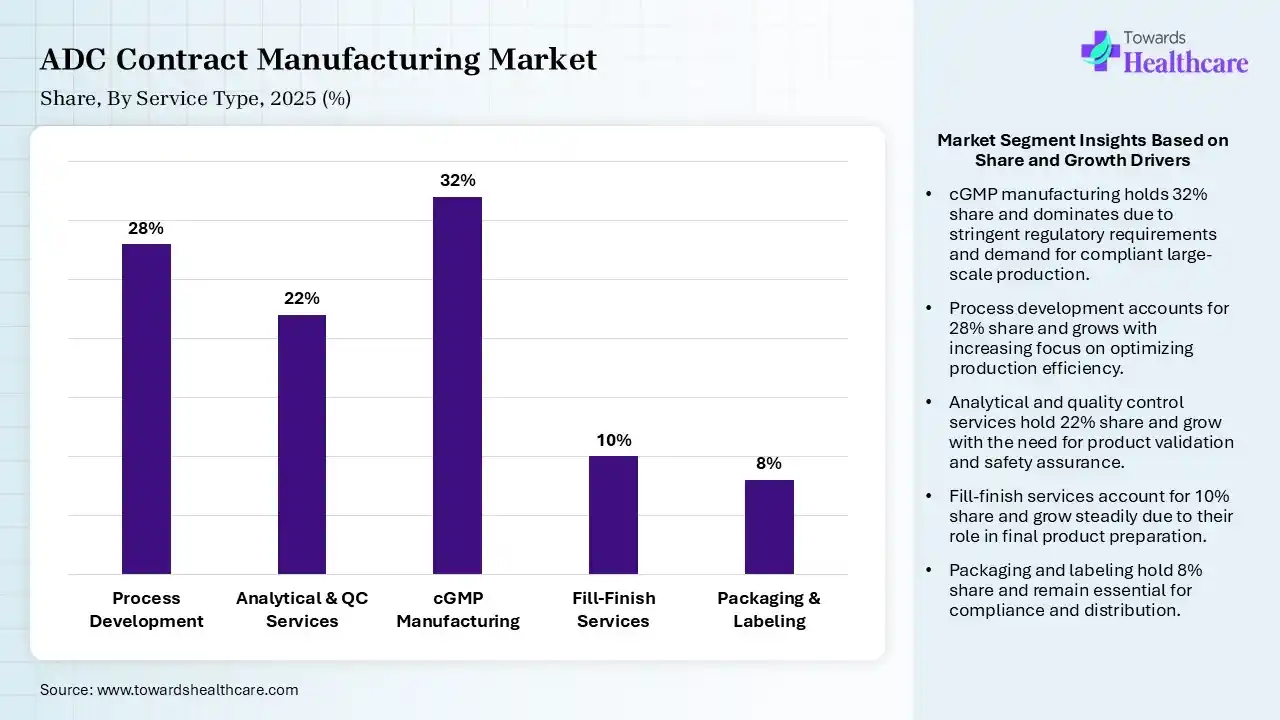

The cGMP Manufacturing Segment Dominated the Market With 32% in 2025

The cGMP manufacturing segment accounted for the highest revenue share of 32% of the ADC contract manufacturing market in 2025, due to a rise in the large-scale ADC production demand driven by growth in their approvals. High-capital facilities also pushed outsourcing to CDMOs. Growth in the commercialization pipelines also increased their demand.

The process development segment held the second-largest share of 28% of the market in 2025 and is expected to show the highest growth during the forecast period, due to the increasing complexity of ADC design, which drives demand for optimized processes. They are also used for early-stage outsourcing to boost innovation efficiency. Rising pipeline also fuels development contracts, increasing their use.

The analytical & quality control services segment held 22% of the ADC contract manufacturing market share in 2025, and is expected to grow at the fastest CAGR during the forecast period, driven by regulatory scrutiny, which increases the need for robust analytical validation, driving their adoption rates. Complex ADC characterization is also expanding testing demand. Biopharma outsourcing also accelerates QC services.

The fill-finish services segment held 10% of the market share in 2025, due to a rise in the sterile handling requirements, which boost specialized fill-finish demand. Growth in injectable oncology drugs also increases their utilization. Expansion of biologics packaging capacity is also supporting their growth.

")

| Segment | Share 2025 (%) |

| Cytotoxic Payloads | 46% |

| DNA Damaging Agents | 24% |

| Topoisomerase Inhibitors | 20% |

| Others | 10% |

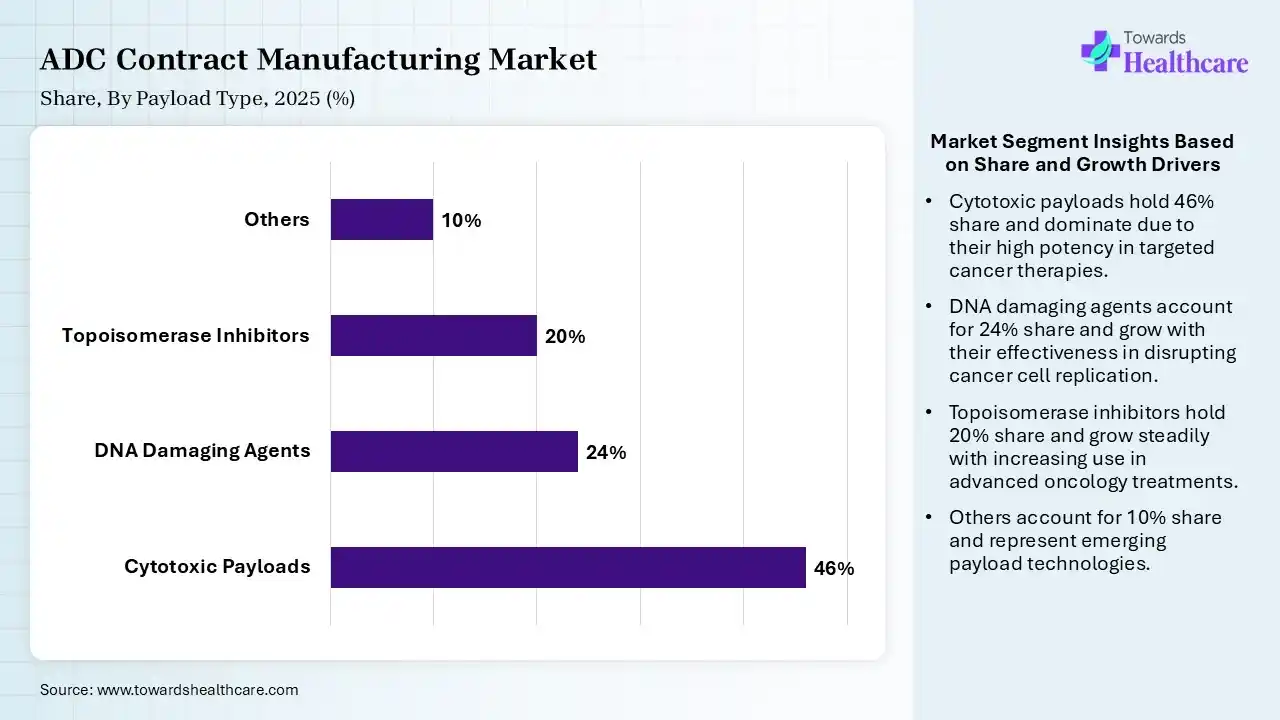

The Cytotoxic Payloads Segment Dominated the Market With 46% in 2025

The cytotoxic payloads segment held a major revenue share of 46% of the ADC contract manufacturing market in 2025, due to established clinical success, which contributed to their continued adoption. A strong pipeline of MMAE-based ADCs also increased the demand for cytotoxic payloads. Proven efficacy also ensured commercial dominance.

The DNA-damaging agents segment held the second-largest share of 24% of the market in 2025 and is expected to expand rapidly during the forecast period, due to their superior potency driving next-gen ADC development. Increased investment in PBD-based payloads also supports their use. Rising focus on targeted cancer therapies is also increasing their demand.

The topoisomerase inhibitors segment held 20% of the ADC contract manufacturing market share in 2025, due to expanding approvals, which are increasing their manufacturing demand. Their improved safety profiles are also promoting their adoption. Strong pipeline growth is also supporting segment expansion.

The others segment held 10% of the market share in 2025, due to growing innovation in novel payloads, which diversifies applications. A rise in the early-stage research also drives niche demand. Emerging technologies are also expanding their opportunities.

")

| Segment | Share 2025 (%) |

| Cleavable Linkers | 62% |

| Non-cleavable Linkers | 38% |

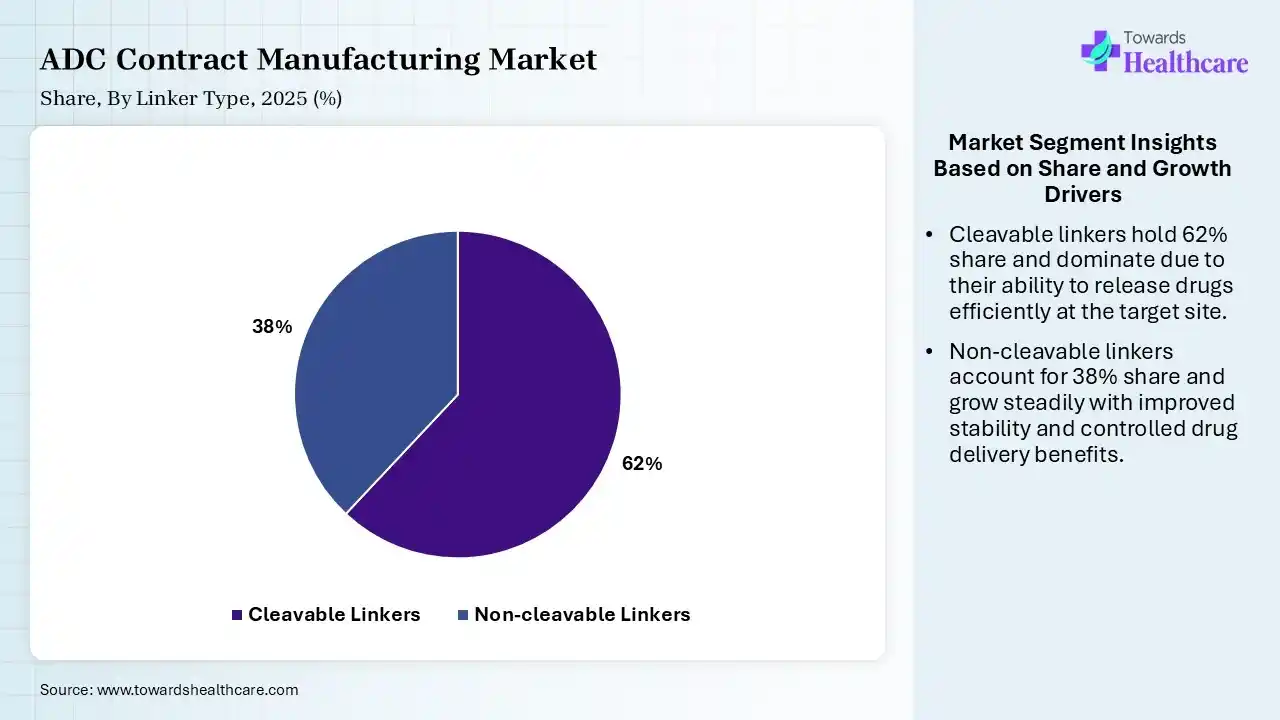

The Cleavable Linkers Segment Dominated the Market With 62% in 2025

The cleavable linkers segment held the largest revenue share of 62% of the ADC contract manufacturing market in 2025 and is expected to grow with the highest CAGR during the forecast period, due to enhanced tumor-specific drug release, which increased their adoption. Advances in linker chemistry improved their efficacy, which enhanced their use. Strong pipeline preference for cleavable systems also increased their use.

The non-cleavable linkers segment held the second-largest share of 38% of the market in 2025, driven by improved stability, which supports their continued usage. Established ADC products rely on non-cleavable systems, fueling their demand. Lower toxicity profiles also sustain their demand.

")

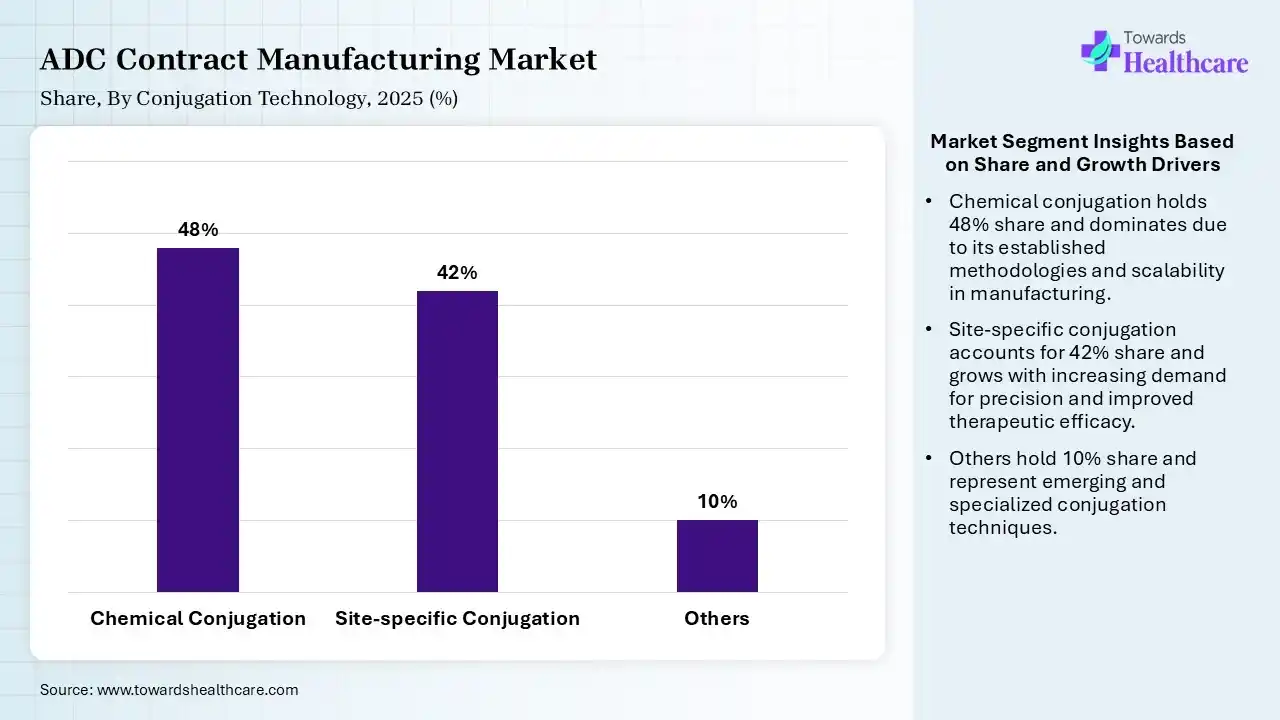

| Segment | Share 2025 (%) |

| Chemical Conjugation | 48% |

| Site-specific Conjugation | 42% |

| Others | 10% |

The Chemical Conjugation Segment Dominated the Market With 48% in 2025

The chemical conjugation segment contributed the biggest revenue share of 48% of the ADC contract manufacturing market in 2025, due to its widespread adoption driven by established protocols. Cost-effective manufacturing also increased their preference. The presence of legacy ADCs also maintained the segment strength.

The site-specific conjugation segment held the second-largest share of 42% of the market in 2025 and is expected to gain the highest share during the forecast period, driven by precision targeting that improves therapeutic index. Growing adoption of engineered antibodies is also increasing their demand. Innovation enhances product consistency, driving its adoption.

The others segment held 10% of the ADC contract manufacturing market share in 2025, due to emerging technologies that are supporting niche applications. Ongoing R&D activities also drive innovation, promoting their adoption. The growing development of new ADC products and focus on enhancing their efficacy, safety, and stability are also increasing their use.

")

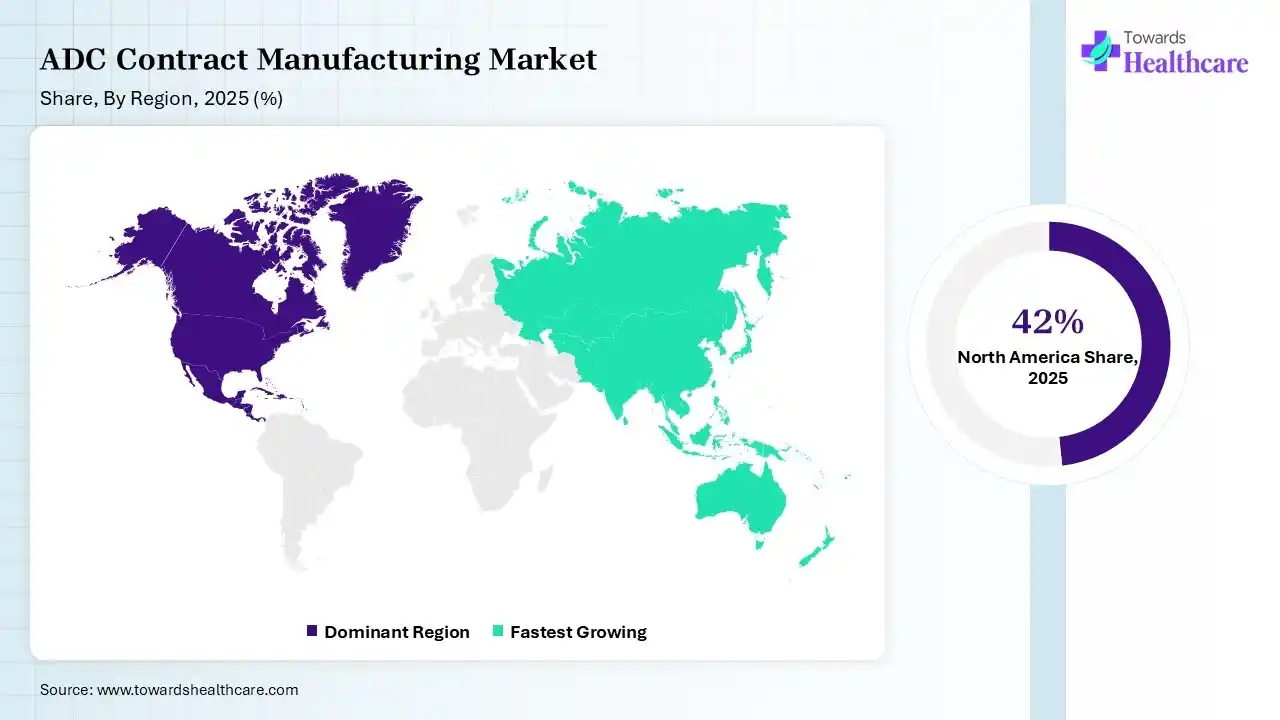

North America dominated the ADC contract manufacturing market with 42% in 2025, due to the strong presence of leading CDMOs and pharma firms. The presence of an advanced regulatory framework and a rise in the oncology drug demand also supported the growth of ADC contract manufacturing. Growth in funding, outsourcing trends, and advanced technology adoption also contributed to the market growth.

U.S. Market Trends

The presence of the largest ADC pipeline globally in the U.S. is driving the demand for ADC contract manufacturing. Strong CDMO presence enhances capacity, where high biologics spending also fuels growth. Growing outsourcing trends and R&D investments are also increasing their adoption rates.

Canada Market Trends

Canada is strengthening its position in the ADC contract manufacturing market through investments in biologics production and pharmaceutical research. The country offers strong academic support and government funding for life sciences innovation. Several manufacturers are expanding specialized production capabilities for complex biologics. Growing collaborations between biotechnology companies and contract manufacturers create new business opportunities. Canada's skilled workforce and high regulatory standards continue attracting global pharmaceutical companies seeking reliable manufacturing partners.

Mexico Market Trends

Mexico is gradually expanding its ADC contract manufacturing market with growing investments in pharmaceutical production and healthcare infrastructure. International companies are exploring manufacturing partnerships because of competitive operating costs and improved industrial capabilities. Government efforts to strengthen the life sciences sector also support market development. Local manufacturers are upgrading facilities and quality systems. These improvements help Mexico attract outsourcing projects from pharmaceutical companies serving North American and Latin American markets.

Asia Pacific held 22% share of the ADC contract manufacturing market in 2025 and is expected to grow at the fastest CAGR during the forecast period, due to the rapid expansion of CDMO capabilities, which is driving the ADC contract manufacturing. Cost advantages are also attracting global outsourcing, promoting their use. A growing biotech ecosystem, increasing investments, and growing clinical trials are also accelerating their demand, enhancing the market growth.

China Market Trends

Rapid CDMO expansion and growing GMP infrastructure are boosting global outsourcing in China, increasing the demand for ADC contract manufacturing services. Strong government support and an increasing domestic ADC pipeline are accelerating their growth. Growing biotech investments and expanding clinical trials are also increasing their demand.

India Market Trends

India is becoming an important destination for ADC contract manufacturing because of its strong pharmaceutical industry and cost-efficient production capabilities. Domestic companies are investing in advanced biologics manufacturing facilities and skilled talent. Increasing research activities and partnerships with global pharmaceutical firms support market expansion. Regulatory improvements and growing expertise in complex drug manufacturing create additional opportunities. India continues attracting international companies seeking high-quality and scalable contract manufacturing services.

Japan Market Trends

Japan plays an important role in the ADC contract manufacturing market through its advanced pharmaceutical industry and strong focus on innovation. Companies invest in modern manufacturing technologies and high-quality production standards for complex biologics. Collaboration between domestic manufacturers and global biotechnology firms continues to increase. The country's experienced workforce and well-established regulatory framework support reliable manufacturing. Japan remains a preferred location for specialized and precision-focused ADC production services.

| Category | Market Participants | Role in ADC Contract Manufacturing |

| Technology Providers | Bioconjugation technology companies, linker-payload specialists, analytical technology providers | Provide conjugation platforms, payload chemistry, characterization technologies |

| Product Manufacturers | ADC developers and pharmaceutical companies | Develop ADC therapeutics and outsource manufacturing |

| Service Providers | CDMOs/CMOs | Provide ADC development, GMP manufacturing, fill-finish, analytical services |

| Platform Providers | Integrated CDMO platforms | Offer end-to-end ADC manufacturing from antibody to final drug product |

| CROs/CDMOs | Lonza, WuXi XDC, Catalent, Piramal Pharma Solutions, AGC Biologics | Support clinical and commercial ADC production |

| Software Vendors | Manufacturing execution systems, quality management platforms | Support GMP operations, documentation, and regulatory compliance |

| Research Institutions | Oncology research centers, biotechnology institutes | Support ADC discovery and translational research |

| End-User Industries | Pharmaceutical, biotechnology, oncology therapeutics companies | Outsource ADC production to accelerate development timelines |

R&D

Formulation and Final Dosage Preparation

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 55% | 30% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza Group | Basel, Switzerland | Switzerland | One of the leading global CDMOs with integrated ADC development and manufacturing capabilities | ADC bioconjugation, payload handling, GMP manufacturing, drug product services |

| WuXi AppTec | Shanghai, China | China | Major global CRDMO with integrated ADC and bioconjugate manufacturing through WuXi XDC | ADC development, linker-payload, conjugation, drug substance and product manufacturing |

| Catalent | Somerset, New Jersey, USA | United States | Large CDMO supporting complex biologics and ADC programs | ADC conjugation, analytical testing, sterile fill-finish |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Piramal Pharma Solutions | Mumbai, Maharashtra, India | India | Specialized CDMO with dedicated ADC development and manufacturing solutions | ADC drug substance, drug product manufacturing, ADCelerate platform |

| AGC Biologics | Tokyo, Japan | Japan | Global biologics CDMO supporting complex biologics manufacturing | Biologics manufacturing, conjugation support |

| Boehringer Ingelheim BioXcellence | Ingelheim am Rhein, Germany | Germany | Established biologics CDMO supporting advanced therapies | Biologics production, process development |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Abzena | San Diego, California, USA | United States | Specialist in antibody engineering and ADC technologies | ThioBridge ADC conjugation technology |

| Axplora | Raubling, Germany | Germany | Provides complex pharmaceutical manufacturing including ADC-related services | Linker-payload manufacturing, conjugation support |

| Sterling Pharma Solutions | Cramlington, England, UK | United Kingdom | Specialized CDMO with high-potency and ADC capabilities | ADC development, HPAPI manufacturing |

Strengths

Weaknesses

Opportunities

Threats

Dr. Campbell Bunce, Chief Scientific Officer, Abzena: At Abzena, we are lucky to work with so many exciting next-generation molecules. We’re seeing three trending areas. One is technology developments, particularly conjugation technologies that support site-directed conjugation, allowing better control of the DAR, improved stability, and increased yield. Abzena has its own proprietary conjugation platform called ThioBridge®, which, alongside other platforms, opens up the potential for different cargoes to reach distinct disease indications. We have learned a lot from classical ADCs that have allowed us to understand where the limitations are and areas of improvement, leading to the development of new conjugation and linker technologies supporting more options for the development of optimized ADCs.

By Service Type

By Payload Type

By Linker Type

By Conjugation Technology

By Scale of Operation

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar