Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

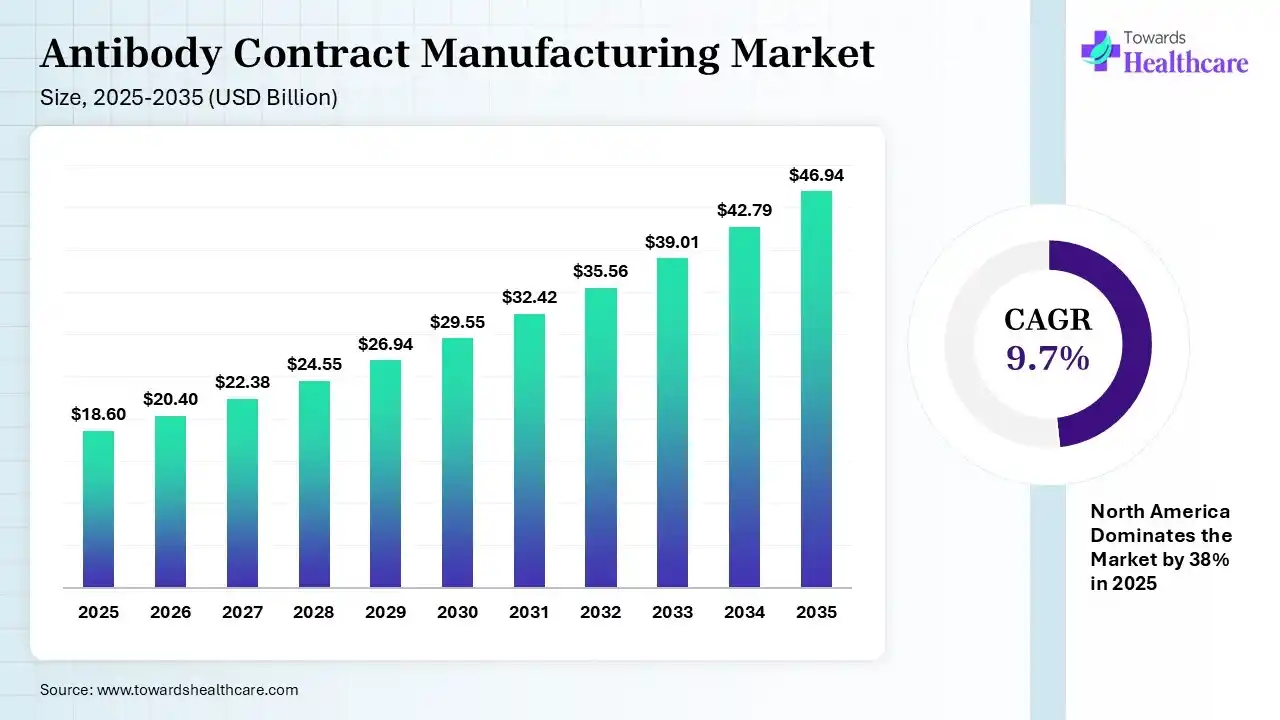

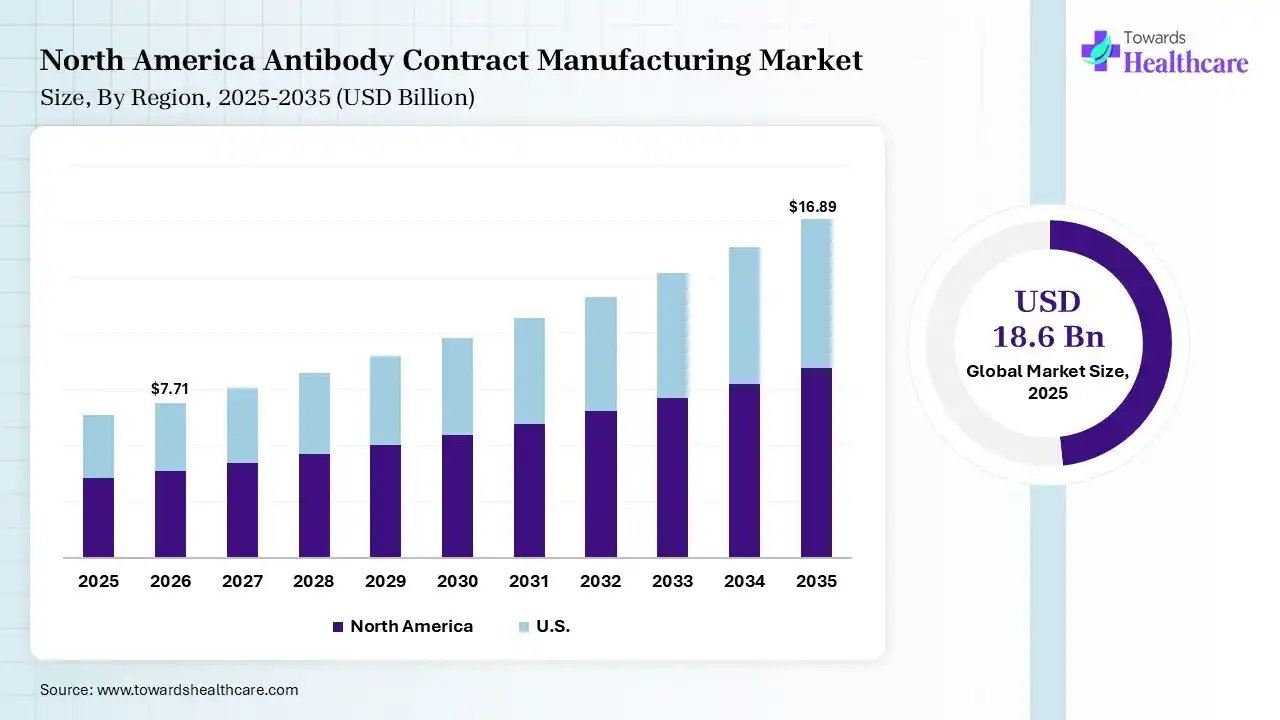

The global antibody contract manufacturing market size was estimated at USD 18.6 billion in 2025 and is predicted to increase from USD 20.4 billion in 2026 to approximately USD 46.94 billion by 2035, expanding at a CAGR of 9.7% from 2026 to 2035. A rise in the chronic disease burden globally is increasing the demand for antibody contract manufacturing services. Growing R&D activities, healthcare investments, advancements in biosimilars, strategic partnerships, technological innovations, and new platform launches are also enhancing the market growth.

")

The antibody contract manufacturing market is driven by increasing outsourcing trends and a surge in the demand for biologics. The antibody contract manufacturing refers to the outsourcing of therapeutic antibodies to specialized third-party companies for their production. They are preferred for large-scale production and faster drug development due to their affordable services, quality assurance, expertise, and regulatory support.

The antibody contract manufacturing market is expanding rapidly due to the surging global demand for targeted therapeutics. Pharmaceutical developers increasingly rely on contract manufacturing organizations to manage complex production scales and minimize high capital expenditures. Technical trends highlight a significant shift toward automated single-use bioreactors, which accelerate validation timelines and reduce contamination risks. This technological evolution allows contract facilities to pivot quickly between distinct batches while maintaining strict regulatory compliance across global drug development centers.

Strategic opportunities exist in expanding mammalian cell culture capacities and developing novel bispecific antibody production platforms. The global competitive landscape features a mix of established contract manufacturing giants and specialized niche companies focused on rapid geographical expansion. Advanced clinical pipelines for aggressive oncology and rare autoimmune diseases drive continuous outsourcing activities worldwide. Consequently, dedicated service providers are heavily investing in cutting-edge purification technologies to ensure absolute product consistency and meet stringent international drug safety standards.

AI offers process optimization, improving production efficiency and predictive maintenance, reducing the chances of errors, and increasing its adoption in antibody contract manufacturing. It also helps in monitoring process deviation and data analysis, ensuring quality control, and consistent yield of the products. AI also helps in accelerating the antibody manufacturing, workflow automation, and real-time monitoring, which increases their adoption.

Biologics on Rise

The growth in the demand for biologics is increasing the adoption of antibody contract manufacturing services to develop products with high specificity and effectiveness. This increases the use of monoclonal antibodies to drive the development of new biologics for a wide range of disease treatment.

Blooming Advanced Antibody Modalities

The growing R&D activities and collaborations are increasing the development of next-generation antibody-based products, driving the demand for antibody contract manufacturing services. This is increasing the development of antibody-drug conjugates and fragment-based antibodies, creating new opportunities.

Shift Towards Personalized Medicines

A rise in health awareness is driving the demand for patient-specific antibody therapies. This, in turn, is increasing the use of antibody contract manufacturing services for small batch production and flexible manufacturing systems.

| Table | Scope |

| Market Size in 2026 | USD 20.4 Billion |

| Projected Market Size in 2035 | USD 46.94 Billion |

| CAGR (2026 - 2035) | 9.7% |

| Leading Region | North America by 38% |

| Key Applications | Monoclonal antibodies, oncology biologics, autoimmune therapies, infectious disease antibodies, antibody-drug conjugates (ADCs), biosimilars, immunotherapies |

| Primary End Users | Biopharmaceutical companies, biotech startups, pharmaceutical companies, research organizations, specialty therapeutics developers |

| Key Challenges | High manufacturing complexity, regulatory compliance requirements, long development timelines, capacity constraints, technology transfer risks, expensive biologics production infrastructure |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Antibody Type, By Expression System, By Scale of Operation, By End User, By Application, By Region |

| Top Key Players | Lonza Group, Samsung Biologics, FUJIFILM Diosynth Biotechnologies, WuXi Biologics, Siegfried Holding, Thermo Fisher Scientific (Patheon), AGC Biologics, Catalent, Inc, Merck KGaA (MilliporeSigma), Boehringer Ingelheim (BioXcellence) |

")

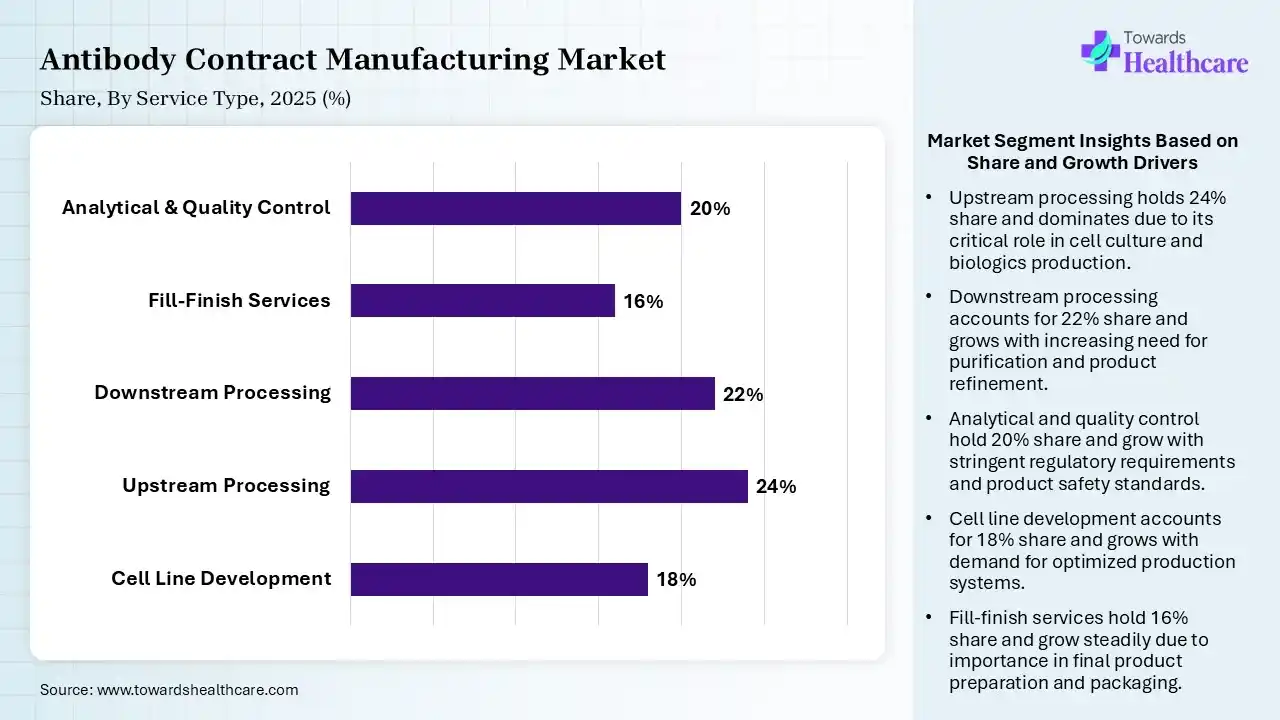

| Segment | Share 2025 (%) |

| Cell Line Development | 18% |

| Upstream Processing | 24% |

| Downstream Processing | 22% |

| Fill-Finish Services | 16% |

| Analytical & Quality Control | 20% |

The Upstream Processing Segment Dominated the Market With 24% in 2025

The upstream processing segment led the antibody contract manufacturing market with 24% share in 2025, due to a growth in the biologics pipeline, which increased the large-scale cell culture needs. Continuous bioprocessing improves efficiency, which also increases the use of antibody contract manufacturing services. Expansion of the CDMOs' investments in bioreactor capacity also increased their adoption.

The downstream processing segment held the second-largest share of 22% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 10.4% during the forecast period, due to the complexity of antibody purification, which drives their demand. High purity standards require advanced chromatography solutions, which promote their use. Automation enhances scalability and consistency, driving their adoption.

The analytical & quality control segment held 20% of the antibody contract manufacturing market share in 2025, due to stringent regulatory requirements driving analytical testing demand. They are also being used in stability studies to ensure product safety. Increasing biosimilar development boosts QC services, increasing their use.

The cell line development segment held 18% of the market share in 2025, due to increasing demand for high-yield cell lines, which drives their outsourcing. Companies seek stable and scalable production platforms, increasing the use of antibody contract manufacturing services. The presence of advanced genetic engineering also accelerates adoption.

")

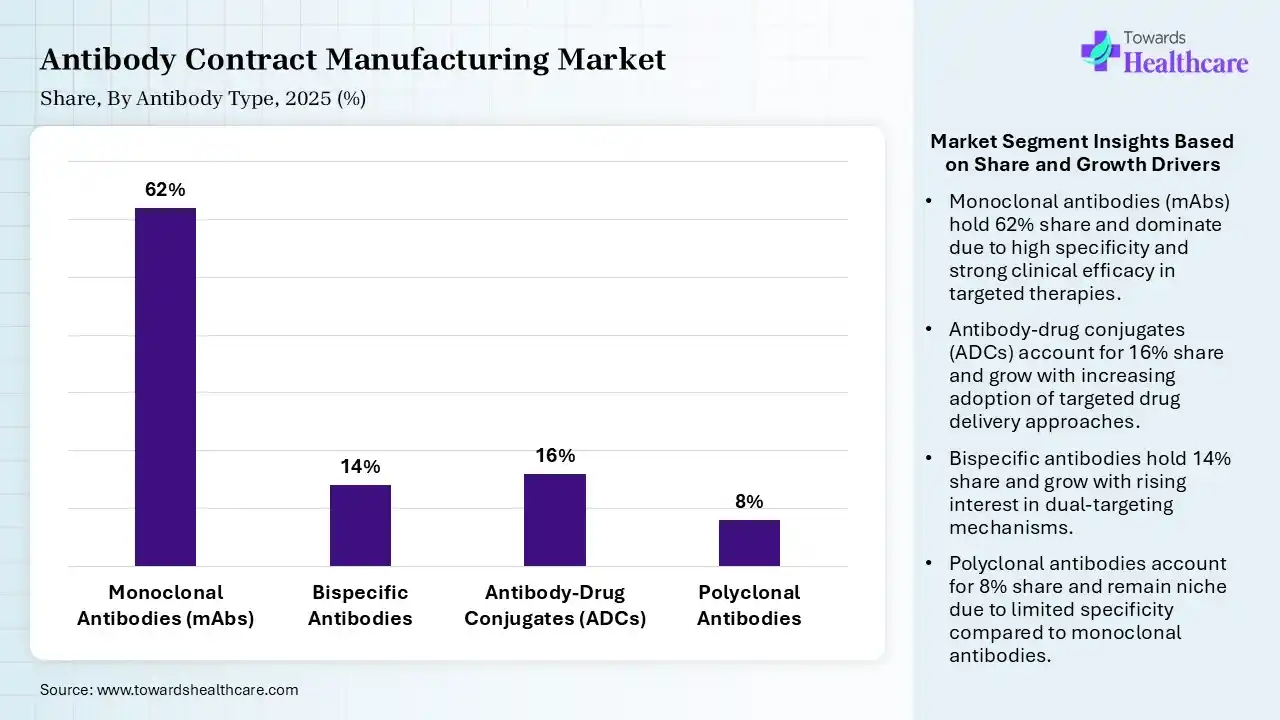

| Segment | Share 2025 (%) |

| Monoclonal Antibodies (mAbs) | 62% |

| Bispecific Antibodies | 14% |

| Antibody-Drug Conjugates (ADCs) | 16% |

| Polyclonal Antibodies | 8% |

The Monoclonal Antibodies (mAbs) Segment Dominated the Market With 62% in 2025

The monoclonal antibodies (mAbs) segment accounted for the highest revenue share of 62% of the antibody contract manufacturing market in 2025, due to a strong pipeline of approved biologics, which sustained their demand. Their wide use in oncology and immunology has also increased their use. Continuous innovation to enhance their therapeutic efficacy also contributed to their advancements.

The antibody-drug conjugates (ADCs) segment held the second-largest share of 16% of the market in 2025, due to their increasing oncology applications, fueling their demand. Advanced linker technologies improve efficacy, which drives their adoption. Manufacturing complexity favors CDMOs, promoting a rise in their use.

The bispecific antibodies segment held 14% of the antibody contract manufacturing market share in 2025 and is expected to show the highest growth with a CAGR of 11.2% during the forecast period, due to rising interest in dual-target therapies, which drives their adoption. Clinical success increases investment, which boosts their advancements. Complex manufacturing also increases outsourcing needs.

The polyclonal antibodies segment held 8% of the market share in 2025, due to their niche applications, sustaining moderate demand. They are also being used in diagnostics and research settings. Their strong binding affinity and detection of complex antigens are also increasing their use.

")

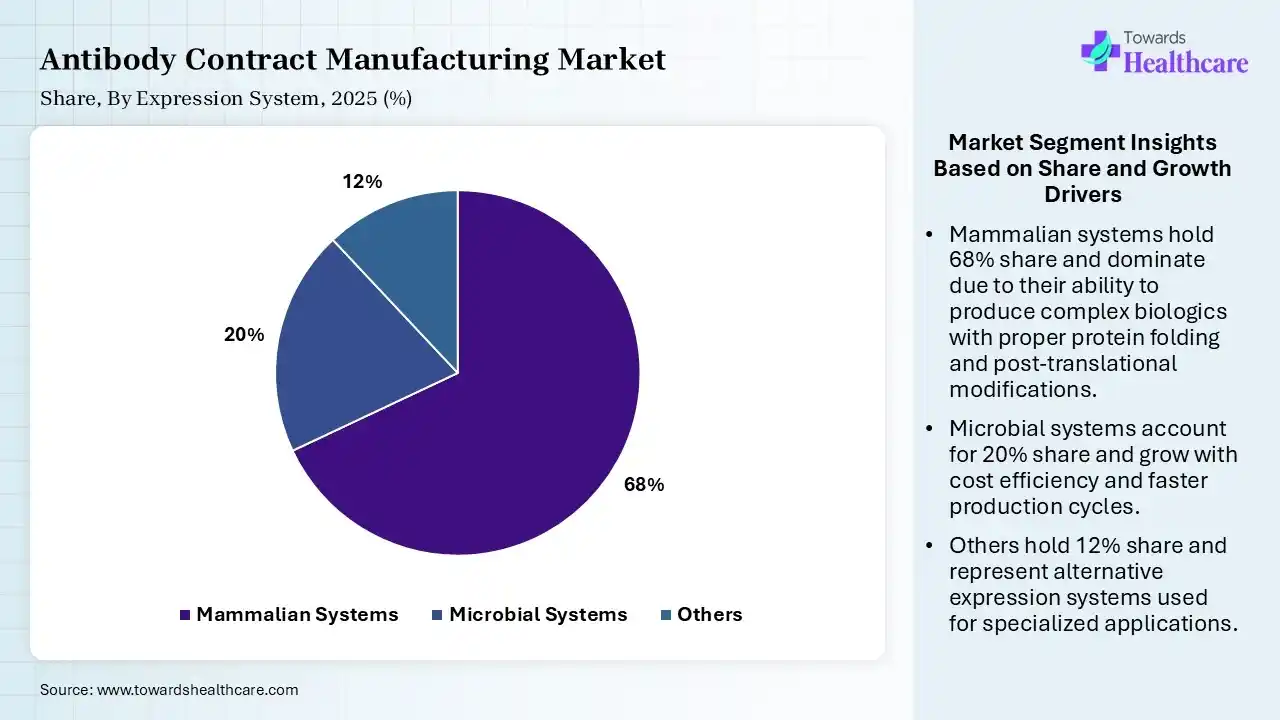

| Segment | Share 2025 (%) |

| Mammalian Systems | 68% |

| Microbial Systems | 20% |

| Others | 12% |

The Mammalian Systems Segment Dominated the Market With 68% in 2025

The mammalian systems segment held a major revenue share of 68% of the antibody contract manufacturing market in 2025, due to their increased preference for complex protein expression. High product quality and regulatory acceptance also increased their adoption rates. Advances in CHO cell engineering, boosting productivity also increased their use.

The microbial systems segment held the second-largest share of 20% of the market in 2025, due to their cost-effective production, which supports early-stage research. Faster growth cycles improve turnaround time, promoting their use. Simple production and high yield potential also drive their demand.

The others segment held 12% of the antibody contract manufacturing market share in 2025 and is expected to expand rapidly with a CAGR of 10.7% during the forecast period, due to a rise in emerging systems like insect and plant cells. Lower production costs are also attracting innovators. Additionally, they are suitable for specialized antibody formats, which drives their adoption.

")

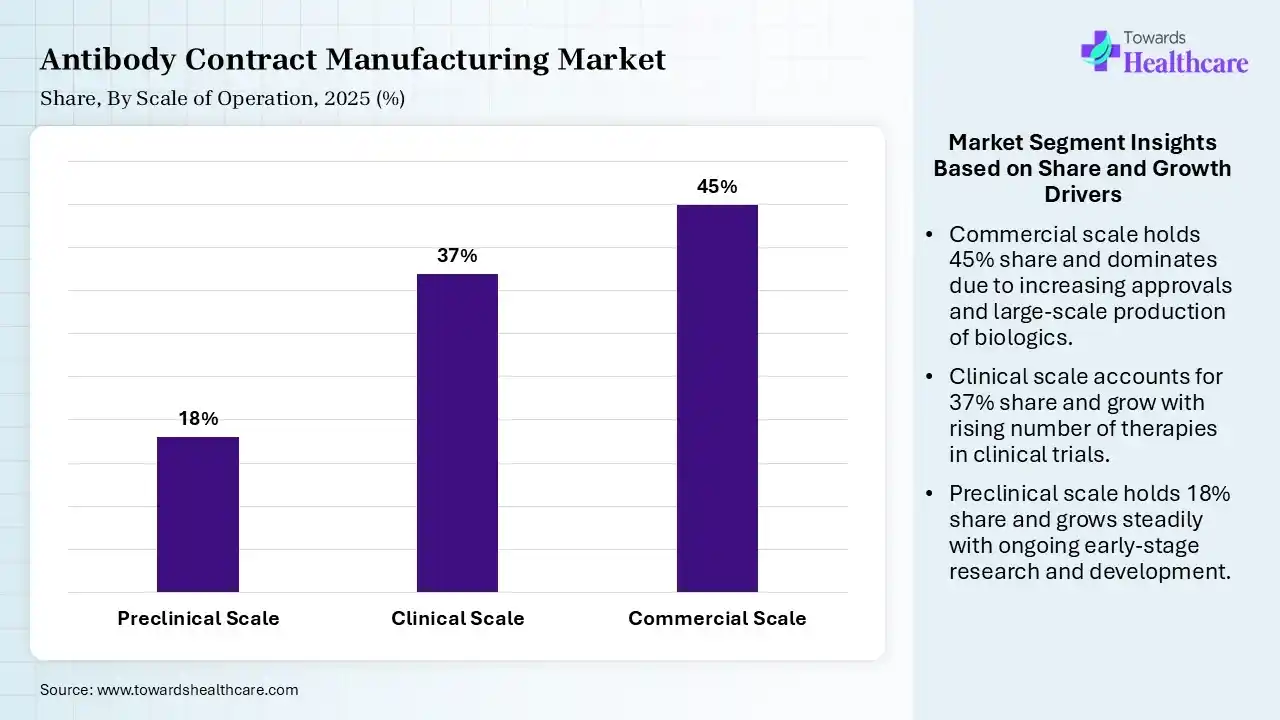

| Segment | Share 2025 (%) |

| Preclinical Scale | 18% |

| Clinical Scale | 37% |

| Commercial Scale | 45% |

The Commercial Scale Segment Dominated the Market With 45% in 2025

The commercial scale segment contributed the biggest revenue share of 45% of the antibody contract manufacturing market in 2025 and is expected to gain the highest share with a CAGR of 10.5% during the forecast period, driven by a growth in biologics approvals, which increased the demand for large-scale production. Capacity constraints also contributed to the outsourcing of the products. Long-term manufacturing contracts also supported their growth.

The clinical scale segment held the second-largest share of 37% of the market in 2025, due to growing clinical trials, which increase the production demand. Flexible manufacturing also supports multiple phases, promoting their use. Regulatory approvals accelerate scale-up needs, fueling their demand.

The preclinical scale segment held 18% of the antibody contract manufacturing market share in 2025, driven by growing early-stage R&D activities, which drive their demand. Small batch production also supports the demand for screening technologies. Increasing biotech startups also boost their usage.

")

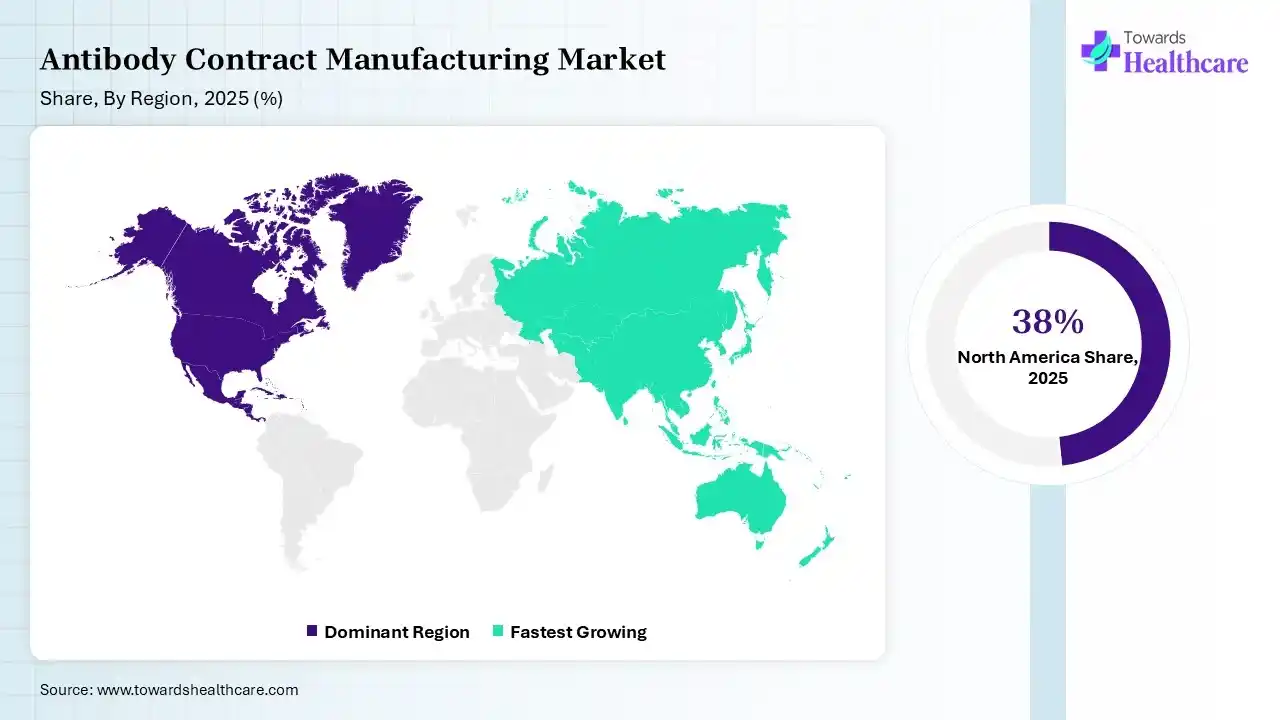

North America dominated the antibody contract manufacturing market with 38% in 2025, due to strong biopharma presence, which increased the demand for antibody contract manufacturing services. Advanced manufacturing infrastructure also supported their growth. High R&D investment also accelerated their innovation, which contributed to the market growth.

U.S. Market Trends

The large biologics market supporting outsourcing trends across the U.S. is increasing the use of antibody contract manufacturing services. The presence of leading CDMOs, biotech industries, and pharmaceutical companies is also driving their growth. The presence of a robust regulatory framework also increases their use to ensure quality standards.

Canada Market Trends

Canada is establishing itself as a specialized hub for early-stage antibody production. The country possesses advanced research laboratories and highly skilled bioprocess engineers. Domestic firms choose to outsource clinical-phase batches to avoid heavy capital investments in operational manufacturing infrastructure. Government tax incentives for scientific research further attract foreign biotech companies to the region. Consequently, local contract facilities are expanding small-scale mammalian cell culture capabilities to support rapid therapeutic discoveries daily.

Mexico Market Trends

Mexico is emerging as a cost-effective nearshoring destination for antibody manufacturing. Its close geographical proximity to major North American pharmaceutical hubs provides significant logistical advantages for developers. Local service providers are upgrading facilities to comply with international regulatory standards. Increased investment in bioprocessing infrastructure helps domestic contract firms secure mid-scale production agreements. Furthermore, lower operational costs make the country highly attractive for international companies seeking flexible contract outsourcing solutions now.

Asia Pacific held 23% share of the antibody contract manufacturing market in 2025 and is expected to grow at the fastest CAGR of 11.2% during the forecast period, due to cost advantages that attract outsourcing. Expanding manufacturing capacity also supports antibody contract manufacturing growth. Rising biotech investments also accelerate their demand, enhancing the market growth.

China Market Trends

Rapid expansion of CDMO capabilities across China drives the growth of antibody contract manufacturing services. Increasing government support and demand for biologics also drive their adoption. Expanding biotech companies, clinical trials, and outsourcing trends are also increasing their use.

India Market Trends

India is rapidly expanding its commercial footprint in the antibody contract manufacturing sector. The nation offers substantial cost advantages alongside a vast pool of technical bioprocess professionals. Major domestic contract firms are investing heavily in large-scale bioreactor facilities to meet rising international demand. Stringent regulatory approvals from global health agencies have boosted trust in Indian manufacturing quality. This robust infrastructure development successfully positions the country as a primary global destination.

Japan Market Trends

Japan is prioritizing advanced technological integration within its domestic antibody contract manufacturing facilities. The market is defined by strict quality control standards and highly sophisticated automation systems. Japanese contract firms are adopting automated continuous processing to maximize yield and lower overall operational costs. Strong collaboration between local pharmaceutical corporations and contract organizations drives steady market volume. Service providers continually expand their advanced mammalian lines to handle highly complex antibody therapies.

| Ecosystem Category | Key Participants / Explanation |

| Technology Providers | Companies providing cell line development, expression systems, bioreactors, purification technologies, analytical platforms, and biologics manufacturing technologies |

| Product Manufacturers | Pharmaceutical and biotech companies developing antibody therapeutics that outsource manufacturing activities |

| Service Providers | CDMOs offering antibody development, process optimization, GMP manufacturing, testing, and commercialization support |

| Platform Providers | Companies offering integrated biologics development platforms, mammalian expression systems, automation, and manufacturing platforms |

| CROs/CDMOs | Specialized organizations providing antibody discovery, development, clinical manufacturing, and commercial-scale production |

| Software Vendors | Digital manufacturing, laboratory information management, quality management, and biologics process optimization platforms |

| Research Institutions | Universities and biotechnology research centers supporting antibody discovery and innovation |

| End-User Industries | Pharmaceutical, biotechnology, oncology, immunology, rare disease, and vaccine industries |

R&D

Formulation and Final Dosage Preparation

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 60% | 28% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza Group | Basel, Switzerland | Switzerland | One of the largest global biologics CDMOs with extensive antibody manufacturing capabilities and commercial-scale operations | Mammalian biologics manufacturing, monoclonal antibody development, cell line development, GMP production |

| Samsung Biologics | Incheon, South Korea | South Korea | Major global antibody manufacturing CDMO with large-scale production capacity and global pharma partnerships | Antibody drug substance manufacturing, cell line development, fill-finish services |

| Catalent | Somerset, New Jersey, USA | United States | Leading biologics outsourcing provider supporting antibody development and manufacturing | Biologics manufacturing, formulation, analytical services, fill-finish |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| WuXi Biologics | Wuxi, Jiangsu, China | China | Large-scale biologics CDMO with strong antibody manufacturing capabilities and global customer base | Antibody discovery, development, clinical and commercial manufacturing |

| Boehringer Ingelheim BioXcellence | Ingelheim am Rhein, Germany | Germany | Established biologics manufacturing provider supporting antibody therapeutics | Mammalian cell culture, antibody manufacturing, process development |

| Rentschler Biopharma | Laupheim, Germany | Germany | Specialized biologics CDMO focused on complex biologics including antibodies | Antibody development, GMP manufacturing, analytical services |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| KBI Biopharma | Durham, North Carolina, USA | United States | Specialized biologics CDMO supporting antibody programs from development to manufacturing | Antibody process development, GMP manufacturing |

| Vetter Pharma | Ravensburg, Germany | Germany | Provides biologics manufacturing and fill-finish capabilities for antibody products | Sterile fill-finish, injectable biologics manufacturing |

| Biosynth | Staad, Switzerland | Switzerland | Provides specialized biologics and research manufacturing services | Antibody-related research materials and custom biologics services |

Strengths

Weaknesses

Opportunities

Threats

In July 2026, Dr. Jingsong Wang, Chairman of Nona Biosciences, commented: "This partnership validates Nona's platform and strategic focus in next-generation delivery technologies. Lonza's global reach, regulatory expertise, and commercial manufacturing capabilities will help accelerate the advancement of our BBB-crossing technology. Beyond technology development, the collaboration creates opportunities for licensing, commercialization, and long-term value creation, while strengthening our position in the CNS delivery space and supporting better outcomes for patients."

By Service Type

By Antibody Type

By Expression System

By Scale of Operation

By End User

By Application

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar