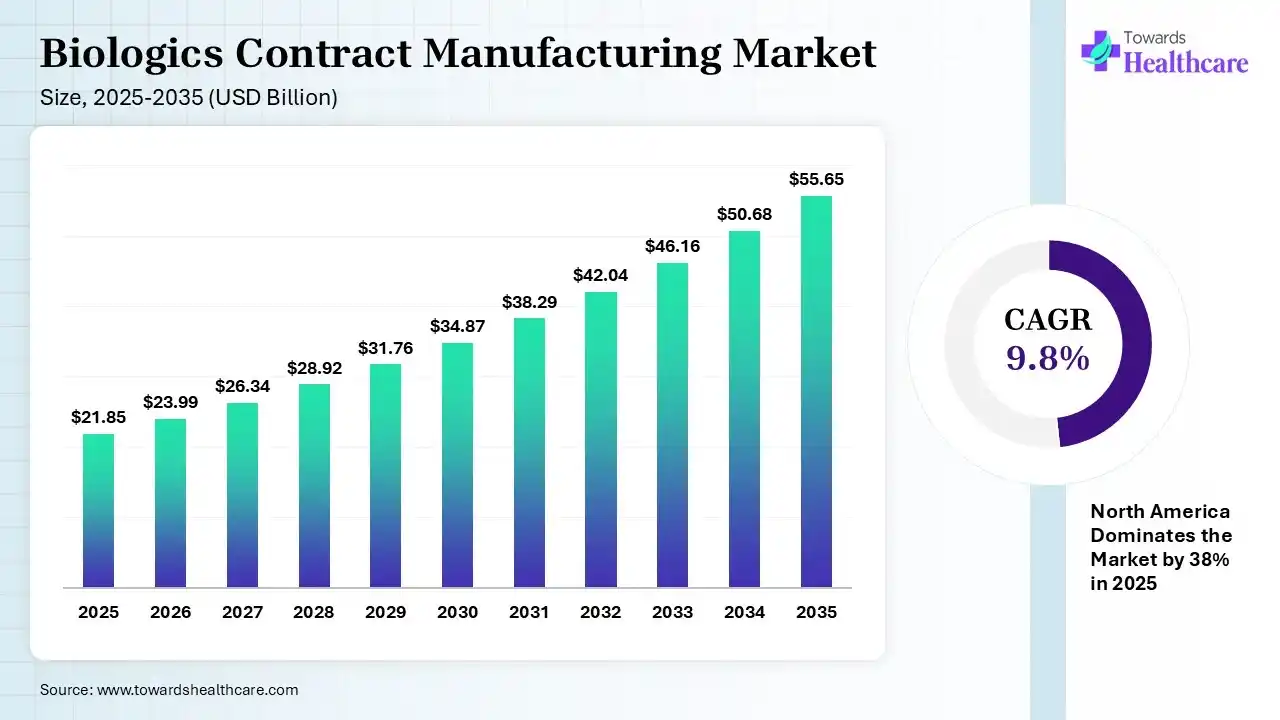

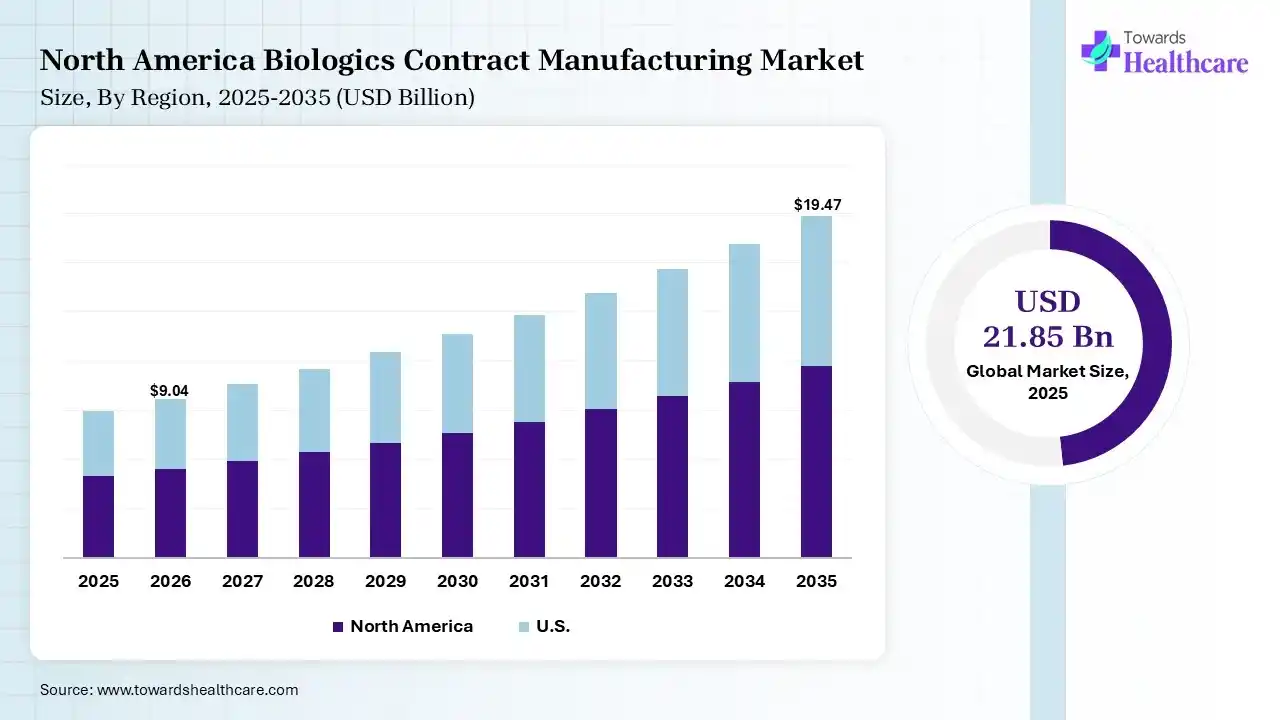

The global biologics contract manufacturing market size was estimated at USD 21.85 billion in 2025 and is predicted to increase from USD 23.99 billion in 2026 to approximately USD 55.65 billion by 2035, expanding at a CAGR of 9.8% from 2026 to 2035. The biologics contract manufacturing market is increasing due to the prevalence of chronic diseases like diabetes, cancer, and autoimmune disorders, which is increasing the demand for biologics, leading medicinal companies to increase outsourcing to contract manufacturers for large-scale manufacturing.

")

Biologics contract manufacturing services quicken the development of biopharmaceuticals from concept to cure. It provides biologics contract manufacturing, including cell line advancement (MCB/WCB) and large molecule production. Biologics CDMO is an outside partner that provides comprehensive solutions in the development and manufacturing of biologic medicine. These solutions encompass everything from initial advancement to commercial productions, including government support, analytical testing, and packaging.

These services also support process development, technology transfer, quality control, and regulatory compliance. They help biotechnology and pharmaceutical companies reduce costs and save time. Advanced manufacturing facilities improve production efficiency and product consistency. Growing demand for monoclonal antibodies, vaccines, cell therapies, and recombinant proteins increases the need for experienced manufacturing partners. Flexible production capacity supports both clinical trials and commercial supply. Strong quality standards ensure product safety and reliability. Continuous investments in automation, single-use technologies, and digital manufacturing improve operational performance. Global outsourcing trends further expand opportunities for biologics contract manufacturing providers worldwide.

AI-powered predictive analytics are transforming the assessment of biologic drug stability. By forecasting the shelf life and stability of biologics, AI boosts supply chain efficiency and helps products retain their effectiveness throughout their lifecycle. Artificial intelligence is also revolutionizing how biopharma companies evaluate CDMOs, especially in the complex areas of biologics and CGT. AI algorithms are streamlining bioprocessing workflows, shortening production timelines, and improving yield predictability. Additionally, AI enhances the shift from laboratory to commercial scale by predicting yields and optimizing fermentation and purification protocols. Furthermore, AI and Machine Learning (ML) tools are advancing biologics discovery, moving toward the de novo design of new biological entities drug.

| Table | Scope |

| Market Size in 2026 | USD 23.99 Billion |

| Projected Market Size in 2035 | USD 55.65 Billion |

| CAGR (2026 - 2035) | 9.8% |

| Leading Region | North America by 38% |

| Key Applications | Monoclonal antibodies, recombinant proteins, vaccines, biosimilars, cell therapies, gene therapies, antibody-drug conjugates (ADCs), fusion proteins |

| Primary End Users | Biopharmaceutical companies, biotechnology firms, virtual biotech startups, academic research institutions, pharmaceutical manufacturers |

| Key Growth Drivers | Increasing biologics approvals, rising outsourcing trend, growing biosimilar pipeline, expansion of cell & gene therapy manufacturing, capacity constraints among innovators |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Source, By Service Insight, By Scale of Operation, By End User, By Region |

| Top Key Players | Thermo Fisher Scientific, AGC Biologics, Catalent, Inc., Boehringer Ingelheim |

")

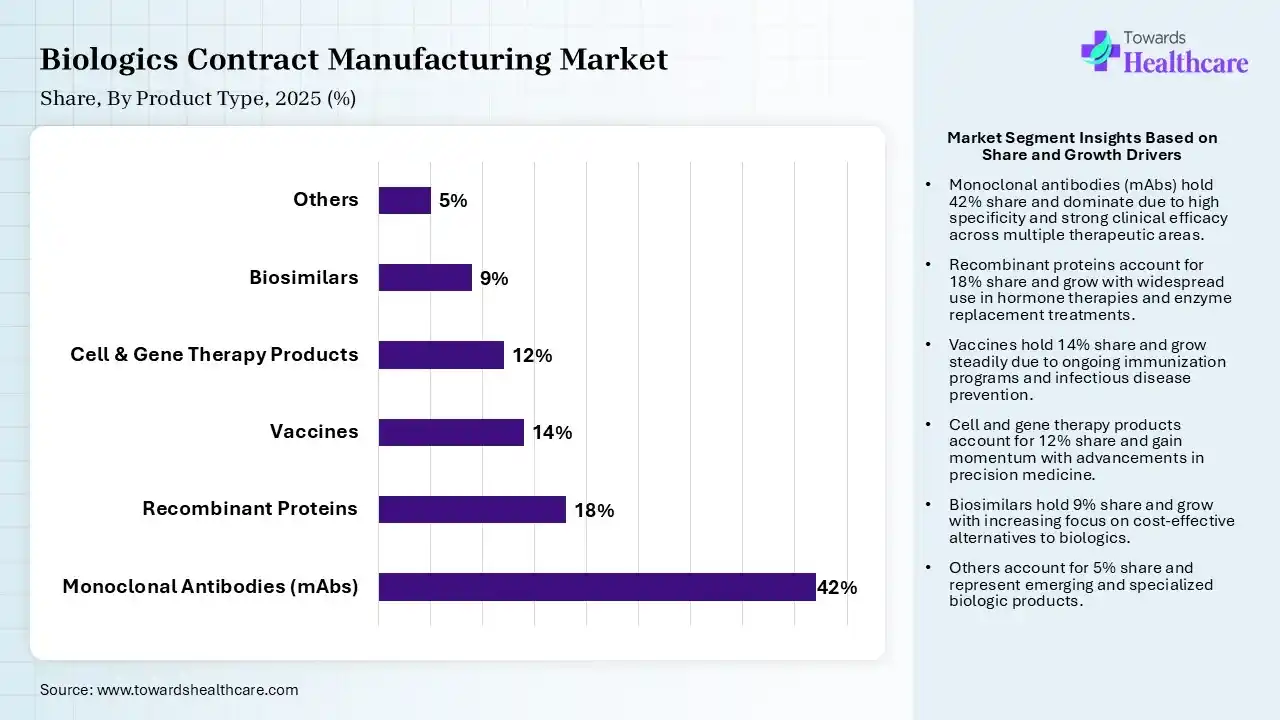

| Segment | Share 2025 (%) |

| Monoclonal Antibodies (mAbs) | 42% |

| Recombinant Proteins | 18% |

| Vaccines | 14% |

| Cell & Gene Therapy Products | 12% |

| Biosimilars | 9% |

| Others | 5% |

The Monoclonal Antibodies (mAbs) Segment Led the Biologics Contract Manufacturing Market in 2025

The monoclonal antibodies (mAbs) segment contributed the largest market share of 42% in 2025, as monoclonal antibodies are manufactured proteins intended to function such as human antibodies in the immune system. Monoclonal antibodies are one of the most effective reagents for a broad range of applications. mAbs are engineered proteins intended to bind with high specificity to molecules that cause diseases, allowing targeted modulation of biological pathways.

The recombinant proteins segment held a significant share of 18% in the market, as recombinant proteins have overcome restraints in sourcing from natural organisms, making them broadly accessible to scientists and pharmaceutical organizations. Recombinant proteins remove the challenges of contamination from pathogens that are present in natural sources.

The vaccines segment held a significant share of 14% in the market, as vaccine production in biologics contract manufacturing provides significant benefits, involving accelerated time, access to specialized expertise in new platforms such as mRNA and viral vectors, and enhanced regulatory compliance.

The cell & gene therapy products segment held a significant share of 12% in the market, and is expected to grow at the fastest CAGR during the forecast period, as cell and gene technologies offer effectiveness and flexibility while lowering challenges in the production of cell and gene therapies. Cell and gene therapy CDMOs work as a specialised extension of a biopharma’s team, providing their knowledge, services, and tools to handle significant parts of C> advancement and manufacturing.

")

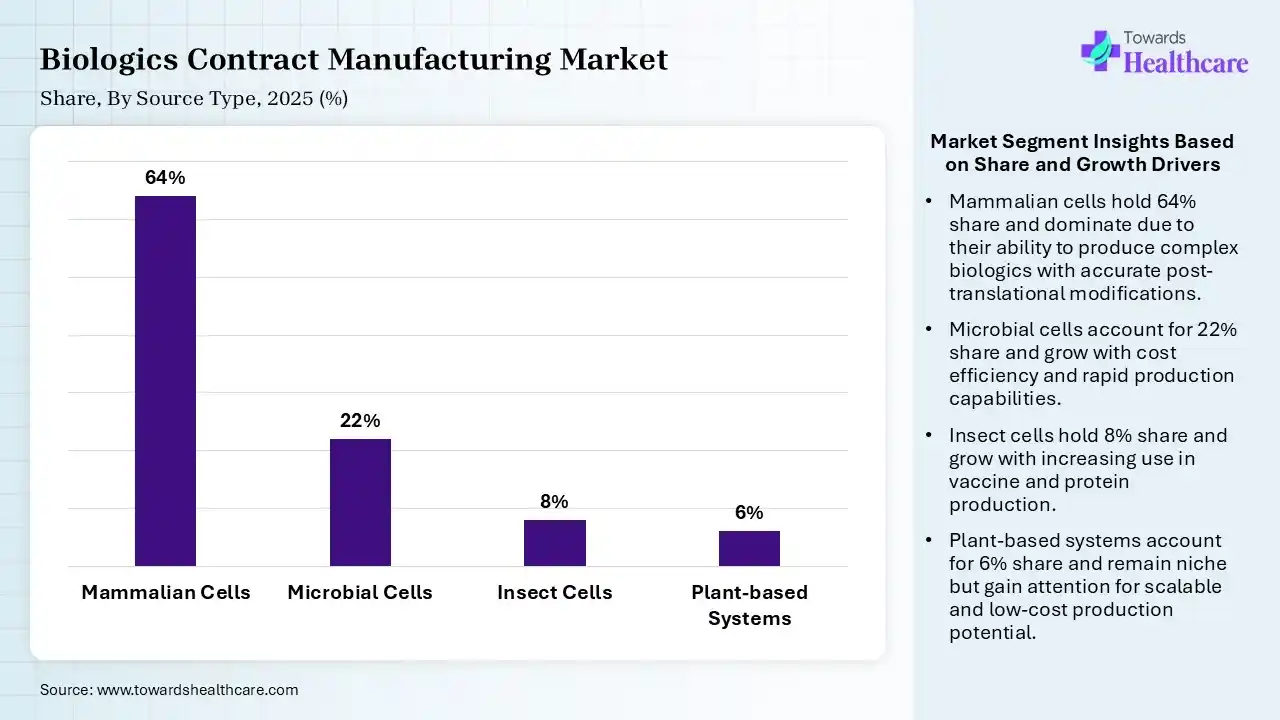

| Segment | Share 2025 (%) |

| Mammalian Cells | 64% |

| Microbial Cells | 22% |

| Insect Cells | 8% |

| Plant-based Systems | 6% |

Mammalian Cells Segment Led the Biologics Contract Manufacturing Market in 2025

The mammalian cells segment contributed the largest market share of 64% in 2025. Mammalian cell culture provides advantages like the capability to research complex cellular functions and mimic human physiological conditions. Mammalian cells produce numerous glycoform patterns, which are affected by culture conditions.

The microbial cells segment held a significant share of 22% of the market, as microbial cells have been used for decades to produce biologics, involving insulin and other recombinant proteins. It provides a clear operational benefit to substitutes such as mammalian cell culture.

The insect cells segment held a significant share of 8% of the market, as expected to grow at the fastest rate of 10.2% during the forecast period. Insect cell culture creates high levels of recombinant proteins and can be simply adapted to high-density suspension culture. It provides advantages for expressing intracellular proteins and multi-protein complexes that are difficult to obtain using mammalian and bacterial systems.

The plant-based systems segment held a significant share of 6% of the market, as increasing applications of plants in vaccine production provide various advantages, involving rapid scalability, low cost, and the capability to produce vaccines without the requirement for refrigeration.

")

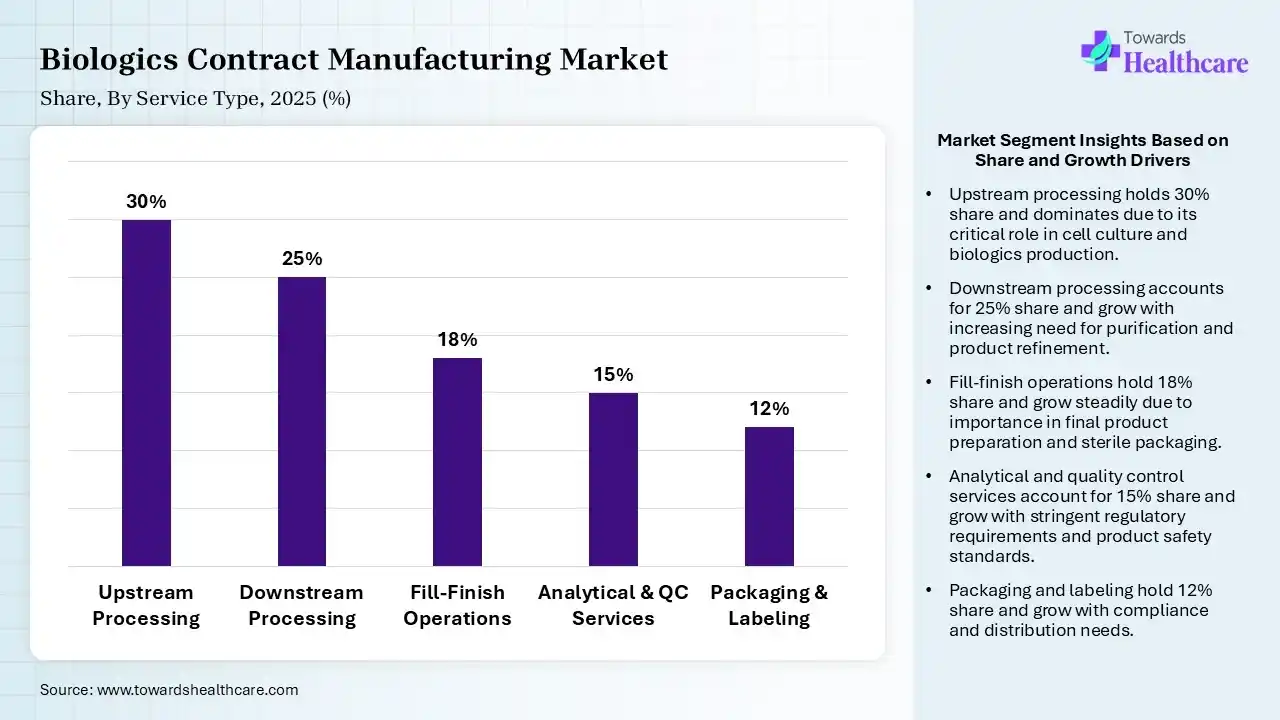

| Segment | Share 2025 (%) |

| Upstream Processing | 30% |

| Downstream Processing | 25% |

| Fill-Finish Operations | 18% |

| Analytical & QC Services | 15% |

| Packaging & Labeling | 12% |

Upstream Processing Segment Led the Biologics Contract Manufacturing Market in 2025

The upstream processing segment contributed the largest market share of 30% in 2025, as the upstream processing stage of biologics manufacturing includes the cultivation of cells in bioreactors to produce the intended product. Upstream processing goal to optimize the microbial or cell culture's development and productivity while ensuring purity and quality.

The downstream processing segment held a significant share of 25% in the market, as this bioprocessing is responsible for separating the particular protein from complex cell culture harvests while ensuring product safety, purity, and quality. Its effectiveness is influenced by the recombinant protein concentration, the difficulty of the plant extracts or cell-free ethos.

The fill-finish operations segment held a significant share of 18% in the market, and is expected to grow at the fastest CAGR of 10.8% during the forecast period, as contract fill finish manufacturing processes to fill finish manufacturing organization provides a cost saving strenth for drug developers as it lowers the capital expenditure related to the establishment of well-equipped filling lines.

The analytical & QC services segment held a significant share of 15% in the market, as CDMOs with advanced analytical development and testing abilities brilliantly supplement or even support to strengthen production capabilities. Analytical testing and processes support bio/pharmaceutical organizations in expanding their product profiles.

")

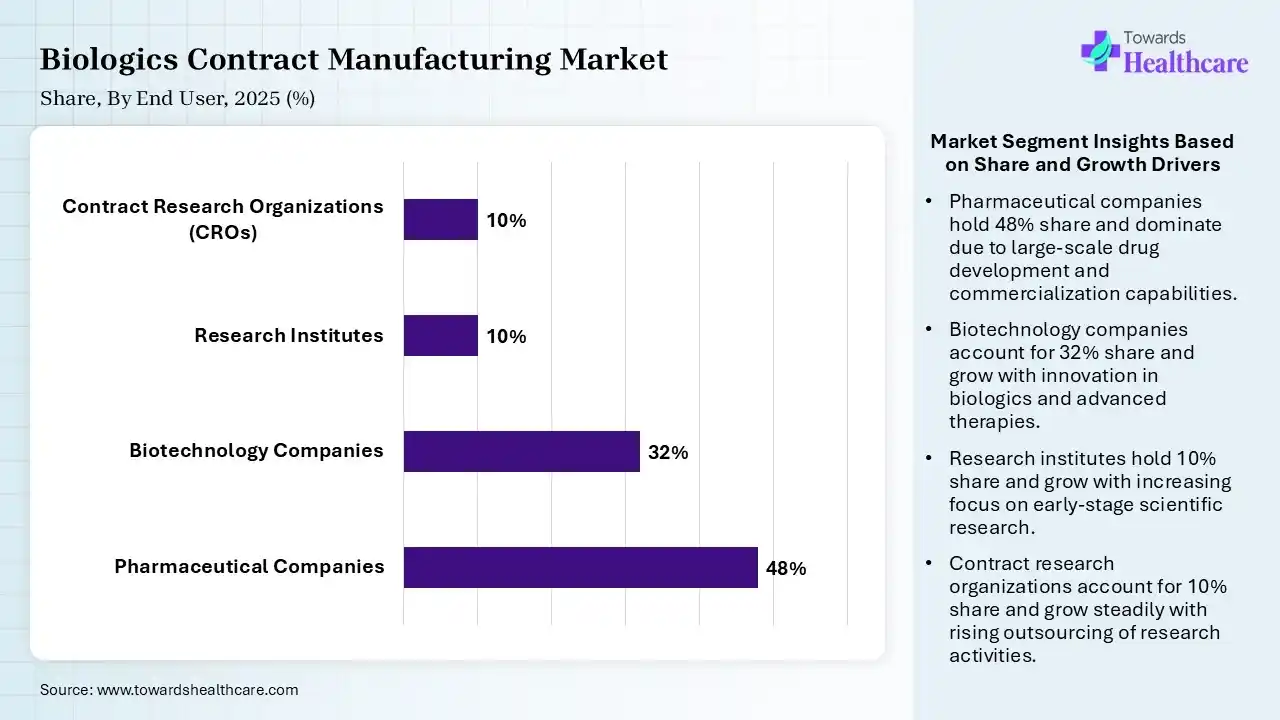

| Segment | Share 2025 (%) |

| Pharmaceutical Companies | 48% |

| Biotechnology Companies | 32% |

| Research Institutes | 10% |

| Contract Research Organizations (CROs) | 10% |

Pharmaceutical Companies Segment Led the Biologics Contract Manufacturing Market in 2025

The pharmaceutical companies segment contributed the largest market share of 48%, as these biopharmaceutical companies provide many distinct benefits over small molecules, making them a popular choice among patients, healthcare teams, and drug makers alike. It avoids significant capital spending to build R&D and clinical manufacturing services.

The biotechnology companies segment held a significant share of 32% in the market, and is expected to grow at the fastest rate of 11.5% during the forecast period, as biotechnology is significantly reshaping the medical care business, allowing the advancement of well-developed therapies, enhancing patient results. Biotechnology has supported the pharma industry in the development of better technology and novel products.

The research institutes segment held a significant share of 10% in the market, as these institutes offer access to highly skilled experts, dedicated knowledge in molecular biology, and advanced technologies such as single-use systems. Outsourcing removes substantial capital spending on infrastructure and equipment.

The contract research organizations (CROs) centers segment held a significant share of 10% in the market, as biologics contract development and manufacturing organization (CDMO) offers biological medical product advancement and production services for pharmaceutical organizations.

")

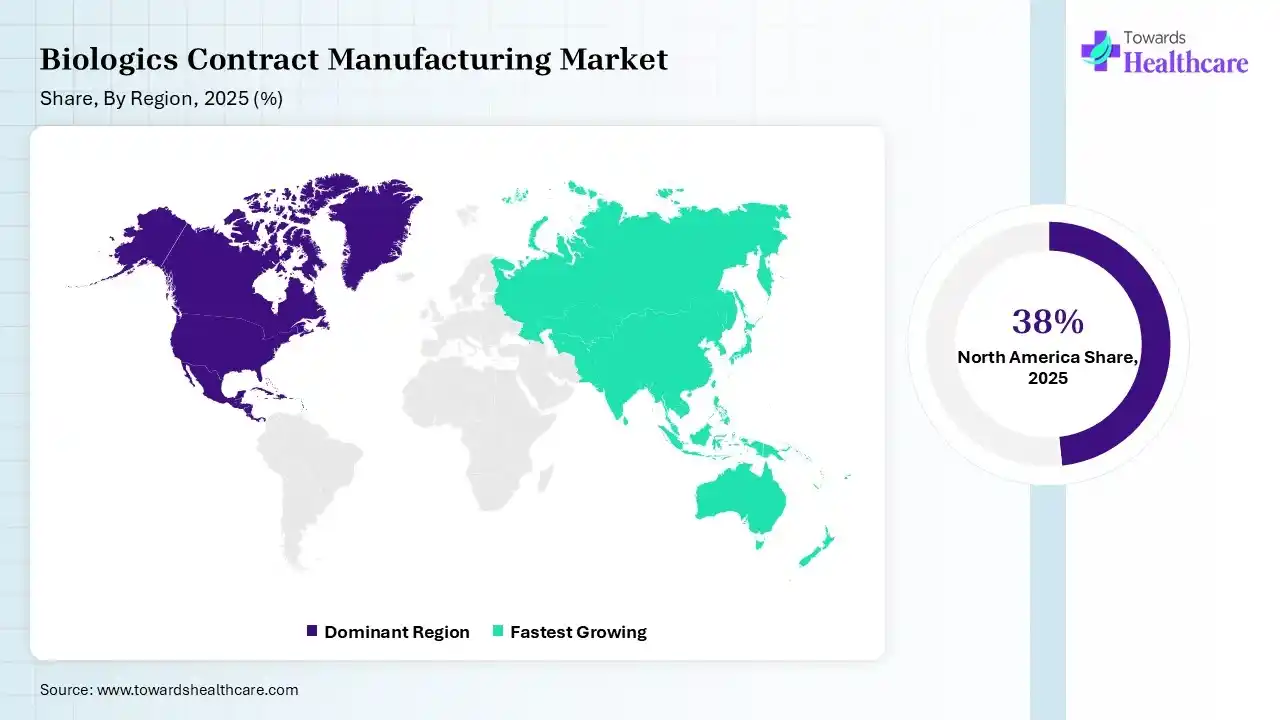

In 2025, North America dominated the biologics contract manufacturing market with a share of 38% in 2025, due to advance biotechnology network, extensive spending in research and development, and a strong government framework that supports novelty. The presence of various biopharmaceutical organizations, combined with academic institutions and research facilities. accepting advanced technologies, like single-use bioreactors, incessant processing, and AI-based automation, drives the growth of the market.

For Instance,

U.S. Market Trends

In the U.S., three in four adults have at least one long-term condition, and over half have two or more chronic conditions. The U.S. is a worldwide powerhouse in healthcare contract development and manufacturing, a hub to some of the world's most well-developed CDMOs. Biopharma and biotech organizations rely on CDMOs to cover internal capacity, achieve scale, and execute challenging manufacturing approaches.

Canada Market Trends

Canada is expanding biologics contract manufacturing through government funding and biotechnology investments. The country has more than 1,000 life sciences companies supporting research and production. Demand for monoclonal antibodies and vaccines continues rising. Companies increase single use manufacturing capacity and automation. Strong regulatory standards improve product quality. Global CDMOs collaborate with local firms through partnerships and facility expansion. Growing clinical trials create new manufacturing opportunities and strengthen the competitive environment nationwide.

Asia Pacific held 24% share of the biologics contract manufacturing market, and is expected to have the fastest CAGR of 11.8% during the forecast period, due to healthcare technology in the Asia-Pacific region being confronted with vast complexities because of an aging population and its increasing demand for healthcare services. Technological development, socioeconomic conditions, and the government landscape eventually revolutionise medical care delivery in APAC, which contributes to the growth of the market.

India Market Trends

In India, a growing aging population and an increasing prevalence of chronic diseases such as cancer and diabetes in APAC are driving massive internal demand for biologic therapies. India is transitioning from generics dominance to a worldwide biologic and biosimilars leader, shaping the future of well-developed therapies. India has a significant pharma network, with more than 10,000 manufacturing services and over 3,000 pharma organizations.

China Market Trends

China is rapidly strengthening biologics contract manufacturing with major investments in biopharmaceutical production facilities. The country has over 5,000 biotechnology companies driving innovation and outsourcing demand. Rising biologic drug approvals encourage manufacturing expansion. Domestic CDMOs compete with global providers by offering cost-effective services and advanced technologies. Government support, skilled workforce availability, and improving quality standards attract international clients while increasing commercial production capabilities across multiple therapeutic segments.

Europe remains a leading region for biologics contract manufacturing because of strong pharmaceutical research and advanced production infrastructure. The region hosts thousands of biotechnology companies and numerous GMP-certified manufacturing facilities. Demand for biosimilars and innovative biologics supports continuous investment. CDMOs expand capacity through acquisitions and technology upgrades. Strict regulatory requirements ensure high product quality. Cross-border partnerships and increasing outsourcing create long-term growth opportunities across European countries.

UK Market Trends

The UK has a well-developed biologics contract manufacturing market supported by strong biotechnology research and innovation. More than 6,800 life sciences businesses contribute to industry growth. Demand for advanced therapies and biologic medicines continues to increase. CDMOs invest in flexible manufacturing facilities and digital technologies. Collaboration between universities, pharmaceutical companies, and manufacturers strengthens competitiveness. Government funding and skilled professionals support continued expansion and commercial manufacturing success.

Germany Market Trends

Germany is a major biologics contract manufacturing hub with advanced pharmaceutical infrastructure and strong industrial capabilities. The country has over 800 biotechnology companies supporting biologics development and manufacturing. Growing demand for biosimilars, vaccines, and monoclonal antibodies drives production expansion. Leading CDMOs invest in automation, process optimization, and sustainable manufacturing technologies. Strong quality standards, research partnerships, and export opportunities improve competitiveness while supporting long-term market growth across global pharmaceutical industries.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Cytiva, Sartorius, Merck KGaA, Danaher (Pall) | Provide bioprocessing equipment, filtration, cell culture, and manufacturing technologies |

| Product Manufacturers | Amgen, Roche, AbbVie, Bristol Myers Squibb | Develop biologic therapeutics requiring outsourced manufacturing support |

| Service Providers | Lonza, Catalent, Samsung Biologics, FUJIFILM Diosynth Biotechnologies | Offer process development, manufacturing, fill-finish, and commercial production |

| Platform Providers | WuXi Biologics, AGC Biologics, Lonza | Provide integrated biologics development and manufacturing platforms |

| CROs/CDMOs | Lonza, Thermo Fisher (Patheon), Samsung Biologics, WuXi Biologics, AGC Biologics | Support biologic drug development through commercial manufacturing |

| Software Vendors | Siemens Digital Industries, Emerson, Honeywell, Werum PAS-X (Körber) | Manufacturing execution systems (MES), digital bioprocessing, quality management |

| Research Institutions | National Institutes of Health, University of Oxford, Massachusetts Institute of Technology | Biologics research, process innovation, translational medicine |

| End-User Industries | Biopharmaceuticals, Biotechnology, Vaccines, Cell & Gene Therapy, Biosimilars | Primary customers outsourcing manufacturing activities |

In July 2026, “The market is demanding capable, reliable manufacturing partners with global quality standards and geographic flexibility. This agreement reflects the strength of our network, our single-use expertise, and the strategic role Japan can play in resilient biologics supply chains”, said Alberto Santagostino, President and CEO of AGC Biologics.

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 62% | 25% | 13% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza | Basel | Switzerland | World's leading biologics CDMO with large commercial manufacturing footprint | Mammalian manufacturing, microbial production, ADCs, cell & gene therapy manufacturing |

| Samsung Biologics | Incheon | South Korea | Largest biologics manufacturing capacity globally | Monoclonal antibody manufacturing, drug substance and drug product services |

| Thermo Fisher Scientific (Patheon) | Waltham, Massachusetts | USA | Major integrated CDMO serving biologics from development through commercialization | Biologics development, commercial manufacturing, fill-finish |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Catalent | Somerset, New Jersey | USA | Major biologics and advanced therapies manufacturing provider | Biologics manufacturing, fill-finish, cell and gene therapy services |

| AGC Biologics | Seattle, Washington | USA | Specialized biologics CDMO with global operations | Mammalian and microbial biologics manufacturing |

| Boehringer Ingelheim BioXcellence | Ingelheim am Rhein, Rhineland-Palatinate | Germany | Strong biologics contract manufacturing business | Biopharmaceutical development and commercial production |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Abzena | San Diego, California | USA | Specialized biologics and ADC development partner | Biologics development, antibody engineering, manufacturing |

| BioFactura | Frederick, Maryland | USA | Biosimilar and biologics manufacturing specialist | Biosimilar development and biologics production |

| MabPlex International | Yantai, Shandong | China | Growing biologics CDMO focused on monoclonal antibodies | Cell line development and GMP manufacturing |

Strengths

Weakness

Opportunities

Threat

By Product Type

By Source

By Service Insight

By Scale of Operation

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar