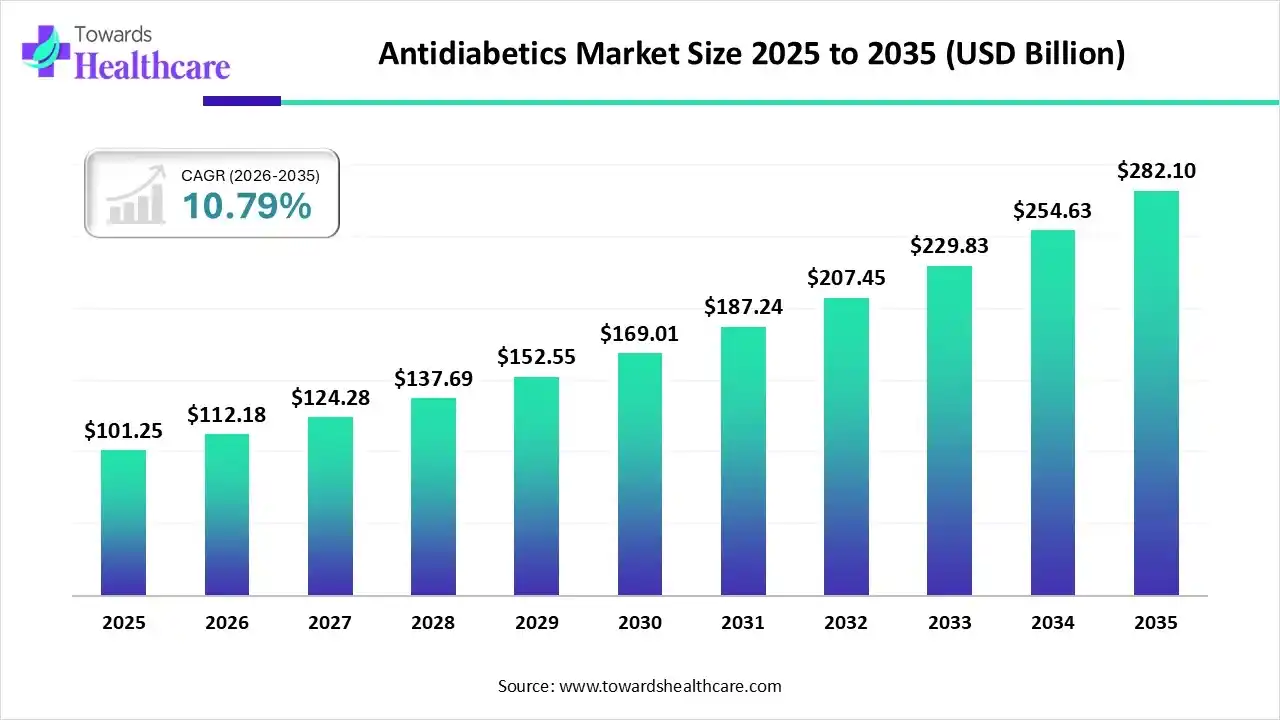

The global antidiabetics market size was estimated at USD 101.25 billion in 2025 and is predicted to increase from USD 112.18 billion in 2026 to approximately USD 282.1 billion by 2035, expanding at a CAGR of 10.79% from 2026 to 2035.

")

The market is expanding steadily, driven by rising diabetes prevalence, growing adoption of oral drugs and injectables, and increasing focus on early diagnosis, long-term disease management, and innovation in combination therapies and advanced insulin formulations.

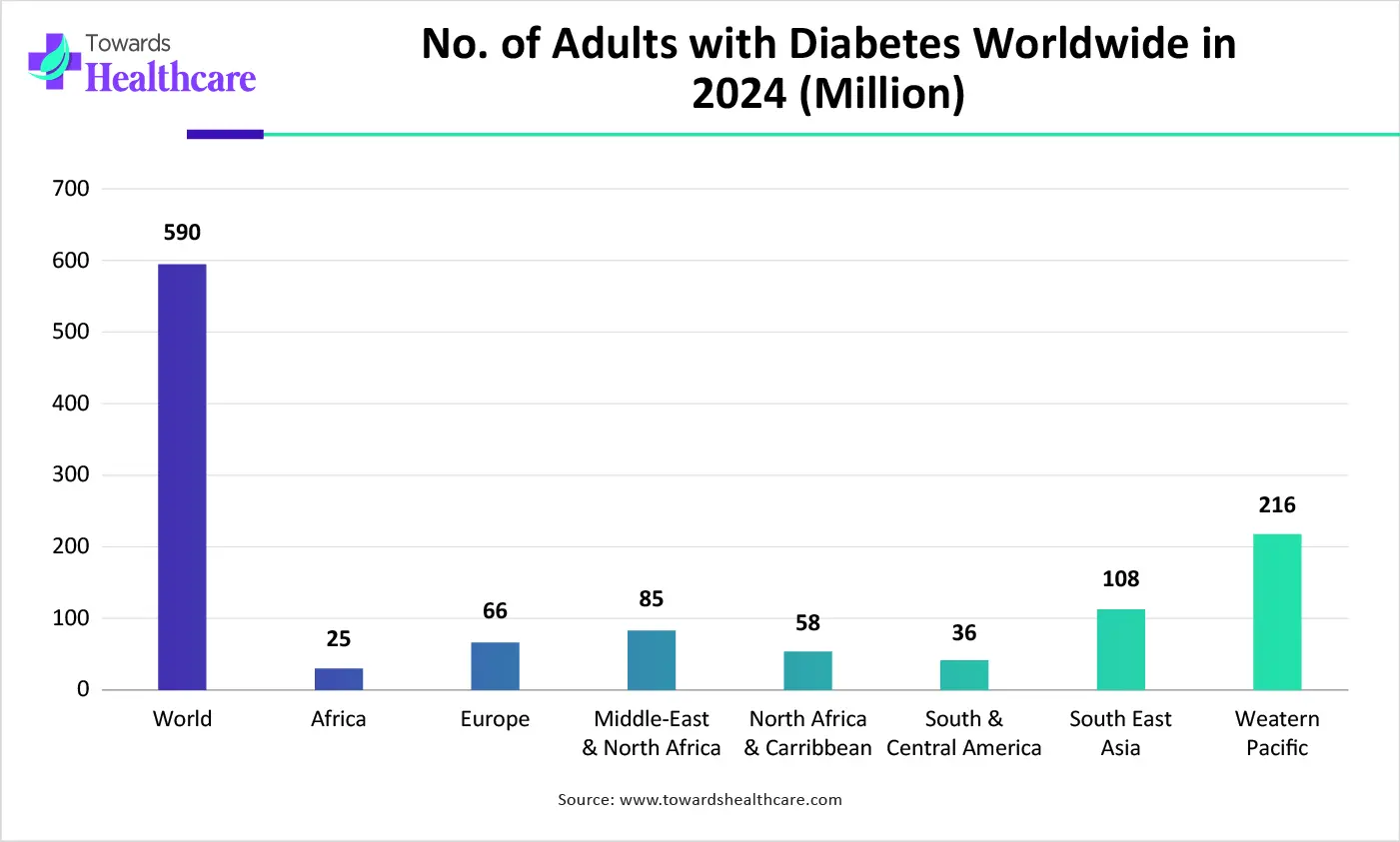

Antidiabetics are medications used to control blood glucose levels in people with diabetes by improving insulin actions, increasing insulin secretion, or reducing glucose production and absorption. The antidiabetics market is growing due to the rising global prevalence of diabetes, unhealthy lifestyles, and increasing obesity rates. Greater awareness, early diagnosis, and improved access to treatment are boosting demand. Additionally, continuous innovation in oral drugs, injectables, combination therapies, and advanced insulin formulations, along with supportive government initiatives and expanding healthcare infrastructure, is accelerating market growth worldwide.

")

Artificial intelligence can revolutionize the antidiabetics market by enabling personalized treatment plans through predictive analytics, real-time glucose monitoring, and optimized drug dosing. AI-driven insights improve early diagnosis, patient adherence, and clinical decision-making, while accelerating drug discovery, reducing development costs, and enhancing outcomes through smarter, data-driven diabetes management solutions.

| Table | Scope |

| Market Size in 2026 | USD 112.18 Billion |

| Projected Market Size in 2035 | USD 282.1 Billion |

| CAGR (2026 - 2035) | 10.79% |

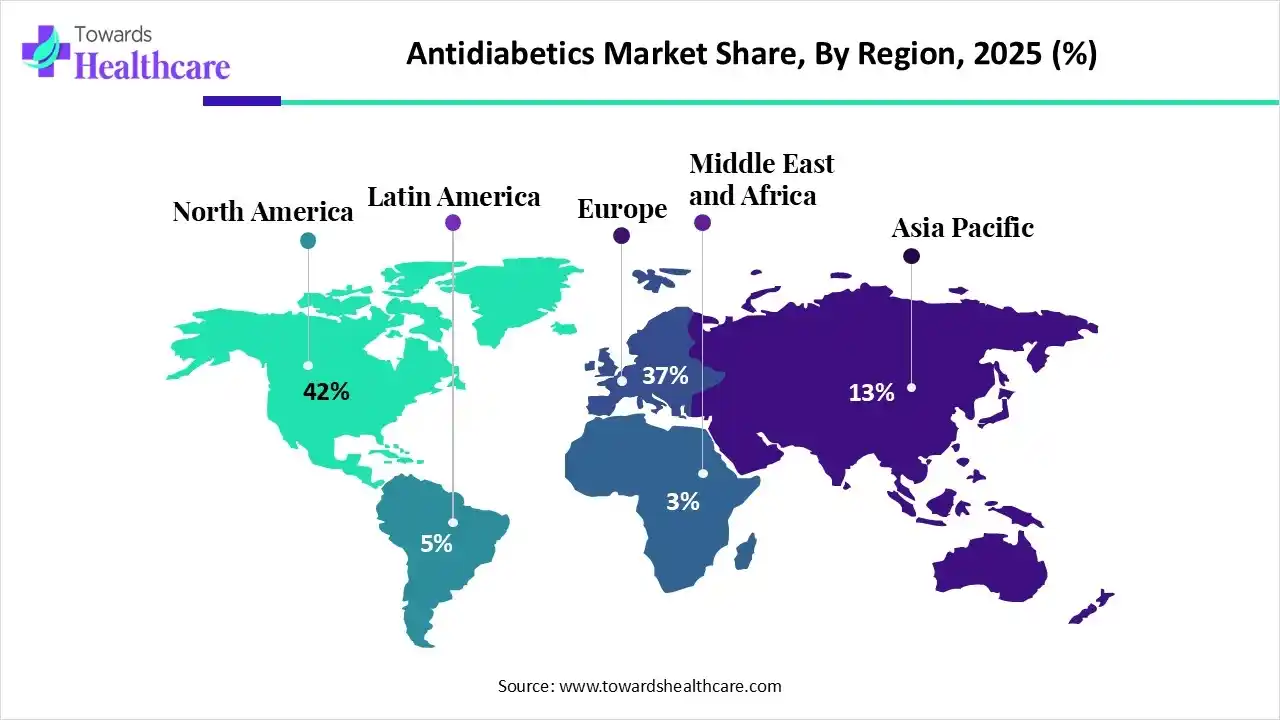

| Leading Region | North America by 42% |

| Key Applications | Glycemic control, Type 2 diabetes management, Type 1 insulin replacement, obesity-linked diabetes management, cardiovascular risk reduction in diabetics |

| Primary End Users | Hospitals, retail pharmacies, specialty clinics, diabetes care centers, home-care patients |

| Key Challenges | High drug pricing pressure, biosimilar insulin competition, regulatory scrutiny, adherence issues, supply chain constraints |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Diabetes Type, By Distribution Channel, By Region |

| Top Key Players | Novo Nordisk, Eli Lilly and Company, Sanofi, Merck & Co., Inc., AstraZeneca, Johnson & Johnson Services Inc |

| Segments | Shares % |

| GLP-1 Receptor Agonists | 30% |

| Insulin | 28% |

| SGLT2 Inhibitors | 16% |

| DPP-4 Inhibitors | 14% |

| Others | 12% |

Why Did the GLP-1 Receptor Agonists Segment Dominate in the Market in 2025?

The GLP-1 receptor agonists segment dominated the antidiabetics market by 30% share in 2025 due to its superior glycemic control, significant weight-loss benefits, and proven cardiovascular risk reduction. Strong clinical outcomes, rising obesity-linked diabetes cases, and expanding approvals for comorbid conditions increased physician preference. Additionally, high patient adherence, premium pricing, and strong uptake of branded GLP-1 therapies across major markets supported revenue leadership.

SGLT2 Inhibitors

The SGLT2 inhibitors segment is expected to grow at a significant rate during the forecast period due to strong clinical evidence supporting cardiovascular and renal protection beyond glycemic control. Increasing use in patients with type 2 diabetes, heart failure, and chronic kidney disease, along with expanding label indications and growing physician adoption, is accelerating demand. Improved safety profiles and rising awareness of long-term benefits further support rapid segment growth.

| Segments | Shares % |

| Type 2 | 88% |

| Type 1 | 12% |

How the Type 2 Diabetes Segment Dominated the Antidiabetics Market in 2025?

The type 2 diabetes segment dominated the market by 88% share in 2025 due to its high and growing prevalence driven by sedentary lifestyles, obesity, and aging populations. Most antidiabetic drug classes, including oral agents, injectables, and combination therapies, primarily target type 2 diabetes. Continuous treatment requirements, early diagnosis, and agonists and SGLT2 inhibitors further supported segment dominance.

Type 1 Diabetes

The type 1 diabetes segment is expected to grow at a notable rate during the forecast period due to rising disease awareness, improved rates, and increasing access to advanced insulin therapies. Technological advancements such as continuous glucose monitoring systems, insulin pumps, and smart insulin delivery are improving disease management and patient outcomes. Additionally, supportive reimbursement policies and ongoing research into novel insulin formulations and immunotherapies are contributing to steady market growth.

| Segments | Shares % |

| Intravenous | 42% |

| Subcutaneous | 38% |

| Oral | 20% |

Why the Intravenous Segment Dominated the Antidiabetics Market?

The intravenous segment is dominate the market by 42% share in 2025 due to its widespread use in hospitals and critical-care settings for managing severe hyperglycemia, diabetic ketoacidosis, and perioperative glucose control. Intravenous administration enables rapid onset, precise dose titration, and continuous monitoring, making it the preferred choice for acute diabetes management in emergency and inpatient care environments.

Subcutaneous

The subcutaneous segment is expected to grow at the fastest CAGR during the forecast period due to increasing adoption of injectable therapies suchas GLP-1 receptor agonists and long-acting insulins. The shift toward self-administration, availability of user-friendly pens and auto-injectors, and improved patient convenience are boosting adherence. Additionally, rising outpatient care, home-based treatment trends, and expanding approvals for injectable anti-diabetics are accelerating demand for subcutaneous delivery.

| Segments | Shares % |

| Hospital Pharmacies | 48% |

| Retail Pharmacies | 35% |

| Online Pharmacies | 17% |

Why Did the Hospital Pharmacies Segment Dominate in the Market in 2025?

The hospital pharmacies segment dominated the antidiabetics market in 2025 due to high patient inflow for diabetes-related complications, inpatient insulin therapy, and acute care management. Hospitals remain the primary point of treatment for severe hyperglycemia, diabetic emergencies, and comorbid conditions. Availability of advanced injectable drugs, better cold-chain infrastructure, specialty supervision, and strong reimbursement support further strengthened hospital pharmacies’ leading market position.

Online Pharmacies

The online pharmacies segment is expected to grow at the fastest CAGR during the forecast period due to rising preference for convenient, home-based medicine delivery and digital prescription services. Increasing internet penetration, smartphone usage, and awareness of chronic disease management are driving adoption. Online platforms also offer competitive pricing and subscription refills for long-term antidiabetic therapies, improved access in remote areas, and integration with telemedicine, collectively accelerating market growth.

")

North America dominated the global market by 42% share in 2025 due to the high prevalence of diabetes, strong healthcare infrastructure, and early adoption of advanced therapies. Favorable reimbursement policies, widespread use of innovative drug classes such as GLP-1 receptor agonists and SGLT2 inhibitors, and the strong presence of leading pharmaceutical companies supported market leadership. Additionally, higher healthcare spending, extensive clinical research activity, and rapid regulatory approvals further strengthened the region’s dominant position.

United States at the Forefront of the Antidiabetics Market Growth

The U.S. led the market in 2025 by capturing the largest revenue share due to its high diabetes burden, strong insurance coverage, and rapid adoption of premium therapies. Advanced healthcare infrastructure, favorable reimbursement for innovative drugs, and widespread use of GLP-1 and SGLT2 inhibitors supported revenue growth. Additionally, the presence of major pharmaceutical players, strong R&D investments, and early regulatory approvals further reinforced the country's market leadership.

Canada Market Trend

The antidiabetic market in Canada is experiencing steady growth as a result of various factors such as increasing incidences of diabetes, aging population and growing adoption of new glucose-lowering treatments. The healthcare infrastructure in Canada is in strong condition, the penetration of GLP-1 receptor agonists and SGLT2 inhibitors in the market strengthened the market growth.

Mexico Market Trend

Mexico antidiabetic market is growing due to the increase in type 2 diabetes incidences resulting mainly from obesity and other lifestyle problems. Increased investments in the healthcare sector are being made and there is an increase in diabetes awareness among the people which is creating major demand for antidiabetic drugs in hospitals and pharmacies.

Asia Pacific is anticipated to grow by 13% share at the fastest CAGR during the forecast period due to the rapidly growing diabetes population, driven by urbanization, sedentary lifestyles, and dietary changes. Improving healthcare infrastructure, increasing awareness, and expanding access to diagnosis and treatment are boosting demand. Additionally, a growing middle-class population, rising healthcare spending, government-led diabetes management programs, and the entry of cost-effective generic and branded antidiabetic drugs are accelerating market expansion across the region.

India: A High-Growth Hub in the Antidiabetics Market

India is anticipated to grow at a rapid CAGR during the forecast period due to the rising prevalence of diabetes driven by urbanization, lifestyle changes, and a growing aging population. Increasing awareness, early screening initiatives, and expanding access to affordable antidiabetic therapies are fueling demand. Strong growth in domestic pharmaceutical manufacturing, wider availability of generics, improving healthcare infrastructure, and government programs targeting chronic disease management further support sustainable market expansion.

Japan Market Trend

Japan’s antidiabetic market is seen to benefit being a country that has an aging and mature population. The healthcare system is well advanced while the prevalence of type 2 diabetes is also growing rapidly in Japan. One of the pharmaceutical company strategies is the development of innovative therapies and appropriate combination treatments.

Europe is expected to grow by 37% share at a notable rate during the forecast period due to the increasing prevalence of diabetes and an aging population. Strong healthcare systems, widespread reimbursement coverage, and early adoption of innovative therapies such as GLP-1 receptor agonists and SGLT2 inhibitors are driving demand. Additionally, rising focus on preventive care, supportive regulatory frameworks, and ongoing investment in clinical research and digital diabetes management solutions are contributing to sustained market growth across the region.

Germany Market Trends

Germany is one of the leading antidiabetics markets in Europe owing to its high healthcare spending, good diabetes screening practices and acceptance of innovative therapies. The growing demand for GLP-1 receptor agonists, insulin therapy and personalized diabetes care is leading to the sustained growth of the market.

Netherlands Market Trends

Over the years Netherlands has been experiencing continuous growth in the antidiabetics market due to rise in diabetes rate, established primary healthcare services and active initiatives towards preventive care. The use of modern antidiabetics and integrated diabetes management programs has seen improvements in the patients' lives and has contributed to the expansion of the market.

UK: A Fast-Emerging Growth Market for Antidiabetics

The UK is anticipated to grow at a rapid CAGR during the forecast period due to rising diabetes prevalence, an aging population, and a strong focus on early diagnosis. Expanding adoption of advanced therapies, supportive reimbursement through public healthcare systems, and increasing use of digital diabetes management tools are boosting treatment access. Additionally, ongoing clinical research, government-led prevention programs, and growing awareness of long-term disease management are driving sustained market expansion.

| Category | Key Participants | Role in Ecosystem |

| Technology Providers | Medtronic, Abbott, Dexcom | Provide CGM (continuous glucose monitoring) and insulin delivery tech |

| Product Manufacturers | Novo Nordisk, Eli Lilly, Sanofi | Develop and manufacture insulin, GLP-1, and oral antidiabetics |

| Service Providers | CVS Health, Walgreens Boots Alliance | Drug distribution, patient access programs, pharmacy services |

| Platform Providers | Omada Health, Livongo (Teladoc Health) | Digital diabetes management platforms and remote monitoring |

| CROs/CDMOs | Lonza, Catalent, WuXi Biologics | Biologic manufacturing, insulin/peptide production support |

| Software Vendors | Roche Diabetes Care (mySugr), Glooko | Diabetes tracking and analytics platforms |

| Research Institutions | NIH, Joslin Diabetes Center, Karolinska Institute | Clinical research, diabetes innovation, biomarker discovery |

| End-User Industries | Hospitals, outpatient clinics, home healthcare | Direct treatment and disease management environments |

R&D

Clinical Trials

Packaging and Serialization

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 81% | 14% | 5% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Novo Nordisk A/S | Bagsværd, Copenhagen | Denmark | Global leader in insulin and GLP-1 therapies with dominant diabetes portfolio | Ozempic, Wegovy, Tresiba, Levemir |

| Eli Lilly and Company | Indianapolis, Indiana | USA | Fast-growing GLP-1 and insulin innovator with strong obesity-diabetes overlap | Mounjaro, Trulicity, Humalog |

| Sanofi S.A. | Paris | France | Legacy insulin leader with diversified diabetes portfolio | Lantus, Toujeo, Admelog |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Boehringer Ingelheim GmbH | Ingelheim am Rhein | Germany | Co-developer of SGLT2 therapies and metabolic disease treatments | Jardiance (with Eli Lilly partnership) |

| Abbott Laboratories | Abbott Park, Illinois | USA | Leader in diabetes monitoring and CGM ecosystem | FreeStyle Libre system |

| Dexcom Inc. | San Diego, California | USA | Pure-play CGM leader driving real-time glucose monitoring adoption | Dexcom G6, G7 |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| MannKind Corporation | Danbury, Connecticut | USA | Focused on inhaled insulin delivery innovation | Afrezza inhaled insulin |

| Zealand Pharma A/S | Copenhagen | Denmark | GLP-1 and peptide-based metabolic drug developer | Dasiglucagon, GLP-1 analog pipeline |

| Viking Therapeutics Inc. | San Diego, California | USA | Emerging metabolic/obesity-diabetes drug pipeline company | VK2735 (GLP-1/GIP dual agonist) |

Strengths

Weaknesses

Opportunities

Threats

In June 2025: Abbott and MSD Pharmaceuticals announced a strategic distribution partnership in India for Sitagliptin, Janumet, and Janumet XR to strengthen access to oral anti-diabetic therapies. Abbott Vice President Ambati Venu said, “As the largest diversified healthcare company in India, Abbott is uniquely positioned to address some of the most pressing health challenges, particularly non-communicable diseases, which contribute to a considerable burden on the healthcare system.”

By Drug Class

By Diabetes Type

By Route of Administration

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar