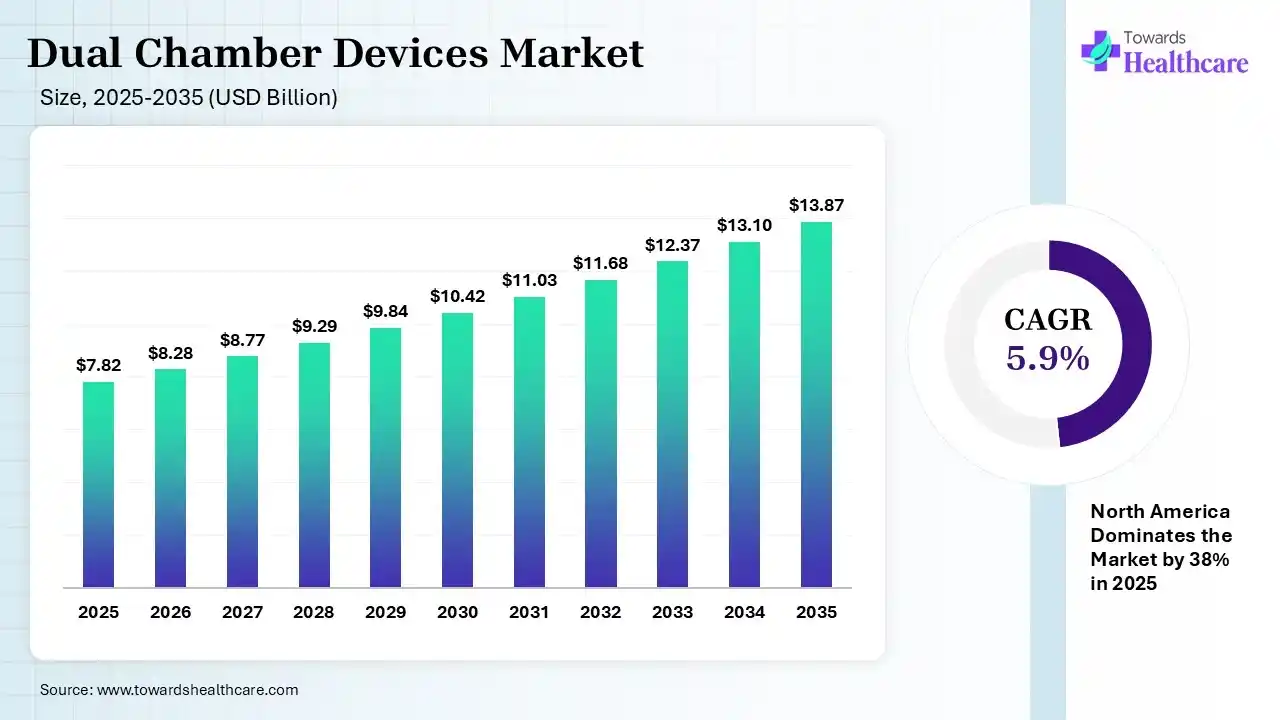

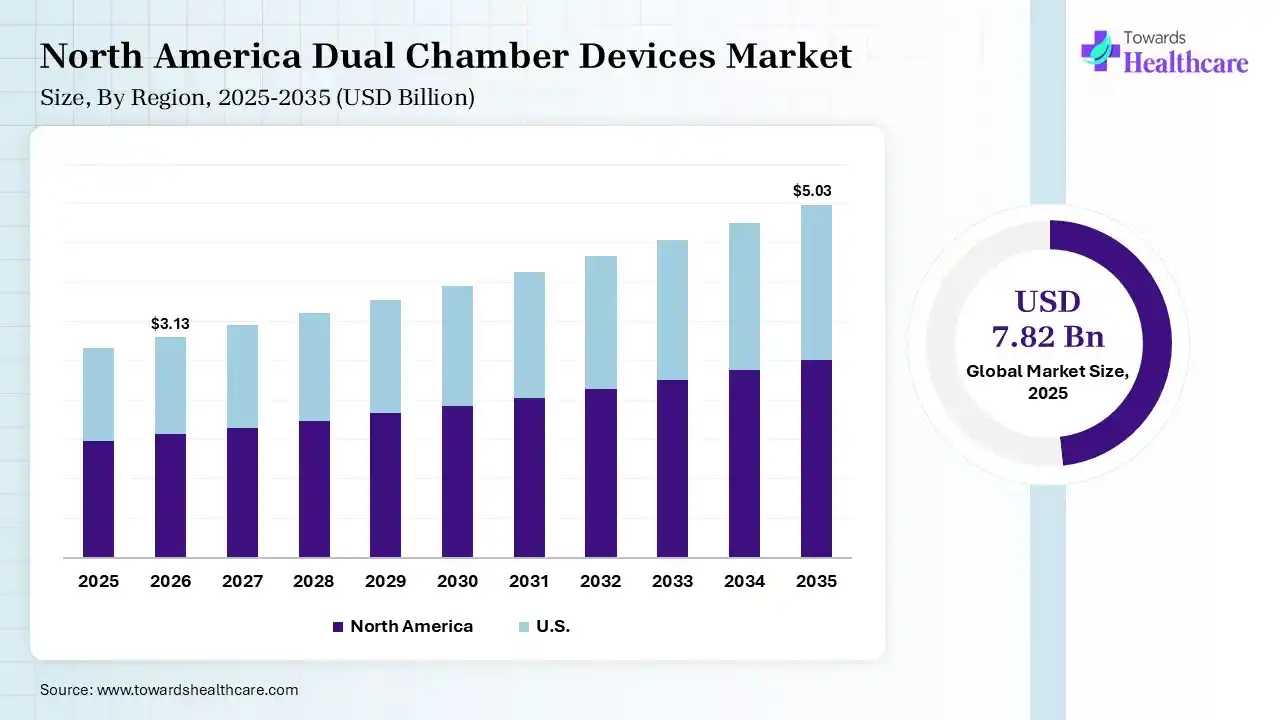

The global dual chamber devices market size was estimated at USD 7.82 billion in 2025 and is predicted to increase from USD 8.28 billion in 2026 to approximately USD 13.87 billion by 2035, expanding at a CAGR of 5.9% from 2026 to 2035. The market is driven by rising demand for advanced cardiac pacing solutions, particularly for treating arrhythmias and heart failure, along with an aging global population. Technological advancements and increasing adoption of minimally invasive procedures are further accelerating market growth worldwide.

")

Dual chamber devices are cardiac pacing devices that use two leads to regulate both the atrium and ventricles, ensuring coordinated heartbeats. They are mainly used to treat arrhythmias by mimicking the heart’s natural electrical conduction systems. The dual chamber devices market is growing due to the increasing prevalence of cardiac disorders such as arrhythmia and heart failure, especially among the aging population. These devices offer improved synchronization of heart function compared to single-chamber systems, driving adoption.

The dual chamber devices market is experiencing significant expansion driven by rising global cases of cardiovascular conditions. In 2026, the high prevalence of cardiac arrhythmias and heart failure acts as a major catalyst for product adoption. Technical trends highlight a shift toward smart, Bluetooth-enabled pacing therapies that allow remote patient tracking. Notable opportunities lie in developing miniaturized designs and biocompatible materials to increase comfort. The competitive landscape features prominent medical technology giants focusing on strategic approvals and geographical expansion to capture emerging regional territories. Furthermore, the rising volume of clinical cases requiring precise dual-chamber synchronization pushes hospitals to upgrade their current inventory. These collective factors create a highly dynamic environment for device manufacturers globally.

Artificial intelligence is accelerating the market by enabling smarter cardiac monitoring and personalized therapy. AI-powered algorithms improve the detection of arrhythmias, optimize pacing settings, and allow predictive maintenance of devices. Integration with remote monitoring systems enhances patient management and reduces hospital visits. These advancements lead to better clinical outcomes, increased physician confidence, and higher adoption of advanced dual-chamber cardiac devices globally.

| Table | Scope |

| Market Size in 2026 | USD 8.28 Billion |

| Projected Market Size in 2035 | USD 13.87 Billion |

| CAGR (2026 - 2035) | 5.9% |

| Leading Region | North America by 38% |

| Key Applications | Bradycardia management, atrioventricular block treatment, arrhythmia management, sudden cardiac death prevention, heart failure management |

| Primary End Users | Hospitals, cardiac centers, electrophysiology clinics, ambulatory surgical centers |

| Key Growth Drivers | Aging population, increasing prevalence of arrhythmias, growing cardiovascular disease burden, leadless pacing innovations, remote monitoring adoption |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Device Type, By Application, By End User, By Technology, By Age Group, By Distribution Channel, By Region |

| Top Key Players | Gerresheimer, Nipro Corporation, SCHOTT AG (Headquarters), Vetter Pharma-Fertigung GmbH & Co. KG, ARTE Corporation, Credence MedSystems, Inc. |

")

| Segment | Share 2025 (%) |

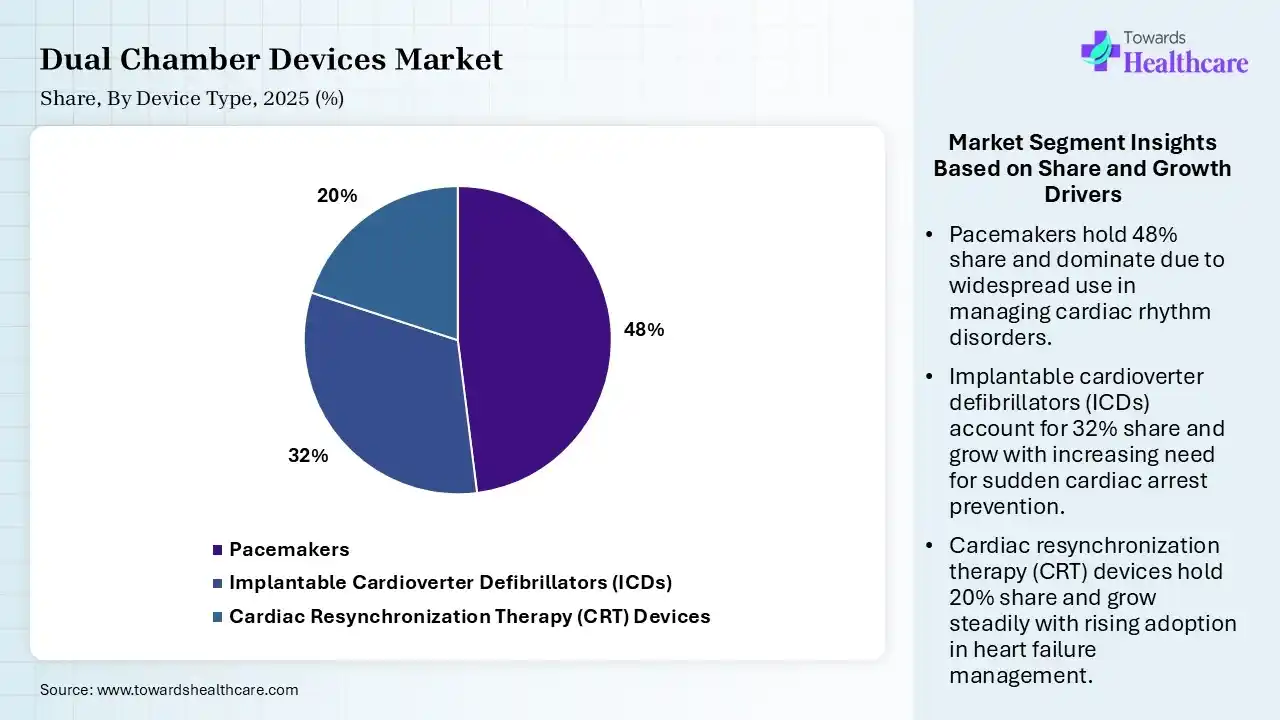

| Pacemakers | 48% |

| Implantable Cardioverter Defibrillators (ICDs) | 32% |

| Cardiac Resynchronization Therapy (CRT) Devices | 20% |

The Pacemakers Segment Dominated the Market in 2025

The pacemakers segment dominated the dual chamber devices market with a revenue share of 48% in 2025 due to their widespread use in managing common rhythm disorders such as bradycardia. They are cost-effective, highly effective, and routinely recommended as first-line therapy compared to more complex implantable devices. Additionally, an aging population, strong clinical success rate, and continuous technological improvements in pacing systems further support their higher adoption globally.

The implantable cardioverter defibrillators (ICDs) segment held the second-largest share of 32% of the market in 2025 due to the rising incidence of life-threatening arrhythmias such as ventricular tachycardia and sudden cardiac arrest. Increasing awareness, improved survival benefits, and expanding indications for high-risk patients are driving demand. Technological advancements, including enhanced detection accuracy and device reliability, further support the rapid adoption of ICDs globally.

The cardiac resynchronization therapy (CRT) devices segment held a 20% share in 2025 and is expected to grow at the fastest CAGR of 7.10% in the dual chamber devices market during the forecast period due to the rising prevalence of heart failure and increasing demand for advanced treatment options. CRT devices improve heart-pumping efficiency and patient outcomes, especially in severe cases. Expanding clinical indications, growing awareness, and continuous technological advancements in device design and implantation procedures are further accelerating adoption globally.

")

| Segment | Share 2025 (%) |

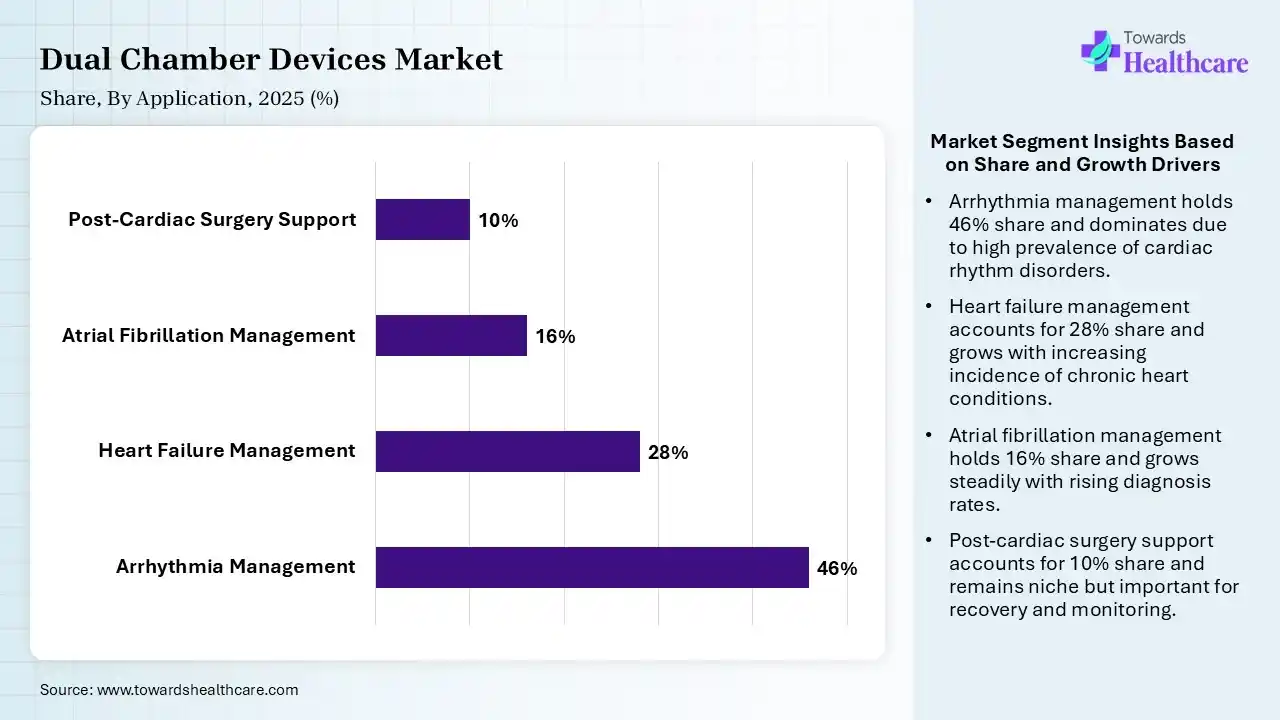

| Arrhythmia Management | 46% |

| Heart Failure Management | 28% |

| Atrial Fibrillation Management | 16% |

| Post-Cardiac Surgery Support | 10% |

The Arrhythmia Management Segment Led the Market in 2025 with the Largest Share

The arrhythmia management segment held a dominant share of the dual chamber devices market with a share of 46% in 2025 due to the high global prevalence of heart rhythm disorders such as atrial fibrillation. Increasing diagnosis rates, a growing aging population, and strong reliance on device-based therapies like pacemakers and defibrillators have driven demand. Additionally, continuous advancement in cardiac monitoring and treatment technologies has further strengthened the segment’s leading position in the market.

The heart failure management segment held the second-largest share of 28% of the market in 2025 and is expected to grow at the fastest CAGR of 6.80% in the market during the forecast period due to the rising global burden of heart failure and increasing need for advanced treatment options. While not as widespread as arrhythmias, heart failure cases often require complex device-based therapies like CRT. Growing awareness, improved diagnosis rates, and strong clinical benefits of these devices are supporting steady adoption, contributing to their significant position.

The atrial fibrillation management segment is growing, with a dual chamber devices market share of 16% due to the increasing prevalence of atrial fibrillation, especially among the aging population. Rising awareness, improved screening, and early diagnosis are boosting treatment rates. Additionally, advancements in device-based therapies and monitoring technologies, along with a higher risk of stroke associated with untreated AF, are driving demand for effective management solutions globally.

The post-cardiac surgery support segment is growing with shares of 10% in 2025 due to the increasing number of cardiac procedures, such as coronary artery bypass grafting and valve surgeries. Patients often require temporary pacing and rhythm management after surgery, driving demand for dual-chamber devices. Rising surgical success rates, improved postoperative care, and the need to prevent complications like arrhythmias are further supporting growth in this segment globally.

")

| Segment | Share 2025 (%) |

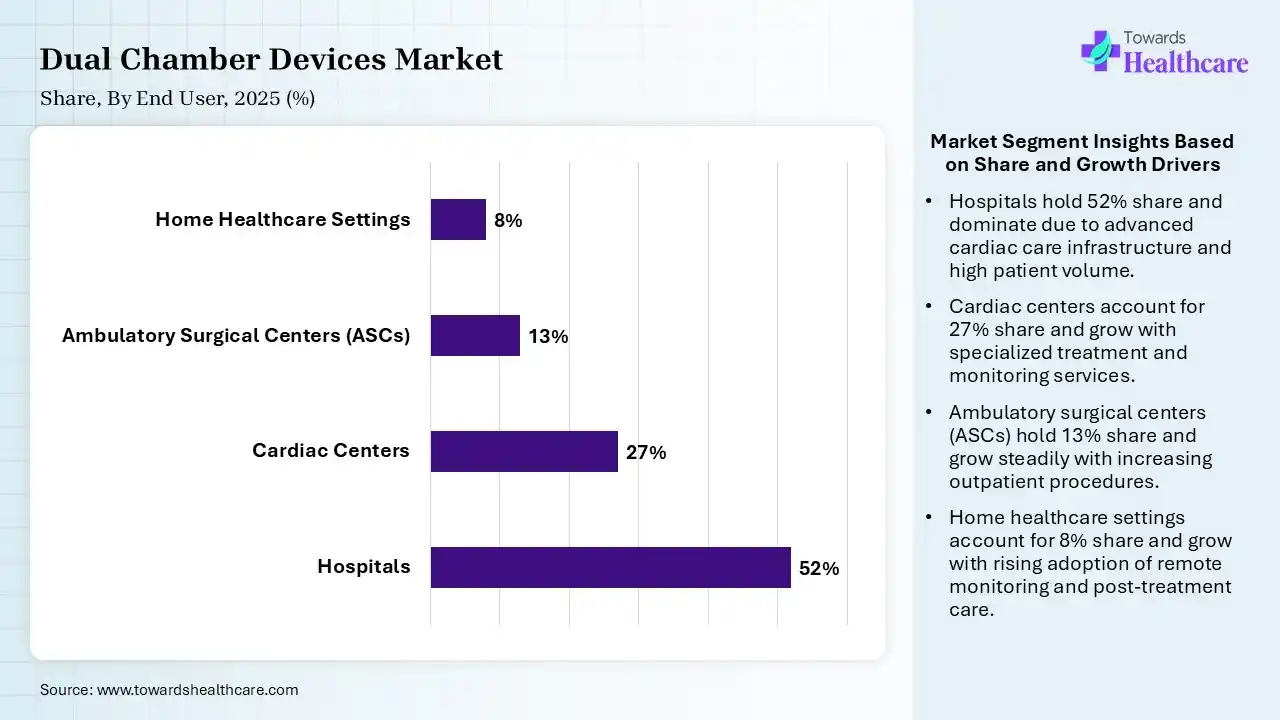

| Hospitals | 52% |

| Cardiac Centers | 27% |

| Ambulatory Surgical Centers (ASCs) | 13% |

| Home Healthcare Settings | 8% |

The Hospitals Segment Led the Market in 2025 with the Largest Share

The hospitals segment led the dual chamber devices market with a share of 52% in 2025 due to the availability of skilled cardiologists and the ability to perform complex procedures like device implantation and monitoring. Hospitals are primary centers for treating conditions such as arrhythmia and heart failure, ensuring high patient inflow. Additionally, better reimbursement policies, access to advanced technologies, and comprehensive post-procedure care further support their dominant market share.

The cardiac centers segment held the second-largest share of 27% of the market in 2025 and is expected to grow at the fastest CAGR of 6.70% in the market during the forecast period due to its specialized focus on diagnosing and treating heart conditions like arrhythmia. These centers offer advanced diagnostic tools, skilled, specialized, and efficient procedures at relatively lower costs than hospitals. Increasing patient preference for specialized care, shorter waiting times, and growing investments in defined cardiac facilities are driving their strong market presence.

The ambulatory surgical centers (ASCs) management segment is growing with shares of 16% in the dual chamber devices market in 2025 due to the rising preference for minimally invasive procedures and same-day discharge options. These centers offer cost-effective treatment, reduced hospital stays, and faster recovery, attracting both patients and providers. Increasing adoption of the device implantation procedure and improved infrastructure in outpatient settings are further driving demand, making ambulatory surgical centers an important and rapidly expanding end-user segment.

The home healthcare settings segment is expanding with a share of 8% in 2025 due to the growing demand for remote patient monitoring and convenient, cost-effective care. Patients with conditions such as heart failure prefer at-home management to reduce visits. Advancements in portable cardiac devices, telehealth integration, and improved patient comfort are further driving this trend, making home-based care an increasingly important segment in the dual chamber devices market.

")

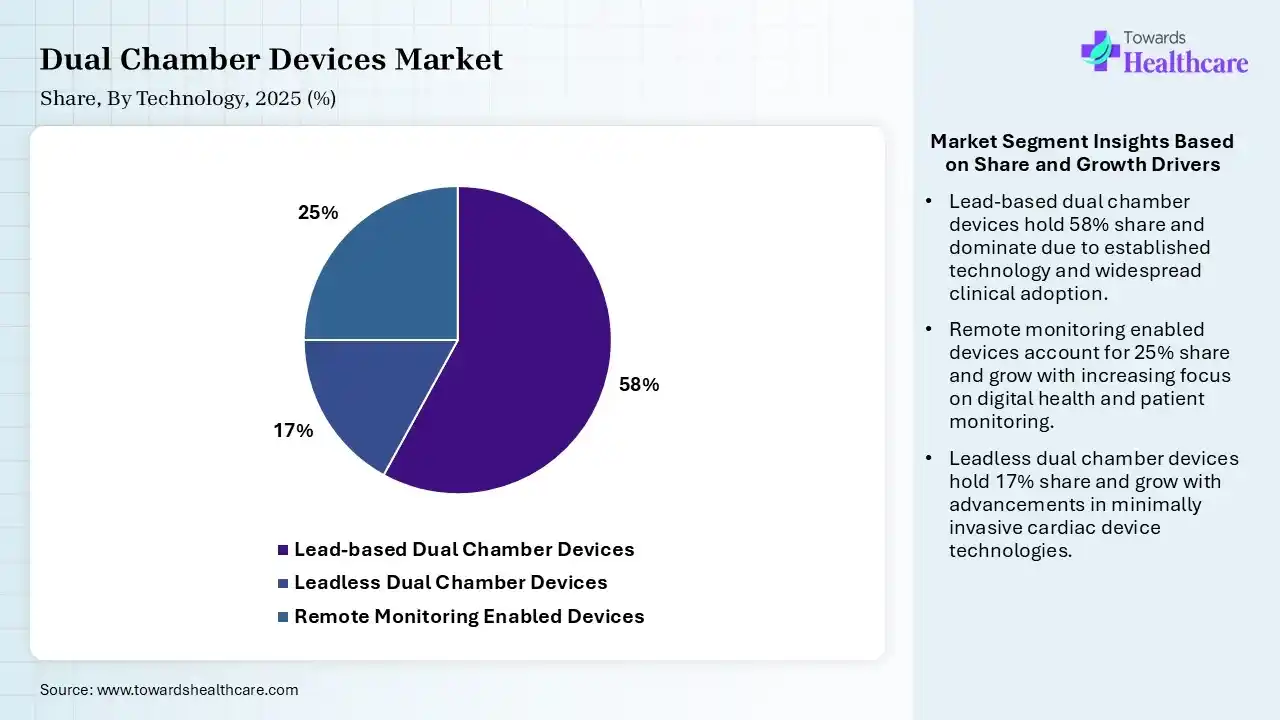

| Segment | Share 2025 (%) |

| Lead-based Dual Chamber Devices | 58% |

| Leadless Dual Chamber Devices | 17% |

| Remote Monitoring Enabled Devices | 25% |

The Lead-based Dual Chamber Devices Segment Led the Market in 2025 with the Largest Share

The lead-based dual chamber devices segment held a dominant share of 58% in 2025 due to their proven clinical reliability and widespread use in managing conditions like bradycardia. These systems provide precise atrial and ventricular coordination, ensuring effective pacing. Strong physician familiarity, established implantable procedure, and broader availability compared to newer technologies have supported their continued dominance in the market.

The remote monitoring enable devices segment held the second-largest share of 25% of the dual chamber devices market in 2025, due to increasing demand for continuous cardiac tracking and early detection of conditions like arrhythmia. These devices allow real-time data transmission, reducing hospital visits and improving patient management. Growing adoption of telehealth, enhanced patient convenience, and better clinical outcomes are key factors supporting their strong position in the market.

The leadless dual chamber devices segment held a 17% share in 2025 and is expected to grow at the fastest CAGR of 8.20% in the dual chamber devices market during the forecast period due to their minimally invasive nature and lower risk of complications such as infections and lead dislodgement. These devices eliminate the need for leads, improving patient comfort and recovery time. Increasing preference for advanced technologies, along with rising cases of arrhythmia, is further driving rapid adoption globally.

")

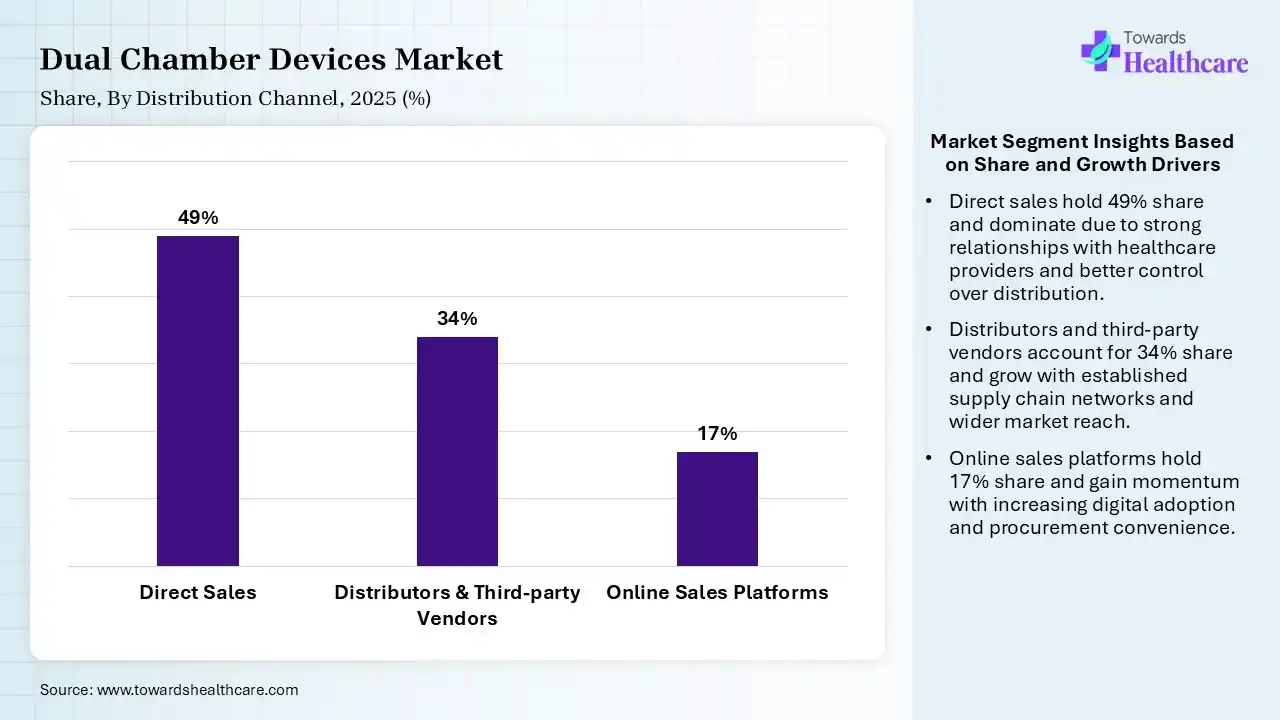

| Segment | Share 2025 (%) |

| Direct Sales | 49% |

| Distributors & Third-party Vendors | 34% |

| Online Sales Platforms | 17% |

The Direct sales Segment Led the Market in 2025 with the Largest Share

The direct sales segment led the dual chamber devices market with a share of 49% in 2025 due to strong relationships between manufacturers and healthcare providers, ensuring better pricing, customization, and after-sales support. Hospitals and cardiac centers prefer procurement for critical devices used in conditions like arrhythmia. Additionally, direct channels enable faster delivery, training support, and reliable supply chains, making them the preferred distribution mode in the market.

The distribution & third-party vendors segment held the second-largest share of 34% of the dual chamber devices market in 2025, due to their wide distribution networks and ability to reach smaller hospitals and clinics. These vendors offer flexible pricing, faster accessibility, and support for devices used in conditions like arrhythmia. Their role in expanding market penetration, especially in emerging regions, and ensuring consistent product availability is driving their strong position in the market.

The online sales platforms segment held a 17% share in 2025 and is expected to grow at the fastest CAGR of 7.30% in the dual chamber devices market during the forecast period due to increasing digitization and preference for convenient procurement channels. Online platforms offer easy product comparison, competitive pricing, and faster ordering for devices used in managing conditions like arrhythmia. Expanding e-commerce infrastructure, improved logistics, and growing acceptance of digital healthcare solutions are further accelerating adoption in this segment.

")

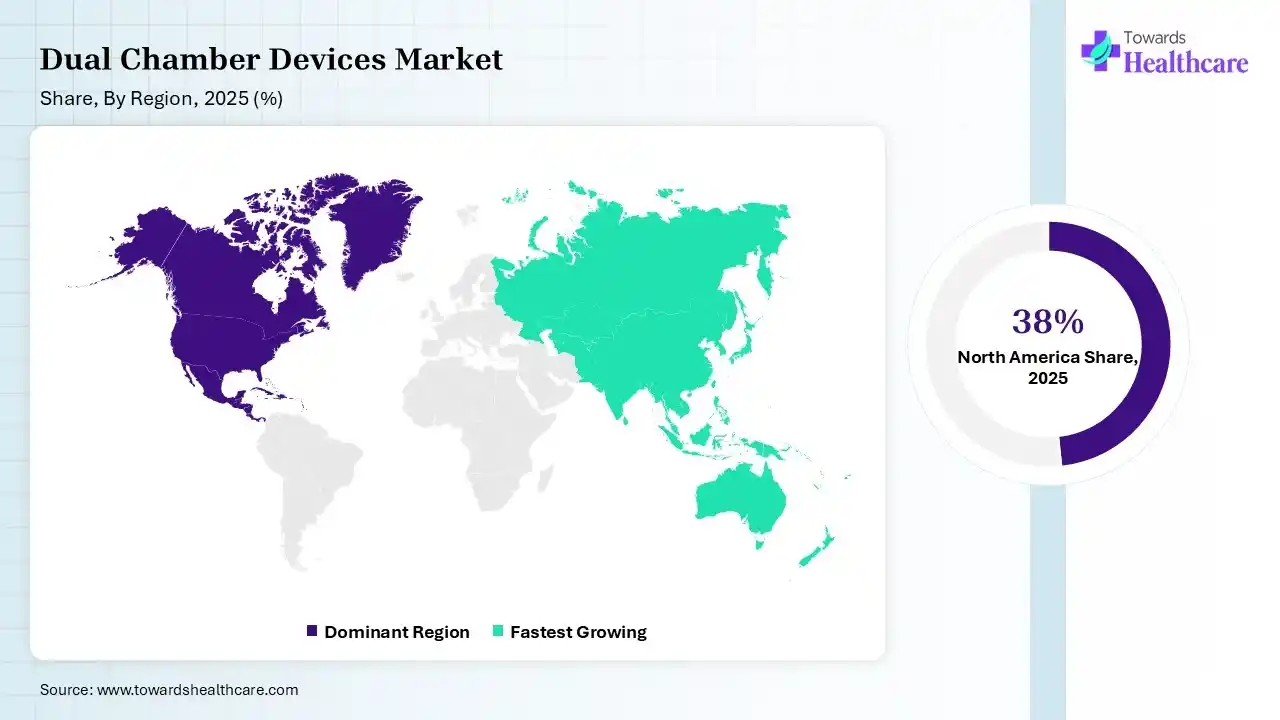

North America dominated the dual chamber devices market with a share of 38% in 2025 due to its well-established healthcare infrastructure, high adoption of advanced cardiac technologies, and strong presence of leading medical device companies. The region also faces a high prevalence of conditions like arrhythmia, supported by favorable reimbursement policies and early diagnosis rates. Additionally, the increasing geriatric population and continuous technological innovation further strengthened market growth.

U.S. Market Trends

The U.S. dual chamber devices market is expanding due to the high prevalence of cardiovascular conditions such as arrhythmia and heart failure. Advanced healthcare infrastructure, rapid adoption of innovative technologies, and strong support for reimbursements are key growth drivers. Additionally, an aging population, rising awareness, and continuous product advancements are further accelerating the adoption of dual-chamber devices across the country.

Canada Market Trends

The demand for cardiac therapies in Canada is rising steadily. In 2026, healthcare reports highlighted that nearly six million Canadians live with severe heart disease or stroke. This massive patient base drives the domestic need for dual-chamber pacemakers and implantable cardioverter-defibrillators. Hospitals prioritize dual-chamber variants to manage complex arrhythmias over traditional single-chamber options. Enhanced provincial funding for remote-monitoring applications further helps dual chamber device patients manage their health conditions from home.

Mexico Market Trends

Mexico faces an escalating burden of metabolic illnesses that severely impact cardiac health. Recent 2025 public health assessments indicate that ischemic heart disease continues to be the leading cause of mortality across the nation. This situation creates an urgent clinical need for dual-chamber synchronization systems to prevent sudden cardiac fatalities. Regional hospitals are rapidly integrating dual-chamber technology to improve patient therapeutic outcomes. Medical infrastructure upgrades in urban centers help expand local access to these specialized cardiac devices.

Asia Pacific held a significant market share of 22% and is anticipated to grow at the fastest CAGR of 7.20% in the dual chamber devices market during the forecast period due to improving healthcare infrastructure, rising healthcare expenditure, and increasing awareness of cardiac conditions such as arrhythmia. The regions’ large populations and growing patient pool are driving demand. Additionally, expanding access to advanced medical technologies and supporting government initiatives are accelerating adoption across emerging economies.

India Market Trends

India is expected to grow at a significant CAGR due to significant untapped market potential and low penetration of advanced cardiac devices. Increasing urbanization, rising disposable income, and improving insurance coverage are enabling more patients to access treatment for conditions like arrhythmia. Additionally, expansion of tier-2 and tier-3 healthcare facilities is further driving demand.

China Market Trends

China is experiencing a noticeable surge in cardiovascular conditions due to a rapidly aging demographic. National surveillance data from 2024 revealed a crude incidence rate of 620.33 per 100,000 for adult cardiovascular diseases. Dual chamber devices represent the largest and fastest-growing revenue segment within the domestic pacing market. Local medical centers are rapidly increasing their adoption of advanced dual-chamber leadless pacemakers. This rapid technology adoption helps optimize atrioventricular synchrony and heart rhythm regulation for patients nationwide.

Japan Market Trends

Japan possesses one of the oldest populations globally, which directly impacts its medical device utilization patterns. According to 2025 epidemiological projections, age-standardized heart failure and arrhythmia prevalence rates show continuous growth among senior citizens. This demographic reality creates a sustained domestic demand for implantable dual-chamber pacemakers. Japanese healthcare systems heavily prioritize dual-chamber setups to maintain natural heart function over single-chamber variants. These advanced pacing tools help structurally reduce long-term surgical complications for elderly individuals.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Medtronic, Abbott, Boston Scientific, BIOTRONIK | Develop pacing, sensing, telemetry, and leadless technologies |

| Product Manufacturers | Medtronic, Abbott, Boston Scientific, BIOTRONIK, LivaNova, MicroPort | Design and manufacture dual chamber pacemakers, ICDs, and CRT devices |

| Service Providers | Hospitals, Cardiac Centers, Electrophysiology Clinics | Implantation, monitoring, follow-up care |

| Platform Providers | Medtronic CareLink, Abbott Merlin.net, Boston Scientific LATITUDE | Remote monitoring and device management |

| CROs/CDMOs | NAMSA, ICON plc, IQVIA | Clinical trials, regulatory support, post-market surveillance |

| Software Vendors | Medtronic, Abbott, Boston Scientific | Device programming, remote diagnostics, data analytics |

| Research Institutions | Mayo Clinic, Cleveland Clinic, Stanford Medicine, Johns Hopkins | Clinical research and technology validation |

| End-User Industries | Healthcare Providers, Specialty Cardiac Centers | Clinical utilization and patient management |

R&D

Clinical Trials

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 78% | 17% | 5% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Medtronic | Dublin | Ireland | Global CRM market leader with extensive dual chamber pacemaker and ICD portfolio | Azure™, Advisa™, Micra AV™, CRT-D systems |

| Abbott Laboratories | Abbott Park, Illinois | USA | Pioneer in dual-chamber leadless pacing technology | AVEIR DR™, Assurity MRI™, Gallant ICDs |

| Boston Scientific Corporation | Marlborough, Massachusetts | USA | Major CRM supplier with broad pacing and ICD portfolio | ACCOLADE™, VITALIO™, ICD/CRT systems |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| MicroPort Scientific Corporation | Shanghai | China | Significant CRM business through MicroPort CRM | Pacemakers, ICDs, CRT devices |

| Lepu Medical Technology Co., Ltd. | Beijing | China | Growing cardiovascular device manufacturer | Implantable pacemakers and CRM solutions |

| Oscor Inc. | Palm Harbor, Florida | USA | Specialized cardiac rhythm management products | Leads, pacing technologies, CRM accessories |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Osypka Medical GmbH | Rheinfelden | Germany | Specialized pacing technology provider | Pacemaker systems and leads |

| MEDICO S.p.A. | Rubano, Padua | Italy | European implantable cardiac device manufacturer | Pacemakers and pacing leads |

| Shree Pacetronix Ltd. | Indore, Madhya Pradesh | India | One of the few Indian pacemaker manufacturers | Implantable dual chamber pacemakers |

Strengths

Weaknesses

Opportunities

Threats

In October 2025, “Nearly one in three patients who require a pacemaker in India need dual chamber pacing,” said Ajay Singh Chauhan, General Manager for Abbott’s Cardiac Rhythm Management business in India, Southeast Asia, Hong Kong, Taiwan, and Korea. “With AVEIR DR, we are expanding the benefits of leadless pacing to more people, offering a precise, minimally invasive, and technologically advanced solution for abnormal heart rhythms.”

By Device Type

By Application

By End User

By Technology

By Age Group

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar