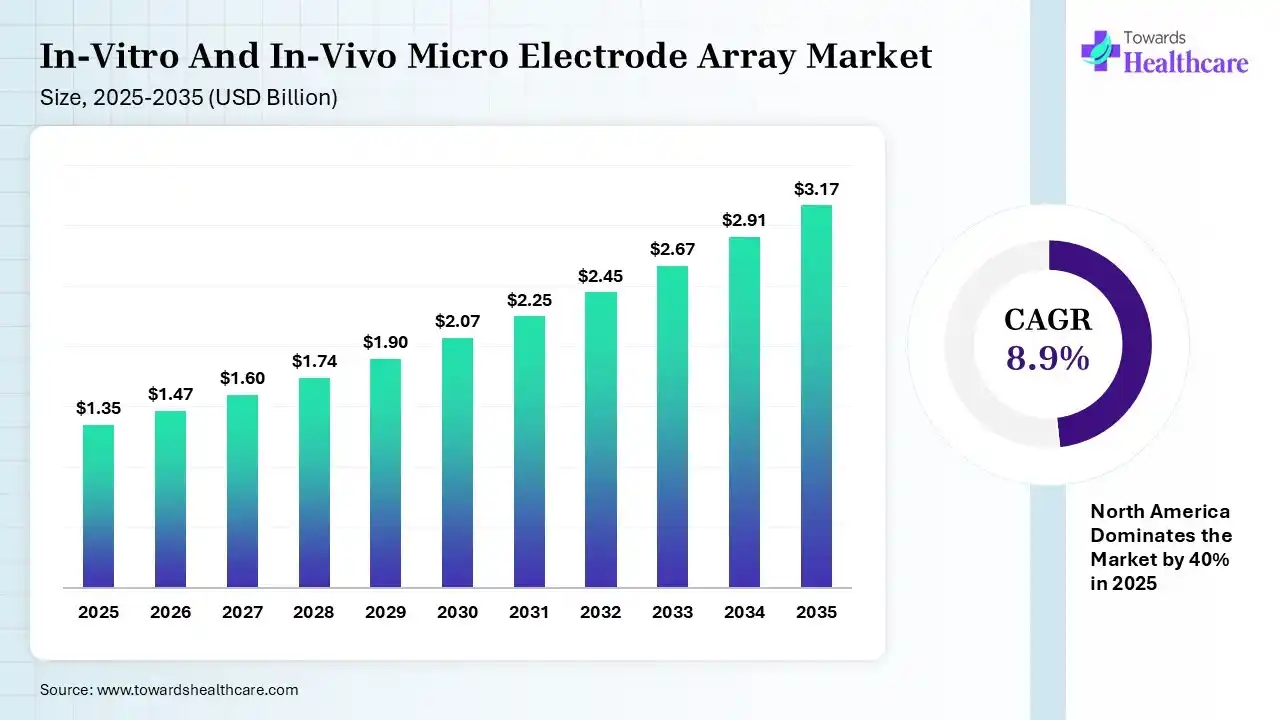

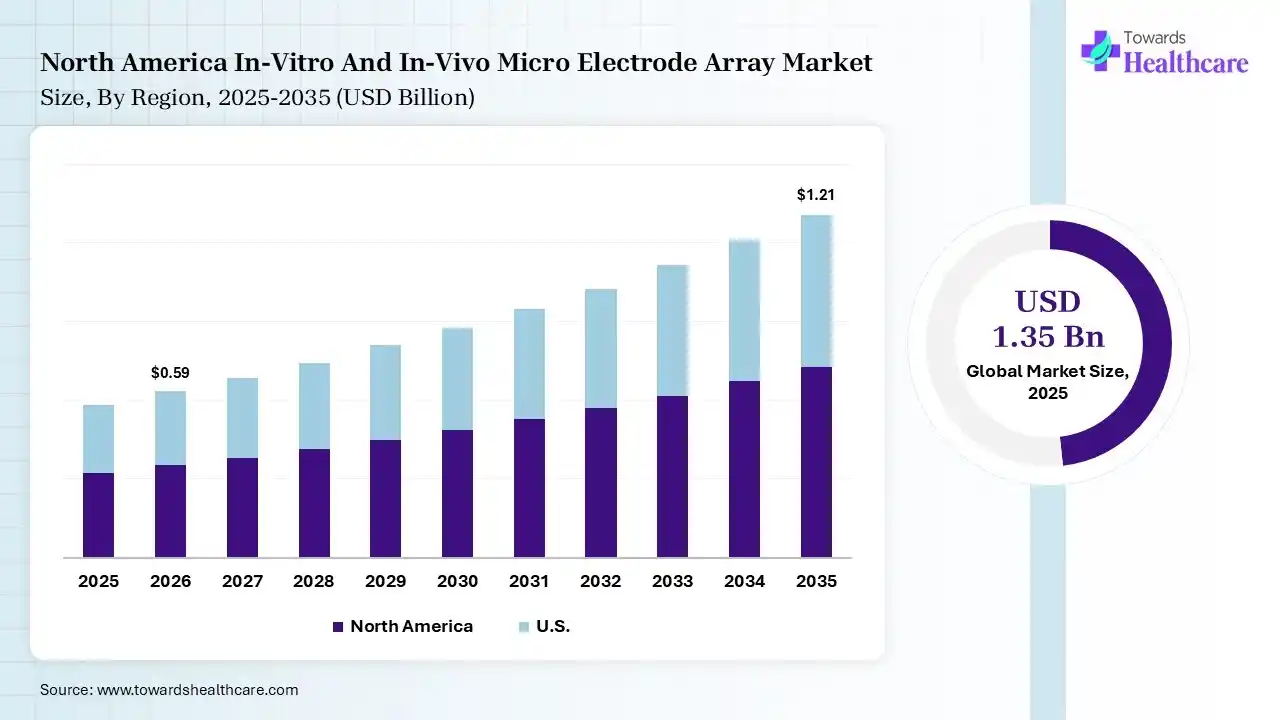

The global in-vitro and in-vivo micro electrode array market size was estimated at USD 1.35 billion in 2025 and is predicted to increase from USD 1.47 billion in 2026 to approximately USD 3.17 billion by 2035, expanding at a CAGR of 8.9% from 2026 to 2035. The worldwide rising neurological disorder cases and major advances in research activities drive the global market development. Eventual progressions in the market will explore flexible & soft electronics, along with the latest high-density probes.

")

The in-vitro and in-vivo micro electrode array market is defined as the wider adoption of devices comprising numerous microelectrodes to capture or stimulate neural electric signals. Specifically, in-vitro MEAs are employed to track cultured neurons on a dish for drug testing, whereas in-vivo MEAs are inserted into living brains to record neural activity for brain-machine interfaces. The globally surging significance of these devices in the study of neuronal pathology, physiology, & circuit connectivity, along with accelerating cases of Alzheimer’s, Parkinson’s, epilepsy, and ALS, is fueling the immense demand for MEA.

Primarily, AI has immersive applications across the global market, such as its algorithms, which allow real-time feedback loops by assessing neural activity & responding with accurate electrical/optical stimulation to guide network progression or plasticity. Alongside, various research activities have expanded by utilizing MEAs cultured with in-vitro neural networks as biological brains for robots, while AI assists in decoding motor intent for complex motion control tasks.

Exploring 3D & Organoid Integration

Gradually, the market is enforcing the evolution of 3D MEAs, i.e., nanovolcanoes, mesh structures, enabling recording from complex tissue models & brain organoids.

Advancing Flexible & Soft Electronics

Researchers are increasingly focusing on the transformation of flexible, polymer-based probes to lower chronic inflammation & mechanical mismatch with soft brain tissue, which raises the lifespan of implants.

Reinforcing High-Density Probes

A prominent step towards thousands of recording sites for simultaneous brain-wide recording of neural populations is also empowering prospective research activities.

| Table | Scope |

| Market Size in 2026 | USD 1.47 Billion |

| Projected Market Size in 2035 | USD 3.17 Billion |

| CAGR (2026 - 2035) | 8.9% |

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Material, By Application, By End-User, By Region |

| Top Key Players | Axion BioSystems, Inc., MaxWell Biosystems AG, 3Brain AG, Blackrock Neurotech, Multi Channel Systems MCS GmbH, Med64 (Alpha MED Scientific), Plexon Inc., NeuroNexus Technologies, Inc., Tucker-Davis Technologies, Inc., Harvard Bioscience Inc. |

")

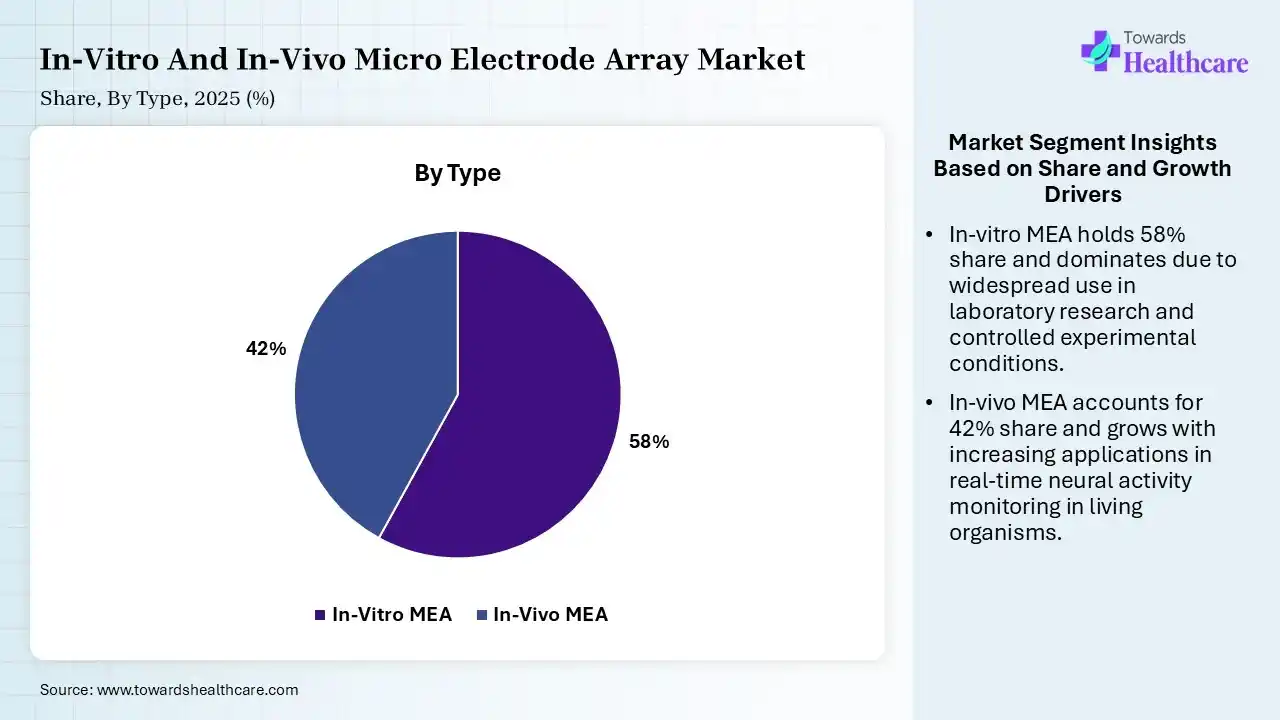

| Segment | Share 2025 (%) |

| In-Vitro MEA | 58% |

| In-Vivo MEA | 42% |

The In-Vitro MEA Segment Dominated the Market in 2025

The in-vitro MEA segment held a major share of 58% of the in-vitro and in-vivo micro electrode array market in 2025. Key drivers are the increasing need for non-invasive, long-term, high-throughput monitoring of neural & cardiac networks for drug discovery & disease modeling. The latest trend includes 3D MEAs, which support monitoring brain organoids & 3D tissues, further enabling structure to conform to the tissue for extensive interface.

Moreover, the in-vivo MEA segment held the second-largest share of a 42% in 2025 & is predicted to expand at 9.80% CAGR. Broadening neuroscience research & diagnostics, like recognising complex brain functions & assessment of neurological disorders, drives the demand for this kind of MEA. Also, this type is pivotal in the translation of neural activity into control signals for neuroprosthetics. Ongoing efforts are fostering multifunctional 3D MEAs for optogenetic stimulation/drug delivery, & self-folding ‘Kirigami’ sensors for 3D organoids.

")

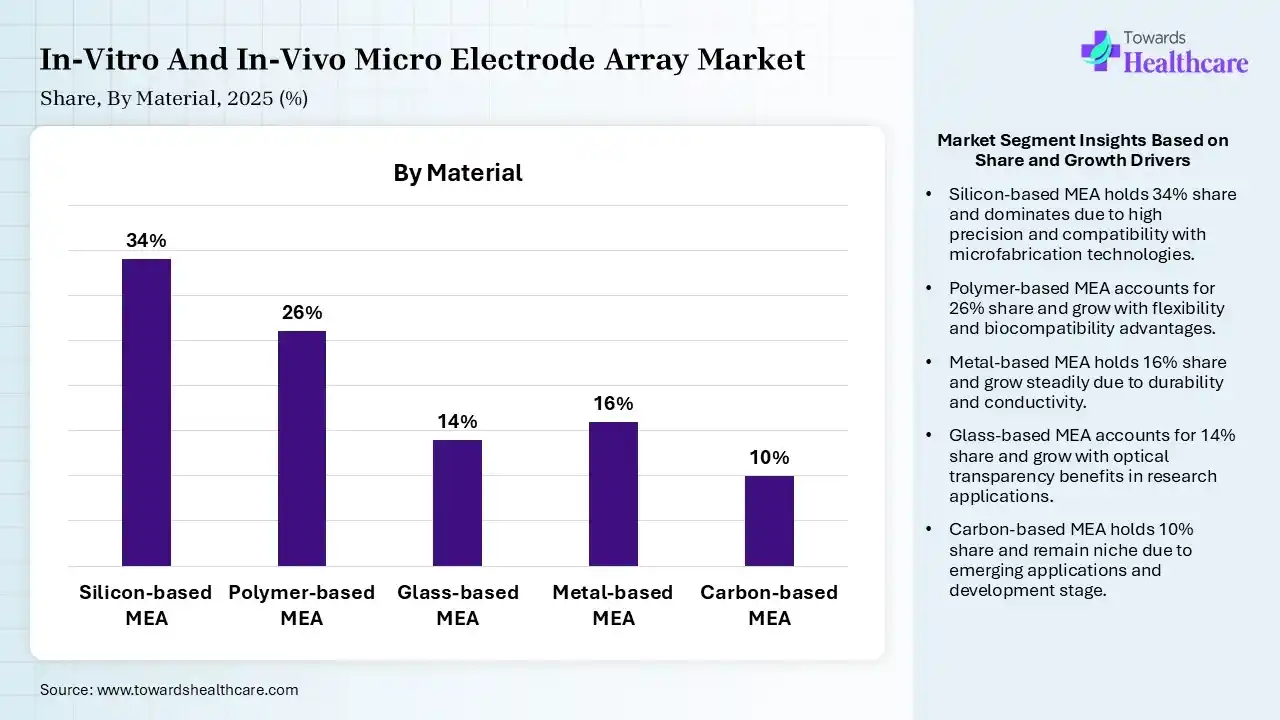

| Segment | Share 2025 (%) |

| Silicon-based MEA | 34% |

| Polymer-based MEA | 26% |

| Glass-based MEA | 14% |

| Metal-based MEA | 16% |

| Carbon-based MEA | 10% |

The Silicon-Based MEA Segment Led the Market in 2025

In 2025, the silicon-based MEA segment dominated with a 34% of the in-vitro and in-vivo micro electrode array market. Dominance is propelled by its significant properties, including high-density, precise, & scalable interfaces for neural recording & stimulation in neuroscience & clinical purposes. A breakthrough encompasses the use of amorphous silicon carbide & Parylene-C coatings, which assist in highlighting immune responses & insulation degradation.

Whereas the polymer-based MEA segment captured the second largest share of a 26% share in 2025 & is estimated to expand at 10.20% CAGR. This material type has rigorous mechanical flexibility, substantial biocompatibility, & minimal foreign body response. Nowadays, the globe is seeking PEDOT: PSS-based micro-electrocorticography (µECoG) arrays that provide low impedance & lowered distortion in high-magnetic field (9.4 T) MRI.

The metal-based MEA segment accounted for 16% share of the in-vitro and in-vivo micro electrode array market. Particularly, platinum, gold, or iridium oxide offers superior charge transfer, with minimal signal distortion. Additionally, optimizing MEMS (Micro-Electro-Mechanical Systems) & photolithography.

The glass-based MEA segment held 14% share of the market in 2025, due to its transparency, which offers imaging integration in research. Alongside, stable substrates are supporting long-term experiments, & these MEAs have a major role in in-vitro applications.

")

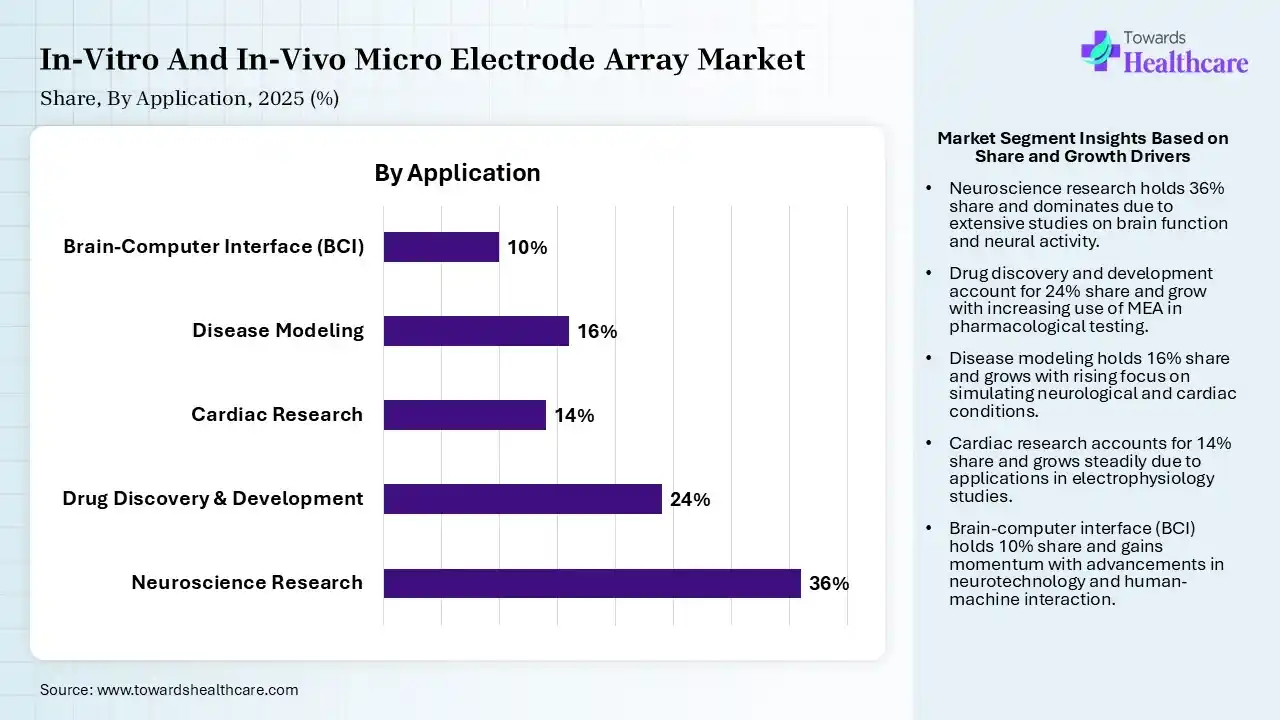

| Segment | Share 2025 (%) |

| Neuroscience Research | 36% |

| Drug Discovery & Development | 24% |

| Cardiac Research | 14% |

| Disease Modeling | 16% |

| Brain-Computer Interface (BCI) | 10% |

The Neuroscience Research Segment Was Dominant in the Market in 2025

The neuroscience research segment captured a 36% share of the market in 2025. Significantly rising instances of diverse neurological issues, like Alzheimer's, Parkinson’s, and epilepsy, are demanding reliable platforms for high-throughput screening of drugs & in vitro modeling of neural networks. Consistent research includes the use of Platinum-black-coated vertical nanoneedles or microholes to penetrate cells or evolve tight-junctions.

However, the drug discovery & development segment held 24% share of the in-vitro and in-vivo micro electrode array market. A major driver is that MEA allows expedited, functional screening of drug effects on network-level activity, offering predictive safety pharmacology & disease modeling& this finally surges compound improvement.

The disease modeling segment held 16% of the market share and is anticipated to expand at 9.4% CAGR in the coming era. Along with a rise in demand for non-invasive & long-term monitoring approaches, patient-derived models are supporting researchers to map disease phenotypes & evaluate drug responses in real time. Moreover, the latest HD-MEAs are facilitating numerous recording sites on a single chip with micro-pitch spacing.

The cardiac research segment captured a 14% share in 2025, due to the accelerating cardiovascular studies. Also, immersive electrophysiology is assisting drug safety, coupled with the advanced clinical trials, which are bolstering applications of MEAs.

")

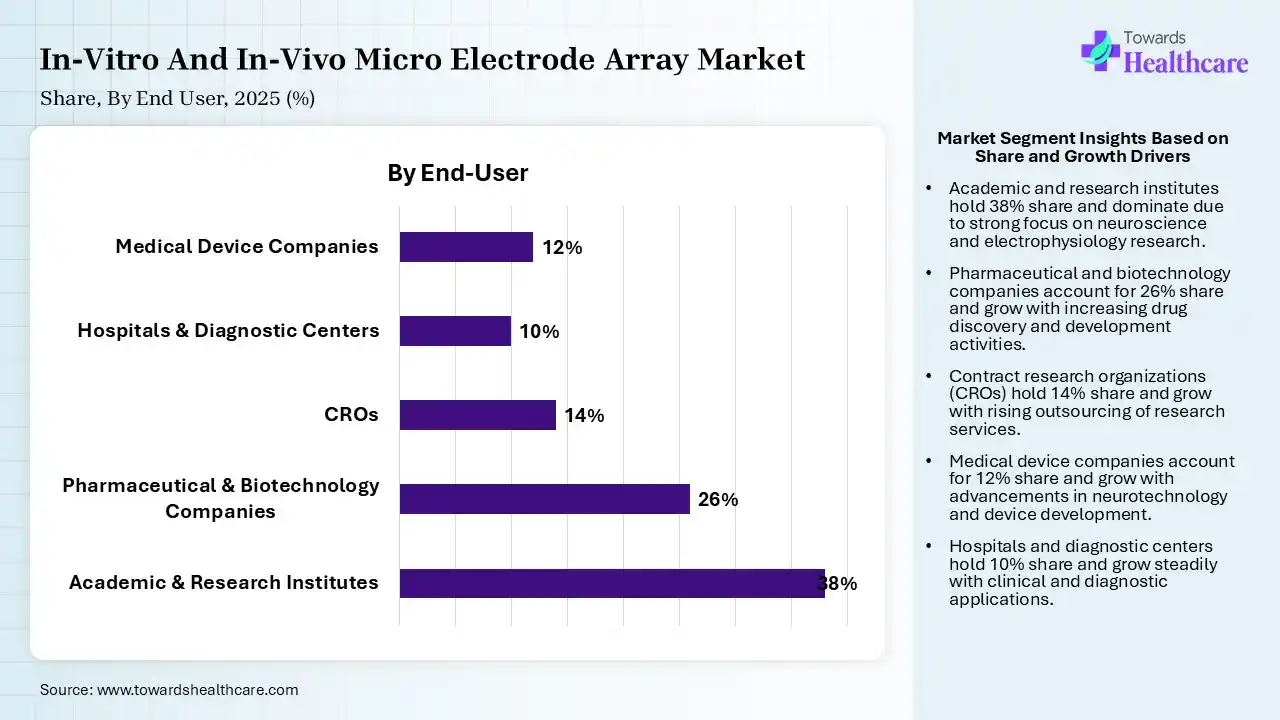

| Segment | Share 2025 (%) |

| Academic & Research Institutes | 38% |

| Pharmaceutical & Biotechnology Companies | 26% |

| CROs | 14% |

| Hospitals & Diagnostic Centers | 10% |

| Medical Device Companies | 12% |

The Academic & Research Institutes Segment Dominated the Market in 2025

In 2025, the academic & research institutes segment led with a 38% share of the in-vitro and in-vivo micro electrode array market. Their dominance is propelled by continuous innovation activities in 3D and high-density (HD) MEAs, with the development of innovative electrode materials. Several institutes are facilitating specialized expertise to validate MEA-based drug screening platforms.

The pharmaceutical & biotechnology companies segment held 26% share in 2025, due to growing neurological research, drug discovery, & adoption of high-throughput screening. This mainly covers Axion BioSystems, MaxWell Biosystems, Multi Channel Systems (MCS), 3Brain AG, & Blackrock Neurotech, which extensively specialize in MEA.

The contract research organizations (CROs) segment held 14% of the market share in 2025 and is predicted to show rapid growth at 9.70% CAGR. CROs are generalists, specialized & industrial-scale providers that provide in-vitro & in-vivo MEA services, including neurotechnology platforms, engaged in clinical and preclinical development, etc. Also, CROs are emphasizing functional, non-invasive, long-term monitoring of iPSC-derived neuronal & cardiac cell cultures.

")

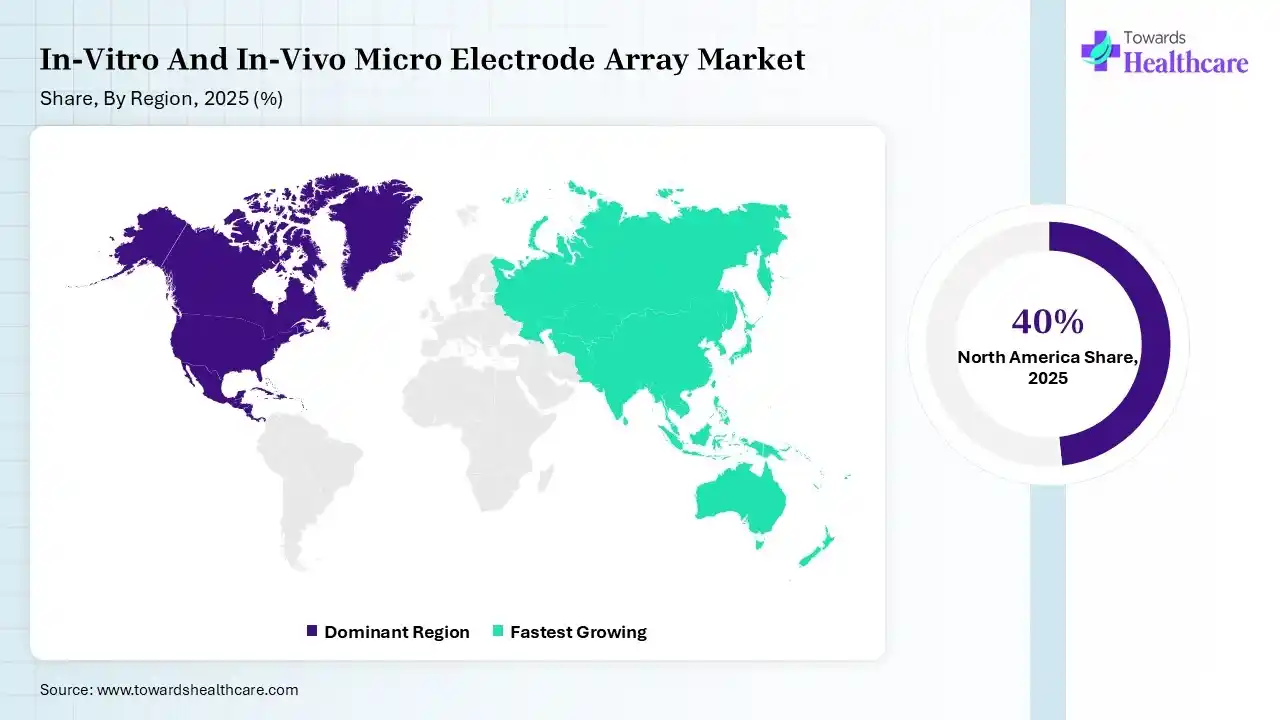

North America registered dominance with 40% share of the in-vitro and in-vivo micro electrode array market. The regional expansion is driven by a well-developed R&D ecosystem, with increased funding, which supports innovations & advanced research, respectively. Besides this, the region is promoting early adoption of neurotechnology, which impacts the overall progression.

For instance,

U.S. Market Trends

The U.S. market captured a dominant share of 32% in 2025, due to its leading neuroscience research institutions & the presence of major leaders. Also, the U.S. is fostering the use of machine learning algorithms for real-time spike sorting, data processing, & analysis of massive datasets developed by high-density, multi-channel recordings.

Asia Pacific captured 22% of the market share and is anticipated to expand fastest at 10.20% CAGR in the in-vitro and in-vivo micro electrode array market. This is mainly spurred by faster strengthening of research infrastructure & neurotechnology through the robust investments, with the surging pharma sector, specifically in China, Japan, & India. Also, APAC is broadening the application of in-vitro MEAs for high-throughput screening in drug development, with the expansion of pre-clinical trials.

For instance,

China Market Trends

China is predicted to expand rapidly, as its studies are focusing on the use of MEAs to model epilepsy in hippocampal slices to recognize epileptiform activities. Moreover, China market is demonstrating improvements with platinum nanoparticles (PtNPs) or carbon nanotubes & sensitivity.

| Companies | Description |

| Axion BioSystems, Inc. | Its offerings cover in-vitro microelectrode array (MEA) solutions focused on its Maestro MEA platform. |

| MaxWell Biosystems AG | They are highly emphasizing in-vitro high-density microelectrode array (HD-MEA) technology. |

| 3Brain AG | This firm specialises in high-density microelectrode arrays relied on CMOS (complementary metal-oxide-semiconductor) technology. |

| Blackrock Neurotech | A company offers Utah Array technology, which is ideal for both in-vivo & in-vitro research applications. |

| Multi Channel Systems MCS GmbH | This leader facilitates a comprehensive suite of microelectrode array (MEA) solutions for both in vitro & in vivo electrophysiology. |

| Med64 (Alpha MED Scientific) | Its brand highly provides solutions for extracellular electrophysiology in cell cultures & tissue slices. |

| Plexon Inc. | Its offerings cover specialized 3D arrays, active CMOS probes, & unified stimulation systems. |

| NeuroNexus Technologies, Inc. | This firm provides solutions from high-density penetrating silicon probes to flexible surface grids & specialized 3D arrays. |

| Tucker-Davis Technologies, Inc. | A player focuses on comprehensive hardware & software approaches for microelectrode array (MEA) interfacing. |

| Harvard Bioscience Inc. | Their offerings feature cutting-edge Mesh MEA technology for organoids, with traditional planar and 3D arrays. |

Strengths

Weaknesses

Opportunities

Threats

By Type

By Material

By Application

By End-User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar