Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

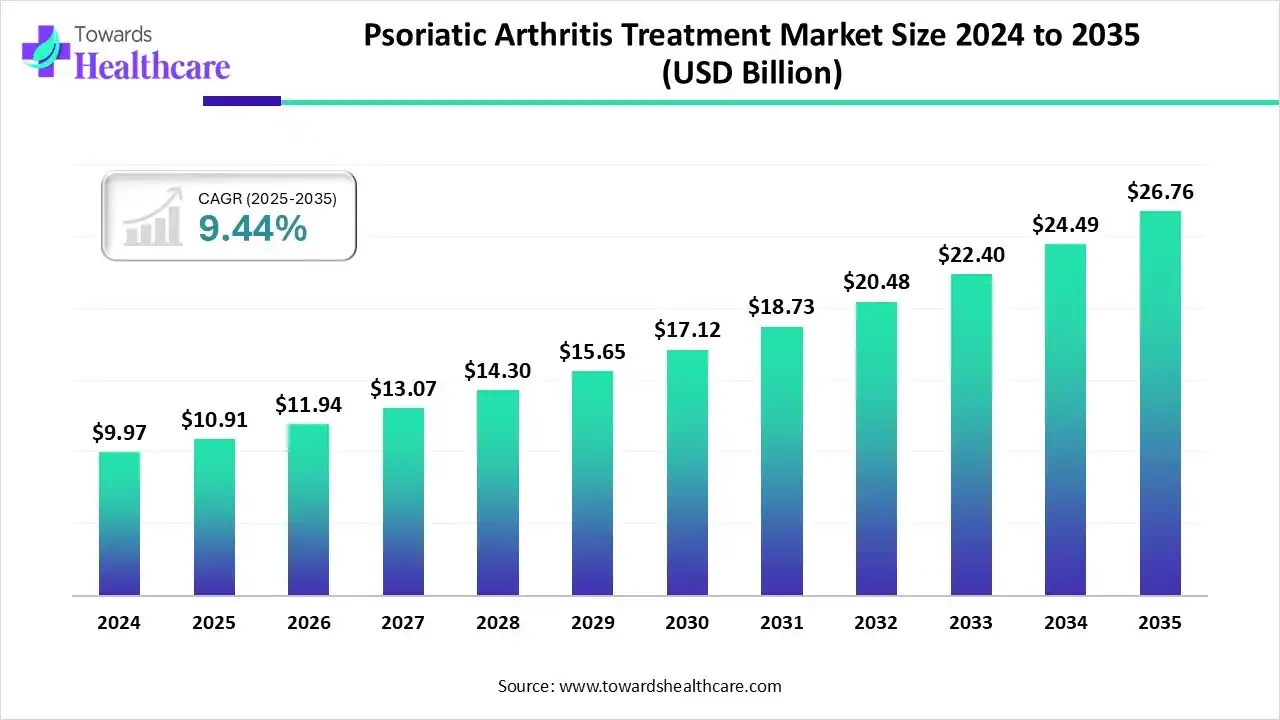

The global psoriatic arthritis treatment market size is calculated at USD 10.91 billion in 2025, grew to USD 11.94 billion in 2026, and is projected to reach around USD 26.76 billion by 2035. The market is expanding at a CAGR of 9.44% between 2026 and 2035.

The psoriatic arthritis treatment market is primarily driven by the increasing prevalence of psoriasis and the growing development of immunotherapy drugs. As patients are more aware of early diagnosis, healthcare professionals are encouraged to provide early intervention. Favorable reimbursement policies and increasing healthcare expenditure contribute to market growth. Artificial intelligence (AI) revolutionizes the diagnosis and treatment of psoriatic arthritis (PsA).

The psoriatic arthritis treatment market is experiencing robust growth, driven by the rising prevalence of psoriasis, the shifting trend toward personalized medicines, and technological innovations. It covers approved and late-stage therapies used to prevent and control musculoskeletal and cutaneous manifestations of PsA, including pain, joint swelling/erosion, enthesitis, dactylitis, axial disease, and skin psoriasis.

The market includes conventional therapies (NSAIDs, corticosteroids), conventional synthetic DMARDs, biologic DMARDs (TNF, IL-17, IL-23, etc.), targeted synthetic DMARDs (JAK / TYK inhibitors), combination regimens, delivery formats (injectable, infusion, oral), and related services (diagnostics, specialty pharmacy, monitoring).

AI can play a crucial role in managing PsA by predicting treatment outcomes and guiding more informed therapeutic decision-making. This helps healthcare professionals to provide personalized treatment. AI and machine learning (ML) algorithms can analyze vast amounts of data and suggest appropriate treatment based on patients’ symptoms. They can also determine different stages of diseases with high accuracy and precision.

For instance,

| Table | Scope |

| Market Size in 2026 | USD 11.94 Billion |

| Projected Market Size in 2035 | USD 26.76 Billion |

| CAGR (2026 - 2035) | 9.44% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Clinical Manifestation, By Route of Administration & Delivery, By Patient Setting/End-User, By Region |

| Top Key Players | Eli Lilly and Company, UCB, Amgen, Inc., Bristol Myers Squibb, Roche/Genentech, Sun Pharmaceuticals Ltd., Biocon, Gilead Life Sciences, Alvotech |

| Sub-Segment | Market Share (%) |

| Biologic DMARDs | 51% |

| Targeted Synthetic DMARDs (tsDMARDs/JAK/TYK inhibitors) | 20% |

| Conventional Synthetic DMARDs | 15% |

| Adjunctive/Symptomatic Therapies (NSAIDs, corticosteroids, analgesics) | 14% |

Explanation:

Which Drug Class Segment Dominated the Psoriatic Arthritis Treatment Market?

The biologic DMARDs segment held a dominant presence in the market in 2025, with an 51% share due to the growing need for targeted treatment and reduced side effects. Biologic disease-modifying anti-rheumatic drugs (DMARDs) are highly specific and target a particular pathway of the immune system. They offer superior benefits compared to conventional DMARDs, including a faster onset of action and improved symptoms. These drugs directly target the immune system, reducing inflammation, pain, and joint damage.

Targeted Synthetic DMARDs

The targeted synthetic DMARDs segment is expected to grow at the fastest CAGR in the market during the forecast period. JAK inhibitors and tyrosine kinase inhibitors are some examples of targeted synthetic DMARDs. These drugs are widely preferred because they can be administered orally. Newer drugs are developed to selectively target IL-17, IL-23, and other receptors. They are comparatively cost-effective, enhancing patient convenience.

Adjunctive/Symptomatic Therapies

The adjunctive/symptomatic therapies segment is expected to grow in the coming years, due to the need for relieving symptoms and improving the quality of life of individuals. Adjuvant therapies for PsA include NSAIDs, corticosteroids, and non-pharmacological treatment. They complement PsA therapeutics and provide synergistic effects.

| Sub-Segment | Market Share (%) |

| Peripheral arthritis | 50% |

| Axial psoriatic disease/spondylitis | 20% |

| Enthesitis | 12% |

| Dactylitis | 10% |

Explanation:

Why Did the Peripheral Arthritis Segment Dominate the Psoriatic Arthritis Treatment Market?

The peripheral arthritis segment held the largest revenue share of 50% of the market in 2025. This segment dominated because peripheral arthritis is one of the major clinical features and can exist in various patterns. Peripheral arthritis refers to the inflammation of the joints in the hands, wrists, feet, ankles, and knees. It is a potentially debilitating feature of PsA, necessitating its early treatment. Treatment focuses on reducing symptoms and preventing damage progression.

Axial Psoriatic Disease/Spondylitis

The axial psoriatic disease/spondylitis segment is expected to grow with the highest CAGR in the market during the studied years. Axial psoriatic disease occurs in 25% to 70% of patients with PsA. It results in worse arthritis and psoriasis as measured by several clinical variables compared with nonaxial patients. Treatment plans for this condition are based on evidence from patients with axial spondyloarthritis, including biologics.

Enthesitis

The enthesitis segment is expected to grow at a notable CAGR. Enthesitis is the inflammation of the sites where tendons, ligaments, and joint capsules attach to bones. Symptoms include pain and stiffness, especially when the body part is moved. Enthesitis is also considered a root cause of some common orthopedic problems, such as tennis elbow. It is estimated that over 40% of PsA patients suffer from enthesitis.

| Sub-Segment | Market Share (%) |

| Parenteral (subcutaneous injectables, IV infusions) | 70% |

| Oral (small-molecule JAK/TYK inhibitors) | 25% |

| Topical (adjunctive for skin symptoms) | 5% |

Explanation:

What Made Parenteral the Dominant Segment in the Psoriatic Arthritis Treatment Market?

The parenteral segment accounted for the highest revenue share of 70% of the market in 2025, due to faster onset of action, higher bioavailability, and reduced systemic side effects. Biologics are delivered through the parenteral route, such as subcutaneous and i.v. Infusions. They completely bypass the digestive system, thereby delivering drugs into body fluids. Drugs are absorbed more quickly and provide the desired action at the target site.

Oral

The oral segment is expected to expand rapidly in the market in the coming years. The oral route is more convenient and affordable than injectable medicines. Oral drugs can be administered to patients of all age groups. Tablets are available in various forms, including sustained release and immediate release. The oral route is generally safe, simple, convenient, and non-invasive. Patients do not need skilled professionals for drug administration.

Topical

The topical segment is expected to show lucrative growth due to the growing demand for targeted treatment and patient convenience. Drugs are available in creams, gels, and ointments that are applied to the skin. They are delivered into the body fluids through the skin layers. As PsA is an inflammatory disorder, topical drugs can help relieve inflammatory symptoms and swelling.

| Sub-Segment | Market Share (%) |

| Specialist rheumatology clinics & hospitals | 60% |

| Dermatology clinics (skin-dominant cases) | 15% |

| Outpatient infusion centres/specialty pharmacies | 15% |

| Primary care (diagnosis, early management, referrals) | 10% |

Explanation:

Which Patient Setting/End-User Segment Led the Psoriatic Arthritis Treatment Market?

The specialist rheumatology clinics & hospitals segment led the market in 2025, with a share of approximately 60% due to favorable infrastructure and the availability of specialized equipment. Clinics and hospitals have skilled professionals who provide personalized treatment to patients. Favorable reimbursement policies also encourage patients to visit rheumatology clinics and hospitals. Hospitals and clinics are also part of clinical trials, benefiting patients by receiving novel therapeutics before market approval.

Outpatient Infusion Centers/Specialty Pharmacies

The outpatient infusion centers/specialty pharmacies segment is expected to witness the fastest growth in the market over the forecast period. Outpatient centers save a lot of costs for patients as they do not need to stay overnight. Specialty pharmacies possess the required facilities to store and manage innovative PsA therapeutics. Pharmacists guide patients about the dose and drug delivery of biologics.

Primary Care

The primary care segment is expected to grow significantly, due to the increasing awareness of screening and early diagnosis of PsA. Healthcare professionals manage PsA at an initial stage through NSAIDs and other over-the-counter (OTC) medications to manage mild symptoms. They also suggest lifestyle changes and screen for joint involvement. They can refer to specialized professionals for advanced treatment.

| Region | Market Share (%) |

| North America | 42% |

| Europe | 30% |

| Asia-Pacific | 18% |

| Latin America | 6% |

| Middle East & Africa | 4% |

Explanation:

North America dominated the global market in 2025, with a revenue of 42% share. The availability of a robust healthcare infrastructure, the rising prevalence of autoimmune disorders, and the presence of key players are the factors that govern market growth in North America. Favorable regulatory policies and the rising adoption of advanced technologies propel the market. Government and private organizations provide funding for conducting advanced research activities.

Increasing Prevalence Fuels the U.S. Growth

Key players, such as Pfizer, Johnson & Johnson, and AbbVie, are the major contributors to the market in the U.S. About 8 million people live with psoriasis, of which approximately 3.3 million people in the U.S. live with PsA. In September 2025, the U.S. FDA approved Tremfya (guselkumab) for the treatment of children six years or older with PsA.This FDA approval will benefit 14,000 American children who are impacted by PsA.

Asia-Pacific is expected to grow at the fastest CAGR in the market during the forecast period. The market is driven by increasing R&D investments and growing research and development activities. Companies in China and India primarily focus on manufacturing biosimilars for PsA treatment to cater to a wide range of the population, providing affordable medications. The rapidly expanding clinical trial infrastructure is attracting foreign companies to conduct clinical trials in the region.

India - The Global Destination for Medical Tourism

The prevalence rate of PsA in India ranges from 0.44% to 8.7% in patients with psoriasis. The burgeoning medical tourism sector attracts foreign patients for affordable and advanced treatment in India. India has expertise in complementary therapies, such as acupuncture, massage therapy, dietary supplements, and herbal remedies. Approximately 2 million patients visit India every year for medical treatment.

Europe is expected to grow at a considerable CAGR in the upcoming period. Government organizations launch initiatives to screen for and diagnose autoimmune disorders. The Horizon Europe’s iPROLEPSIS project aims to transform the early detection, diagnosis, and treatment of PsA by using AI and different types of biological data. The European Medicines Agency (EMA) regulates the approval of PsA therapeutics in Europe. The increasing prevalence of PsA and technological innovations boost the market.

Biosimilar Boom Contributes to the UK’s Growth

A recent comprehensive analysis and modelling study found that the incidence of PsA in patients with psoriasis varied from 2.31 per 1000 person-years in the UK. The shifting trend toward biosimilars fosters market growth. The NHS England estimated that the broader adoption of biosimilars, including those for ustekinumab, could generate up to £1 billion in savings by 2028.

South America's psoriatic arthritis treatment sector is witnessing a strong expansion. Improved healthcare access and growing patient awareness drive the demand for advanced therapies like biologics. Expanding insurance coverage is making expensive, effective treatments more readily available to a larger patient population.

Brazil: Biologics Lead the Charge

The Brazilian market is experiencing notable momentum, primarily fueled by the increasing adoption of advanced biologic drugs. A rising prevalence of the disease, combined with enhanced diagnostic capabilities, contributes significantly to the market growth in this key Latin American nation.

The Middle East and Africa region demonstrates a robust growth trajectory. Improved healthcare infrastructure and increasing patient education are key factors. The market sees a rising demand for targeted therapies, including novel small molecules, reflecting a push toward more effective and specialized treatment options.

GCC Nations Drive Upscale Demand

The Gulf Cooperation Council countries are a high-value, growing segment. Elevated healthcare spending and the swift regulatory approval of cutting-edge therapies ensure patients receive the newest treatments. The availability of high-cost biologics is a major component of this sophisticated market's latest expansion.

Company Overview: A global, research-based biopharmaceutical company focused on developing and commercializing advanced therapies, with Immunology as its largest and most strategic revenue-driving franchise. It is actively and successfully navigating the loss of exclusivity for Humira by aggressively growing its next-generation PsA treatments.

Corporate Information:

History and Background: Established as an independent entity focused on specialty pharmaceuticals. Its history is defined by the massive success of Humira (adalimumab) in the PsA and autoimmune space. The current phase is marked by a focus on diversifying and driving market adoption of its successor products, Skyrizi and Rinvoq.

Key Milestones/Timeline:

Key Offerings:

Key Developments and Strategic Initiatives:

Mergers & Acquisitions:

Partnerships & Collaborations:

Feb 2024: Collaboration with Tentarix to develop conditionally-active, multi-specific biologics for both Oncology and Immunology.

Product Launches/Innovations:

Capacity Expansions/Investments:

Announced plans for a $195 million investment in a new U.S. manufacturing facility, part of a $10 billion decade-long strategy to expand U.S. biopharmaceutical manufacturing capabilities.

Regulatory Approvals:

Technological Capabilities/R&D Focus:

Strengths & Differentiators:

SWOT Analysis:

Recent News and Updates:

Press Releases:

Company Overview: A focused global healthcare company specializing in Innovative Medicine (Janssen) and MedTech. The Janssen division is a major force in the PsA market, focused on immunology, oncology, and neuroscience.

Corporate Information:

History and Background: Long history as a diversified healthcare giant. Janssen's immunology success was pioneered with Remicade and solidified with the launch of Stelara and the next-generation Tremfya, maintaining a key competitive edge in autoimmune diseases. The company fully separated its Consumer Health business (Kenvue) in 2023 to sharpen its focus on Innovative Medicine and MedTech.

Key Milestones/Timeline:

Key Offerings:

Key Developments and Strategic Initiatives:

Partnerships & Collaborations:

Product Launches/Innovations:

Regulatory Approvals:

Technological Capabilities/R&D Focus:

Strengths & Differentiators:

SWOT Analysis:

Recent News and Updates:

Press Releases:

R&D

Researchers are focusing on better understanding the pathophysiology of PsA to develop targeted treatments. Novel biomarkers are identified to derive biologics for personalized treatments.

Key Players: Bristol Myers Squibb, Amgen, Inc., and UCB.

Clinical Trials & Regulatory Approval

Clinical trials are conducted to assess the safety and efficacy of PsA therapeutics. These therapeutics are then subsequently approved by several regulatory agencies.

Key Players: MoonLake Immunotherapeutics AG, Novartis Pharmaceuticals, Hansoh BioMedical R&D Company, and ACELYRIN Inc.

Patient Support & Services

Patient support & services refer to regular monitoring and lifestyle changes like exercise and stress management. It also includes reimbursement for treatment regimens.

| Companies | Headquarters | Offerings | Sales (USD) |

| AbbVie, Inc. | Illinois, United States | Skyrizi | $4.7 billion (Q3 2025) |

| Novartis AG | Basel, Switzerland | Consentyx | $6.14 billion (FY2024) |

| Johnson & Johnson | New Jersey, United States | Tremfya | $1.2 billion (Q2 2025) |

| Pfizer, Inc. | New York, United States | Xeljanz | $1.7 billion (FY2023) |

| Sanofi | Paris, France | Arava | - |

By Drug Class

By Clinical Manifestation

By Route of Administration & Delivery

By Patient Setting/End-User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar