Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

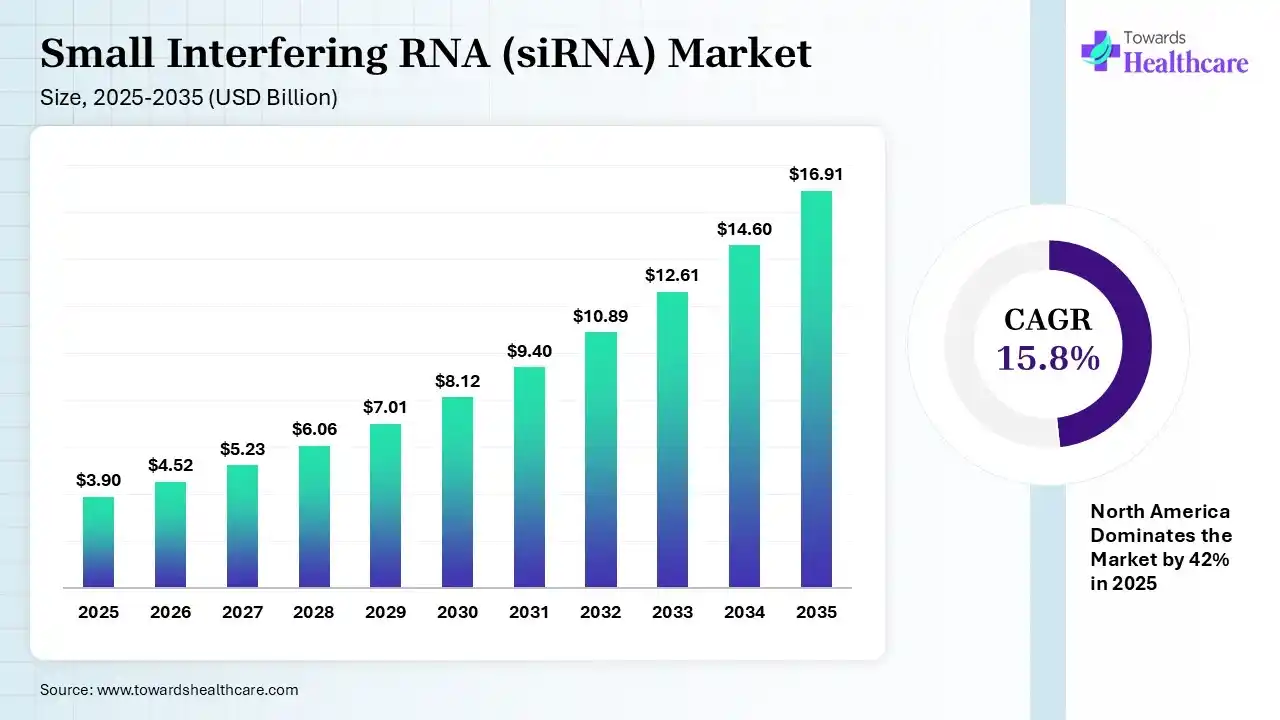

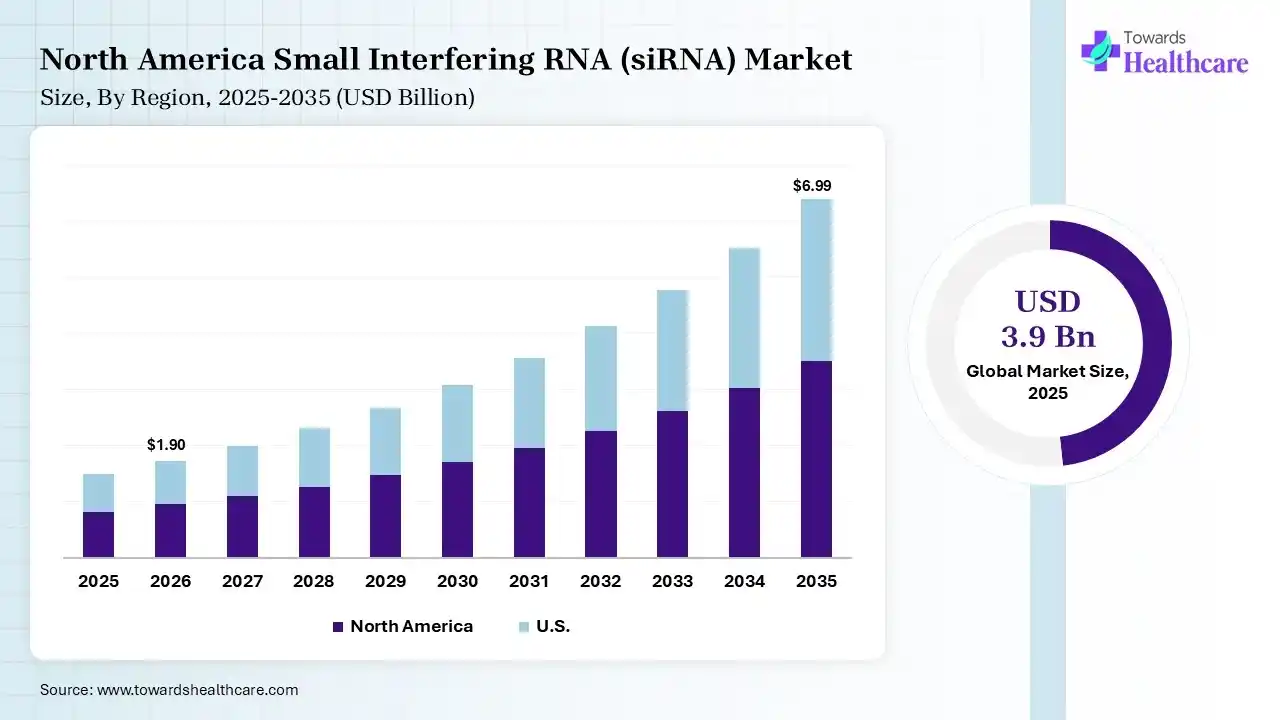

The global small interfering RNA (siRNA) market size was estimated at USD 3.9 billion in 2025 and is predicted to increase from USD 4.52 billion in 2026 to approximately USD 16.91 billion by 2035, expanding at a CAGR of 15.8% from 2026 to 2035. The Market is expanding, driven by growing interest in gene-silencing therapies and advancements in RNA-based drug development. Rising cases of chronic and genetic diseases, along with improving delivery technologies, are accelerating adoption across oncology and rare disease treatments.

Market Size 2025 - 2035 (USD Billion)")

The global small interfering RNA (siRNA) market is growing rapidly due to an urgent need for targeted medical treatments. These advanced therapies work by turning off disease-causing genes before they can cause harm. A major factor driving this growth is the rising number of chronic and rare genetic disorders worldwide. Recent scientific breakthroughs are also making these treatments much safer and more effective. For instance, new protective delivery systems allow the medicine to target specific sick cells without damaging healthy tissue. Looking ahead, the market's future is highly promising. Drug pipelines are expanding fast, particularly for complex oncology and cardiovascular diseases. Large pharmaceutical firms are investing heavily in these innovations. Increased funding and faster approval processes mean these highly precise therapies will soon transform standard patient care globally.

Small interfering RNA (siRNA) is a class of short, double-stranded RNA molecules that silence specific genes by degrading targeted messenger RNA (miRNA). The small interfering RNA (siRNA) market is expanding due to increasing demand for targeted therapies that can precisely silence disease-causing genes. Growth is supported by the rising prevalence of chronic and genetic disorders, ongoing advancements in RNA delivery technologies, and strong investment in biotechnology research. Additionally, a growing pipeline of RNA-based drugs and expanding clinical applications in oncology and rare diseases are accelerating market adoption.

AI is transforming the market by accelerating target identification, optimizing sequence design, and predicting off-target effects with greater accuracy. It helps improve delivery systems and reduces development time and costs. Additionally, AI-driven analytics enhance clinical trial success rates and enable personalized therapies, supporting faster commercialization and broader adoption of siRNA-based treatments across multiple disease areas.

| Table | Scope |

| Market Size in 2026 | USD 4.52 Billion |

| Projected Market Size in 2035 | USD 16.91 Billion |

| CAGR (2026 - 2035) | 15.8% |

| Leading Region | North America by 42% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Delivery Method, By Application, By End User, By Route of Administration, By Region |

| Top Key Players | Alnylam Pharmaceuticals, Silence Therapeutics, Silenseed Ltd, Sylentis S.A., Sanofi (Genzyme division), Quark Pharmaceuticals |

Market Share, By Type, 2025 (%)")

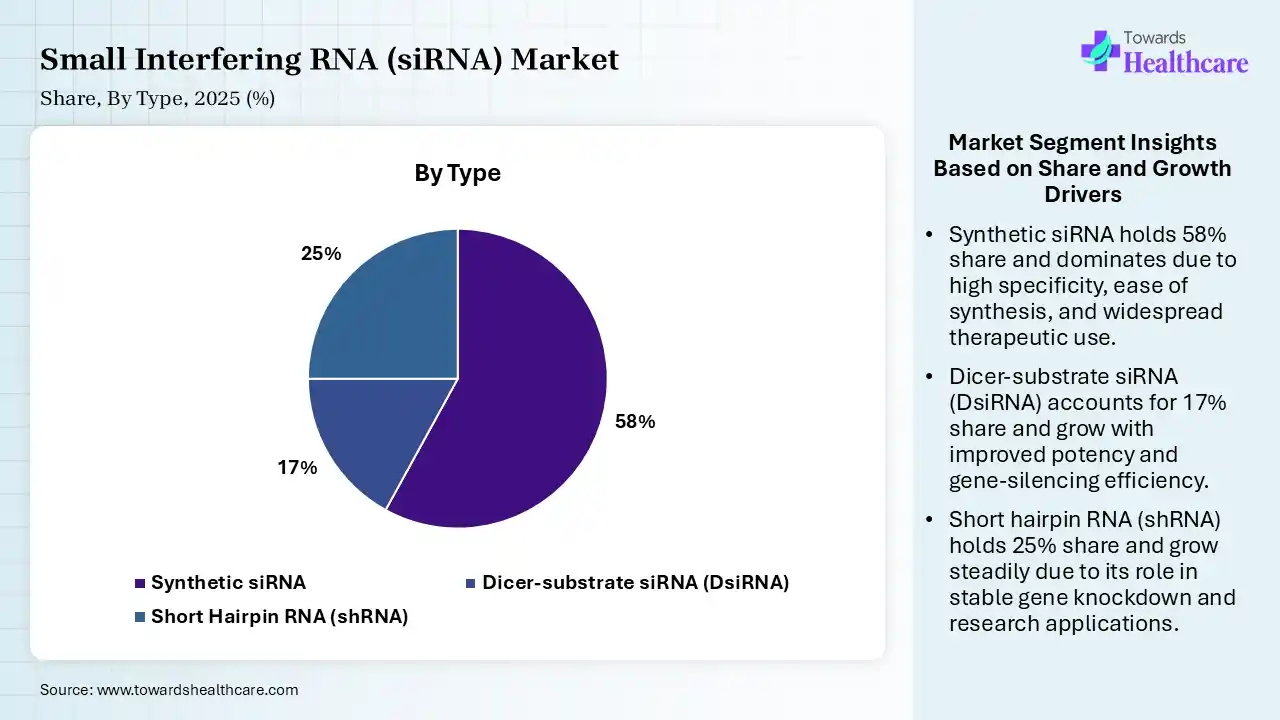

| Segment | Share 2025 (%) |

| Synthetic siRNA | 58% |

| Dicer-substrate siRNA (DsiRNA) | 17% |

| Short Hairpin RNA (shRNA) | 25% |

The synthetic siRNA segment dominated the small interfering RNA (siRNA) market with a revenue share of 58% in 2025 due to its high stability, precision gene-targeting ability, and scalable manufacturing compared to natural RNA forms. It offers improved safety, consistent quality, and easier chemical modification, enhancing therapeutic efficiency. Strong adoption in clinical pipelines for rare genetic, cardiovascular, and oncology diseases, along with advancements in delivery systems like lipid nanoparticles, further strengthened its leading market position.

The short hairpin RNA (shRNA) segment held the second-largest share of 25% of the market in 2025 due to its ability to provide sustained and long-lasting gene silencing through continuous intracellular expression. It is widely used in functional genomics, cancer research, and genetic disorders studies. Cost-effective production, efficient viral vector delivery systems, and strong research applications in gene knockdown experiments further drive its adoption, supporting its steady growth in the siRNA market.

The dicer-substrate siRNA (DsiRNA) segment held a 17% share in 2025 and is expected to grow at the fastest CAGR in the small interfering RNA (siRNA) market during the forecast period due to its higher gene-silencing efficiency and improved potency compared to traditional siRNA molecules. It requires lower doses for effective results, reducing toxicity risks and improving safety profiles. Increasing adoption in cancer and genetic disorders research, along with advancements in RNA delivery technologies and expanding clinical pipeline applications, further support its rapid market growth.

Market Share, By Delivery Method, 2025 (%)")

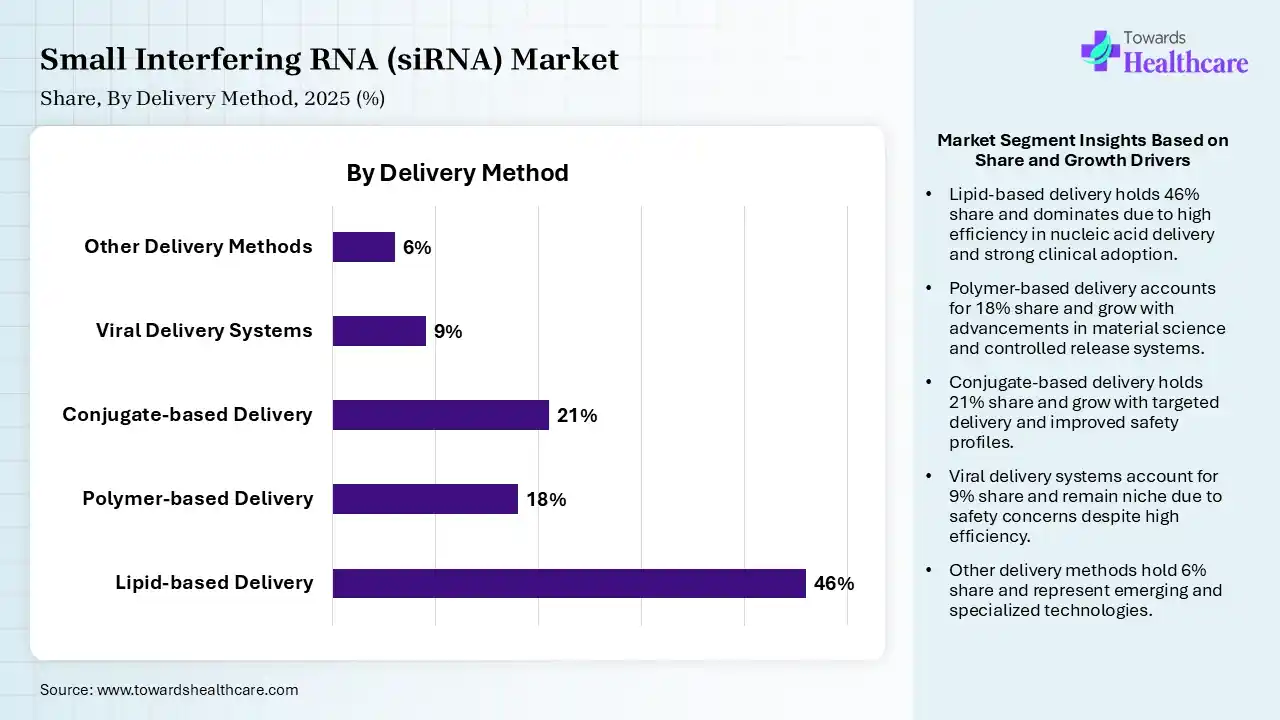

| Segment | Share 2025 (%) |

| Lipid-based Delivery | 46% |

| Polymer-based Delivery | 18% |

| Conjugate-based Delivery | 21% |

| Viral Delivery Systems | 9% |

| Other Delivery Methods | 6% |

The Lipid-based Delivery Segment Led the Market in 2025 with the Largest Share

The lipid-based delivery segment held a dominant share of 46% in 2025 due to its high efficiency in protecting RNA molecules and enabling targeted cellular delivery. Lipid nanoparticles enhance stability, reduce degradation, and improve gene-silencing effectiveness in vivo. Their proven success in FDA-approved therapies and strong application in liver, cardiovascular, and strong application in liver, cardiovascular, and genetic disorders further drive widespread adoption, making them the preferred delivery system for siRNA therapeutics.

The conjugate-based delivery segment held the second-largest share of 21% of the small interfering RNA (siRNA) market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to its high specificity and ability to target particular tissues, especially the liver, without requiring complex carriers. Technologies like GaINAc conjugation improve cellular uptake stability and reduce off-target effects. Its convenience, lower immunogenicity, and successful use in FDA-approved therapies make it a strong alternative to lipid-based delivery systems in clinical applications.

The polymer-based delivery segment held 18% of the small interfering RNA (siRNA) market share in 2025 due to its ability to provide stable, controlled, and sustained release of RNA molecules. Polymers enhance protection against enzymatic degradation and improve cellular uptake while allowing flexible chemical modification. Increasing research in biodegradable and biocompatible polymers, along with expanding applications in oncology and genetic disorders, is driving adoption as an emerging alternative delivery platform for siRNA therapies.

The viral delivery systems segment held 9% of the small interfering RNA (siRNA) market share in 2025 due to its high efficiency in delivering genetic material directly into target cells. Viral vectors enable strong and long-lasting gene silencing, making them suitable for complex diseases like cancer and genetic disorders. Increasing use in research applications, improved vector engineering, and advancements in safety and specificity are further driving the adoption of viral-based siRNA delivery approaches.

Market Share, By Application, 2025 (%)")

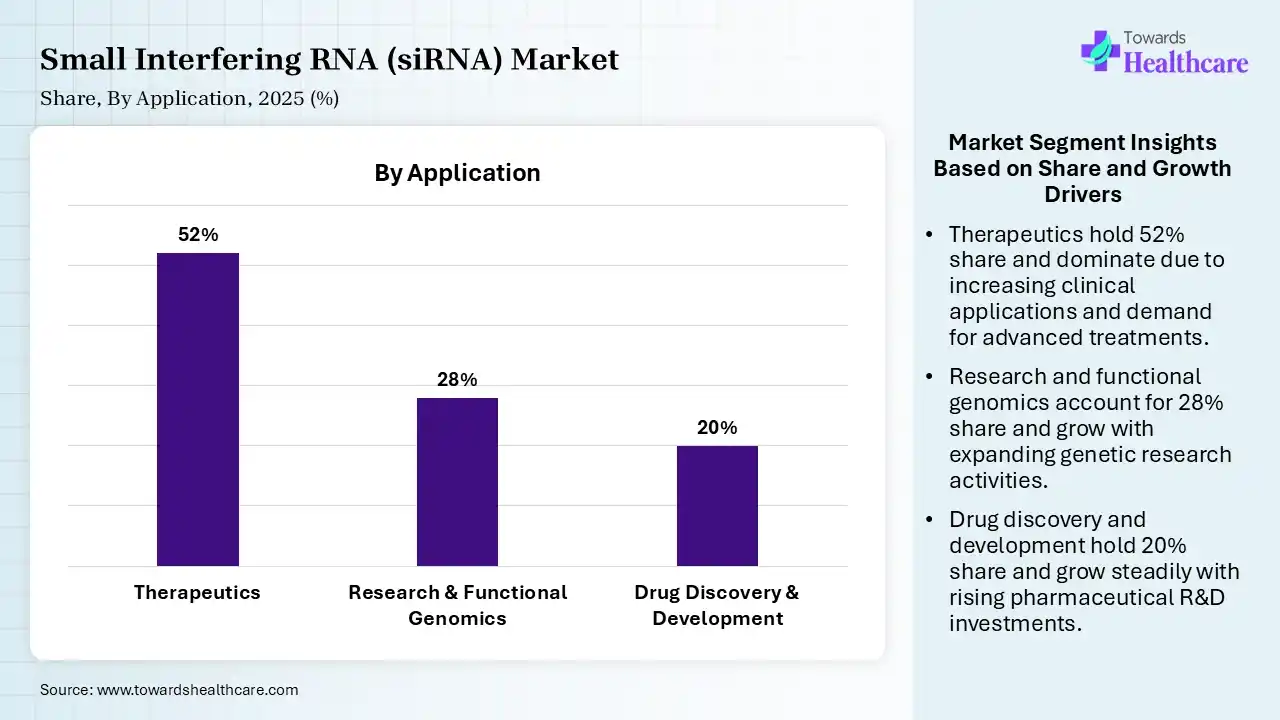

| Segment | Share 2025 (%) |

| Therapeutics | 52% |

| Research & Functional Genomics | 28% |

| Drug Discovery & Development | 20% |

The Therapeutics Segment Led the Market in 2025 with the Largest Share

The therapeutics segment led the market with a share of 52% in 2025 and is expected to grow at the fastest CAGR in the small interfering RNA (siRNA) market during the forecast period due to the increasing adoption of RNA interference technology for treating genetic, rare, and chronic diseases. Growing FDA approvals of siRNA-based drugs, rising prevalence of conditions like cardiovascular disorders, cancers, and metabolic diseases, and strong clinical pipeline development are drivers. Additionally, advancements in targeted delivery systems and expanding use in precision medicine further strengthen its dominance in clinical applications.

The research & functional genomics segment held 28% of the small interfering RNA (siRNA) market share in 2025 due to its widespread use in gene silencing studies, target validation, and understanding gene function. Increasing adoption in drug discovery programs, rising demand for advanced molecular biology tools, and expanding academic and pharmaceutical research activities are key drivers. SiRNA’s ability to selectively knock down genes makes it highly valuable in functional genomics and biomedical research applications.

The drug discovery & development segment held 20% of the small interfering RNA (siRNA) market share in 2025 due to increasing use of RNA interference technology for identifying and validating new therapeutic targets. Growing investment in precision medicine, rising demand for faster and more efficient drug development processes, and advancements in delivery systems are key drivers. Additionally, expanding clinical pipelines for genetic, cancer, and rare diseases further strengthened siRNA’s role in modern drug development

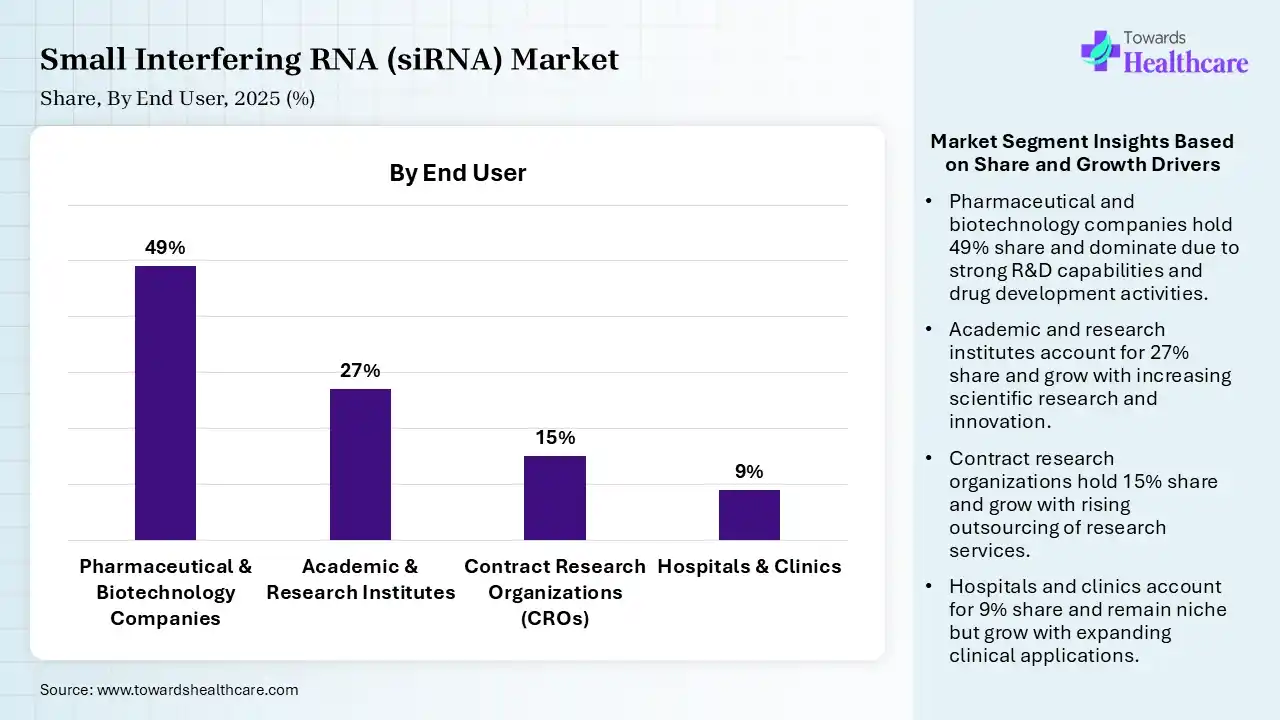

Market Share, By End User, 2025 (%)")

| Segment | Share 2025 (%) |

| Pharmaceutical & Biotechnology Companies | 49% |

| Academic & Research Institutes | 27% |

| Contract Research Organizations (CROs) | 15% |

| Hospitals & Clinics | 9% |

The Pharmaceutical & biotechnology Segment Led the Market in 2025 with the Largest Share

The pharmaceutical & biotechnology segment held a dominant share of 49% in 2025 and is expected to grow at the fastest CAGR in the small interfering RNA (siRNA) market during the forecast period due to strong investment in RNA-based drug development and large-scale clinical research capabilities. These companies drive innovation through robust pipelines targeting genetic, cardiovascular, and oncology diseases. Advanced infrastructure, expertise in biologics manufacturing, and strategic collaborations further support their dominance, enabling faster commercialization and wider adoption of siRNA therapeutics across global healthcare markets.

The academic & research institutes segment held 27% of the small interfering RNA (siRNA) market share in 2025 due to increasing focus on gene function studies and early-stage drug discovery. Rising government funding, expanding genomics research programs, and growing collaborations with pharmaceutical companies are key drivers. Additionally, widespread use of siRNA in functional genomics and molecular biology research is accelerating demand across universities and research organizations.

The contract research organizations segment held 15% of the small interfering RNA (siRNA) market share in 2025 due to increasing outsourcing of research and clinical trial activities by pharmaceutical and biotechnology companies. CROs offer cost-effective, specialized expertise and faster study execution, supporting efficient drug development. Rising demand for RNA-based therapies, growing clinical pipelines, and the need to reduce development timelines are driving greater reliance on CRO services in the siRNA space.

The hospitals & clinics segment held 9% of the small interfering RNA (siRNA) market share in 2025 due to increasing availability of approved RNA-based therapies and rising patient demand for advanced targeted treatments. Growing diagnosis of genetic and chronic diseases is driving treatment uptake in clinical settings. Additionally, improvements in healthcare infrastructure, physician awareness, and integration of precision medicine approaches are supporting wider adoption of siRNA therapies across hospitals and specialty clinics.

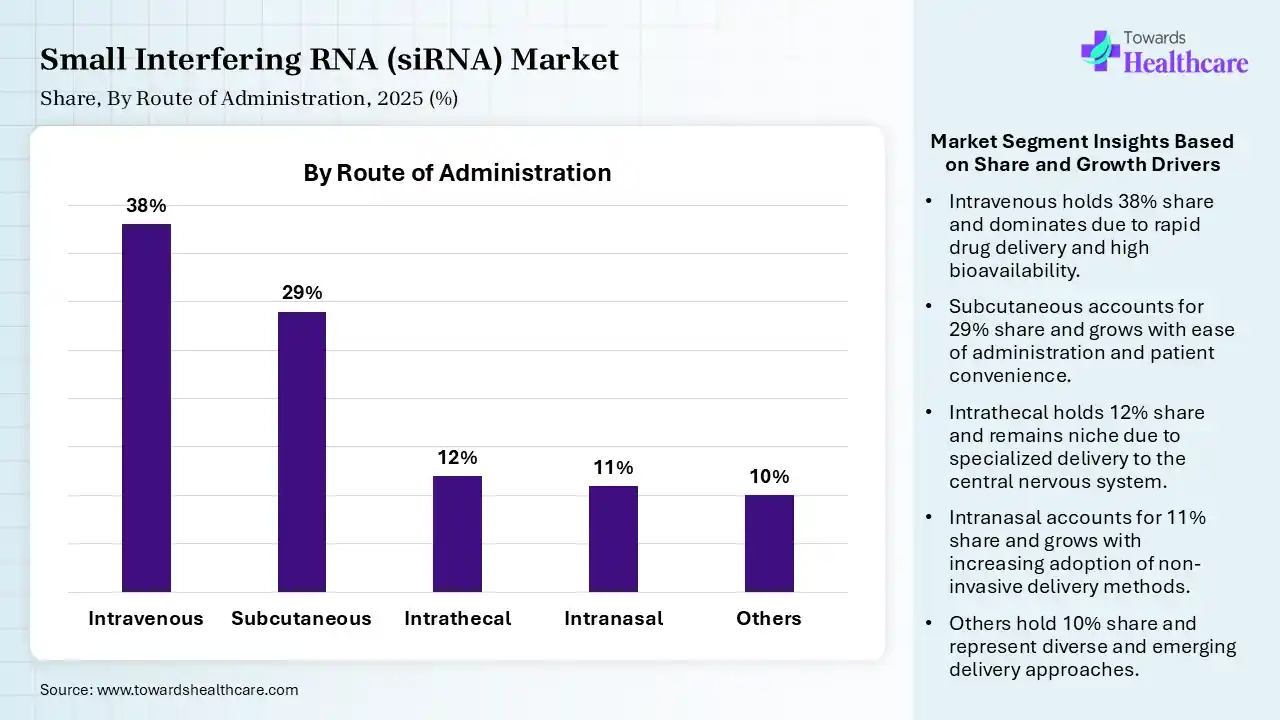

Market Share, By Route of Administration, 2025 (%)")

| Segment | Share 2025 (%) |

| Intravenous | 38% |

| Subcutaneous | 29% |

| Intrathecal | 12% |

| Intranasal | 11% |

| Others | 10% |

The Intravenous Segment Led the Market in 2025 with the Largest Share

The intravenous segment held a dominant share of 38% in 2025 due to its ability to deliver therapies directly into the bloodstream, ensuring rapid distribution and high bioavailability. It is widely used for approved siRNA drugs, especially for liver-targeted treatments, where precise dosing and controlled administration are critical. Compatibility, clinical preference, hospital-based administration, and compatibility with lipid nanoparticle delivery systems further support its leading position in the market.

The subcutaneous segment held the second-largest share of 29% of the market in 2025 and is expected to grow at the fastest CAGR in the small interfering RNA (siRNA) market during the forecast period due to its convenience, allowing self-administration and improved patient compliance compared to intravenous methods. It offers sustained drug release and is widely used in therapies targeting chronic conditions like hypercholesterolemia. Growing preference for less invasive treatment options, along with successful use in approved siRNA drugs, is driving its strong adoption in clinical practice.

The intrathecal segment held 12% of the small interfering RNA (siRNA) market share in 2025 due to its ability to deliver therapies directly into the central nervous system, bypassing the blood-brain barrier. This approach enhances treatment effectiveness for neurological and genetic disorders. Increasing research in CNS-targeted therapies, along with advancements in delivery techniques, is driving their adoption in specialized clinical applications.

The intranasal segment held 11% of the small interfering RNA (siRNA) market share in 2025 due to its non-invasive nature and ability to deliver therapies directly to the brain via the nasal route, bypassing the blood-brain barrier. This enhances the potential treatment of neurological disorders. Increasing research focus, ease of administration, and improved patient compliance are further supporting its growing adoption.

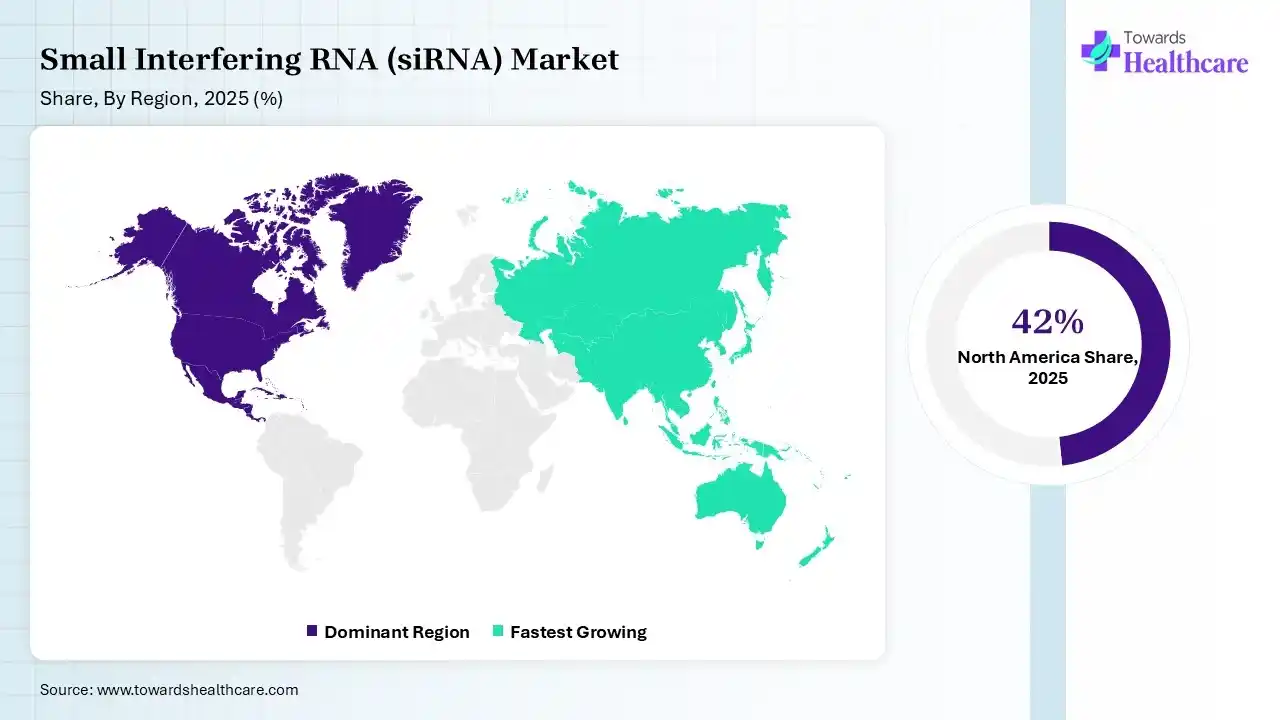

Market Share, By Region, 2025 (%)")

Market Growth")

North America dominated the small interfering RNA (siRNA) market with a share of 42% in 2025 due to its well-established biotechnology and pharmaceutical industry, supported by high research and development investments and advanced healthcare infrastructure. The region benefits from early adoption of innovation, RNA-based therapies, strong pressure from key market players, and a robust clinical trial landscape. Favorable regulatory frameworks and increasing focus on precision medicine further accelerate the development and commercialization of siRNA treatments.

U.S. Market Trends

The U.S. leads the small interfering RNA (siRNA) market due to its strong biotech ecosystems, high R&D funding, and presence of major pharmaceutical companies. Advanced clinical trial infrastructure, rapid adoption of precision medicine, and supportive regulatory pathways further accelerate innovation. Additionally, growing investments in gene-silencing therapies and a robust pipeline of siRNA candidates are strengthening the country’s market leadership position.

Canada Market Trends

Canada is experiencing steady market growth due to strong research infrastructure and robust public funding. The government actively supports biotechnology through agencies like the Canadian Institutes of Health Research. Academic hubs in Toronto and Vancouver are collaborating with local biopharma firms to pioneer novel lipid nanoparticle delivery systems. This strong collaborative environment ensures a highly promising future outlook for genetic disease treatments nationwide.

Asia Pacific held 17% share of the market in 2025 and is expected to grow at the fastest CAGR in the small interfering RNA (siRNA) market due to rising healthcare investments, increasing prevalence of genetic and chronic diseases, and expanding biotechnology research capabilities. Growing clinical trials activity, improving regulatory support, and cost-effective drug development environments in countries like China, India, and Japan are further attracting global pharmaceutical companies, accelerating regional market growth significantly during the forecast period.

India Emerging as a High-Growth siRNA Market Hub

India is projected to grow at the fastest CAGR in the small interfering RNA (siRNA) market due to the rapidly expanding biotechnology sector, increasing prevalence of genetic and chronic diseases, and rising government support for life science research. Growing clinical trial activities, availability for skilled scientific talent, and cost-effective R&D infrastructure are attracting global pharmaceutical investments, accelerating the adoption of advanced RNA-based therapies during the forecast period.

China Market Trends

China is rapidly transforming into a global powerhouse for RNA therapeutics. Extensive government initiatives, including the "Made in China 2025" bio-innovation goals, provide massive funding to domestic laboratories. The competitive landscape features a strong mix of large global enterprises and agile domestic startups like Genecon Biotechnologies. Advanced research pipelines in oncology are setting a massive trend for future market dominance.

Clinical Trails

Regulatory Approvals

Patient Support and Services

Market Top Companies")

| Companies | Headquarters | Offerings |

| Alnylam Pharmaceuticals | Massachusetts, USA | Pioneer in RNA interference (RNAi) therapeutics; develops FDA-approved siRNA drugs like patisiran, givosiran, and lumasiran for rare genetic diseases, cardiovascular conditions, and liver-targeted disorders. |

| Silence Therapeutics | London, United Kingdom | Focuses on siRNA-based medicines using mRNAi GOLD™ platform; developing therapies for cardiovascular diseases, rare genetic disorders, and hematological conditions |

| Silenseed Ltd | Rehovot, Israel | Specializes in locally delivered siRNA therapies using polymeric implant technology; primarily targeting solid tumors such as pancreatic cancer. |

| Sylentis S.A. | Madrid, Spain | Subsidiary of PharmaMar; develops siRNA-based treatments mainly for ophthalmology (glaucoma, dry eye disease) and respiratory disorders. |

| Sanofi (Genzyme division) | Paris, France | Invests in RNA-based therapeutics through collaborations; focuses on rare diseases, genetic disorders, and expanding precision medicine pipelines. |

| Quark Pharmaceuticals | California, USA | Develops RNAi therapeutics targeting kidney diseases, ocular disorders, and cancer; strong focus on siRNA molecules like QPI-1002 for acute kidney injury |

Strengths

Weaknesses

Opportunities

Threats

In June 2026, "We are excited to take part in this fireside chat with Force Family Office," said Robert Bitterman, CEO and Chairman of Phio Pharmaceuticals. "Dr. Jim Cardia will discuss the future direction of siRNA oncology and highlight how our INTASYL® siRNA program represents a differentiated and innovative approach to immuno-oncology."

By Type

By Delivery Method

By Application

By End User

By Route of Administration

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar