Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

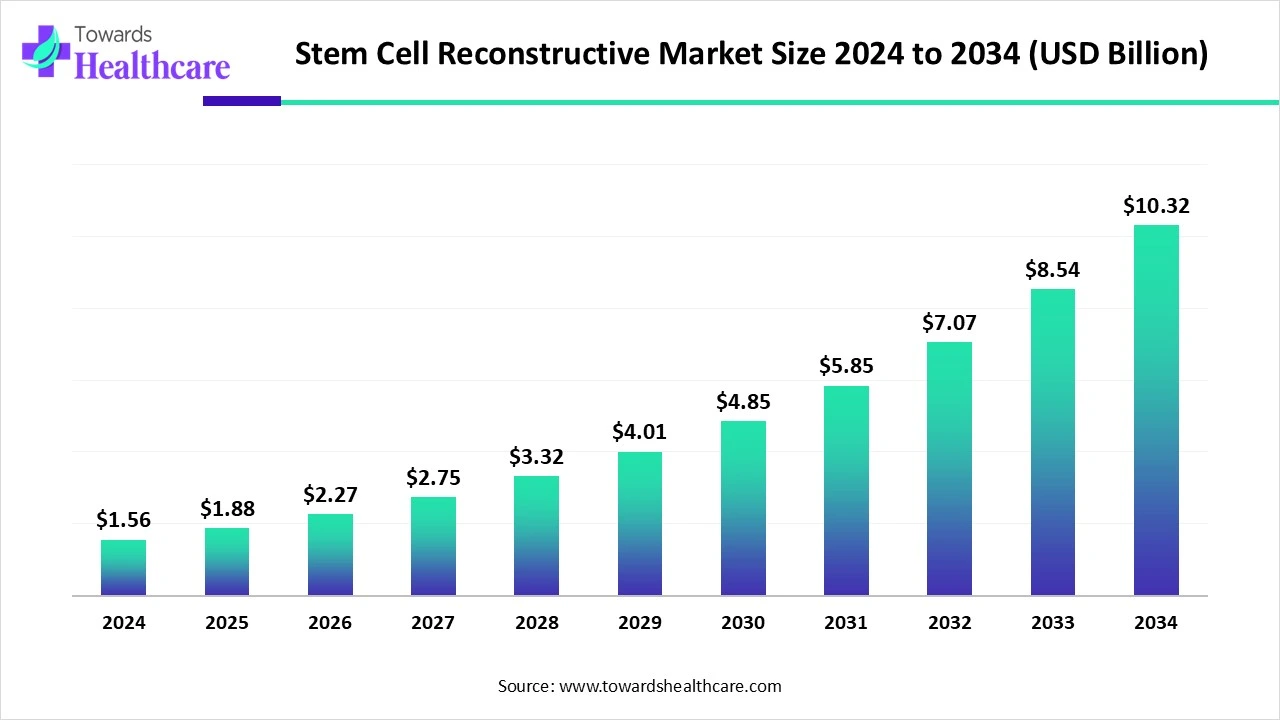

The global stem cell reconstructive market size is calculated at US$ 1.88 billion in 2025, grew to US$ 2.28 billion in 2026, and is projected to reach around US$ 12.48 billion by 2035. The market is expanding at a CAGR of 20.81% between 2026 and 2035.

In the current era, the global stem cell reconstructive market has been experiencing major growth, driven by several contributing factors, such as a rise in cases of chronic issues, including cancer, cardiovascular diseases, and musculoskeletal disorders, growing research approaches in the innovation of therapies for tissue and organ regeneration, and demand for personalized medicine. Further, the market will expand major opportunities, including osteoarthritis and Parkinson's, with accelerated technological advancements in novel creations in stem cell isolation, expansion, and differentiation. Also, induced pluripotent stem cells (iPSCs) are widely employed in the development of various therapies.

| Metric | Details |

| Market Size in 2026 | USD 2.28 Billion |

| Projected Market Size in 2035 | USD 12.48 Billion |

| CAGR (2026 - 2035) | 20.81% |

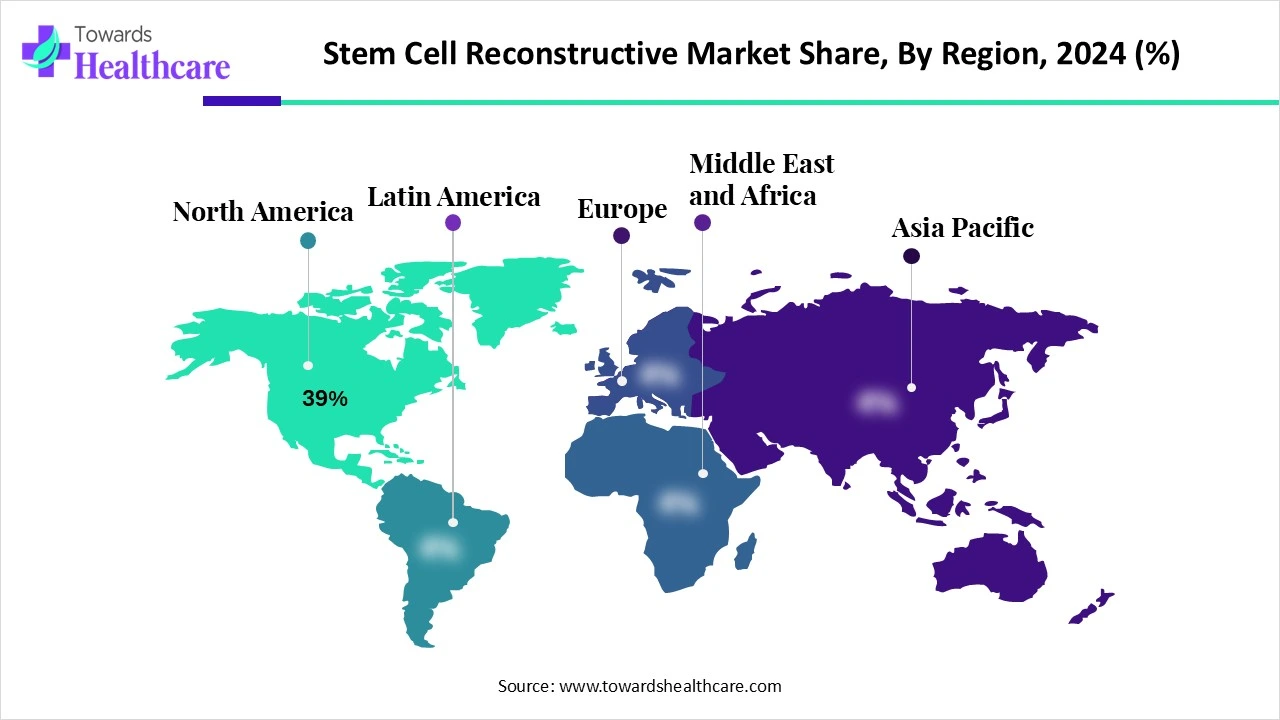

| Leading Region | North America Share by 39% |

| Market Segmentation | By Cell Type, By Source, By Application, By End Use, By Mode of Administration, By Technology, By Region |

| Top Key Players | Mesoblast Ltd., Athersys Inc., Smith+Nephew, BioRestorative Therapies, MEDIPOST Co., Ltd., Vericel Corporation, Anterogen Co., Ltd., NuVasive, Inc., RTI Surgical, Osiris Therapeutics (a part of Smith+Nephew), Organogenesis Holdings Inc., Cynata Therapeutics, TiGenix (acquired by Takeda), Celularity Inc., Thermo Fisher Scientific (Stem Cell Tech Division), Lonza Group, STEMCELL Technologies, Pluristem Therapeutics, BioTime Inc. (now Lineage Cell Therapeutics), ReNeuron Group plc |

The stem cell reconstructive market refers to the market encompassing the use of stem cell-based therapies, technologies, and products for reconstructive purposes, including the restoration, repair, or replacement of damaged tissues or organs. This market integrates regenerative medicine, cell therapy, and biomaterial scaffolds for applications in plastic & cosmetic surgery, orthopedic reconstruction, craniofacial repair, wound healing, burn treatment, and soft tissue regeneration. It includes autologous and allogeneic stem cells, delivery systems, and adjunct technologies used to enhance integration, function, and aesthetic outcomes. The market is experiencing novel developments, including the application of AI automation to customize treatments, the increase in gene editing techniques, and the development of smart scaffolds for tissue regeneration.

AI has a transforming role in this market by improving stem cell production, delivery, and monitoring, along with the prediction of treatment results and assisting in simplifying processes. Generally, AI helps to boost precision, effectiveness, and customization of treatments. Arising factors in the market play a vital role in stem cell function and regeneration, which can be analyzed and employed with AI-powered approaches to accelerate therapeutic.

For instance,

Increasing Incidence of Chronic Diseases and Demand for Tailored Medicine

In 2025, the stem cell reconstructive market will be broadly fueled by a rise in cases of chronic issues, including cancer, cardiovascular diseases, and musculoskeletal disorders are immensely demanding stem cell therapies with probable treatment choices for these conditions. Moreover, enhanced utilization of stem cells to develop customized treatments for individual patients, along with growing research approaches in the innovation of therapies for tissue and organ regeneration, are majorly driving the overall market growth.

Emerging Restrictions on Quality Control and Operational Spending

Many challenges are arriving in the market with a robust need for quality control solutions to reduce the risk of contamination and ensure the purity, viability, and stability of stem cells throughout the manufacturing process. Besides this, another crucial limitation is the requirement of advanced equipment, trained professionals, and complicated production processes involved in stem cell therapy are generating high expenses, with restricted availability.

Technological Breakthroughs and the Emergence of New Applications

The stem cell reconstructive market will have various opportunities in the developing globe, such as the involvement of novel uses in areas like orthopedic applications, neurological disorders, cardiovascular treatments, and even dental applications. Whereas, around the world, a growing geriatric population coupled with major conditions, including osteoarthritis and Parkinson's, with optimized technological advancements in novel creations in stem cell isolation, expansion, and differentiation are boosting the development of the ultimate market.

")

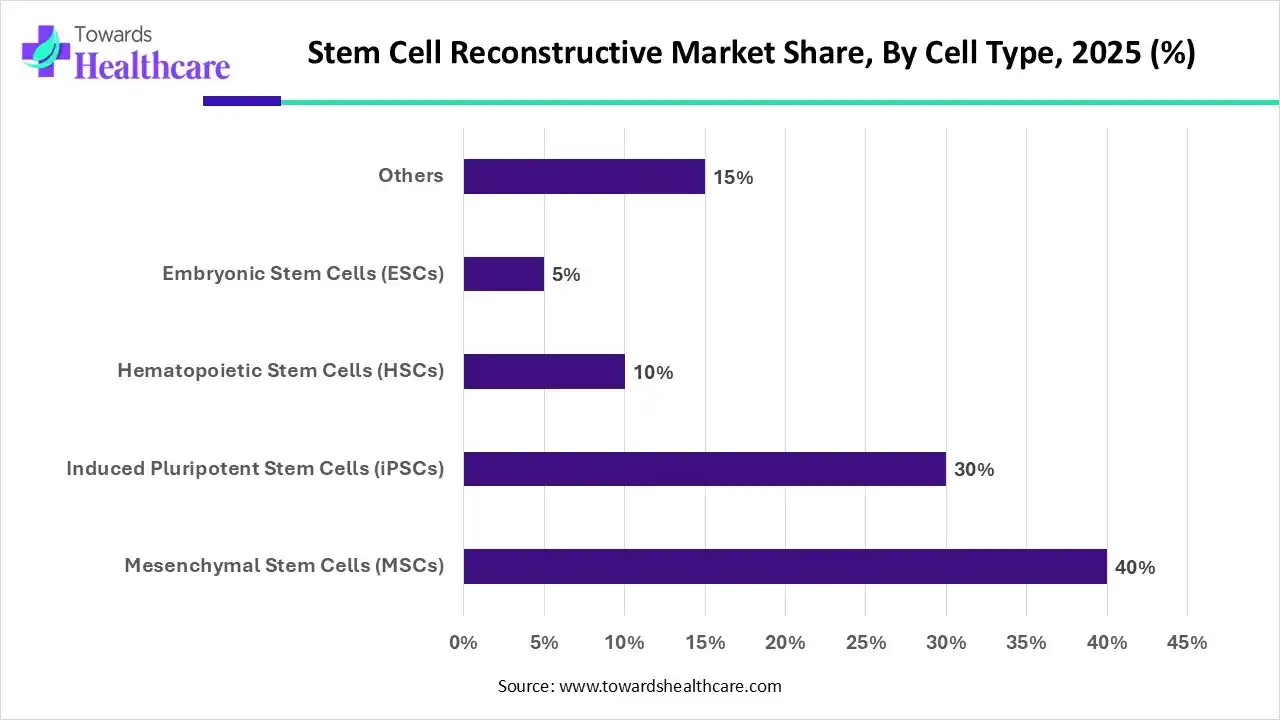

By cell type, the mesenchymal stem cells (MSCs) segment held the largest share of the market by 40%, due to their accelerated use in bone and cartilage repair, cardiovascular disease treatment, and wound healing. As well as they can also be derived from numerous sources such as bone marrow, adipose tissue, and umbilical cord blood, leading to the adoption of these types of cells in various areas.

However, the induced pluripotent stem cells (iPSCs) segment will expand rapidly. With improved iPSC reprogramming approaches, along with enhanced gene delivery systems and refined reprogramming factors, which can contribute to raising the efficiency and reliability of iPSCs for research and therapeutic use. Also, iPSCs can differentiate into different cell types, which makes them a strong tool for regenerative medicine with providing possible treatments for damaged tissues and organs.

| Segment | Share 2025 (%) |

| Autologous (Patient-Derived) | 50% |

| Allogeneic (Donor-Derived) | 40% |

| Xenogeneic (Cross-Species) | 10% |

The autologous (patient-derived) segment led the global stem cell reconstructive market by 50% in 2025. Due to increasing diseases, such as heart conditions, neurological disorders, and cancer, are acting as a major driver in the segment's growth. Besides this, extensive research approaches in stem cell biology and their uses in regenerative medicine are propelling the development of novel therapeutic areas.

By source, the allogeneic (donor-derived) segment is predicted to show rapid expansion, with a crucial contribution in growing cases of cancer, autoimmune disorders, and blood issues, which are generating a higher need for treatments like allogeneic stem cell transplantation. Also, this segment has a vital role in leukemia, lymphoma to redevelop damaged tissues and organs.

The orthopedic reconstruction segment dominated the market due to the rising prevalence of arthritis, sports injuries, and age-related musculoskeletal degeneration in the world. As well as major technologies in surgeries like innovations in 3D bioprinting and novel biomaterials, are allowing highly efficacious and targeted regenerative procedures are accelerating their adoption in orthopedic reconstruction.

By application, the wound & burn healing segment is estimated to grow rapidly, as contributing factors are regulation of stem cell differentiation, proliferation, and migration, as well as angiogenesis (new blood vessel formation) and re-epithelialization (regrowth of skin) will boost the segment expansion. With special inclusion of mesenchymal stem cells (MSCs) in escalating burn wound healing, minimizing inflammation, and reducing scarring.

The hospitals & surgical centers segment was dominant in the global stem cell reconstructive market in 2025. The segment is fueled by the growing demand for regenerative medicine, advancements in stem cell technologies, as well as an increasing cases of chronic diseases like cancer, diabetes, and musculoskeletal disorders.

On the other hand, the cosmetic clinics segment will expand at a rapid CAGR, because of the accelerating demand for aesthetic procedures and the probable of stem cells to rejuvenate and repair damaged skin. Naturally derived proteins that stimulate cell growth and differentiation play a major role in these cosmetic applications, especially in anti-aging treatments and wound healing, which is driving the overall segment development.

By mode of administration, the injection-based segment held the biggest share of the market. Mainly, intra-articular, intradermal administration of stem cells supports the skip of the need for complex surgical procedures, making treatments easily accessible and potentially minimally risky for patients. Along with this, precise delivery of therapeutic agents to the site of injury or disease promotes localized tissue regeneration and repair.

Furthermore, the scaffold/biomaterial-assisted delivery segment will accelerate by its applications in biomaterials as scaffolds to pass stem cells and growth factors, boosting their therapeutic potential and enhancing tissue regeneration. In case of gene therapy, cells are transfected with DNA encoding the desired growth factor and then incorporated into the scaffold.

The stem cell culture & expansion segment registered its dominance in the market, with the surge of novel serum-free media, bioreactors, and 3D culture methods accelerating large-scale stem cell expansion while preserving functionality. Also, this segment possesses numerous applications like disease modeling, drug discovery, and regenerative medicine are impelling its expansion.

Whereas, the 3D bioprinting segment is predicted to show rapid expansion, as it enables the creation of patient-specific tissues and organs, personalized to individual needs, and the elimination of difficulties connected with donor sites. Along with this, ongoing R&D in bioinks, including those incorporating stem cells, is progressing the generation of more complex and functional tissue structures.

")

Across the world, North America held the largest revenue share 39% of the stem cell reconstructive market, due to the emergence of heart diseases, neurodegenerative disorders, and diabetes, which are widely demand for regenerative medicine approaches with robust application of stem cell therapies. Also, North America is highly adopting innovations in stem cell research, including induced pluripotent stem cells (iPSCs), CRISPR gene editing, and 3D bioprinting are optimizing the possible usages and efficacy of stem cell therapies.

The most influential country in North America is the US, which has been experiencing widespread government support and private funding in stem cell research and therapy development, and is expanding clinical trials and the commercialization of new treatments. A compatible regulatory landscape for these research activities is fostering the complete market expansion in this region.

For instance,

Canada’s market is driven by the adoption of innovations such as induced pluripotent stem cells (iPSCs) and 3D bioprinting in the expansion of potential for regenerative medicine and drug discovery. Moreover, the Canadian government is focusing on the development of biotechnology and healthcare innovation to offer major funding and infrastructure support for research and development in stem cell therapies.

According to research, the Asia Pacific is anticipated to grow rapidly in the upcoming years. Day by day, a growing incidence of many chronic diseases in ASAP, with the rising emergence of clinical trials for stem cell therapies, especially in countries like China and Japan, is indicating the growth of promising applications of stem cell therapies in ASAP. Although ASAP is acting as a hub for medical tourism, with countries like India and China attracting patients looking for advanced stem cell treatments.

China's geriatric population is resulting in a rise in age-related diseases and injuries, generating a greater need for regenerative therapies. As well as the Chinese government encouraging investments and partnerships between research institutions and pharmaceutical companies, it is accelerating the development of new stem cell-based treatments.

For this market,

Japanese research institutions and companies are leading stem cell research, developing innovative therapies for many conditions. Along with technological advancements, Japan has been supporting through reimbursement policies for regenerative medicine and stem cell therapies further boost market adoption.

Around this market,

Currently, it is estimated that Europe will expand notably, as governments and private organizations in Europe are putting efforts through investment in stem cell research, with the expansion of their therapies and technologies. Along with this, the European Medicines Agency (EMA) is assisting in streamlining the approval process for Advanced Therapy Medicinal Products (ATMPs), including stem cell therapies, accelerating market access.

Germany, possessing supportive government policies and initiatives, along with a robust healthcare infrastructure, is contributing to the market's expansion. Moreover, adoption of novel technologies such as induced pluripotent stem cells (iPSCs) bypasses ethical issues linked with embryonic stem cells, accelerating the potential applications of stem cell therapies.

The UK has rising advancements in stem cell therapies like induced pluripotent stem cells (iPSCs) and 3D bioprinting, with an enhanced focus on the development of personalized regenerative medicine is driving the respective market growth in the UK.

For instance,

South America is expected to grow significantly in the stem cell reconstructive market during the forecast period, due to growing stem cell therapies awareness. The increasing incidence of chronic disease is also increasing its demand. Moreover, expanding healthcare, growing biotech startups, and blooming medical tourism are also enhancing the market growth.

Brazil consists of a well-developed healthcare infrastructure, which is increasing the adoption of regenerative medicines. At the same time, the growing number of diseases and government investment are also encouraging stem cell research. Additionally, their growing applications are also increasing their demand.

MEA is expected to grow significantly in the stem cell reconstructive market during the forecast period, due to increasing chronic diseases. The increasing healthcare investments and expanding industries are also increasing their development. Additionally, growing awareness, R&D activities, and medical tourism are also promoting the market growth.

Saudi Arabia is experiencing a rise in the incidences for various chronic diseases, which is increasing the demand for stem cell reconstruction to develop new regenerative therapies. The increasing government initiatives and investments are also driving their innovations. Furthermore, the expanding medical tourism and R&D activities are also creating new opportunities.

By Cell Type

By Source

By Application

By End Use

By Mode of Administration

By Technology

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar