Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

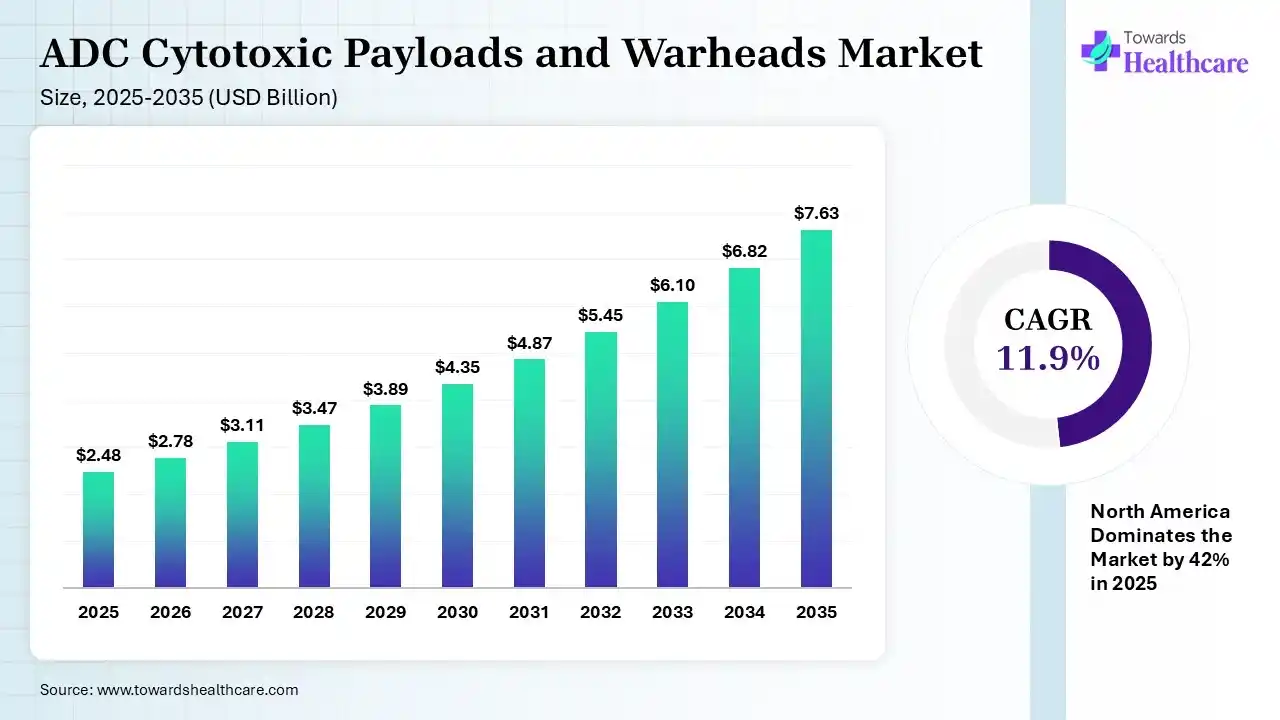

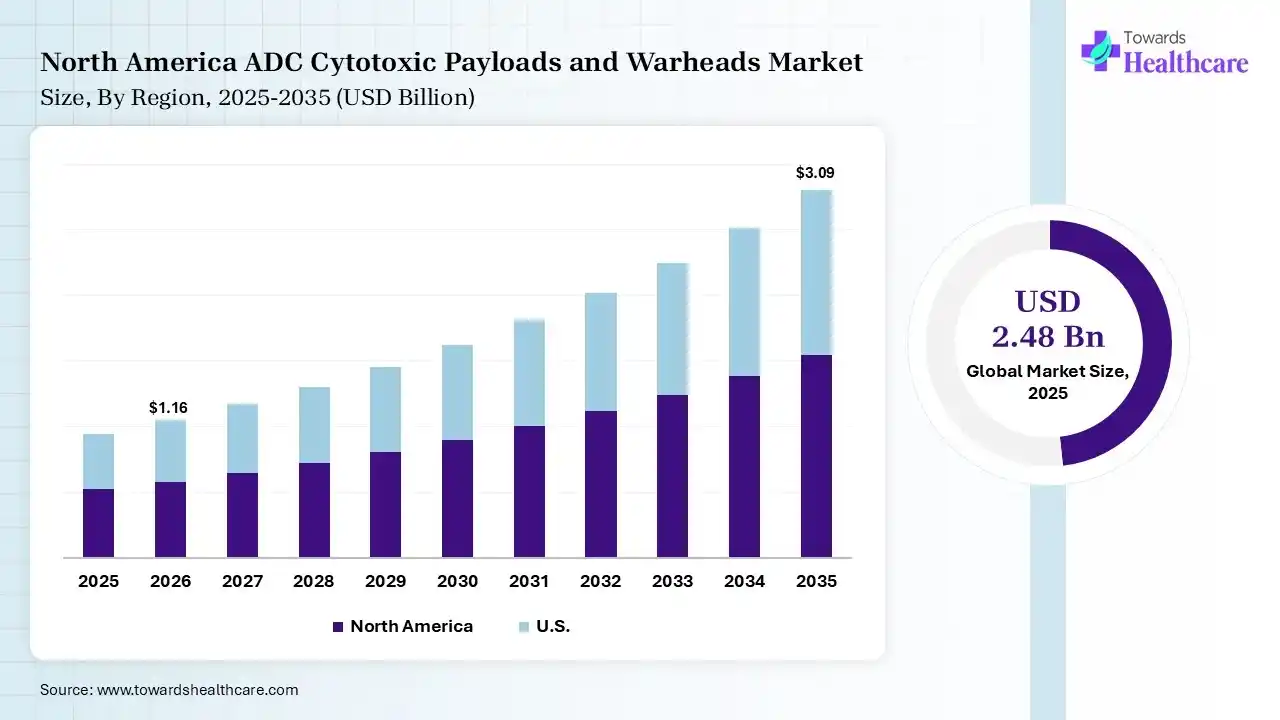

The global ADC cytotoxic payloads and warheads market size was estimated at USD 2.48 billion in 2025 and is predicted to increase from USD 2.78 billion in 2026 to approximately USD 7.63 billion by 2035, expanding at a CAGR of 11.9% from 2026 to 2035.The market is growing steadily, driven by increasing adoption of antibody-drug conjugates in targeted cancer treatment. Rising oncology pipelines and advancements in highly potent payload technologies are further boosting demand and innovation in this market.

")

ADC cytotoxic payloads (warheads) are highly potent small-molecule drugs linked to antibodies in antibody-drug conjugates, designed to selectively kill target cancer cells. The ADC cytotoxic payloads and warheads market is growing due to the rising adoption of targeted cancer therapies that improve treatment efficacy while reducing systemic toxicity. Increasing investments in oncology research, expanding clinical pipelines, and continuous innovation in highly potent payloads and linker technologies are driving demand. Additionally, growing approvals of antibody-drug conjugates and the need for more precise next-generation cancer treatment further accelerate market expansion.

The ADC cytotoxic payloads and warheads market is expanding as antibody drug conjugates gain wider use in targeted cancer treatment. Pharmaceutical companies are investing in the development of highly potent payloads that improve treatment effectiveness while reducing damage to healthy cells. Research into new toxin classes, improved stability, and safer delivery methods is creating significant opportunities for innovation. Demand for specialized manufacturing and custom synthesis services is also increasing. Strategic partnerships between biotechnology firms, pharmaceutical companies, and contract manufacturers are accelerating product development and commercialization. The competitive landscape includes established oncology companies, specialized payload developers, and emerging biotechnology firms competing through innovation, technology advancement, manufacturing expertise, and collaborative research to strengthen their product pipelines.

AI is transforming the market by accelerating drug discovery, optimizing payload selection, and improving linker design for better targeting and efficacy. It enables predictive modeling of toxicity and therapeutic response, reducing development time and costs. Additionally, AI-driven insights support personalized treatment approaches and streamline clinical trials, enhancing success rates and driving innovation in next-generation antibody-drug conjugates.

Shift Toward Next-Generation Payloads

The market is witnessing a transition from traditional microtubule inhibitors to advanced payload classes such as topoisomerase inhibitors and DNA-damaging agents, offering improved efficacy, reduced resistance, and enhanced safety profiles in targeted cancer therapies.

Advancements in Linker and Conjugation Technologies

Innovations in stable and cleavable linker systems, along with site-specific conjugation methods, are improving drug delivery precision, minimizing off-target toxicity, and enhancing the overall therapeutic performance of antibody-drug conjugates.

Expanding Clinical Pipeline and Indications

A strong and growing pipeline of ADC candidates, along with expansion into new cancer types and earlier lines of treatment, is expected to drive sustained market growth and broader adoption of ADC-based therapies globally.

| Table | Scope |

| Market Size in 2026 | USD 2.78 Billion |

| Projected Market Size in 2035 | USD 7.63 Billion |

| CAGR (2026 - 2035) | 11.9% |

| Leading Region | North America by 42% |

| Key Applications | Cancer treatment, targeted oncology therapies, hematological malignancies, solid tumors, precision medicine, next-generation ADC development |

| Primary End Users | Pharmaceutical companies, biotechnology companies, ADC developers, CROs, CDMOs, oncology research institutes |

| Key Growth Drivers | Rising cancer incidence, increasing ADC approvals, expansion of oncology pipelines, demand for targeted therapies, investments in next-generation payload technologies, pharma outsourcing |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Payload Type, By Warhead Potency, By Mechanism of Action, By Linker Compatibility, By Conjugation Technology Compatibility, By Application, By End User, By Region |

| Top Key Players | AstraZeneca plc, F. Hoffmann-La Roche Ltd., ImmunoGen, Inc., Pfizer Inc., Seagen Inc., Takeda Pharmaceutical Company Limited |

")

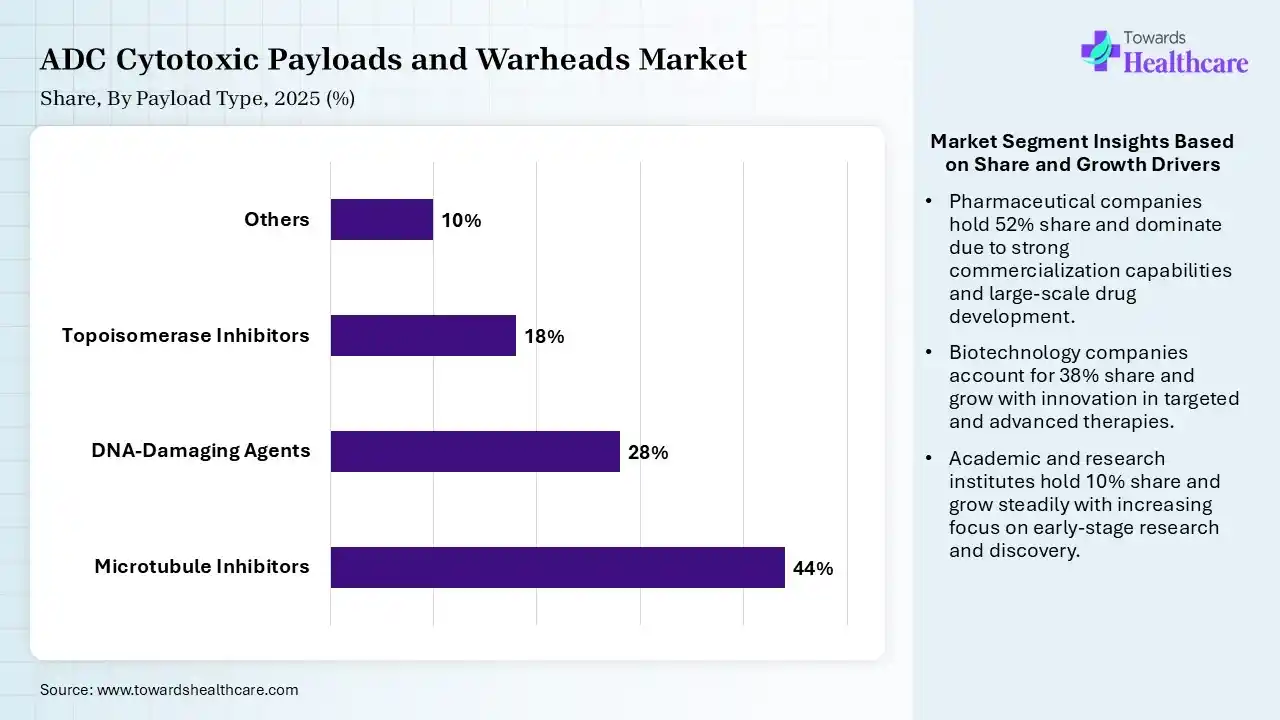

| Segment | Share 2025 (%) |

| Microtubule Inhibitors | 44% |

| DNA-Damaging Agents | 28% |

| Topoisomerase Inhibitors | 18% |

| Others | 10% |

The Microtubule Inhibitors Segment Dominated the Market in 2025

The microtubule inhibitors segment dominated the ADC cytotoxic payloads and warheads market with a revenue share of 44% in 2025 due to their proven efficacy in disrupting cell division and inducing rapid cancer cell death. Their established clinical success, widespread use in approved antibody-drug conjugates, and well-understood safety profiles supported strong adoption. Additionally, ease of conjugation and reliable performance across multiple cancer types further strengthened their leading market position.

The DNA-damaging agents segment held the second-largest share of 28% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to their high potency and strong ability to kill cancer cells, including those resistant to conventional therapies. Their effectiveness at low doses and compatibility with advanced ADC design support their growing use. Additionally, increasing research focus on integration into emerging antibody-drug conjugates has strengthened their position as a key payload class.

The topoisomerase inhibitors segment held a 18% of ADC cytotoxic payloads and warheads market share in 2025 due to their strong ability to interfere wth DNA replication, leading to effective cancer cell death. Their improved safety profiles and reduced off-target toxicity compared to traditional payloads make them attractive for ADC development. Increasing clinical success, rising adoption of newly approved therapies, and expanding research focus on next-generation ADCs are further driving the growth of this segment.

")

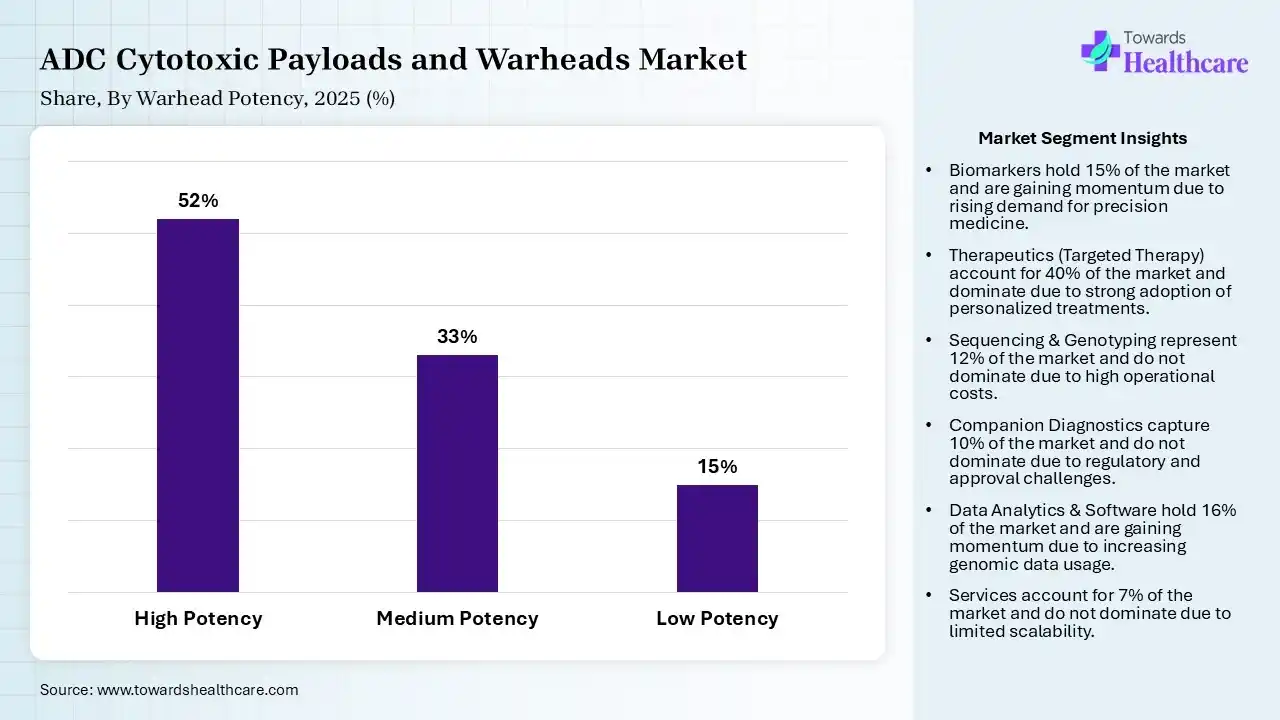

| Segment | Share 2025 (%) |

| High Potency | 52% |

| Medium Potency | 33% |

| Low Potency | 15% |

The High Potency (IC50<1nM) Segment Led the Market in 2025 with the Largest Share.

The high potency (IC50<1nM) segment held a dominant share of 52% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to its ability to deliver a strong cytotoxic effect at very low doses, enhancing therapeutic efficacy while minimizing systemic toxicity. These warheads are essential for effective ADC performance, enabling precise targeting of cancer cells. Their proven clinical success, compatibility with advanced conjugation technologies, and increasing use in approved ADCs have driven their dominant market position.

The medium potency (IC50 1-10nM) segment held the second-largest share of 33% in 2025 due to its balanced profile of efficacy and safety, enabling effective tumor cell killing with reduced risk of off-target toxicity. These warheads offer improved therapeutic windows and flexibility in ADC designs, supporting broader clinical applications. Increasing focus on optimizing dose tolerability and expanding use in next-generation ADCs further drives segment growth.

The low potency segment held a 15% of ADC cytotoxic payloads and warheads market share in 2025 due to increasing demand for optimized efficacy-to-safety balance in antibody-drug conjugates. Both high-and medium-potency warheads are gaining traction as they enable precise tumor targeting while minimizing systemic toxicity. Advances in conjugation technologies and better understanding of dose-response relationships are supporting tailored payload selection, driving broader clinical applications and continuous innovation in ADC development.

")

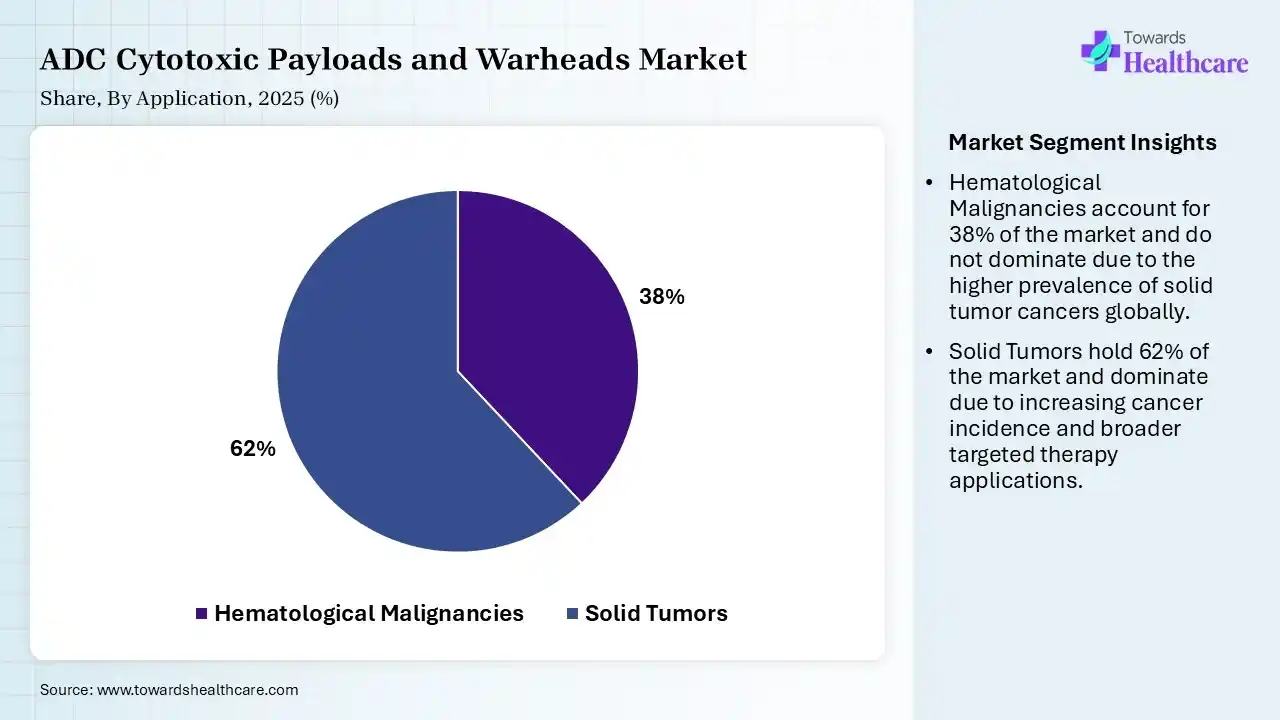

| Segment | Share 2025 (%) |

| Hematological Malignancies | 38% |

| Solid Tumors | 62% |

The Solid Tumors Segment Led the Market in 2025 with the Largest Share

The solid tumors segment held the second-largest share of 62% in 2025 and is expected to grow at the fastest CAGR in the ADC cytotoxic payloads and warheads market during the forecast period due to the high global prevalence of cancers such as breast, lung, and colorectal tumors. The increasing development of antibody-drug conjugates targeting specific tumor antigens has improved treatment potential. Advancements in tumor penetration and targeted delivery, along with a growing clinical pipeline and expanding approvals, have supported the segment’s significant contribution to the overall market.

The hematological malignancies segment held a market share of 38% in 2025 due to the high clinical success of antibody-drug conjugates in treating blood cancers, such as leukemia and lymphoma. These cancers often express well-defined target antigens, enabling effective and precise drug delivery. Additionally, earlier regulatory approvals. Strong treatment response rates and continuous research focus on hematological oncology have contributed to the segment’s dominant position in the market.

")

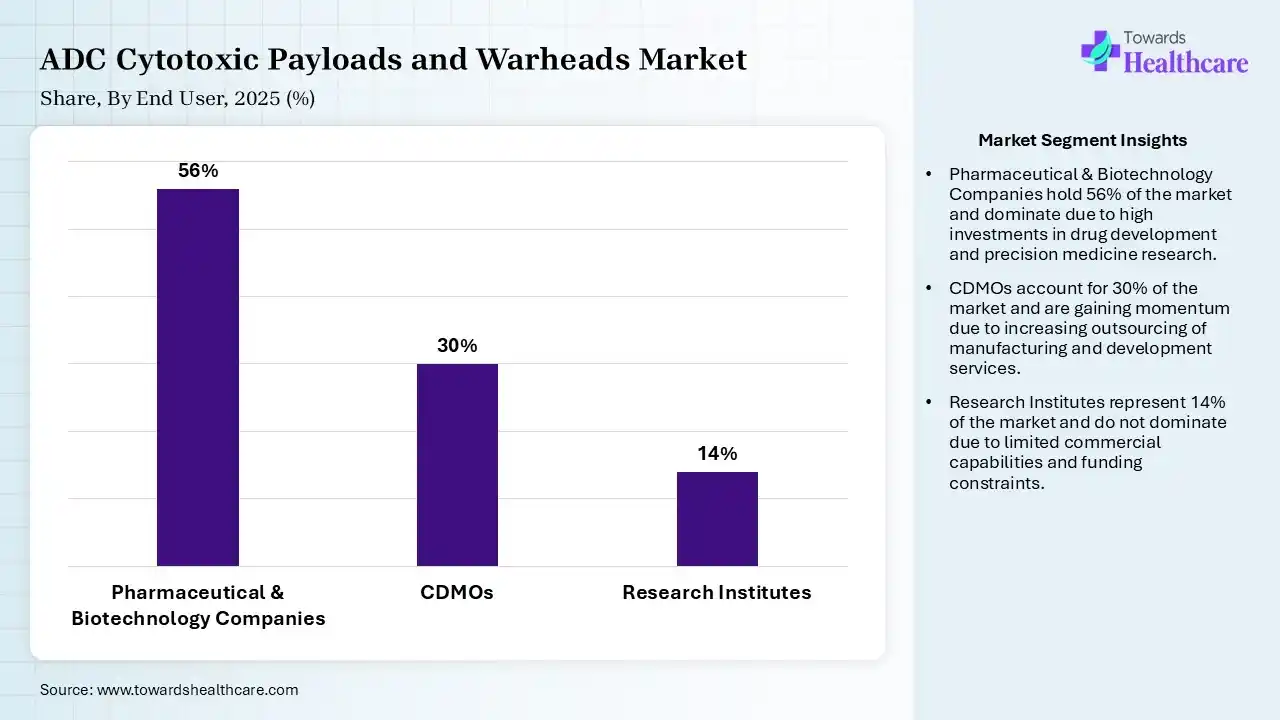

| Segment | Share 2025 (%) |

| Pharmaceutical & Biotechnology Companies | 56% |

| CDMOs | 30% |

| Research Institutes | 14% |

The Pharmaceutical & Biotechnology Companies Segment Led the Market in 2025 with the Largest Share

The pharmaceutical & biotechnology companies segment led the ADC cytotoxic payloads and warheads market with a share of 56% in 2025 due to their strong investment in research and development, advanced drug discovery capabilities, and active involvement in ADC innovation. These companies lead clinical trials, regulatory approvals, and commercialization of new therapies. Additionally, strategic collaborations, robust pipelines, and continuous focus on developing next-generation cytotoxic payloads and warheads have strengthened their leading position in the market.

The contract development & manufacturing organizations (CDMOs) segment held the second-largest share of 30% in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to increasing outsourcing of complex ADC production by pharmaceutical and biotechnology companies. These organizations offer specialized expertise, advanced manufacturing infrastructure, and cost-efficient scalability. Rising demand for high-potency payload handling, regulatory compliance support, and faster time-to-market has further strengthened their role in supporting ADC development and commercial production.

The research institutes segment held a 14% of ADC cytotoxic payloads and warheads market share in 2025 due to increasing focus on early-stage ADC discovery and innovation in novel cytotoxic payloads and warheads. Growing academic industry collaborations, rising government and private funding, and advancements in molecular biology are supporting this growth. These institutes play a key role in identifying new targets and improving payload design, and accelerating preclinical research, driving overall progress in the ADC development pipelines.

")

North America dominated the ADC cytotoxic payloads and warheads market with a share of 42% in 2025 due to its advanced healthcare infrastructure, strong presence of leading pharmaceutical and biotechnology companies, and high investment in oncology research. Early adoption of innovative therapies, robust clinical trial activity, and favorable regulatory support have accelerated ADC approvals. Additionally, growing cancer prevalence and continuous focus on precision medicine further strengthen the region’s leading market position.

U.S. Market Trends

The U.S. ADC cytotoxic payloads and warheads market is leading due to strong investment in oncology research, the presence of major pharmaceutical and biotechnology companies, and a robust clinical trial ecosystem. Early adoption of advanced therapies, continuous innovation in highly potent payloads, and supportive regulatory pathways have accelerated approvals, strengthening the country’s dominant position in the market.

Canada Market Trends

Canada is strengthening its ADC cytotoxic payloads and warheads market through growing investments in oncology research and biologics development. Universities, research centers, and biotechnology companies are working together to develop advanced cancer therapies. Government funding supports innovation in precision medicine and drug development. Pharmaceutical companies continue expanding research partnerships with specialized manufacturers. Canada provides a supportive environment for developing high-quality cytotoxic payload technologies and related manufacturing capabilities.

Mexico Market Trends

Mexico is gradually developing its ADC cytotoxic payloads and warheads market as pharmaceutical manufacturing capabilities continue improving. International companies are increasing collaborations with local organizations to support research and production activities. Growing investments in healthcare infrastructure and life sciences are encouraging innovation. Academic institutions are also contributing to biotechnology research. Mexico offers opportunities for companies seeking cost-effective manufacturing partnerships while expanding access to advanced oncology treatment technologies.

Asia Pacific held a market share of 22% in 2025 and is anticipated to grow at the fastest CAGR in the ADC cytotoxic payloads and warheads market due to increasing cancer prevalence, improving healthcare infrastructure, and rising investments in biotechnology and oncology research. Expanding clinical trial activity, growing presence of regional pharmaceutical companies, supportive government initiatives, access to advanced therapies, and a large patient pool further drive rapid market growth in the region.

India Market Trends

India is expected to grow at the fastest CAGR in the ADC cytotoxic payloads and warheads market due to rising cancer incidence, expanding healthcare infrastructure, and increasing investment in biotechnology and oncology research. Growing participation in clinical trials, supportive government initiatives, and the presence of cost-efficient manufacturing capabilities are accelerating ADC development. Additionally, improving access to advanced therapies and a large patient population further drives rapid market expansion.

China Market Trends

China is an important market for ADC cytotoxic payloads and warheads because of its strong pharmaceutical manufacturing base and expanding biotechnology sector. Companies are investing in advanced research facilities and specialized production technologies for complex oncology products. Partnerships with global pharmaceutical firms are increasing technology transfer and research activities. Skilled scientific talent and improving regulatory standards continue to support innovation. China offers attractive opportunities for contract manufacturing and product development.

Japan Market Trends

Japan remains a leading market for ADC cytotoxic payloads and warheads because of its advanced pharmaceutical industry and strong cancer research capabilities. Companies continue investing in innovative payload technologies and high-quality manufacturing processes. Close collaboration between biotechnology firms, academic institutions, and pharmaceutical companies supports the development of next-generation oncology therapies. Japan's experienced workforce, strong regulatory framework, and focus on innovation create favorable conditions for continued market growth.

| Ecosystem Category | Market Participants / Role |

| Technology Providers | Companies developing novel cytotoxic payload platforms including tubulin inhibitors, DNA-damaging agents, topoisomerase inhibitors, and novel warheads. |

| Product Manufacturers | Organizations producing commercial ADC payloads such as auristatins, maytansinoids, calicheamicins, and proprietary next-generation toxins. |

| Service Providers | Specialized providers offering payload synthesis, conjugation chemistry, analytical testing, and ADC development support. |

| Platform Providers | Companies developing ADC technology platforms integrating antibodies, linkers, and payload systems. |

| CROs/CDMOs | Organizations providing ADC development, GMP payload manufacturing, conjugation, and clinical supply services. |

| Software Vendors | Limited role; mainly computational chemistry, drug design, and molecular modeling platforms. |

| Research Institutions | Universities and oncology research centers developing novel cytotoxic molecules and ADC technologies. |

| End-User Industries | Pharmaceutical and biotech companies developing antibody-drug conjugates for oncology applications. |

Clinical Trials

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 70% | 25% | 5% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza | Basel, Switzerland | Switzerland | One of the largest ADC CDMO providers with commercial-scale payload and conjugation capabilities. | ADC development, cytotoxic payload manufacturing, linker-payload services |

| Bristol Myers Squibb | Lawrenceville, New Jersey, USA | USA | Major ADC developer with oncology portfolio and payload-based ADC programs. | ADC oncology programs, targeted cancer therapeutics |

| Daiichi Sankyo | Tokyo, Japan | Japan | Global ADC leader behind successful DXd payload technology platform. | DXd topoisomerase I inhibitor payload platform, ADC pipeline |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza | Basel, Switzerland | Switzerland | One of the largest ADC CDMO providers with commercial-scale payload and conjugation capabilities. | ADC development, cytotoxic payload manufacturing, linker-payload services |

| Bristol Myers Squibb | Lawrenceville, New Jersey, USA | USA | Major ADC developer with oncology portfolio and payload-based ADC programs. | ADC oncology programs, targeted cancer therapeutics |

| Daiichi Sankyo | Tokyo, Japan | Japan | Global ADC leader behind successful DXd payload technology platform. | DXd topoisomerase I inhibitor payload platform, ADC pipeline |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| ImmunoGen | Waltham, Massachusetts, USA | USA | Developed maytansinoid payload technologies used in ADCs. | DM1 payload technology, ADC innovation |

| Molecular Templates | Austin, Texas, USA | USA | Works on targeted toxin-based oncology platforms. | Engineered toxin payload approaches |

| NBE Therapeutics | Basel, Switzerland | Switzerland | ADC-focused biotechnology company acquired for payload and conjugation expertise. | Novel ADC payload-linker technologies |

Strengths

Weaknesses

Opportunities

Threats

By Payload Type

By Warhead Potency

By Mechanism of Action

By Linker Compatibility

By Conjugation Technology Compatibility

By Application

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar