The China pharmaceutical market size was estimated at USD 86.34 billion in 2025 and is predicted to increase from USD 93.11 billion in 2026 to approximately USD 183.66 billion by 2035, expanding at a CAGR of 7.84% from 2026 to 2035. China’s huge burden of ageing population, emerging chronic illnesses, an emphasis on VBP, & wider demand for oncology drugs, fuel the overall market expansion.

")

The respective market is recognised as the world’s leading manufacturer of active pharmaceutical ingredients (APIs) & a surging powerhouse in groundbreaking biomedical research worldwide. The overall progression of the pharmaceutical industry in China is fueled by an exponentially growing geriatric population, with massive structural demand from huge patient pools, which further necessitate long-term care & treatments for chronic issues. Moreover, China is facing a vast number of cancer cases & metabolic and respiratory diseases, demand for the latest targeted therapies, driving oncology & biopharmaceuticals to the frontline. Pivotal involvement of proactive state encouragement emphasising improvement in drug accessibility & quality through merged regulations.

Primarily, various Chinese AI biotech leaders are highly employing sophisticated algorithms, such as Generative Adversarial Networks (GANs) & multi-agent systems to highlight biological targets & evolve drug candidates in a fraction of the traditional time. Besides this, substantial Western pharmaceutical giant companies have inked notable deals with Chinese AI-powered labs, citing minimal expenditures, access to vast & different datasets, & specialized progression periods.

Bolstering Global Out-Licensing

Many Chinese pharmaceutical & biotech firms are continuing to break historic records in cross-border licensing deals, which is mainly propelled by increasing demand from Western pharma experiencing patent cliffs, Chinese pipelines, especially in oncology & Antibody-Drug Conjugates (ADCs).

Spotlighting AI-enabled Drug Discovery

Specifically, XtalPi, Insilico Medicine, & Helixon in China are leveraging deep learning & robotics to reduce target identification & molecular screening timelines.

Extensive Cell and Gene Therapy (CGT)

Numerous Chinese clinical trials are aiming at a rapid development of CGT products, coupled with advances in CAR-T therapies & CRISPR gene-editing innovations to cure genetic & complex diseases.

| Table | Scope |

| Market Size in 2026 | USD 93.11 Billion |

| Projected Market Size in 2035 | USD 183.66 Billion |

| CAGR (2026 - 2035) | 7.84% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Type, By Product type, By Molecule Type, By Therapeutic Area, By Route of Administration, By Distribution Channel, By Manufacturing Type, By Formulation, By End User |

| Top Key Players | Shanghai Pharmaceuticals, Sinopharm Group, Jiangsu Hengrui Medicine, China Resources Pharmaceutical, CSPC Pharmaceutical Group, BeiGene, Shanghai Fosun Pharmaceutical, Yunnan Baiyao Group, Sino Biopharmaceutical, Hansoh Pharmaceutical |

")

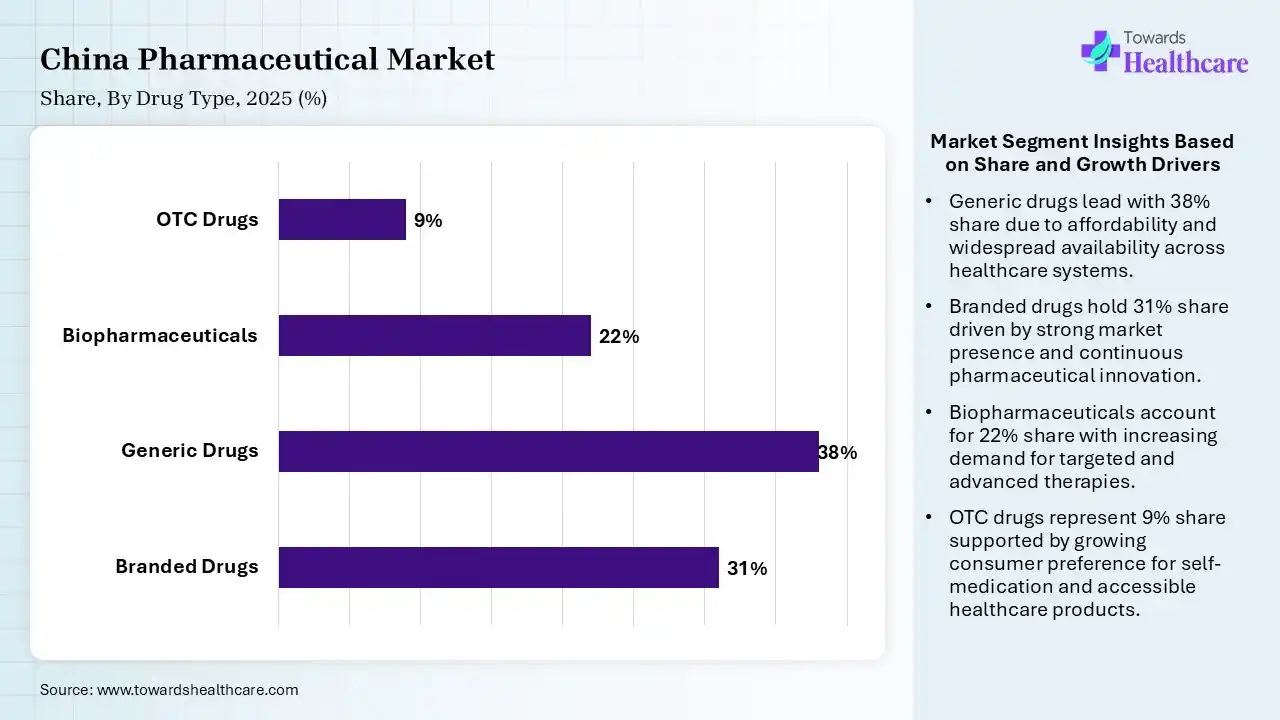

| Segment | Share 2025 (%) |

| Branded Drugs | 31% |

| Generic Drugs | 38% |

| Biopharmaceuticals | 22% |

| OTC Drugs | 9% |

The Generic Drugs Segment Dominated the Market in 2025

In 2025, the generic drugs segment held a 38.0% share of the China pharmaceutical market. A crucial catalyst is the emergence of volume-based procurement, which spurs local manufacturers to substantially decrease their proposals in exchange for guaranteed hospital volumes. Especially, Beijing is widely pushing accessibility to essential medications at a cost-effective price for a huge, diverse population, which demands generic drugs massively.

However, the branded drugs segment captured the second-largest share of a 31.00% in 2025, due to strong physician preference for novel therapies. Alongside, the progression of specialty medicines assists in premium pricing strategies, while urban hospitals are highly using patented therapies in chronic conditions.

The biopharmaceuticals segment accounted for a 22.0% share in 2025 & is predicted to expand at a 11.20% CAGR in the China pharmaceutical market. A prominent catalyst is growing oncology & immunology incidences, driving higher biologics adoption across the nation. Whereas domestic biotech investments are reinforcing monoclonal antibody production, coupled with regulatory changes, push biologic approvals & commercialization.

The OTC drugs segment held 9.00% share in 2025, as China is strengthening consumer awareness regarding preventive healthcare, spurring OTC purchases. Additionally, the revolutionary expansion of e-commerce pharmacies is enhancing accessibility in lower-income cities.

")

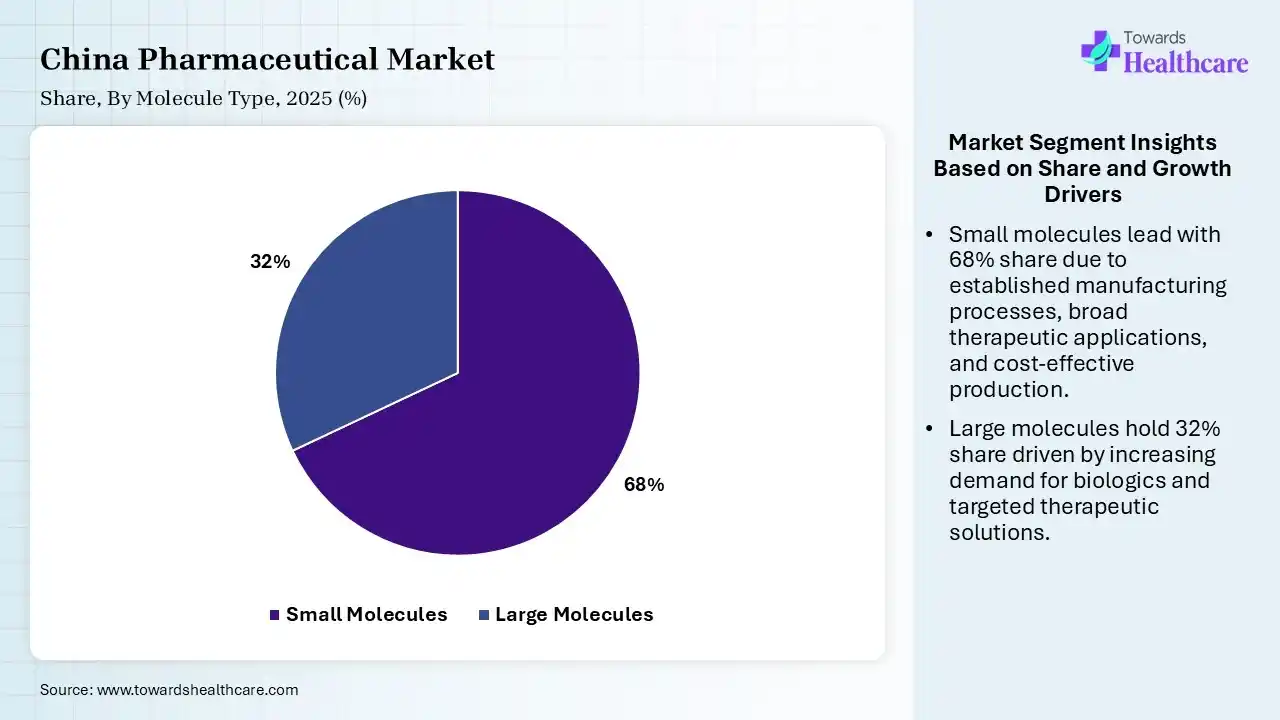

| Segment | Share 2025 (%) |

| Small Molecules | 68% |

| Large Molecules | 32% |

The Small Molecules Segment Led the Market in 2025

The small molecules segment held a major share of 68.0% of the market in 2025. The dominance is propelled by a wider focus on inexpensive, large-scale patient recruitment for clinical trials, integrated with prominent government R&D funding, which speeds up small molecule discovery, specifically for targeted therapies & tailored medicine. Broadening clinical interest in small molecules for their ability to easily penetrate cells & treat intracellular targets impacts the segmental growth.

Moreover, the large molecules segment captured for 32.0% share in 2025 & is estimated to show rapid expansion at a 11.60% CAGR in the China pharmaceutical market. Accelerating cancer prevalence is driving higher usage of biologic therapy, which raises the development of large molecules. Ongoing biologics innovations and biosimilars commercialisation fuel the major investments & improvement in the affordability of large molecules.

")

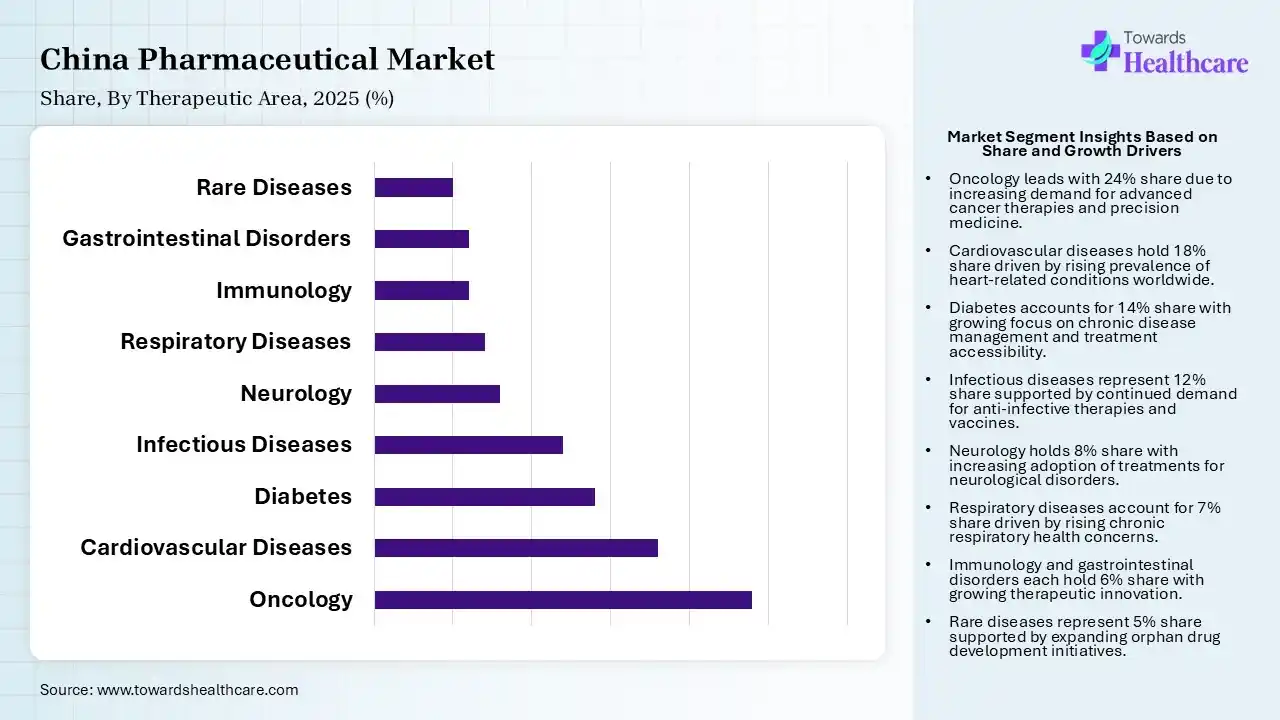

| Segment | Share 2025 (%) |

| Oncology | 24% |

| Cardiovascular Diseases | 18% |

| Diabetes | 14% |

| Infectious Diseases | 12% |

| Neurology | 8% |

| Respiratory Diseases | 7% |

| Immunology | 6% |

| Gastrointestinal Disorders | 6% |

| Rare Diseases | 5% |

The Oncology Segment Was Dominant in the Market in 2025

In 2025, the oncology segment led with a 24.0% share in 2025 & is anticipated to expand at a 11.8% CAGR in the coming era. China is experiencing approximately 5 million new cases of cancer annually, which largely and consistently demand oncology therapeutics. Emerging simplifies processes to fast-track oncology drugs by the National Medical Products Administration (NMPA), supporting prospective innovations in cancer drugs.

The cardiovascular diseases segment held the second-largest share of a 18.00% of the China pharmaceutical market. Surging national ageing population & urban lifestyle changes are highly prone to hypertension & heart disease cases. This further necessitates preventive screening programs, which bolster cardiovascular drug prescriptions.

However, the diabetes segment accounted for a 14.00% share in 2025, due to China’s large diabetic population, which fuels continuous demand for insulin. Alongside, the widespread adoption of GLP-1 therapies is fostering diabetes management.

The infectious diseases segment held a 12.00% share in 2025. Widening public health preparedness assists antivirals & vaccine procurement activities. Additionally, hospital infection management drives antibiotic consumption levels. Moreover, government immunization incentives are empowering vaccine distribution.

")

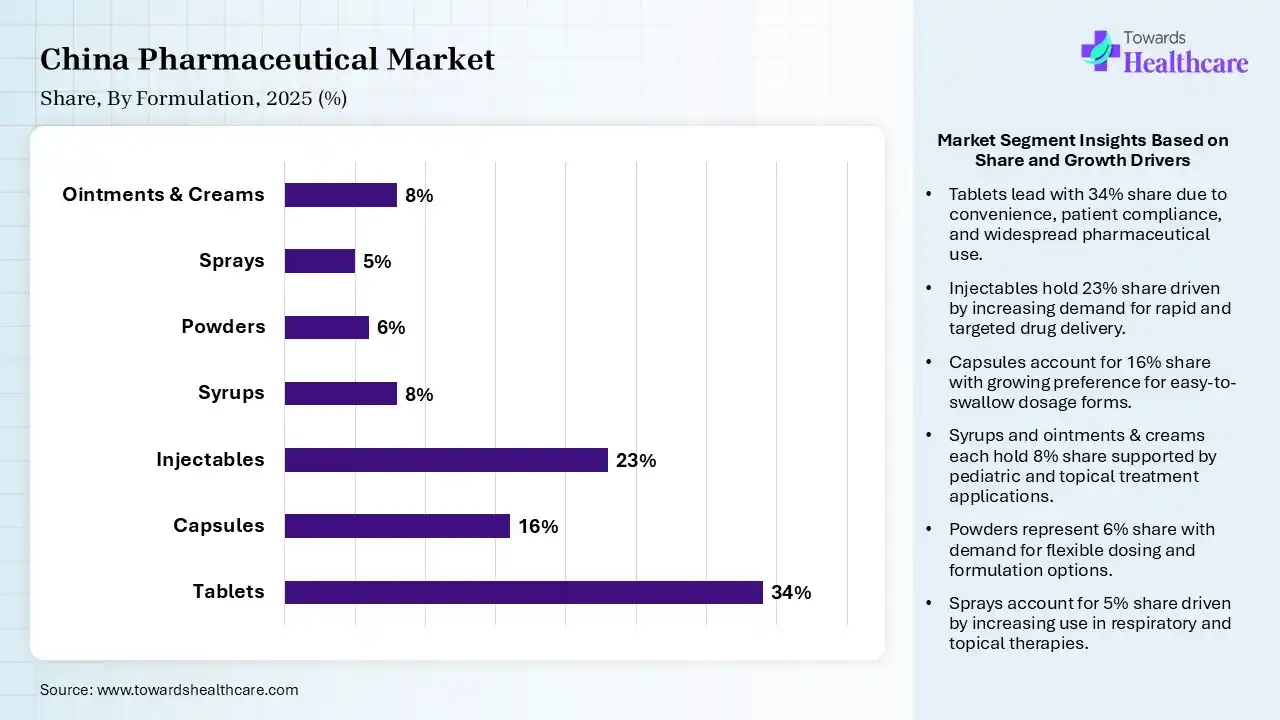

| Segment | Share 2025 (%) |

| Tablets | 34% |

| Capsules | 16% |

| Injectables | 23% |

| Syrups | 8% |

| Powders | 6% |

| Sprays | 5% |

| Ointments & Creams | 8% |

The Tablets Segment Dominated the Market in 2025

In 2025, the tablets segment led with a 34.0% share of the China pharmaceutical market. A broader integration of the domestic supply chain in China enables local manufacturers to manufacture oral solid doses highly affordable. Besides this, local biotech labs are increasingly investing in new small-molecule tablets, like targeted oncology & metabolic therapies, to highlight unfulfilled medical requirements.

The injectables segment captured a 23.0% share in 2025 & is predicted to expand at a 10.50% CAGR. Advancing biologic therapies & hospitals treatments are raising the use of injectables. Especially, oncology and emergency care are widely demanding this kind of formulation. Consistent sterile manufacturing investments are bolstering domestic production capacity.

The capsules segment held a 16.00% share in 2025 in the China pharmaceutical market, due to optimized bioavailability and patient compliance. China is extensively spurring nutraceutical and specialty drugs, which demand capsule formulation. Robust premium formulations are highly using capsule delivery systems.

The syrups segment held a notable share of 8.00% in 2025, due to the growing demand by the pediatric & geriatric population. Also, respiratory infection treatments are sustaining seasonal product consumption, coupled with improved flavour technologies & boosted patient adherence.

")

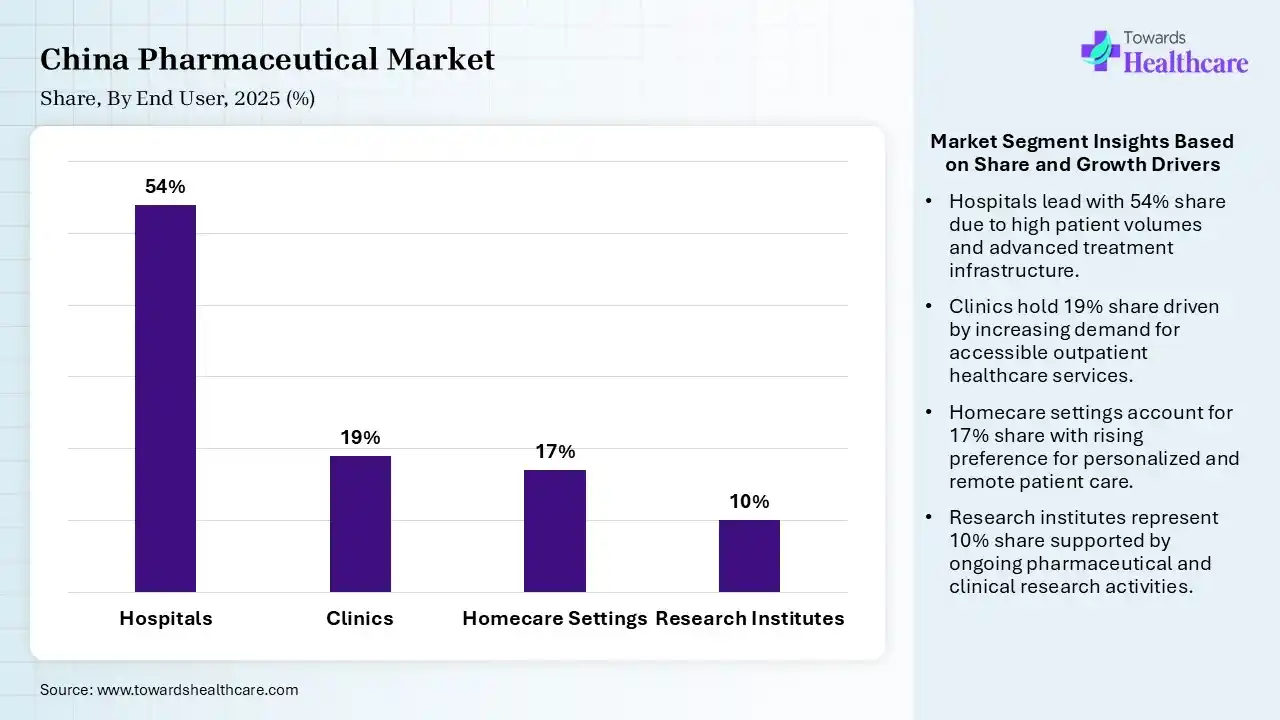

| Segment | Share 2025 (%) |

| Hospitals | 54% |

| Clinics | 19% |

| Homecare Settings | 17% |

| Research Institutes | 10% |

The Hospitals Segment Led the Market in 2025

The hospitals segment captured a dominant share of 54.0% of the China pharmaceutical market in 2025. Dominance is driven by public hospitals that are serving as the primary point of care for prescription drug dispensing, crucially transforming national procurement volumes, reimbursement approvals, & technology adoption. The Chinese government is actively fostering patient volume to step toward domestic community healthcare centers, which impacts multinational & domestic pharma companies.

The clinics segment accounted for 19.00% share in 2025, due to revolutionary efforts enhancing clinic-level pharmaceutical access. Whereas urban outpatient treatment demand is supporting medicine consumption. Ongoing chronic disease management programs are reinforcing clinic usage.

The homecare settings segment held a 17.0% share in 2025 & is estimated to grow at a 10.10% CAGR. Respective expansion is propelled by booming ageing population demands for home-based chronic disease treatment. Alongside, greater telemedicine adoption is enhancing medicine accessibility for homecare patients.

Moreover, the research institutes segment accounted for a 10.00% share of the China pharmaceutical market. Many pharmaceutical R&D investments are empowering research medicine utilization. Government innovation programs and clinical trial expansion are impelling institutional drug innovation & research activities.

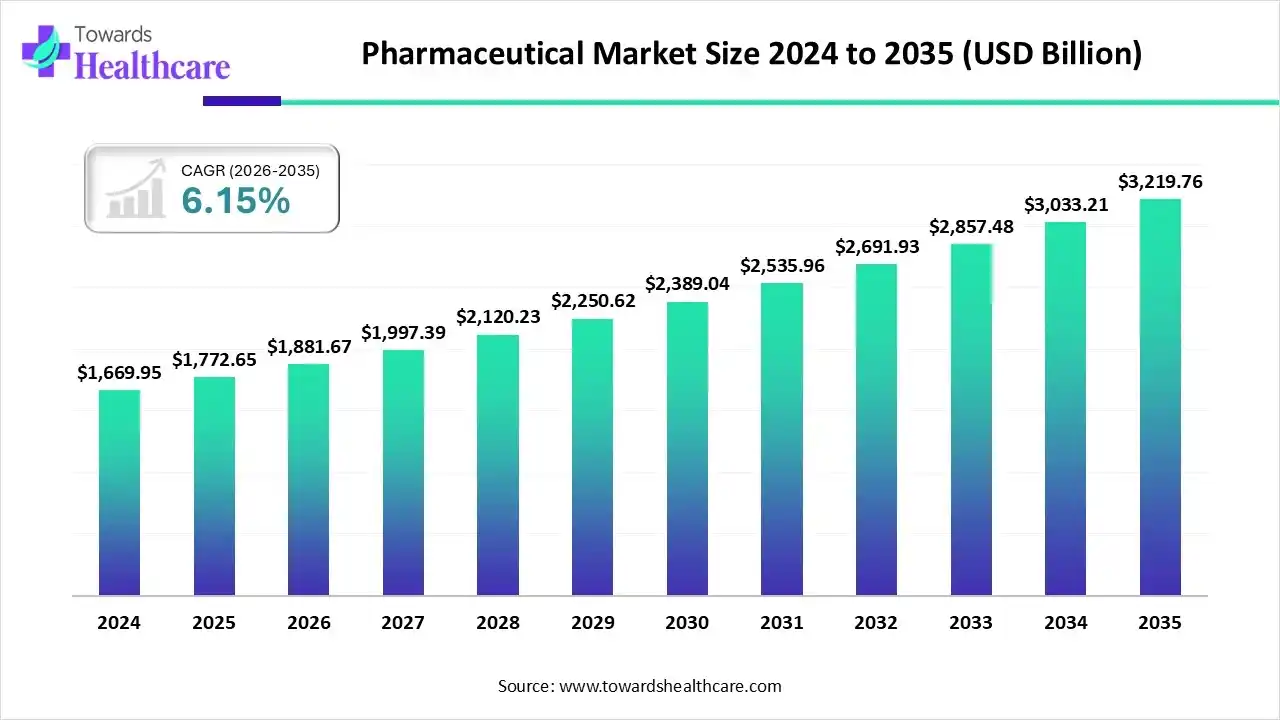

The pharmaceutical market size marked US$ 1772.65 billion in 2025 and is forecast to experience consistent growth, reaching US$ 1881.67 billion in 2026 and US$ 3219.76 billion by 2035 at a CAGR of 6.15%.

")

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Companies | Description |

| Shanghai Pharmaceuticals | This firm specialises in both drug distribution & the research and manufacturing of medical products. |

| Sinopharm Group | Its offerings cover a strong logistics & supply chain backbone for drug distribution across China. |

| Jiangsu Hengrui Medicine | A leader highly focuses on the development of novel oncology therapies & treatments. |

| China Resources Pharmaceutical | This massively covers the comprehensive pharmaceutical value chain, from R&D & production to retail pharmacy. |

| CSPC Pharmaceutical Group | A company specializes in stroke drugs, innovative medicines, & active pharmaceutical ingredients (APIs). |

| BeiGene | This biotech firm offers innovative targeted therapies & immuno-oncology. |

| Shanghai Fosun Pharmaceutical | Its offerings comprise medical devices, diagnostics, private hospitals, & drug R&D. |

| Yunnan Baiyao Group | It is a key player in combining ancient Traditional Chinese Medicine (TCM) with modern pharmaceuticals & daily health consumer products. |

| Sino Biopharmaceutical | This mainly provides therapeutic drugs for liver health, vaccines, and infectious diseases. |

| Hansoh Pharmaceutical | It is a prominent producer of anti-cancer APIs & new drugs. |

Strengths

Weaknesses

Opportunities

Threats

By Drug Type

By Product type

By Molecule Type

By Therapeutic Area

By Route of Administration

By Distribution Channel

By Manufacturing Type

By Formulation

By End User

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar