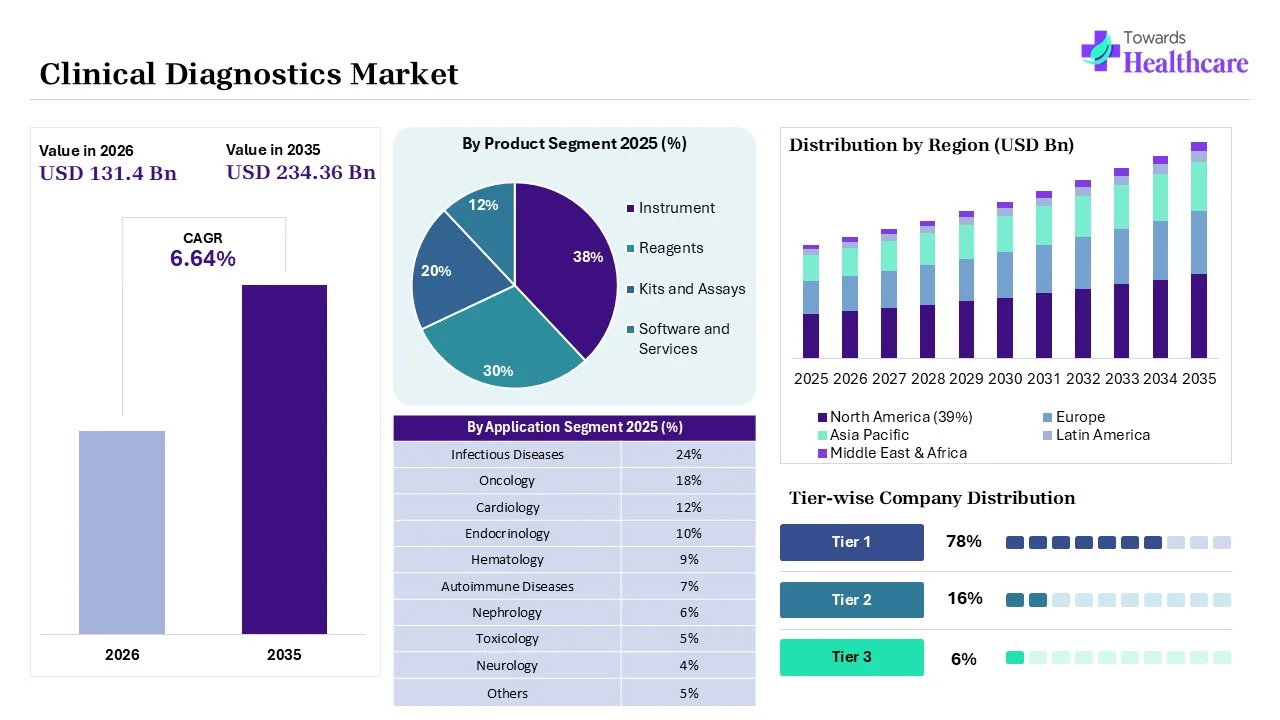

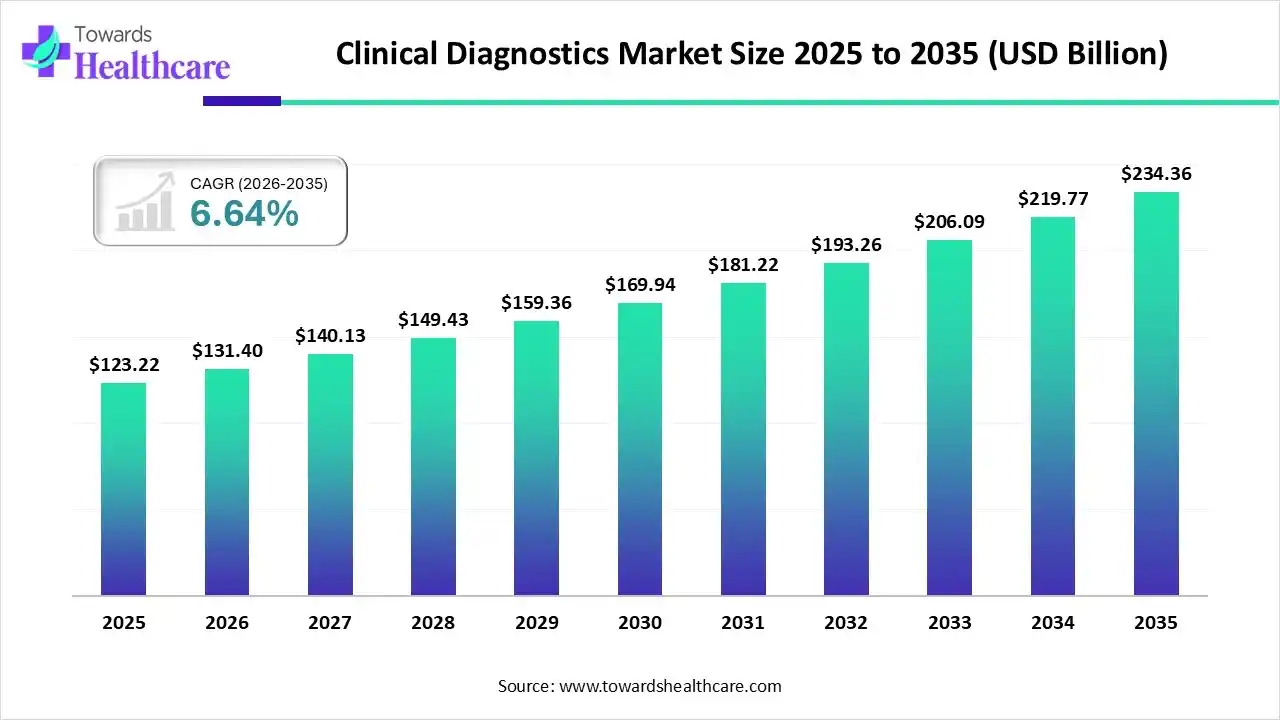

The global clinical diagnostics market size was estimated at USD 123.22 billion in 2025 and is predicted to increase from USD 131.4 billion in 2026 to approximately USD 234.36 billion by 2035, expanding at a CAGR of 6.64% from 2026 to 2035.

The era is experiencing a significant rise in various infectious diseases and different cancer cases, which fosters demand for advanced diagnosis for early detection. Alongside, the leading companies are putting efforts into developing AI-powered diagnostic solutions, wearable sensors, and home care approaches.

The accelerating cases of diverse chronic diseases, like cancer, diabetes and infectious conditions, are fueling the need for early detection through this diagnosis process. The market is bolstering due to the development of non-invasive blood tests for early-stage cancer detection, supporting liquid biopsy progressing. Alongside, the leading firms are exploring quicker, at-home molecular tests & wearables, which enhance proactive health management.

Next-Generation Diagnostics Are Revolutionizing Modern Clinical Healthcare

Clinical diagnostics refers to the use of laboratory tests, imaging techniques, and diagnostic technologies to detect, diagnostics, monitor, and manage disease, enabling timely clinical decision-making and improved patient outcomes. The clinical diagnostics market is expanding due to the increasing emphasis on early disease detection and rising demand for personalized healthcare. Key trends include the rapid adoption of point-of-care testing, molecular diagnostics, and multi-omics technologies for precise disease identification. Technological advancements such as AI-powered diagnostic platforms, laboratory automation, next-generation sequencing, and digital pathology are enhancing diagnostic speed and accuracy. Future opportunities are driven by expanding preventive healthcare programs, increasing home-based diagnostic testing, integration of cloud-connected diagnostic systems, and continued investments in precision medicine, biomarker discovery, and advanced laboratory infrastructure.

Nowadays, AI algorithms are widely employed in the analysis of CT scans, X-rays, & MRIs, with tools to highlight tumours and anomalies early. Alongside, AI is extensively fostering the pathology area through the robust scanning of whole slide images to determine cancer cells. Recently, Noul’s AI has showcased advances in the study of blood cell morphology for faster diagnosis in under-resourced areas.

Spurring Precision Medicine & Multi-omics

The market is increasingly promoting Companion Diagnostics (CDx) and multi-omics to personalize treatments based on an individual's genetic profile & environment.

Broadening Disease Scanning

Nowadays, the globe is strongly expanding testing for conditions, such as hepatitis B, diabetes, & cardiovascular diseases, and also developed emphasis on neurodegenerative diseases.

Modern Laboratories & Automation

Day by day, leaders are focusing on implementing robotics, AI, and IoT (Internet of Things) to manage accelerating test volumes, ensure quality control, and optimise operational effectiveness.

| Key Elements | Scope |

| Market Size in 2026 | USD 131.4 Billion |

| Projected Market Size in 2035 | USD 234.36 Billion |

| CAGR (2026 - 2035) | 6.64% |

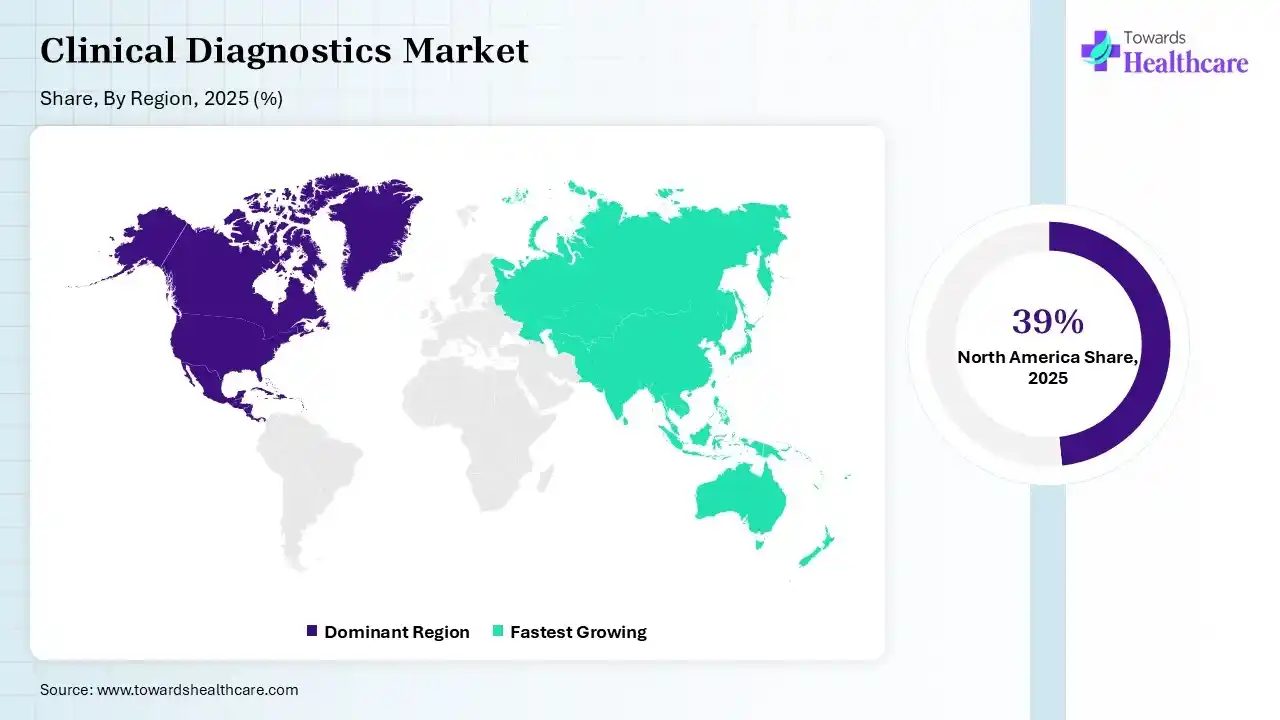

| Leading Region | North America by 39% |

| Key Applications | Infectious disease testing, oncology diagnostics, clinical chemistry, immunoassays, hematology, molecular diagnostics, genetic testing, microbiology, companion diagnostics |

| Primary End Users | Hospitals, diagnostic laboratories, physician offices, reference laboratories, academic medical centers, public health agencies |

| Key Challenges | Regulatory compliance, reimbursement pressure, pricing competition, laboratory workforce shortages, data integration complexity |

| Market Segmentation | By Product, By Application, By End Use, By Region |

| Top Key Players | Abbott, bioMérieux SA, QuidelOrtho Corporation, Siemens Healthineers AG, Bio-Rad Laboratories, Inc.,Qiagen, Charles River Laboratories, Agilent Technologies, Inc. |

| Segments | Shares % |

| Instrument | 38% |

| Reagents | 30% |

| Kits and Assays | 20% |

| Software and Services | 12% |

Which Product Dominated the Clinical Diagnostics Market in 2025?

In 2025, the instrument segment captured a major revenue share of 38% of the market. This involves different kinds of analyzers for chemistry, hematology, and molecular diagnostics, which show rapid, more accurate, and reliable test results in the booming chronic conditions. PCR machines, mass spectrometers, and imaging systems are substantial instruments widely used. However, the key advances include exploration of AI solutions, sophisticated POCT, lab automation and the widespread adoption of LC-MS.

Software And Services

Moreover, the software and services segment is anticipated to expand fastest. Software has a major role in sampling, monitoring, data management, and automated reporting. Advanced companies are fostering cloud-bases solution to execute rigorous data storage, remote access, and analysis. The latest innovation comprises Tempus (Tempus ONE), a tailored medicine platform to combine genomic sequencing with clinical data and further provide AI-enabled therapy recommendations, especially in oncology, neurology and cardiology.

| Segments | Shares % |

| Infectious Diseases | 24% |

| Oncology | 18% |

| Cardiology | 12% |

| Endocrinology | 10% |

| Hematology | 9% |

| Autoimmune Diseases | 7% |

| Nephrology | 6% |

| Toxicology | 5% |

| Neurology | 4% |

| Others | 5% |

How did the Infectious Diseases Segment Lead the Market in 2025?

The infectious diseases segment dominated with the largest share of 24% of the clinical diagnostics market in 2025. Key drivers are a rise in instances of influenza, hepatitis, and HIV, as well as new threats like Zika, Ebola and significant developments in molecular diagnostics. For these cases, the market has shown robustness of AI-assisted smartphone readers for lateral-flow assays (LFAs) to convert qualitative, visual tests into semi-quantitative, digital results, which lowers false negatives in earlier infection stages.

Oncology

On the other hand, the oncology segment will expand rapidly. A huge burden of cancer cases is driven by the rising geriatric population, environmental factors, and lifestyle changes. This is further demanding novel precision treatments and sophisticated molecular diagnostics, like liquid biopsy. Recently evolved AI-powered platforms, such as ComPath AI & Prov-GigaPath, are assisting in the analysis of whole-slide images to detect tumor patterns and biomarkers.

")

| Segments | Shares % |

| Hospitals and Clinics | 52% |

| Diagnostic Laboratories | 30% |

| Public Health Screening Programs | 10% |

| Home Care Settings | 8% |

Which End Use Dominated the Clinical Diagnostics Market in 2025?

The hospitals and clinics segment registered dominance in the market by 52% share in 2025. Globally escalating requirement for early detection to lower long-term treatment spending and raise patient outcomes is propelling the segmental growth. They are highly adopting on-site, immediate, or decentralized tests to accelerate diagnosis. The era is booming with efforts into "phygital", i.e. physical + digital solutions, encouraging AI-enabled automation, and strengthening point-of-care testing (POCT).

Home Care Settings

Moreover, the home care settings segment will witness rapid expansion. Day by day, the world is demanding immediate, user-friendly, and independent testing, alongside rising healthcare expenditures, which are fueling the progression of home-based care solutions. The latest groundbreakings include AI integration into home testing kits and wearables, extensive wearable sensors, and at-home molecular testing, like PCR.

")

North America was dominant in the clinical diagnostics market by 39% share due to the presence of a well-established healthcare infrastructure and broader adoption of molecular diagnostics. Furthermore, the region is emphasizing the development of over-the-counter (OTC) molecular tests, including at-home COVID-19/flu kits. Whereas, hospitals in Ontario, especially London Health Sciences Centre, are locating digital navigators to support patients in navigating virtual care platforms & clarifying digital health data.

U.S. Market Trends

However, the U.S. held the biggest share of this region, due to the growing advances in liquid biopsies, rapid POCT molecular diagnostics for infectious diseases, and other immersive AI-enhanced approaches.

For instance,

Canada’s Advanced Healthcare Infrastructure is Driving Clinical Diagnostics Market Growth

Canada’s clinical diagnostics market is growing significantly due to its significantly due to its strong healthcare infrastructure, increasing prevalence of chronic and infectious diseases, and rising emphasis on early disease detection. Growing adoption of molecular diagnostics efficiency. Additionally, government investments in healthcare modernization, expanding precision medicine initiatives, and increasing demand for personalized diagnostics are supporting sustained market growth.

Asia Pacific is anticipated to expand rapidly in the clinical diagnostics market, due to certain major countries, like China, India, and Japan, which are facing a greater burden of a geriatric population, who are highly prone to an increase in severe health issues. Besides this, continuous breakthroughs in molecular diagnostics, POCT, & next-generation sequencing are transforming to make tests quicker, more accurate, & more accessible. Recently, in Singapore, Synapxe executed "Russel GPT" to abridge patient data & support in clinical decisions.

India Market Trends

India’s significant firms are broadly promoting preventive and genomic medicine, such as Agilus Diagnostics, fostering specialized & genomics-led testing for tailored medicine. However, MapmyGenome & Med Genome are exploring modern genetic testing to develop a precision treatment strategy.

In January 2026, Biopeak raised USD 2.7 million in its latest funding round, empowered by repeat investor Nikhil Kamath to establish structured, preventive & longevity-focused clinical care models in India.

China’s Expanding Healthcare Modernization is Fueling Clinical Diagnostics Market Growth

China clinical diagnostics market is growing notably due to increasing healthcare expenditure, rising prevalence of chronic and infectious diseases, and rapid expansion of diagnostics laboratory infrastructure. Strong government support healthcare modernization, growing adoption of molecular diagnostics and AI-enabled testing platforms, and increasing domestic diagnostics manufacturing are accelerating market growth. Additionally, expanding preventive healthcare programs and precision medicine initiatives are creating long-term opportunities.

Europe's clinical diagnostics market is growing significantly due to its well-established healthcare infrastructure, increasing demand for early disease detection, and widespread adoption of molecular diagnostics and laboratory automation. Strong government support for preventive healthcare, expanding precision medicine initiatives, and continuous investments in diagnostic innovation are further accelerating regional market growth.

The UK's Precision Medicine Initiatives Are Accelerating Market Expansion

The UK's clinical diagnostics market is expanding significantly due to increasing demand for early and accurate disease detection, strong adoption of molecular diagnostics, and growing investments in precision medicine. Supportive government healthcare initiatives, expanding laboratory automation, and the integration of AI-based diagnostic technologies are improving diagnostic efficiency. Additionally, rising clinical research activities and increasing focus on personalized healthcare are driving sustained market growth.

Germany's Diagnostic Innovation Is Driving Clinical Diagnostics Market Growth

Germany's clinical diagnostics market is growing notably due to its advanced healthcare infrastructure, strong diagnostic manufacturing capabilities, and increasing adoption of molecular and automated testing technologies. Rising investments in precision medicine, expanding laboratory modernization, and growing demand for early disease detection are supporting market expansion. Additionally, robust research activities and favorable healthcare reimbursement policies are accelerating the adoption of innovative diagnostic solutions.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Roche Diagnostics, Abbott, Danaher, Siemens Healthineers | Develop diagnostic platforms, analyzers, automation systems, molecular testing technologies |

| Product Manufacturers | Roche Diagnostics, Abbott, Sysmex, bioMérieux, QuidelOrtho | Manufacture instruments, reagents, consumables, test kits |

| Service Providers | Labcorp, Quest Diagnostics, Sonic Healthcare | Offer clinical testing and laboratory services |

| Platform Providers | Roche Diagnostics, Siemens Healthineers, Danaher (Beckman Coulter, Cepheid) | Integrated diagnostic ecosystems including instruments, software, and workflows |

| CROs/CDMOs | ICON plc, IQVIA, Charles River Laboratories | Support diagnostic assay validation, clinical studies, biomarker development |

| Software Vendors | Oracle Health, Epic Systems, CliniSys, Thermo Fisher Scientific | Laboratory Information Systems (LIS), data management, workflow integration |

| Research Institutions | Mayo Clinic, Cleveland Clinic, Broad Institute, Karolinska Institute | Biomarker discovery, assay validation, translational diagnostics research |

| End-User Industries | Hospitals, Reference Laboratories, Public Health Agencies, Biopharma Companies | Deploy diagnostics for patient care, clinical trials, and disease surveillance |

R&D

Clinical Trials & Regulatory Approvals

Patient Support & Services

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Roche Diagnostics | Rotkreuz, Zug | Switzerland | Global diagnostics leader with broad IVD portfolio | Cobas Systems, Molecular Diagnostics, Immunoassays |

| Abbott Laboratories | Abbott Park, Illinois | USA | Strong position across immunoassays and point-of-care diagnostics | Alinity Platform, ID NOW, ARCHITECT |

| Danaher Corporation | Washington, D.C. | USA | Owns leading diagnostic brands including Cepheid and Beckman Coulter | GeneXpert, Beckman Coulter Diagnostics |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| bioMérieux | Marcy-l'Étoile, Auvergne-Rhône-Alpes | France | Global microbiology and infectious disease diagnostics leader | VITEK, BIOFIRE, Microbiology Systems |

| Sysmex Corporation | Kobe, Hyogo | Japan | Global hematology market leader | Hematology Analyzers, Urinalysis Systems |

| Becton Dickinson and Company | Franklin Lakes, New Jersey | USA | Strong infectious disease and microbiology diagnostics portfolio | BD MAX, BD Kiestra |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Exact Sciences | Madison, Wisconsin | USA | Leader in molecular cancer screening diagnostics | Cologuard, Oncotype DX |

| Guardant Health | Palo Alto, California | USA | Pioneer in liquid biopsy and precision diagnostics | Guardant360, Shield |

| Natera | Austin, Texas | USA | Fast-growing molecular diagnostics provider | Signatera, Panorama |

Strengths

Weaknesses

Opportunities

Threats

By Product

By Application

By End Use

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar