Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

The full coverage chemotherapy market is rapidly advancing on a global scale, with expectations of accumulating hundreds of millions in revenue between 2025 and 2034. Market forecasts suggest robust development fueled by increased investments, innovation, and rising demand across various industries.

Across the globe, the acceleration of different types of blood cancers and breast cancers is increasingly fueling demand for highly effective and advanced chemotherapy agents. Along with this, the global full coverage chemotherapy market encompasses several public and private insurance programs for widespread coverage of chemotherapy services, like diagnosis, treatment, and hospital visits. Moreover, breakthroughs in traditional cytotoxic drugs, combination therapies, antiemetics, adjunctive agents (e.g., G-CSF, erythropoiesis-stimulating agents), and infusion technologies are assisting overall market expansion. Mainly, numerous government initiatives for cancer treatment support the detection and adoption of novel therapies.

The full coverage chemotherapy market refers to the global ecosystem of pharmaceutical drugs, supportive care products, and administration services designed to deliver comprehensive chemotherapy regimens for cancer treatment. It encompasses traditional cytotoxic drugs, combination therapies, antiemetics, adjunctive agents (e.g., G-CSF, erythropoiesis-stimulating agents), and infusion technologies. The term "full coverage" implies inclusion of all components: drug formulation, administration support, toxicity management, and insurance reimbursement services delivered either via hospitals, outpatient clinics, or home care.

In 2025, AI is emerging as a crucial part in the market, whereas increasing demand for precision treatment and breakthroughs in AI technology are boosting the comprehensive adoption of AI tools. In this market, AI supports in accelerating different aspects of cancer treatment, such as diagnosis, treatment planning, and personalized medicine. Moreover, AI algorithms assist in the analysis of a large volume of datasets of patient data, comprising medical images, genomic information, and treatment history, to anticipate treatment results, determine optimal drug combinations, and customize chemotherapy regimens for individual patients.

Phenomenal Drug Development and Rising Demand for Chemotherapy

Primarily, the full coverage chemotherapy market is driven by a growing prevalence of diverse cancers. Despite ongoing exceptional innovations in the chemotherapy drug development process, including chemotherapy drug formulations, delivery systems, and an escalation of emphasis on targeted therapies, this is also fueling the market expansion. As mentioned, a rise in the burden of cancer cases requires highly demanding chemotherapy drugs and services, employed in conjunction with other measures, like surgery or radiation therapy.

High Expenses of Services and Safety Issues

As with many chemotherapy treatments, such as the drugs themselves and related services, they are expensive, which creates a vital hurdle to access for numerous patients, especially in developing countries. And, this delay in treatments further affects the overall outcomes in patients. Alongside, adherence to regulatory guidelines and highlighting safety concerns is one more restraining aspect for different healthcare providers.

Advancements in Chemotherapy and Expansion in Home Care Settings

During 2025-2034, the global full coverage chemotherapy market will encompass several opportunities, first of all, the innovations in chemotherapy. These novel solutions will comprise antibody-drug conjugates (ADCs), combination approaches, like immunotherapy and targeted therapies, with increased efficacy and minimized side effects. Furthermore, a significant opportunity will develop in chemotherapy-induced myelosuppression incidences. Also, currently, the globe is putting efforts to establish home care settings or home chemotherapy services with the completion of convenience and accessibility among patients.

In 2024, the alkylating agents segment held the dominating share of the market. These agents have versatile activity in a variety of cancers, particularly in lung cancer, leukemia, lymphoma, and several solid tumors. Along with this, the incorporation of these agents in novel combination chemotherapy treatments and optimized formulations with raised efficacy and reduced harmful effects is fueling the widespread adoption in developing cancer cases across the world.

The targeted chemotherapy combinations segment is estimated to grow rapidly, with contributions from various approaches. Mainly, the adoption of immunotherapy & targeted therapy, as well as targeted therapies & chemotherapy agents, is propelling the segment expansion. These combinations provide enhanced effectiveness to resolve drug resistance issues and decreased toxicity, assisting in boosting overall treatment outcomes. Besides this, multiple targeted therapies are widely used simultaneously to address different pathways and ultimately accelerate results.

The intravenous segment was dominant in the full coverage chemotherapy market in 2024. Numerous advantages of this route of administration are offering a quick drug delivery, ensuring immediate therapeutic concentrations, and it is often the first choice in hospital settings for safety and sterility concerns. IV route is frequently preferred in many advanced cancers where systemic and targeted treatments are essential. In this era, R&D departments are focusing on the use of lipophilic drugs using nanocarrier systems, like liposomes and nanoparticles, to expand the drug delivery methods.

However, the oral segment will register rapid growth during 2025-2034. Major benefits of this segment, including it provides higher convenience and flexibility in terms of administration site and timing as compared to IV approaches. Many times, patients prefer preferring oral route because of minimized clinic visits, decreased time consumption, and enhanced quality of life. As well as consistent research activities on the progression of oral formulations with a focus on at-home consumption, for example, tyrosine kinase inhibitors.

In the full coverage chemotherapy market, the breast cancer segment led with a major share in 2024. Various drivers involved in this segment include a rise in breast cancer instances, advancements in novel targeted therapies, and immunotherapies. These developments are transforming this cancer area with escalated survival rates and the immune system, alongside the improvements in diagnostic tools, like genetic testing and molecular diagnostics, which allow earlier and highly precise detection of breast cancer, enabling timely treatment.

On the other hand, the hematologic cancers segment is predicted to expand fastest. Eventually, growth in leukemia, lymphoma, and multiple myeloma cases can be driven by various factors, such as urbanization, changing lifestyles, and other environmental exposures. This supports a broader adoption of innovative immunotherapies, including monoclonal antibodies, small-molecule inhibitors, and CAR-T cell therapy, which offer more accurate and potentially less toxic treatment solutions.

In 2024, the hospital outpatient segment held a major revenue share of the global full coverage chemotherapy market. Due to affordability and convenience, it is favored by patients as compared to inpatient care. Also, they possess various departments for efficient provision of chemotherapy, especially in outpatient settings having well-developed infrastructure, specialized expertise, and the ability to handle side effects. As well as these treatment settings also consist of full insurance coverage for chemotherapy, which resolves a critical financial hurdle for patients.

Moreover, the homecare/self-administration segment will register rapid expansion in the upcoming years. Various benefits of this segment include the preferred comfort, convenience, and cost-effectiveness over hospital options. Also, nowadays, major developments in digital drug delivery devices, like autoinjectors and wearable injectors, are making easy self-administration with enhanced feasibility and user-friendly. Additionally, patients are increasingly taking wider responsibility for maintaining their health, and self-administration of chemotherapy can help them and potentially improve treatment outcomes.

In 2024, the included segment dominated and is estimated to grow rapidly in the market. Primarily, the widespread population is focusing on palliative care and quality of well-being throughout their cancer journey. Whereas Erythropoiesis-stimulating agents (ESAs), like epoetin alfa, are employed in chemotherapy-induced anemia. As well as G-CSF is also used in severe neutropenia, reducing the risk of febrile neutropenia and infections. Increasing awareness about these inclusions in cancer treatment among healthcare professionals and patients is fueling the ultimate segment and market growth.

The public insurance segment held the biggest share of the global full coverage chemotherapy market. Mainly, the specific health insurance policy like Medicare/Medicaid, NHS, etc., that gives coverage for the expenses of cancer treatment and Diagnosis. A cancer insurance policy is a supplemental health insurance that supports managing the risks associated with cancer and its various manifestations. The rising expenditure on chemotherapy drugs and services is impacting the adoption of public insurance due to affordability among huge patients.

By payer coverage type, the private insurance segment will expand fastest. These kinds of insurance provide numerous benefits, like coverage of multiple cancer stages, hospitalization, and a premium waiver. Along with this, they offer broader and affordable coverage for malignant tumors, and a major contribution of lump sum payout, which allows the payment upon cancer diagnosis with support in treatment spending. Currently, patients are stepping into the adoption of inexpensive options, with the wide range of advantages of insurance driving the segment growth.

In 2024, the oncology hospitals segment was dominant in the full coverage chemotherapy market. Due to comprehensive cancer care services, such as diagnosis, surgery, radiation therapy, and chemotherapy, are provided in oncology hospitals is fueling the segment expansion. Also, they comprise Oncolife Cancer Center, which is a specialized cancer center, with other supportive things, like nutritional guidance, psychological support, and home care options.

And, the homecare providers segment is anticipated to expand at the fastest CAGR. Technological advances, particularly ambulatory infusion devices, digital health platforms, and remote patient monitoring systems, offer safe and effective treatment delivery outside of traditional clinical settings. Furthermore, the movement towards maintenance-based chemotherapy regimens, often administered orally or through longer infusion periods, makes home-based care more feasible and convenient. As well as boosting specialized home infusion providers and mobile oncology nursing teams, this further allows the scalability of home chemotherapy services.

")

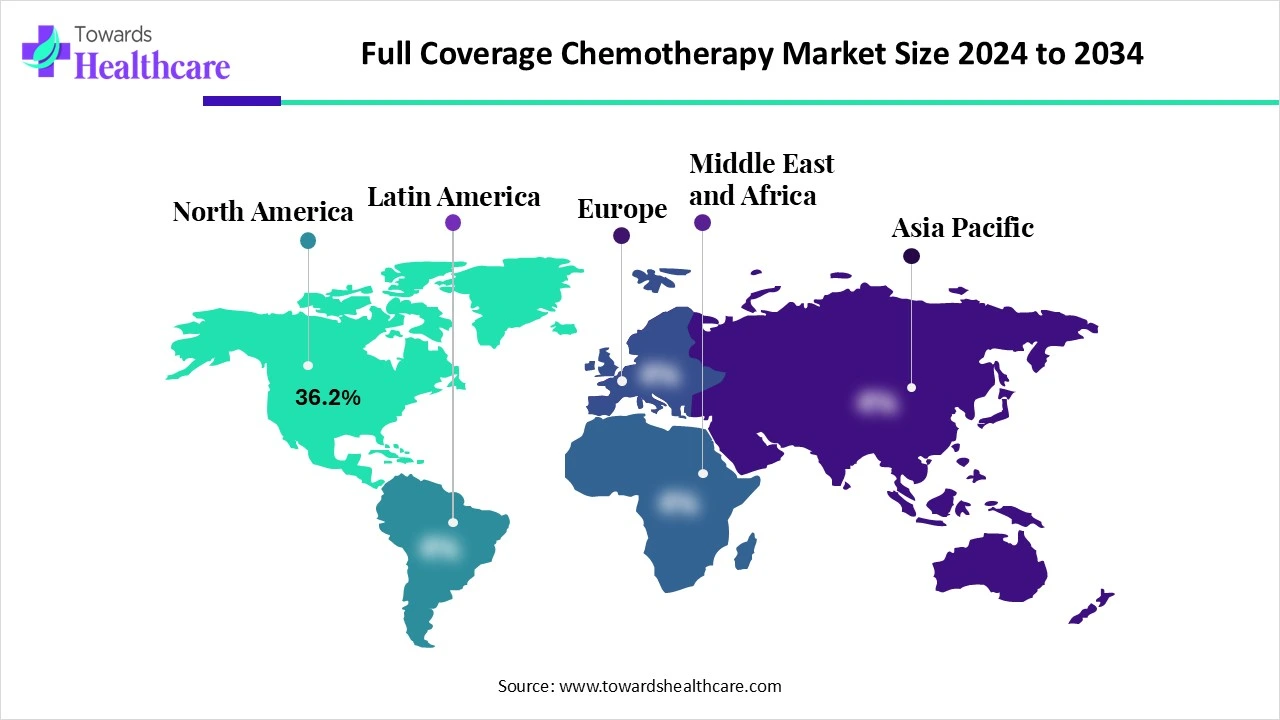

In the global full coverage chemotherapy market share by 36.2% in North America registered dominance in 2024. A significant driver involved in this region’s market expansion is a rise in healthcare expenditure, which allows enhanced access to chemotherapy. Along with this, the accelerating population of this region is focusing on the adoption of personalized cancer care with a broader demand for targeted therapies and compounded therapies. Also, the growing preference for specialized pharmacies consists of the preparation of tailored drug formulations to address specific patient needs and offer cost savings.

The market is fueled by a stringent regulatory landscape, especially in USP <800> (which focuses on safe handling of hazardous drugs), which is raising the demand for specialized compounding services. In addition, the presence of leading market players contributed to the development and production of chemotherapy drugs, which expands market development.

For instance,

Canada’s ongoing innovations in drug delivery systems, like oral chemotherapy and advancements in infusion pumps, are making treatment more feasible and accessible for patients. Besides this, the escalating number of hospitals and specialized cancer centers with chemotherapy capabilities in Canada is contributing to the market’s overall growth.

For this market,

During the forecast period, the Asia Pacific will expand at a rapid CAGR, due to ongoing R&D activities in chemotherapy drugs, like targeted therapies and immunotherapies. As well as significant advancements in supportive care products, including anti-emetics, are assisting in managing chemotherapy side effects and improving patient compliance. Apart from this, government initiatives encouraging cancer awareness, early detection, and treatment are further propelling the market expansion.

China is a major hub for R&D for novel drugs and therapies involved in the oncology area, including a raised emphasis on the expansion of customized treatments, with the adoption of combination approaches. Moreover, a major healthcare spending is required to establish advanced healthcare infrastructure, including hospitals and specialized cancer centers.

For instance,

India’s widespread geriatric population is highly prone to various cancers is mainly influencing the demand for efficient chemotherapy drugs and services. Also, the Indian government is actively promoting numerous cancer-oriented programs and insurance facilities to expand the adoption of early detection and advanced treatment solutions.

For instance,

Primarily, Europe is experiencing a notable growth in the respective market. Europe is increasingly fostering the development of novel targeted therapies and immunotherapies for convenient and effective cancer treatment. As well as rising focus on the establishment of at-home care measures, having enhanced patient convenience and affordability, is impacting the expansion of chemotherapy at-home services in Europe.

For instance,

Germany’s robust healthcare systems and wider digitalization in the healthcare area, including the chemotherapy domain. This has increased the adoption of autoinjectors, and other digital diagnostic tools are driving the market growth.

For this market,

Across the UK, various collaborations, partnerships are going on to study cancer research and develop novel therapies for the global burden of cancer cases. These collaborations often emerged among research universities and healthcare providers, with other drug manufacturers.

For instance,

In July 2025, Revolution Medicines, a late-stage clinical oncology company, and Iambic Therapeutics, an AI-driven drug discovery company, announced a multi-year technology and research collaboration to expand novel drug candidates using Iambic’s AI models. Mark Goldsmith, MD, PhD, CEO and chairman of Revolution Medicines, noted that this collaboration presents an opportunity to further explore oncology targets known to be limiting to address through traditional drug discovery approaches.

By Drug Type

By Route of Administration

By Cancer Type

By Treatment Setting

By Supportive Care Inclusion

By Payer Coverage Type

By End-User

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar