Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

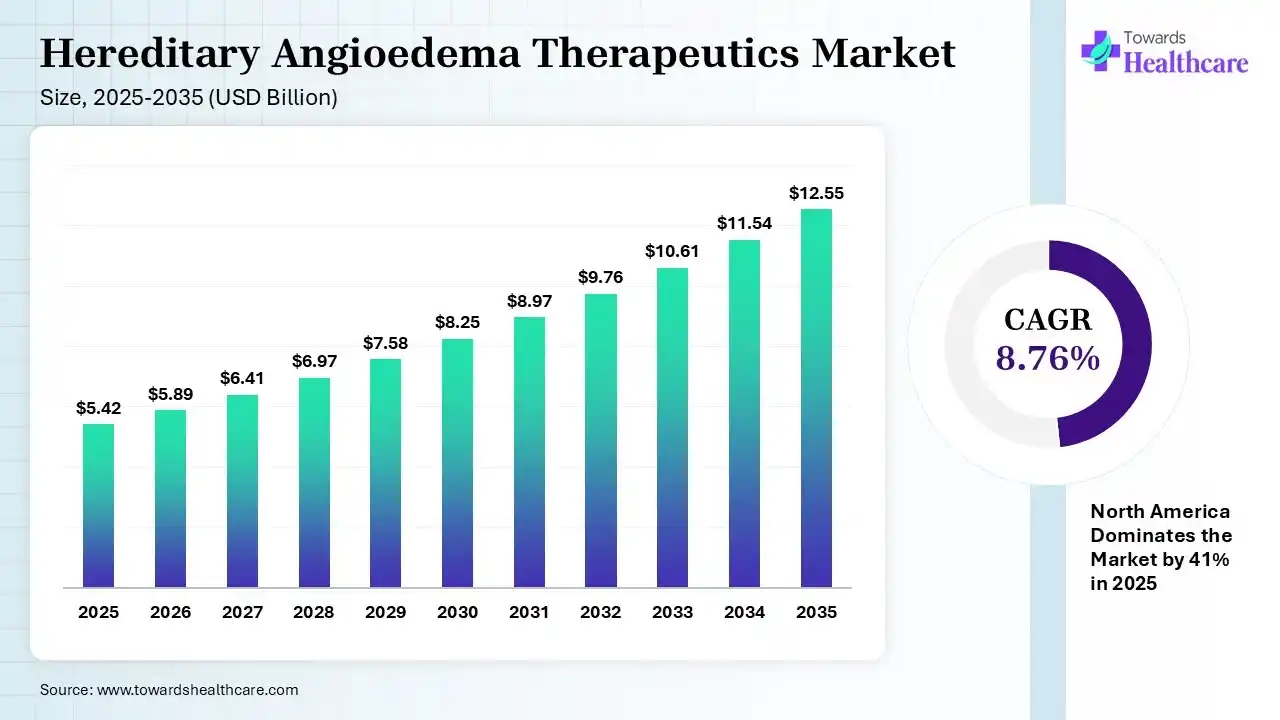

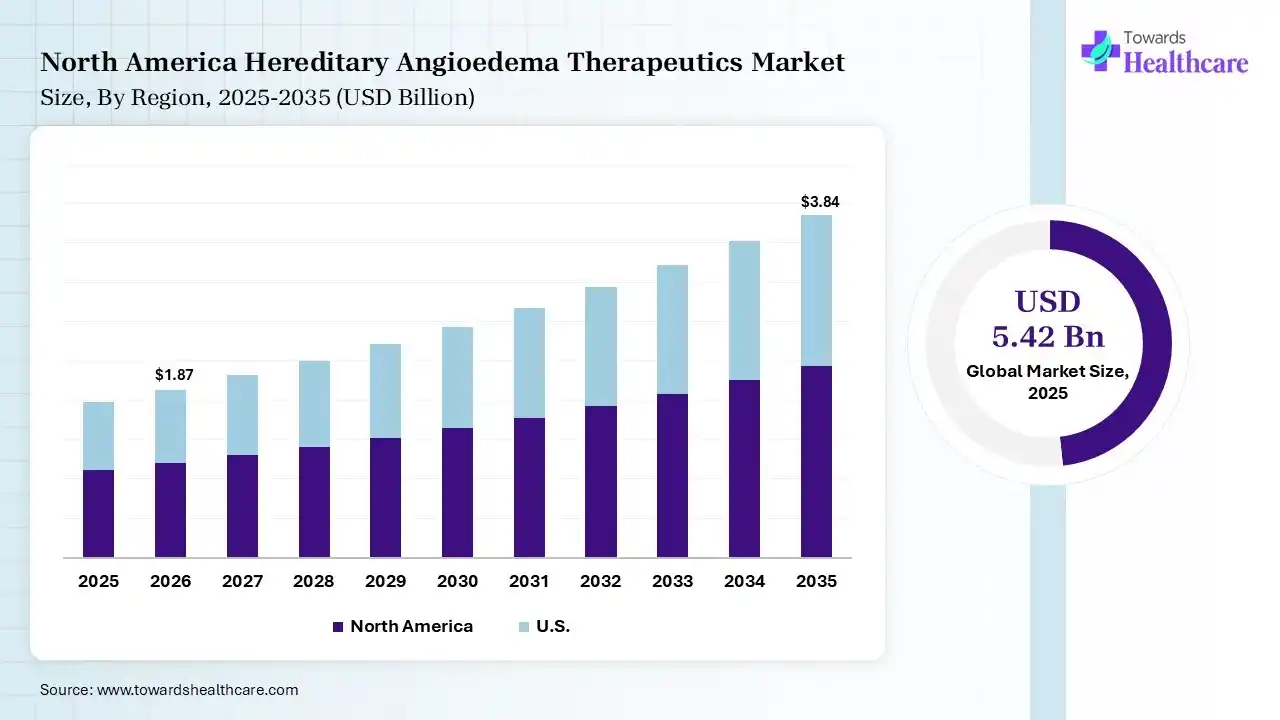

The global hereditary angioedema therapeutics market size was estimated at USD 5.42 billion in 2025 and is predicted to increase from USD 5.89 billion in 2026 to approximately USD 12.55 billion by 2035, expanding at a CAGR of 8.76% from 2026 to 2035. Growing health awareness and early hereditary angioedema (HAE) diagnosis are increasing the demand for hereditary angioedema therapeutics. The growth in R&D activities, collaborations, expanding healthcare, government support, and new product launches is also enhancing the market growth.

")

The hereditary angioedema therapeutics market is driven by a growing shift towards patient-friendly and long-term treatment options. The hereditary angioedema therapeutics encompass medications used for the treatment or prevention of swelling attacks due to a rise in bradykinin levels caused by dysfunction or deficiency of C-1 inhibitors. They are used to treat acute or frequent attacks, prevent airway obstruction, and prevent long-term complications.

AI offers a wide range of applications in the development of hereditary angioedema therapeutics by identifying new targets and accelerating drug discovery and development. It also helps in early disease diagnosis, prevention of attack risks and drug adverse effects, and monitoring disease progression. It also helps in personalized treatment planning and clinical trial optimization, where it offers smart treatment tracking and reminder systems, improving patient adherence to the treatment.

Rising Demand for Advanced Therapies

The growing health awareness and R&D activities are driving the adoption and development of new hereditary angioedema therapeutics. Products such as Kallikrein inhibitor, recombinant and plasma-free C1 inhibitors, and bradykinin pathway blockers are being used for better attack control.

Expanding Pipeline

The companies are developing next-generation therapeutics with oral or subcutaneous administration to enhance patient adherence and outcomes. This is promoting the development of new RNA-based therapies, gene therapies, and monoclonal antibodies.

Technological Advancements

Growing technological advancements are increasing the use of various telehealth platforms and digital tools for patient-centric HAE treatment. This is driving the adoption of attack tracking devices, early prediction systems, and treatment monitoring systems.

| Table | Scope |

| Market Size in 2026 | USD 5.89 Billion |

| Projected Market Size in 2035 | USD 12.55 Billion |

| CAGR (2026 - 2035) | 8.76% |

| Leading Region | North America by 41% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Route of Administration, By Treatment Type, By Distribution Channel, By End User, By Region |

| Top Key Players | Takeda Pharmaceuticals, BioCryst Pharmaceuticals, CSL Behring, KalVista Pharmaceuticals, Pharming Group, Intellia Therapeutics, Astria Therapeutics, Ionis Pharmaceuticals, Pharvaris, Sanofi |

")

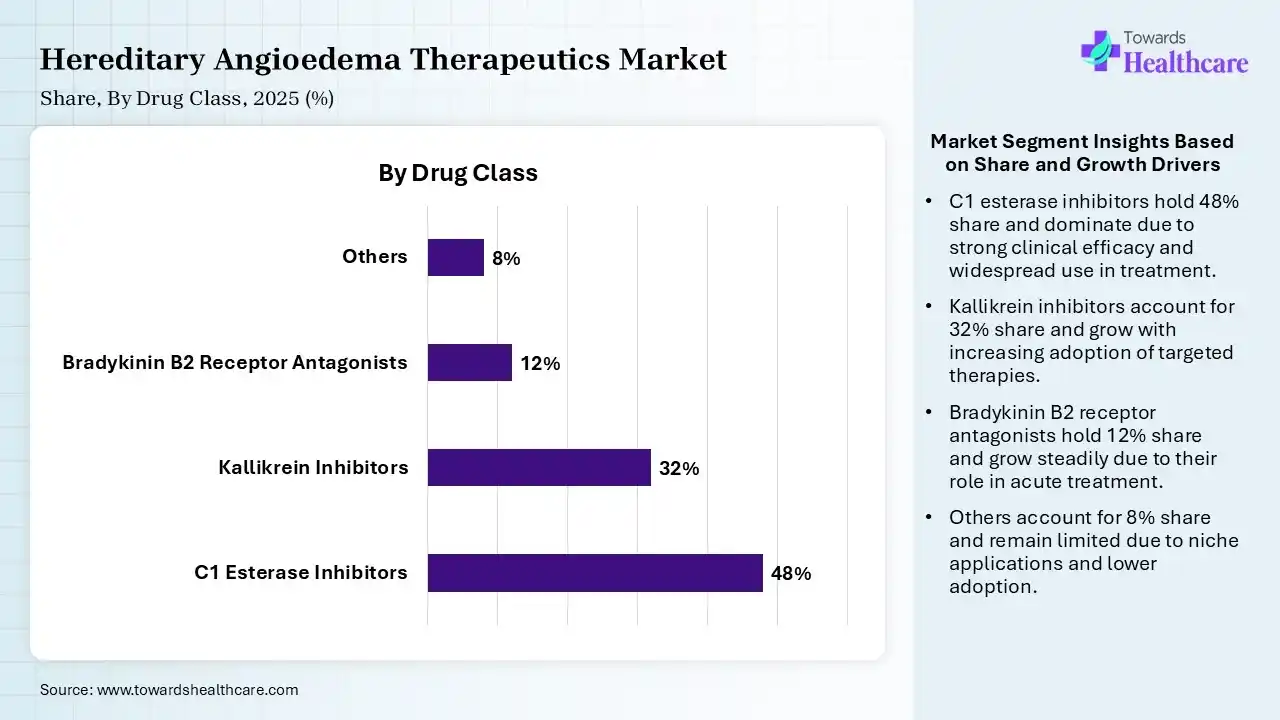

| Segment | Share 2025 (%) |

| C1 Esterase Inhibitors | 48% |

| Kallikrein Inhibitors | 32% |

| Bradykinin B2 Receptor Antagonists | 12% |

| Others | 8% |

The C1 Esterase Inhibitors Segment Dominated the Market With 48% in 2025

The C1 esterase inhibitors segment led the hereditary angioedema therapeutics market with 48% share in 2025, due to established clinical efficacy, which increased the physician preference. The presence of plasma-derived therapies also remained widely adopted globally. Strong reimbursement support also sustained demand.

The kallikrein inhibitors segment held the second-largest share of 32% of the market in 2025 and is expected to witness the fastest growth with a CAGR of 10.80% during the forecast period, driven by increasing adoption of targeted therapies, which enhances patient outcomes. Advancements in monoclonal antibodies also boost their innovations. Favorable dosing frequency improves patient compliance.

The bradykinin B2 receptor antagonists segment held 12% of the hereditary angioedema therapeutics market share in 2025, due to their rapid symptom relief, which supports emergency usage. Their strong presence in acute attack management also drives demand. Increasing diagnosis rates also boost their utilization.

The others segment held 8% of the market share in 2025, as legacy therapies sustain their use in low-resource settings. Their cost-effectiveness also increases their adoption rates. Their oral administration and widespread availability also increase their use.

")

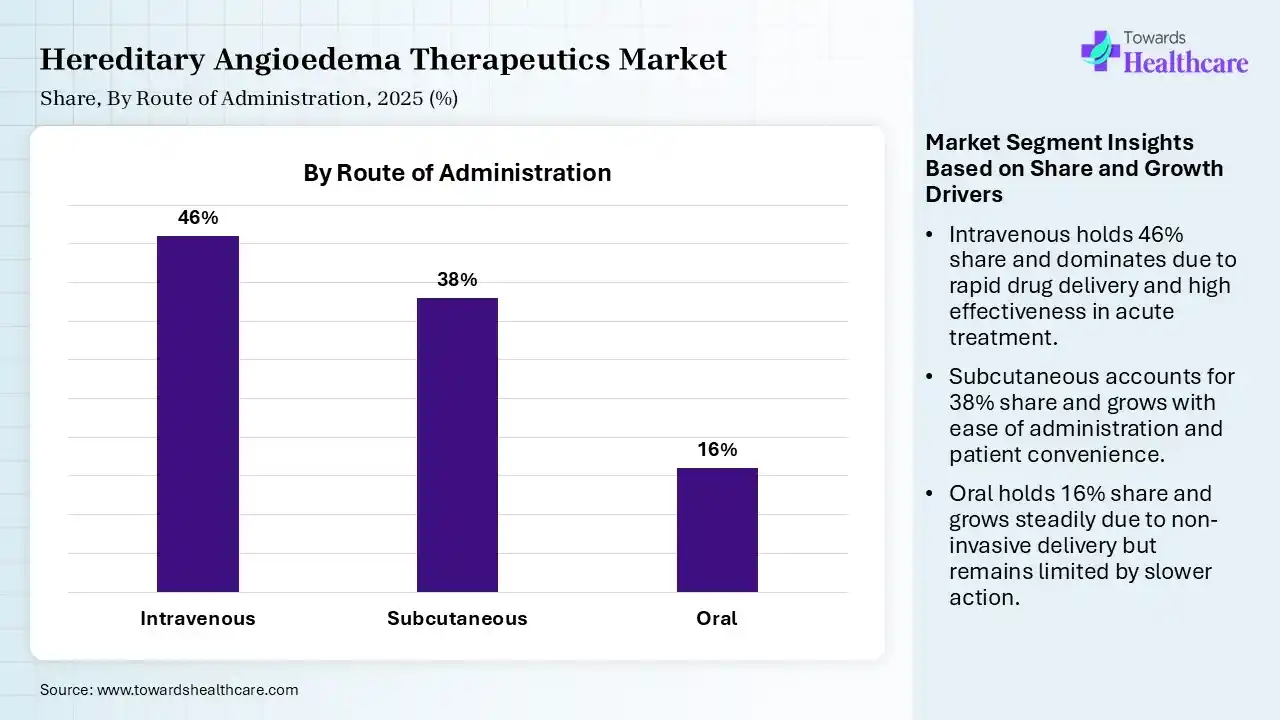

| Segment | Share 2025 (%) |

| Intravenous | 46% |

| Subcutaneous | 38% |

| Oral | 16% |

The Intravenous Segment Dominated the Market With 46% in 2025

The intravenous segment accounted for the highest revenue share of 46% of the hereditary angioedema therapeutics market in 2025, due to long-standing clinical use, which ensured their strong adoption. Their high efficacy in acute care settings also supported their increased demand. Widespread availability across hospitals globally has also increased their use.

The subcutaneous segment held the second-largest share of 38% of the market in 2025, due to its patient-friendly administration. They also help in reducing hospital visits and enhancing patient convenience. Their growing use in prophylactic therapies is also accelerating their growth.

The oral segment held 16% of the hereditary angioedema therapeutics market share in 2025 and is expected to show the highest growth with a CAGR of 11.20% during the forecast period, due to rising pipeline innovations that are expanding oral options. They also help in improving patient adherence, driving their preference. Ease of administration also supports rapid uptake.

")

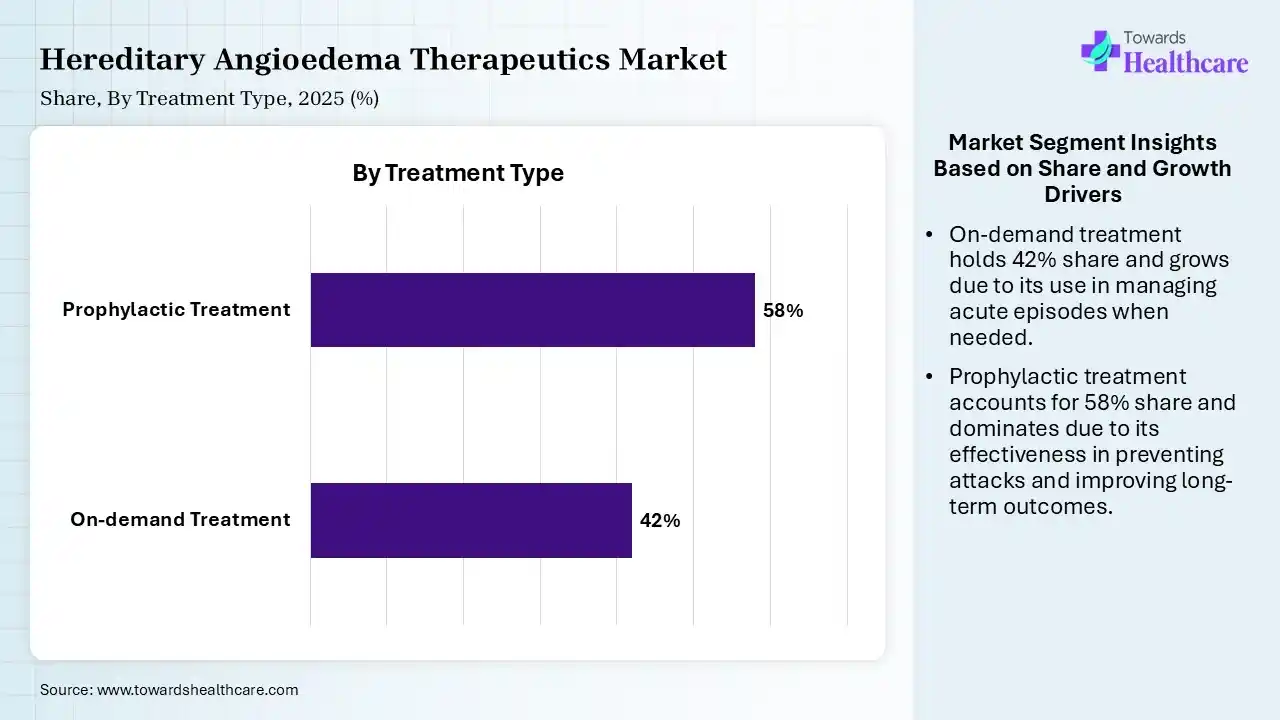

| Segment | Share 2025 (%) |

| On-demand Treatment | 42% |

| Prophylactic Treatment | 58% |

The Prophylactic Treatment Segment Dominated the Market With 58% in 2025

The prophylactic treatment segment held a major revenue share of 58% of the hereditary angioedema therapeutics market in 2025 and is expected to expand rapidly with a CAGR of 9.90% during the forecast period, due to increased focus on prevention, which reduces attack frequency. They also promoted the use of long-term therapies, which improved the quality of life. Strong pipeline expansion also accelerated their growth.

The on-demand treatment segment held the second-largest share of 42% of the market in 2025, as they are essential for acute attack management. They are widely used in emergency scenarios. At the same time, strong clinical necessity also maintains its stable demand.

")

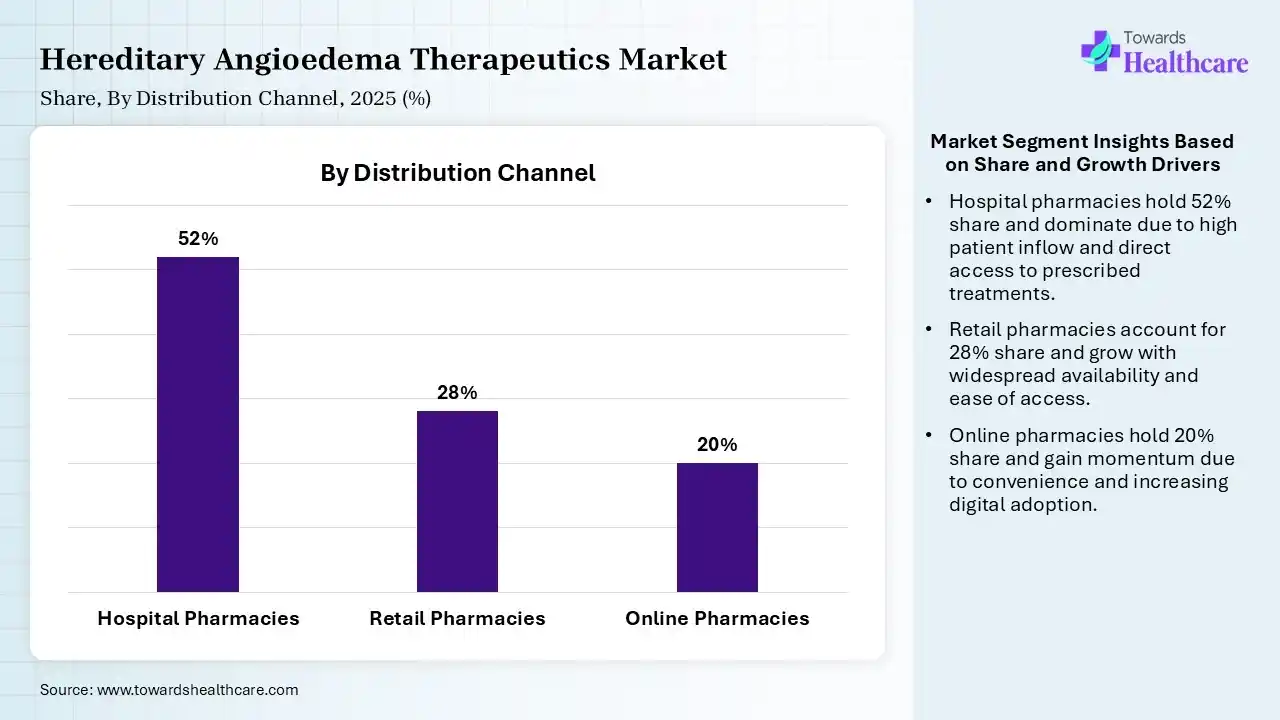

| Segment | Share 2025 (%) |

| Hospital Pharmacies | 52% |

| Retail Pharmacies | 28% |

| Online Pharmacies | 20% |

The Hospital Pharmacies Segment Dominated the Market With 52% in 2025

The hospital pharmacies segment contributed the biggest revenue share of 52% of the hereditary angioedema therapeutics market in 2025, due to centralized treatment protocols, which increased hospital dispensing. The effective management of high-cost biologics also increased their preference. Strong reimbursement frameworks also supported their growth.

The retail pharmacies segment held the second-largest share of 28% of the market in 2025, due to expanding access to chronic therapies, which boosts retail sales. Increasing outpatient treatments also supports their demand. Improved awareness enhances availability, which increases the dependence on retail pharmacies.

The online pharmacies segment held 20% of the hereditary angioedema therapeutics market share in 2025 and is expected to gain the highest share with a CAGR of 10.50% during the forecast period, due to digital healthcare expansion, which is increasing the HAE therapeutics accessibility. Their home deliveries are also supporting chronic disease management. Growing patient preference for convenience also drives adoption.

")

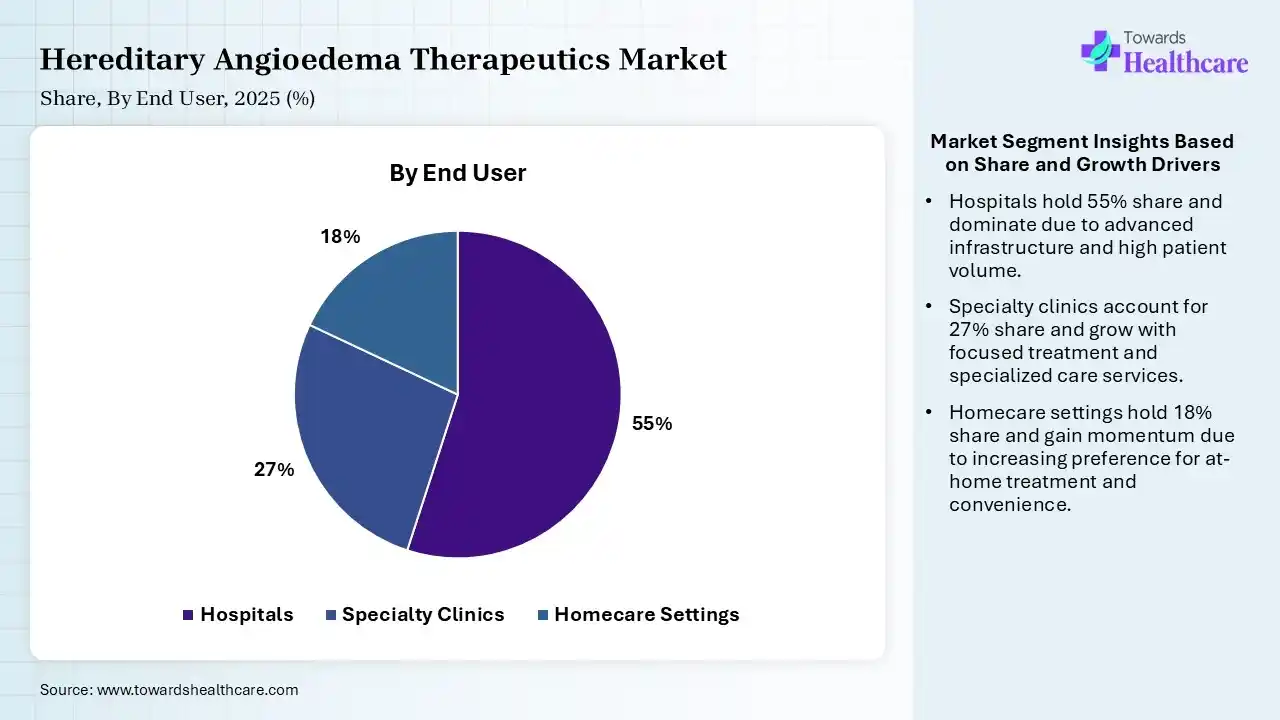

| Segment | Share 2025 (%) |

| Hospitals | 55% |

| Specialty Clinics | 27% |

| Homecare Settings | 18% |

The Hospitals Segment Dominated the Market With 55% in 2025

The hospitals segment held the largest revenue share of 55% of the hereditary angioedema therapeutics market in 2025, as they were considered the primary centers for diagnosis and acute treatment of HAE. They offered access to advanced biologics, which increased their usage. Strong infrastructure also contributed to their dominance.

The specialty clinics segment held the second-largest share of 27% of the market in 2025, due to increasing specialization, which improves treatment outcomes. Their focused care enhances patient monitoring, promoting their use. A rising number of clinics is also driving their growth.

The homecare settings segment held 18% of the hereditary angioedema therapeutics market share in 2025 and is expected to grow with the fastest CAGR of 10.90% during the forecast period, due to a shift toward self-administration. They enhance patient convenience, reducing hospital dependency. Increasing advancements in subcutaneous therapies also drive home care expansion.

")

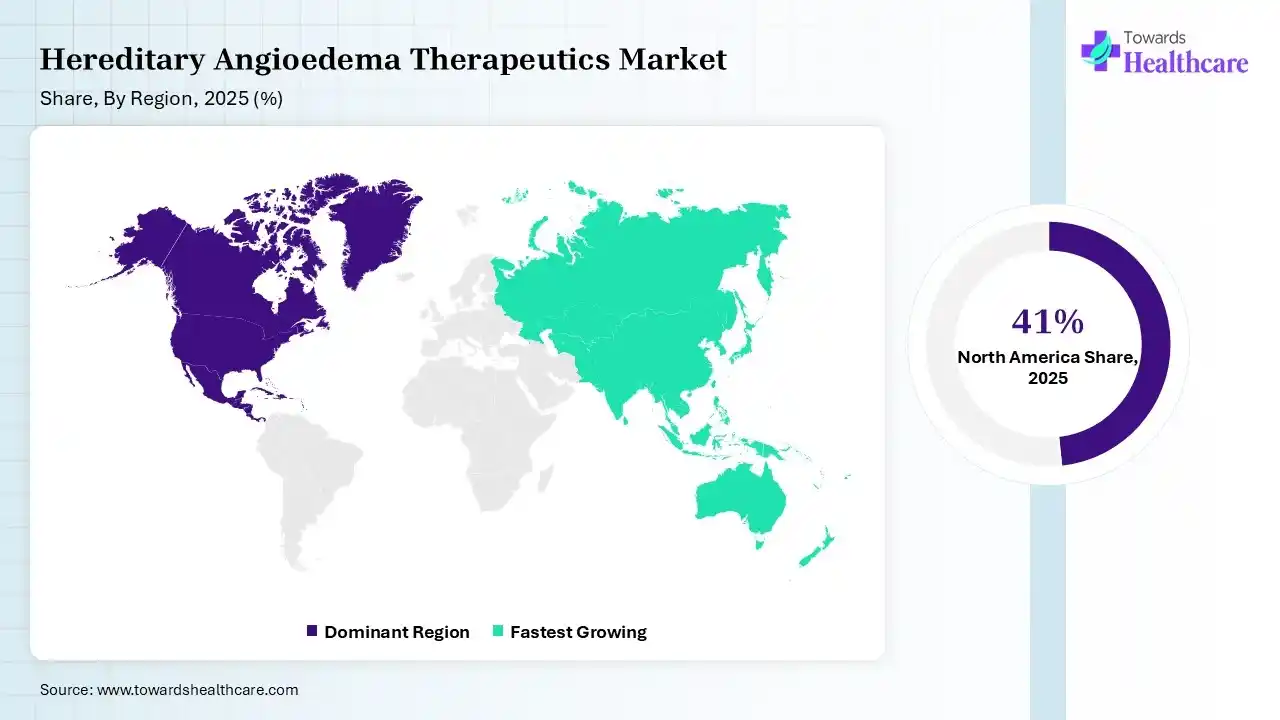

North America dominated the hereditary angioedema therapeutics market with 41% in 2025, due to high diagnosis rates and the presence of advanced healthcare infrastructure. Strong presence of key players also increased the hereditary angioedema therapeutics innovation. Favorable reimbursement policies also enhanced their access, which contributed to the market growth.

U.S. Market Trends

The largest patient pool with high awareness in the U.S. is increasing the demand for hereditary angioedema therapeutics. Strong pipeline and FDA approvals are also supporting their innovations. Premium pricing is also supporting their revenue growth, where the companies are also contributing to their increased innovations.

Asia Pacific held 18% share of the hereditary angioedema therapeutics market in 2025 and is expected to grow at the fastest CAGR of 10.20% during the forecast period, due to rising awareness of rare diseases, which boosts early hereditary angioedema diagnosis. Expanding healthcare infrastructure is also increasing their access to therapeutics. Increasing investments in biologics are also enhancing the market growth.

China Market Trends

Large patient population in China drives demand for hereditary angioedema therapeutics. Expanding healthcare is improving their access, and growing health awareness is also promoting their rapid growth. Growing government initiatives and increasing rare disease R&D activities are also increasing their innovations.

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

| Companies | Headquarters | Hereditary Angioedema Therapeutics |

| Takeda Pharmaceuticals | Tokyo, Japan | Takhzyro, Firazyr, and Cinryze |

| BioCryst Pharmaceuticals | Durham, U.S. | Orladeyo |

| CSL Behring | King of Prussia, U.S. | Haegarda, Andembry, and Berinert |

| KalVista Pharmaceuticals | Cambridge, U.S. | Ekterly |

| Pharming Group | Leiden, Netherlands | Ruconest |

| Intellia Therapeutics | Cambridge, U.S. | Lonvo-z |

| Astria Therapeutics | Boston, U.S. | Navenibart |

| Ionis Pharmaceuticals | Carlsbad, U.S. | Dawnzera |

| Pharvaris | Zug, Switzerland | Deucrictibant |

| Sanofi | Paris, France | General HAE management portfolio |

Strengths

Weaknesses

Opportunities

Threats

By Drug Class

By Route of Administration

By Treatment Type

By Distribution Channel

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar