")

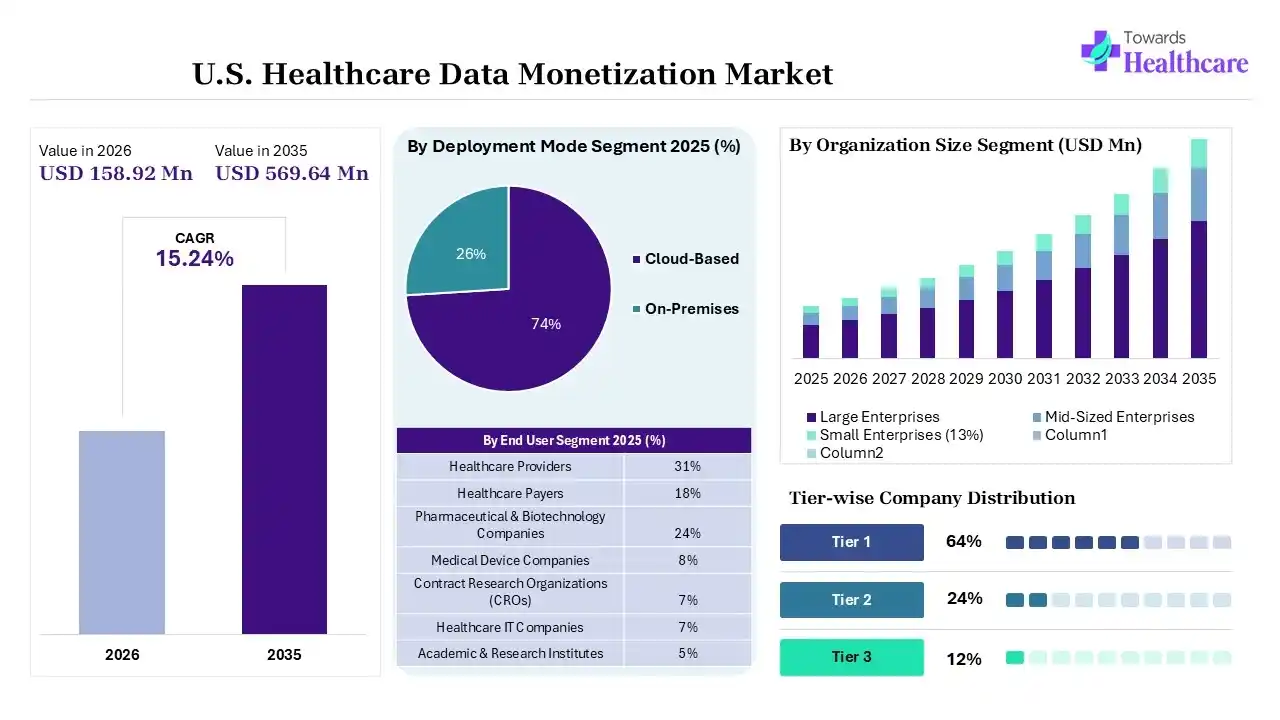

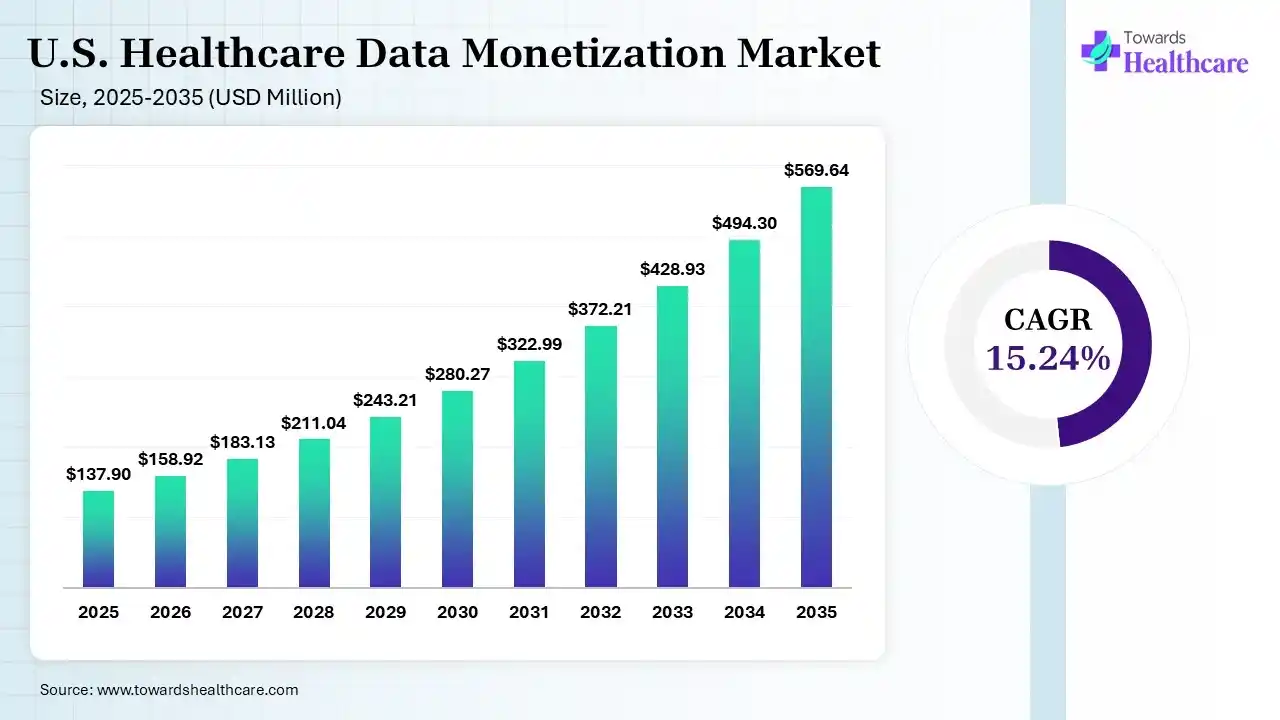

The U.S. healthcare data monetization market size was estimated at USD 137.9 million in 2025 and is predicted to increase from USD 158.92 million in 2026 to approximately USD 569.64 million by 2035, expanding at a CAGR of 15.24% from 2026 to 2035. Surging demand for real-time data analytics, AI-powered approaches, & government initiative programs across the U.S. drives the market expansion. Many technological advances are spurring the development of patient-centric & wearables integration, coupled with clinical research optimization.

")

A process which includes extraction, analysis, & commercialization of the large-volume health datasets developed by Electronic Health Records (EHRs), medical devices, & wearables, is known as healthcare data monetization. Whereas the overall market growth is propelled by a rise in buying de-identified patient information, which assists in regulatory submissions, evaluating long-term safety, designing clinical trials, & discovering novel drug targets. Alongside, payers & providers are highly shifting towards real-time data analytics to acquire treatment outcomes, enhance clinical pathways, & control financial challenges under outcome-based contracts.

Specifically, the use of AI algorithms assists in training on decentralized, localized patient data repositories, omitting transfer or exposure of sensitive Protected Health Information (PHI). This further allows protective alliances among health systems & pharma players for personalized medicine. While several providers are leveraging decentralized blockchain networks & tokenization to securely license anonymized, real-world data (RWD) for drug discovery & clinical trials. Besides this, advances in privacy-enhancing technologies (PETs), including differential privacy & homomorphic encryption, are enabling mathematical guarantees that patient identities remain cryptic, preserving data even while it is being assessed or monetized.

Interoperability & Regulatory Transitions

Mainly, the 21st Century Cures Act demands perfect sharing of patient data & also limits information blocking, which has further spurred an ecosystem of API-first platforms that streamline the extraction & collection of electronic health records (EHRs).

Emphasis on Patient-Centric & Wearable Integrations

In the future, the U.S. will foster ‘Data-as-a-Service’ (DaaS) models where continuous patient-generated data from wearables, connected IoT devices, & telemedicine platforms are unified into longitudinal health profiles.

Promotion of AI & Predictive Analytics

The market will highly focus on the unification of AI & machine learning on enterprise cloud platforms that enable providers & payers to mine detailed financial & operational insights from complex datasets.

| Table | Scope |

| Market Size in 2026 | USD 158.92 Million |

| Projected Market Size in 2035 | USD 569.64 Million |

| CAGR (2026 - 2035) | 15.24% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Data Type, By Monetization Model, By Deployment Mode, By Organization Size, By End User, By Application, By Data Source, By Technology |

| Top Key Players | Datavant, Optum (UnitedHealth Group), IQVIA, Oracle Corporation, Microsoft Corporation, HealthVerity, Flatiron Health, Komodo Health, Merative (formerly IBM Watson Health), Tempus |

")

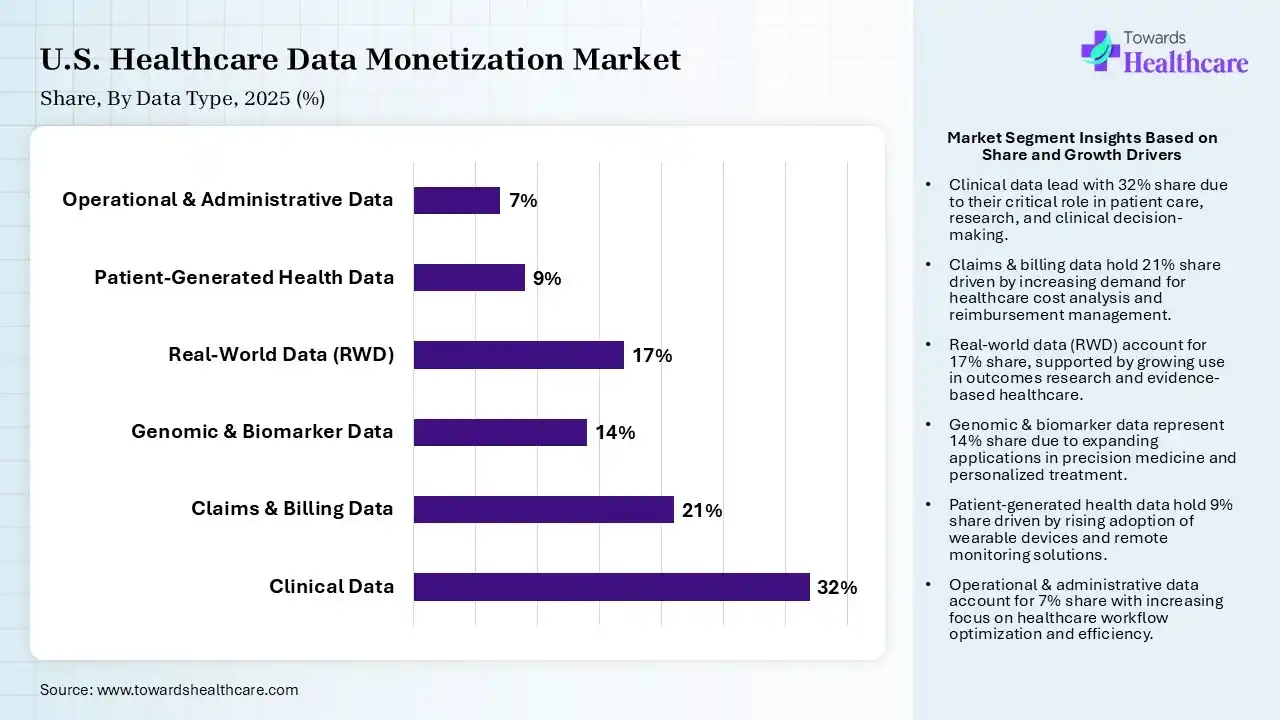

| Segment | Share 2025 (%) |

| Clinical Data | 32% |

| Claims & Billing Data | 21% |

| Genomic & Biomarker Data | 14% |

| Real-World Data (RWD) | 17% |

| Patient-Generated Health Data | 9% |

| Operational & Administrative Data | 7% |

The Clinical Data Segment Led the Market in 2025

In 2025, the clinical data segment held a 32% share of the U.S. healthcare data monetization market. The U.S.'s rising demand for real-world evidence (RWE), especially from many life sciences & biotech firms, is paying for extensive & robust clinical datasets, driving the segmental growth. Also, a rise in steps towards value-based care, clinical data supports in improving clinical directions, lowering hospital readmissions, & verifying affordability.

The claims & billing data segment held the second-largest share of 21% of the market in 2025. Major catalysts cover the intensification of claims analytics adoption by payers to decrease reimbursement leakage & fraud exposure. In addition, providers monetize reimbursement trend data through analytics partnerships.

However, the real-world data (RWD) segment captured a 17% share in 2025, due to regulatory agencies highly supporting real-world evidence for therapy approvals. Whereas drug manufacturers are looking for longitudinal outcome datasets to reinforce commercialisation strategies, this impacts the data type expansion.

The genomic & biomarker data segment held a 14% share in 2025 & is predicted to expand rapidly in the U.S. healthcare data monetization market. Ongoing precision medicine programs are speeding up genomic sequencing investments nationwide. Besides this, numerous biopharma leaders are purchasing biomarker datasets to optimize targeted drug development.

")

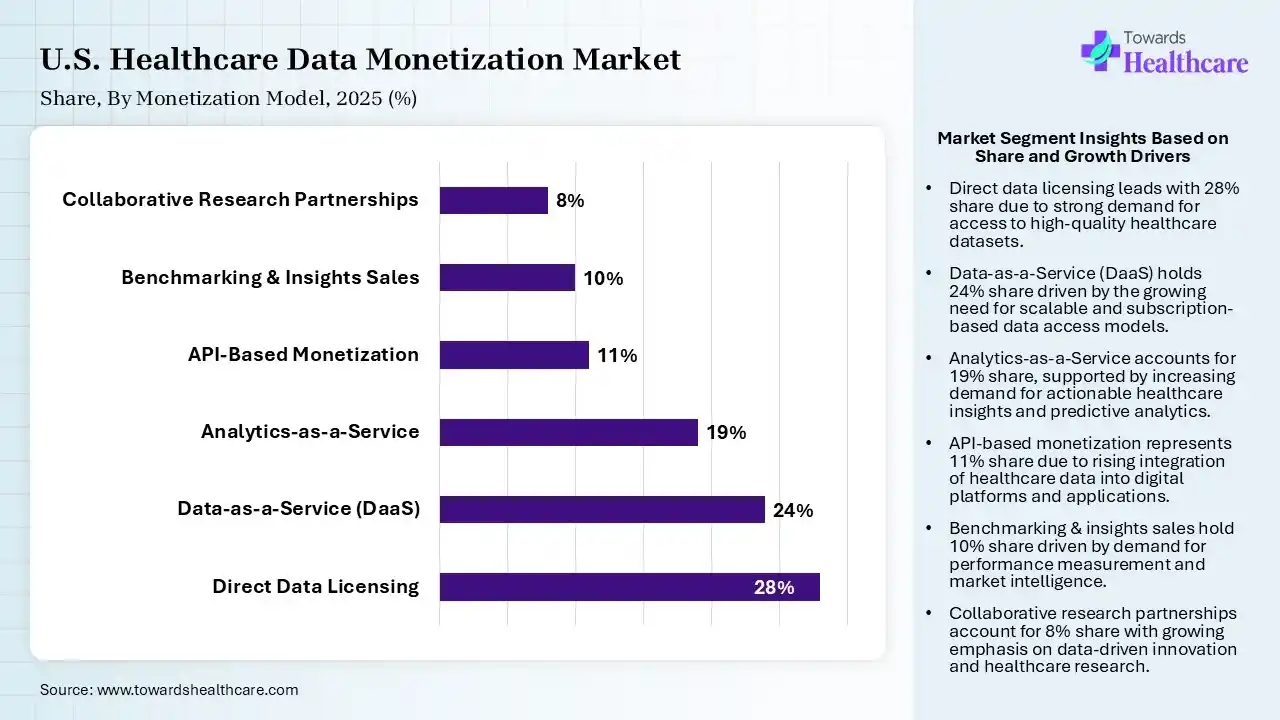

| Segment | Share 2025 (%) |

| Direct Data Licensing | 28% |

| Data-as-a-Service (DaaS) | 24% |

| Analytics-as-a-Service | 19% |

| API-Based Monetization | 11% |

| Benchmarking & Insights Sales | 10% |

| Collaborative Research Partnerships | 8% |

The Direct Data Licensing Segment Dominated the Market in 2025

The direct data licensing segment led with a 28% share of the market in 2025. Dominance is driven by the increasing licensing by life sciences & biotech companies for longitudinal electronic health records (EHRs) & claims data to determine drug targets, develop clinical trials, & match stringent post-market regulatory requirements. Many firms are rolling out broadened, centralized offerings that facilitate businesses & academic institutions with transactional licensing alternatives & internal AI re-use rights.

In 2025, the data-as-a-service (DaaS) segment held 24% of the market. The segmental expansion is fueled by growing cloud-native platforms that allow subscription-based healthcare data access models. Alongside, robust enterprises are seeking scalable & consistently upgraded healthcare datasets, impels these models.

Moreover, the analytics-as-a-service segment captured a 19% share in 2025 & is anticipated to show rapid growth in the U.S. healthcare data monetization market. The emergence of the latest AI-enabled analytics platforms is automating healthcare intelligence generation. Also, many providers are widely outsourcing analytics to specialized vendors, while predictive modeling is spurring across care management & payer operations.

The API-based monetization segment accounted for an 11% share in 2025. Particularly, FHIR-based interoperability standards are empowering API ecosystem development. As well as developers are integrating healthcare datasets into digital health applications rapidly, healthcare IT vendors are commercialising secure API services.

")

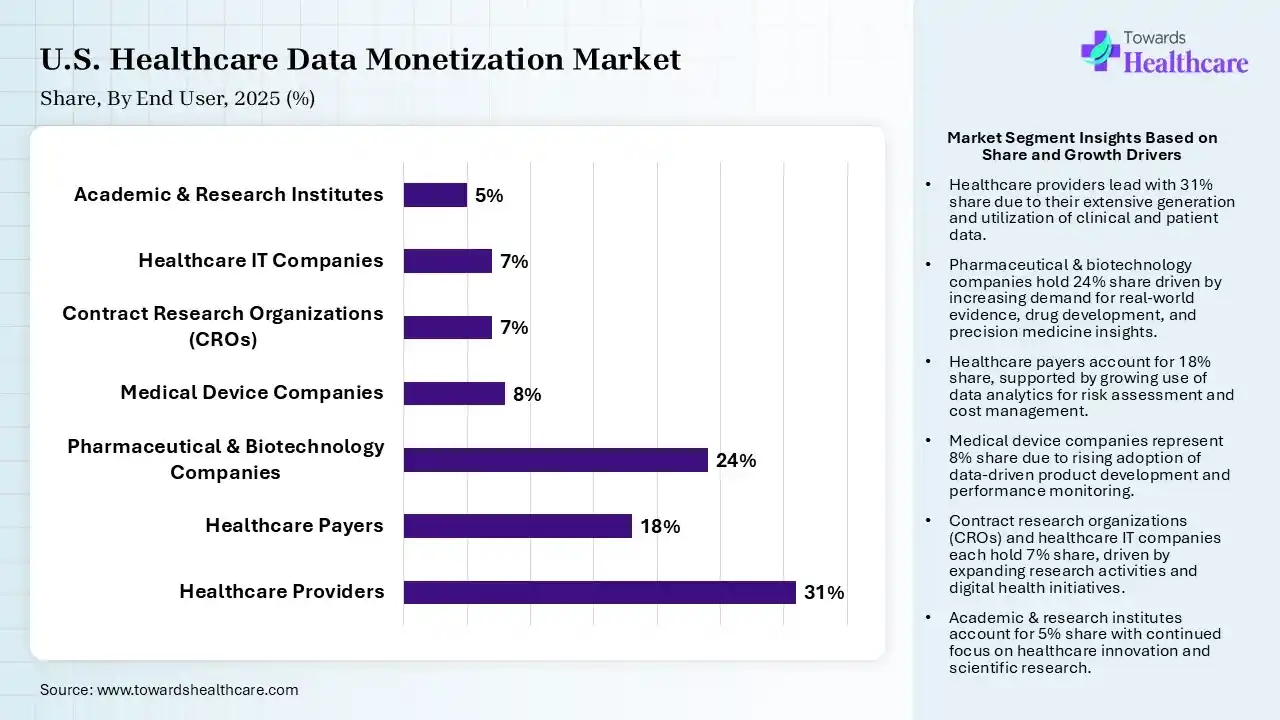

| Segment | Share 2025 (%) |

| Healthcare Providers | 31% |

| Healthcare Payers | 18% |

| Pharmaceutical & Biotechnology Companies | 24% |

| Medical Device Companies | 8% |

| Contract Research Organizations (CROs) | 7% |

| Healthcare IT Companies | 7% |

| Academic & Research Institutes | 5% |

The Healthcare Providers Segment Was Dominant in the Market in 2025

In 2025, the healthcare providers segment registered dominance with a 31% share of the market. They are playing a major role in generating huge volumes of longitudinal patient data, licensing de-identified clinical insights to pharmaceutical & research companies. Alongside, a strong shift towards value-based reimbursement models is supporting providers in tracking & monetizing patient results & population health data.

Although the pharmaceutical & biotechnology companies segment captured a 24% share in 2025, it is estimated to show rapid expansion in the U.S. healthcare data monetization market. Especially, drug developers are highly purchasing real-world evidence & genomic datasets, which impacts the market progression. Growing demand for tailored medicine is pushing demand for longitudinal patient insights, while clinical trials are significantly relying on healthcare data monetization platforms.

The healthcare payers segment held an 18% share in 2025, due to insurers increasingly commercializing claims & reimbursement intelligence datasets. Meanwhile, fraud analytics & risk scoring solutions are continuously gaining traction & also, and value-based reimbursement models are strengthening payer analytics investments.

The medical device companies segment accounted for an 8% share of the market in 2025. Nowadays, diverse connected medical devices are generating scalable real-time patient data streams. Also, several device manufacturers are using analytics to enhance post-market surveillance programs, coupled with the IoMT expansion, which raises monetizable device-generated datasets.

")

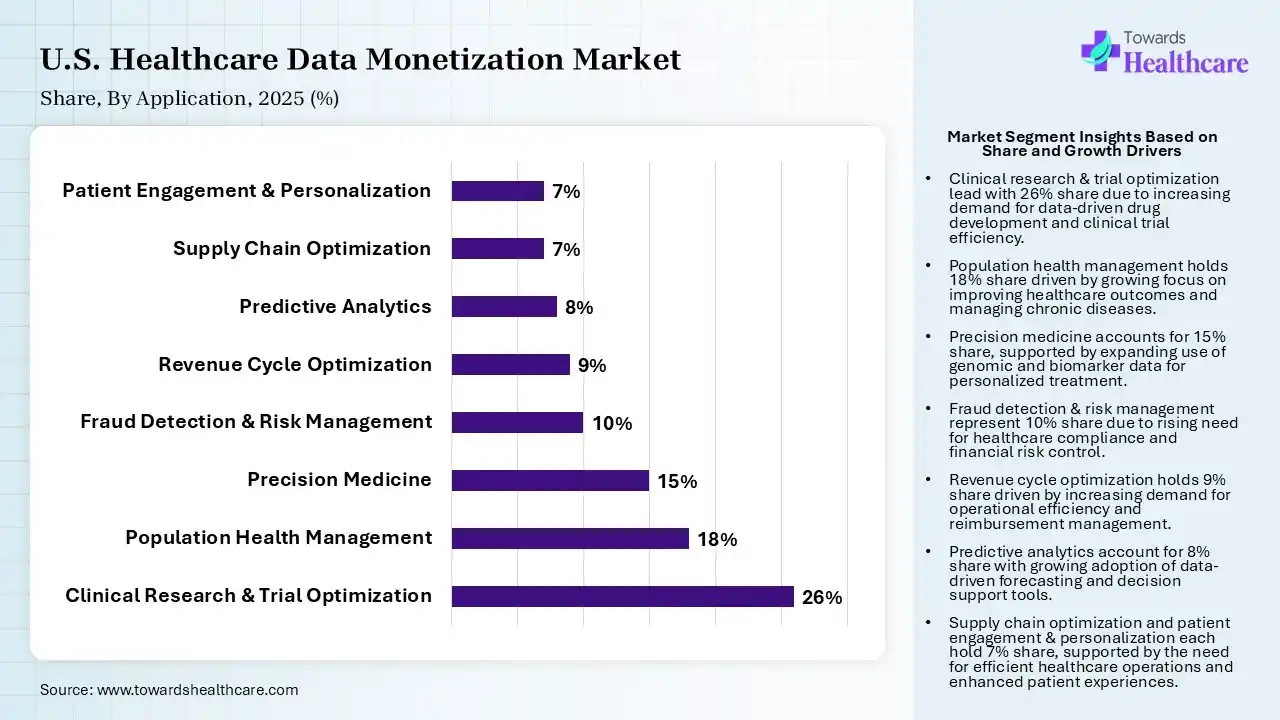

| Segment | Share 2025 (%) |

| Clinical Research & Trial Optimization | 26% |

| Population Health Management | 18% |

| Precision Medicine | 15% |

| Fraud Detection & Risk Management | 10% |

| Revenue Cycle Optimization | 9% |

| Predictive Analytics | 8% |

| Supply Chain Optimization | 7% |

| Patient Engagement & Personalization | 7% |

The Clinical Research & Trial Optimization Segment Led the Market in 2025

The clinical research & trial optimization segment dominated with a 26% share of the U.S. healthcare data monetization market in 2025. In the U.S., pharma firms are experiencing vast financial burdens in launching novel drugs to market, which fuel monetizing anonymized healthcare data to find potential drug targets, evolve more efficient trials, & lower expensive trial failures.

In 2025, the population health management segment captured the second-largest share of 18%. A wider adoption of predictive insights is improving chronic disease management outcomes. Whereas government initiatives are assisting the huge population health analytics deployment.

However, the precision medicine segment held a 15% share in 2025 & is predicted to expand at a rapid CAGR. A notable rise in the adoption of genomic sequencing is bolstering the development of personalised treatment strategies and incentives. Majorly, oncology research activities are heavily dependent on biomarker-driven patient data analysis. Additionally, investments from biopharma players are boosting the commercialization of these medicines.

The fraud detection & risk management segment accounted for a 10% share of the U.S. healthcare data monetization market in 2025. Many payers are employing advanced analytics to lower claims fraud & abuse. Ongoing healthcare cybersecurity initiatives strengthen demand for anomaly detection tools.

")

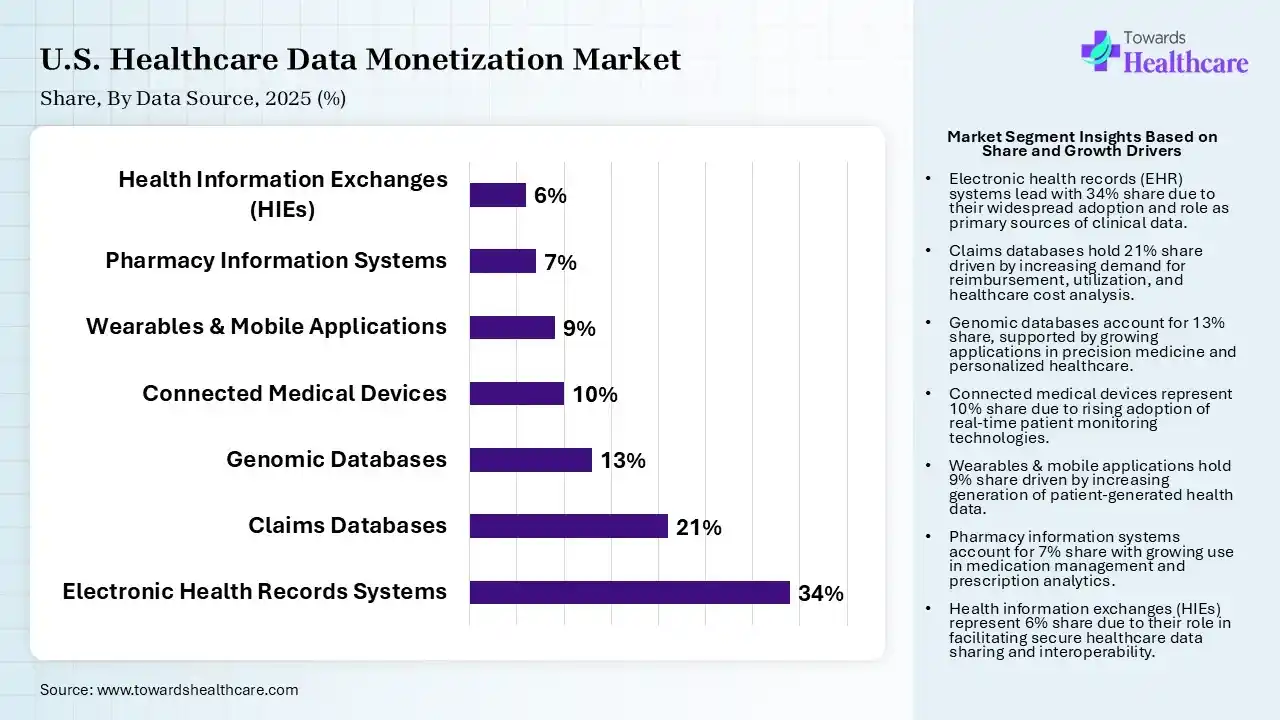

| Segment | Share 2025 (%) |

| Electronic Health Records Systems | 34% |

| Claims Databases | 21% |

| Genomic Databases | 13% |

| Connected Medical Devices | 10% |

| Wearables & Mobile Applications | 9% |

| Pharmacy Information Systems | 7% |

| Health Information Exchanges (HIEs) | 6% |

The Electronic Health Records Systems Segment Dominated the Market in 2025

The electronic health records systems segment held a major share of 34% of the market in 2025. A massive demand for real-world data (RWD) is highly reliant on anonymized EHRs. This further pushes drug discovery, assists in post-market surveillance, & helps in customized medicine development. Continuous breakthroughs in integrated AI & NLP are enabling the automated curation of vast, unstructured clinical datasets, which makes once-fragmented records commercially viable & actionable.

The claims databases segment captured the second-largest share of 21% of the U.S. healthcare data monetization market in 2025. It is driven by expanding claims analytics for reimbursement optimisation initiatives, surging fraud detection programs that are increasingly using longitudinal claims records. Also, many government healthcare programs are developing large-scale administrative datasets.

Furthermore, the genomic databases segment held a 13% share in 2025 & is anticipated to expand rapidly. Key factors are accelerating investments in precision medicine, which foster genomic database commercialization. Besides this, oncology & rare disease research are propelling sequencing data demand. Gradual biotech alliances reinforce biomarker analytics progression.

The connected medical devices segment accounted for a 10% share in 2025. Broadening IoMT deployment is strengthening continuous monitoring capabilities. Additionally, device manufacturers are monetizing real-time physiological data streams. Specifically, the current vast adoption of remote patient monitoring is driving demand for connected device analytics.

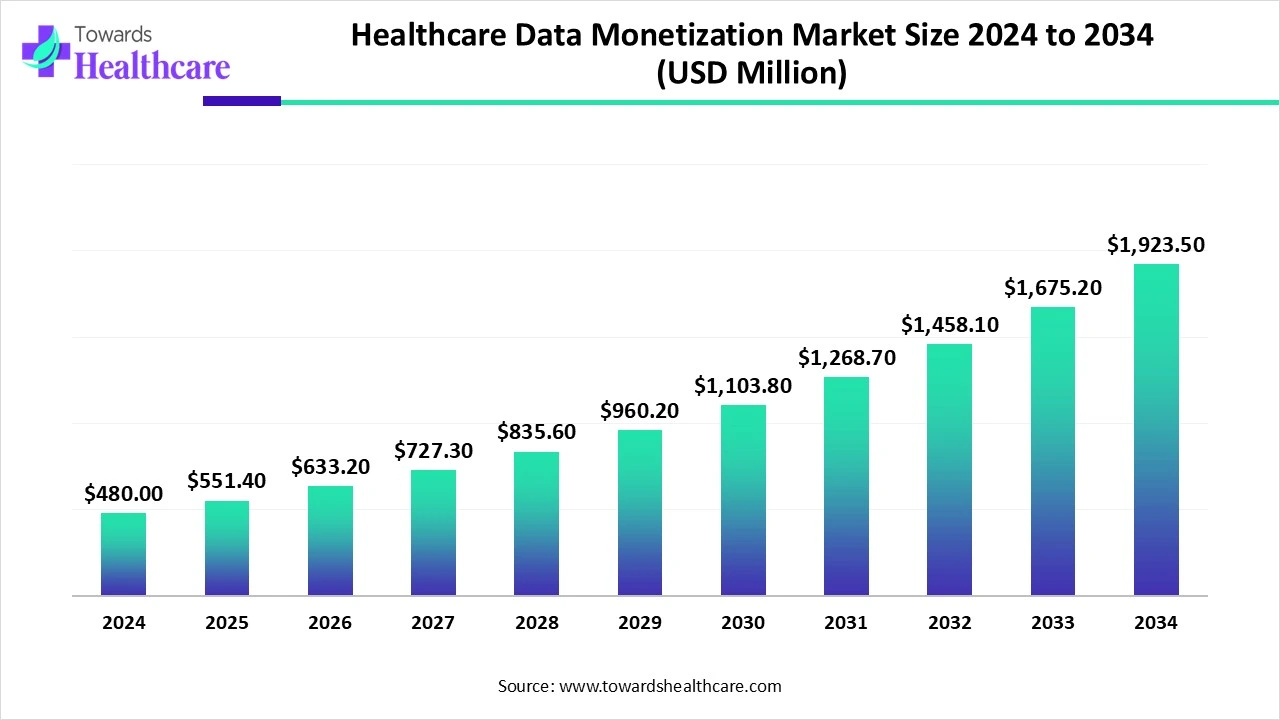

The global healthcare data monetization market size is calculated at USD 480 million in 2024, grew to USD 551.4 million in 2025, and is projected to reach around USD 1923.5 million by 2034. The market is expanding at a CAGR of 14.86% between 2025 and 2034.

")

| Company | Description |

| Datavant | This firm highly facilitates secure, privacy-preserving record linkage (PPRL) & tokenization software. |

| Optum (UnitedHealth Group) | It has explored Optum Labs and Optum Insight through large-scale analytics, real-world evidence (RWE) research, & population health management. |

| IQVIA | A leader specializes in life sciences, MedTech, & payer organizations' scalable insights, AI-powered commercial modeling, & direct data-as-a-service (DaaS) licensing across various core solutions. |

| Oracle Corporation | It offers integrated electronic health records (EHR) with sophisticated AI analytics via Oracle Health & Oracle Cloud Infrastructure (OCI). |

| Microsoft Corporation | Its key offerings cover Microsoft Fabric, Azure Health Data Services, & Microsoft Dragon Copilot. |

| HealthVerity | A firm unveiled its HealthVerity Marketplace, the country’s largest unified ecosystem of clinical, claims, & consumer data. |

| Flatiron Health | They provide services through Data-as-a-Service (DaaS) & analytics offerings, licensing de-identified real-world data (RWD). |

| Komodo Health | Their major products are Marmot, MapLab & MapAI, MapExplorer, Financial Services Datasets, & National Drug Projections. |

| Merative (formerly IBM Watson Health) | This facilitates the monetization of data through modern SaaS analytics, AI, & enterprise data solutions. |

| Tempus | It hugely offers AI-enabled insights, software, & real-world datasets to over 250 biopharma players & hundreds of U.S. hospital networks. |

Strengths

Weaknesses

Opportunities

Threats

By Data Type

By Monetization Model

By Deployment Mode

By Organization Size

By End User

By Application

By Data Source

By Technology

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar