Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

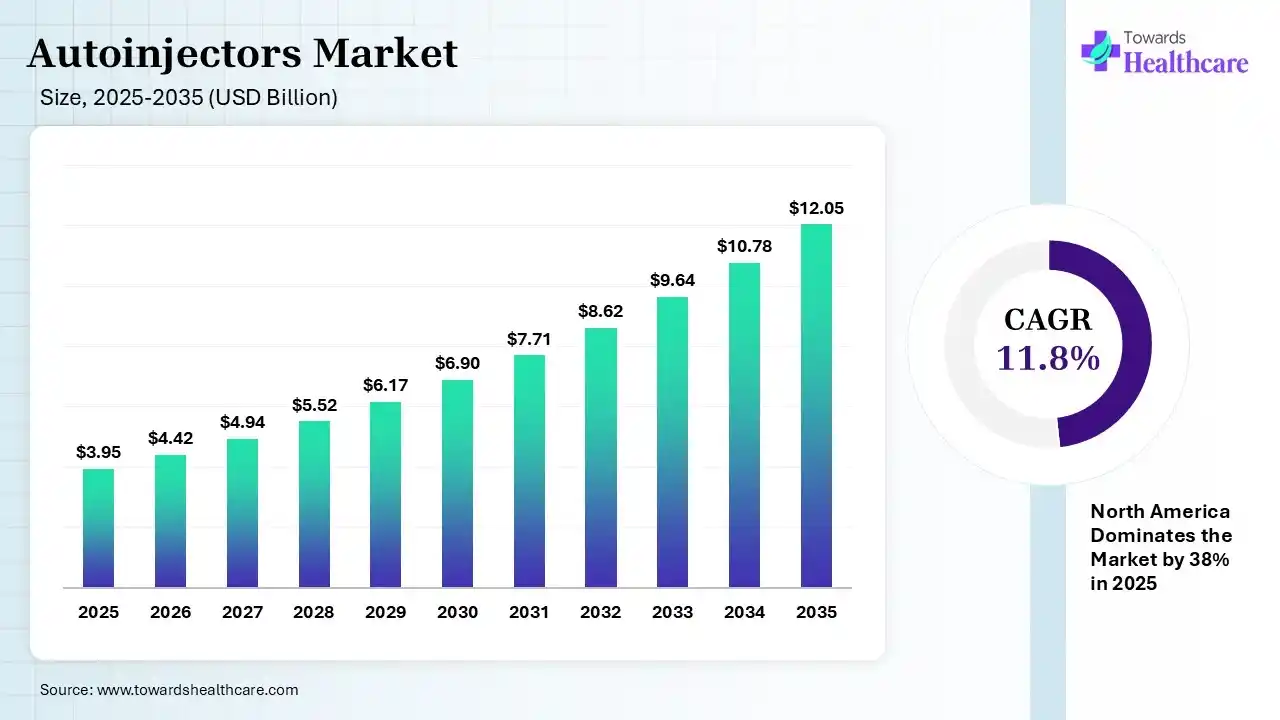

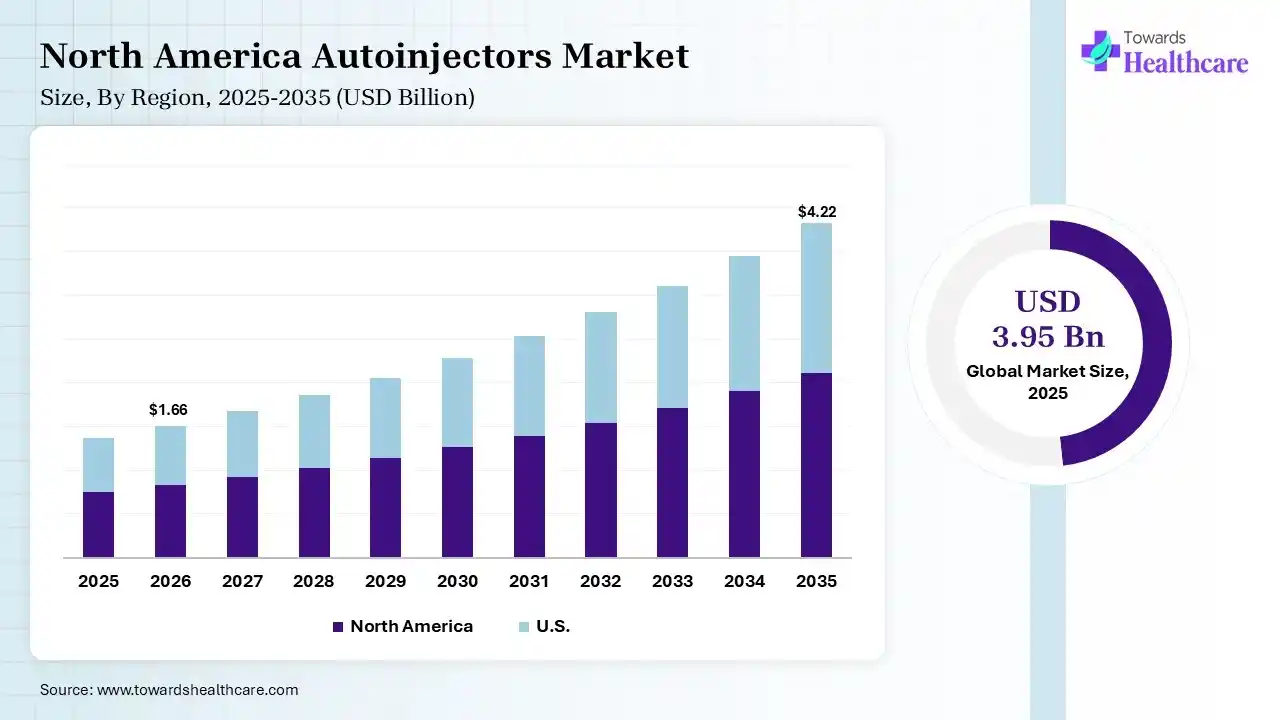

The global autoinjectors market size was estimated at USD 3.95 billion in 2025 and is predicted to increase from USD 4.42 billion in 2026 to approximately USD 12.05 billion by 2035, expanding at a CAGR of 11.8% from 2026 to 2035. The autoinjector market is growing because these tools increase patient compliance and adherence, as the drugs can be self-administered.

")

Autoinjectors are self-injectable tools; they are a significant class of healthcare devices that deliver drugs via subcutaneous or intramuscular injection. They enclose prefilled syringes and cartridges, which are driven by a spring system. This device is simple to self-administer, enhances patient compliance, lowers anxiety, and improves dosage accuracy. An autoinjector is an injection tool that allows the consumer to deliver a predetermined drug dosage via self-injection. An autoinjector is a single-dose product for pre-filled syringes with maximum fill volumes from 1 mL to 5.5 mL. Autoinjectors are often used in the military to protect personnel from chemical warfare agents. Autoinjector devices are significant for the rapid administration of drugs and antidotes, and they are used by those who have not been medically trained.

AI-based technology integration is transforming auto-injector stages, from enhancing patient compliance and experience to navigating challenging government landscapes. AI-based technology in drug discovery quickens target identification and molecule design, lowering R&D timelines. AI-based algorithms adapt to specific patient requirements, potentially adjusting injection protocols. AI-based technology addresses behavioral and emotional factors. Youths who forget auto-injectors or therapeutics can be flagged by usage data. Incorporation of AI-driven technology into autoinjectors holds significant strength for improving their primary functions, specifically addressing challenges identified via PMS, like injuries, malfunctions, device and patient challenges.

| Table | Scope |

| Market Size in 2026 | USD 4.42 Billion |

| Projected Market Size in 2035 | USD 12.05 Billion |

| CAGR (2026 - 2035) | 11.8% |

| Leading Region | North America by 38% |

| Key Applications | Diabetes, Obesity Management (GLP-1s), Anaphylaxis, Rheumatoid Arthritis, Multiple Sclerosis, Migraine, Psoriasis, Autoimmune Diseases |

| Primary End Users | Pharmaceutical Companies, Biotechnology Companies, Hospitals, Specialty Clinics, Homecare Patients |

| Key Challenges | Device-drug compatibility, regulatory complexity, manufacturing scalability, high development costs, competition from alternative drug delivery technologies |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Route of Administration, By Therapy Area, By Technology, By End User, By Distribution Channel, By Region |

| Top Key Players | Eli Lilly and Company, Amgen, Ypsomed, SHL Medical, AbbVie |

")

| Segment | Share 2025 (%) |

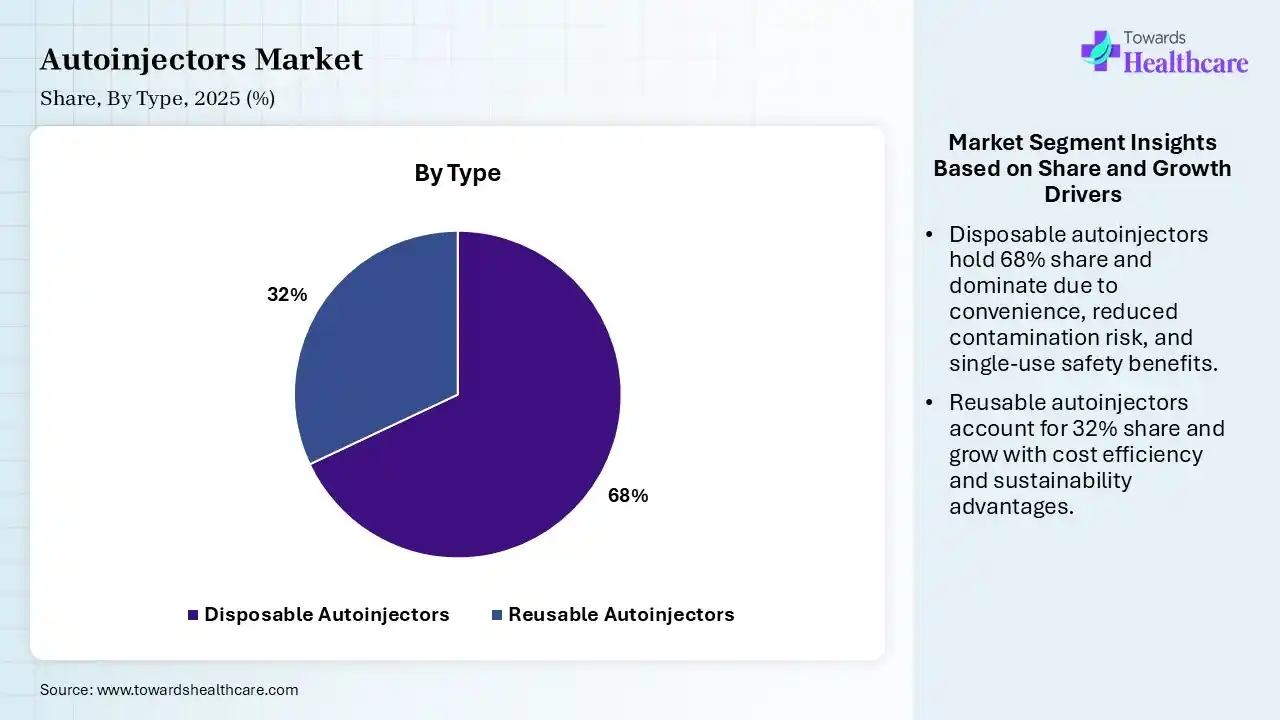

| Disposable Autoinjectors | 68% |

| Reusable Autoinjectors | 32% |

The Disposable Autoinjectors Segment Led the Autoinjectors Market in 2025

The disposable autoinjectors segment contributed the largest market share of 68% in 2025, as disposable autoinjectors are dense, pre-filled products designed to deliver a particular dose of medication rapidly and safely. Most models involve automated needles, which are hidden before and after injection to prevent needle-stick wounds and lower anxiety.

The reusable autoinjectors segment held a significant share of 32% in the market, and is expected to grow at the fastest CAGR during the forecast period, as it offers important advantages, involving enhanced environmental sustainability by lowering plastic waste, lower long-term expenses for patients using chronic medication, and better patient compliance via digital and connected features.

")

| Segment | Share 2025 (%) |

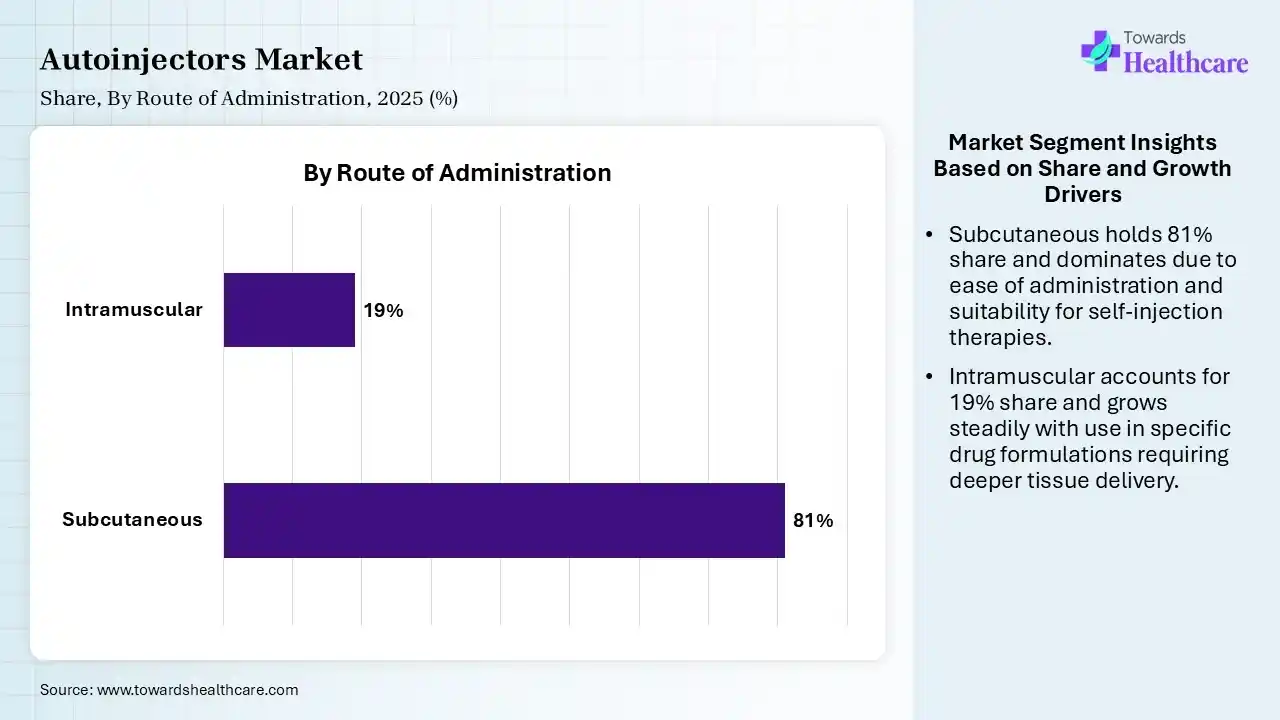

| Subcutaneous | 81% |

| Intramuscular | 19% |

Subcutaneous Segment Led the Autoinjectors Market in 2025

The subcutaneous segment contributed the largest market share of 81%, and is expected to grow at the fastest CAGR during the forecast period. Subcutaneous administration enables therapeutics to be self-administered by individuals or healthcare providers using a variety of drug delivery technologies, involving advanced subcutaneous drug delivery devices. SC administration eases patient self-administration in home or outpatient healthcare environments.

The intramuscular segment held a significant share of 19% of the market, as intramuscular injection (IM) involves injecting medications into the depth of specifically selected muscles. The bulky muscles have good vascularity, and as the injected drug rapidly reaches the systemic flow and thereafter into the particular area of action, bypassing the first-pass metabolism.

")

| Segment | Share 2025 (%) |

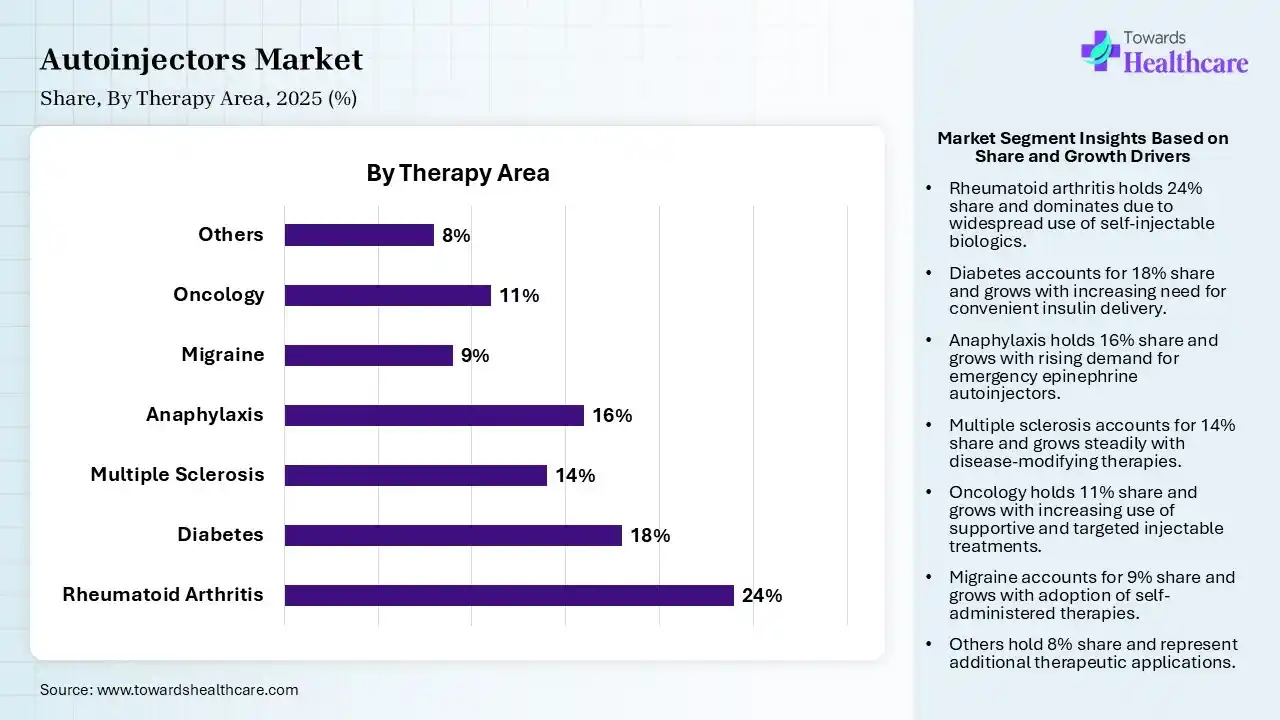

| Rheumatoid Arthritis | 24% |

| Diabetes | 18% |

| Multiple Sclerosis | 14% |

| Anaphylaxis | 16% |

| Migraine | 9% |

| Oncology | 11% |

| Others | 8% |

Rheumatoid Arthritis Diseases Segment Led the Autoinjectors Market in 2025

The rheumatoid arthritis disease segment contributed the largest market share of 24%, as etanercept is efficient in the management of rheumatoid arthritis (RA) and self-administered through an auto-injector. These autoinjectors offer several advantages, including a simplified drug administration process, safer injection, lower challenges of contamination, and reduced maintenance.

The diabetes segment held a significant share of 18% in the market, as autoinjectors lower the complexity and discomfort of injections, allowing patients to administer rugs with reduced effort. Autoinjectors are specifically well-suited for SC injections because of their less invasive nature, consistent delivery rates, and precise depth control.

The multiple sclerosis segment held a significant share of 14% in the autoinjectors market, as autoinjectors are well-established in subsidiary multiple sclerosis (MS) therapy. Autoinjectors lower the complexity and discomfort of injections, allowing patients to administer medications with minimal effort.

The anaphylaxis segment held a significant share of 16% in the market, and is expected to grow at the fastest CAGR during the forecast period. Autoinjectors are related to higher treatment adherence, with research showing that patients using these tools. This autoinjection prevents the progression of anaphylaxis and thereby reduces the need for hospitalization and the challenges of fatality.

The oncology segment held a significant share of 11% in the market, as autoinjectors deliver specific and consistent doses, lowering the human error related to traditional syringe-driven methods. Autoinjectors in oncology evolved as a patient-driven technology that shifts care from hospitals to the home, addressing the increasing requirement for convenient, self-administered subcutaneous injections of biologics.

")

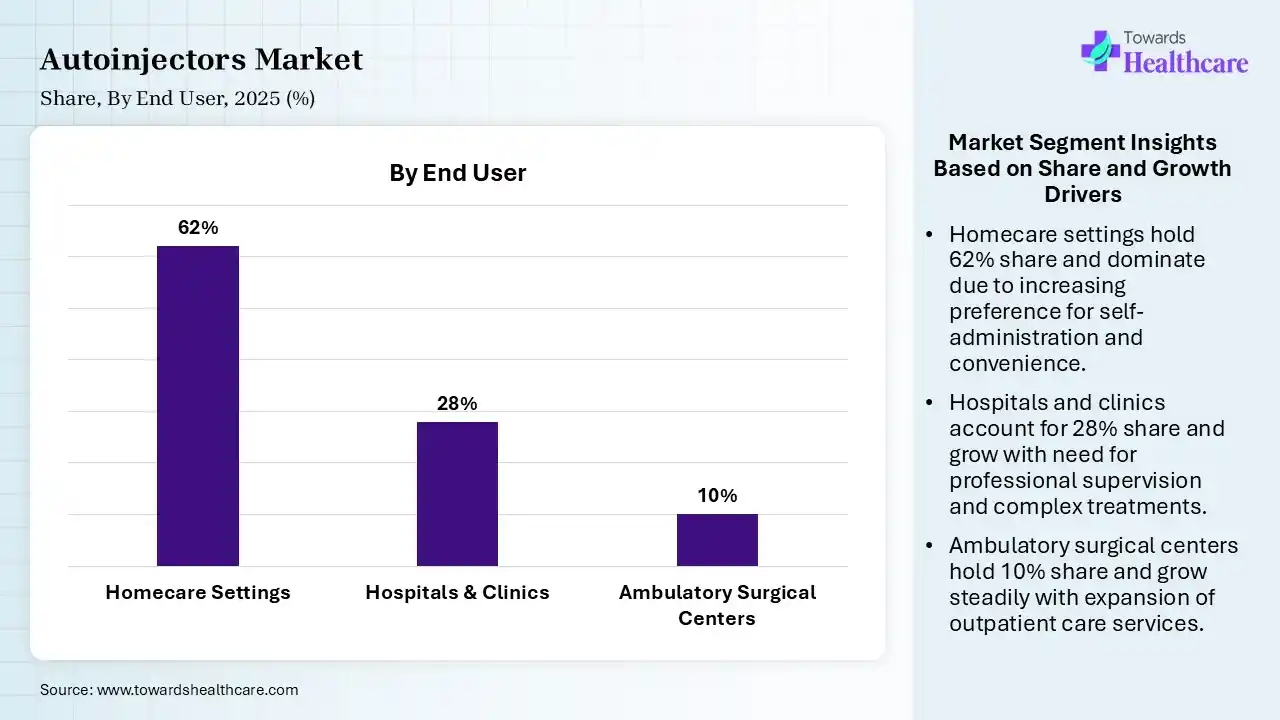

| Segment | Share 2025 (%) |

| Homecare Settings | 62% |

| Hospitals & Clinics | 28% |

| Ambulatory Surgical Centers | 10% |

Homecare Settings Segment Led the Autoinjectors Market in 2025

The homecare settings segment contributed the largest market share of 62%, and is expected to grow at the fastest CAGR during the forecast period, as home care decreases expenses, improves health outcomes, and lowers hospital stays. Home care is focused on preserving the individual's individuality. Home-driven care supports reducing hospital readmissions and enhancing recovery results. By offering services such as medication management and continuing monitoring.

The hospitals & clinics segment held a significant share of 28% in the market, as hospitals and clinics offer significant, accessible healthcare via specialized healthcare staff, advanced technology, and 24/7 emergency care. They offer comprehensive services ranging from preventive check-ups and diagnostic tests to complex surgeries.

The ambulatory surgical centers segment held a significant share of 10% in the market, as ASCs help to cut costs and reduce the out-of-pocket expense for patients. ASCs help to cut costs and reduce the out-of-pocket costs for patients. It is estimated that ASCs can cost 45-60% less than hospital stays. ASCs have better control over the development of surgeries.

")

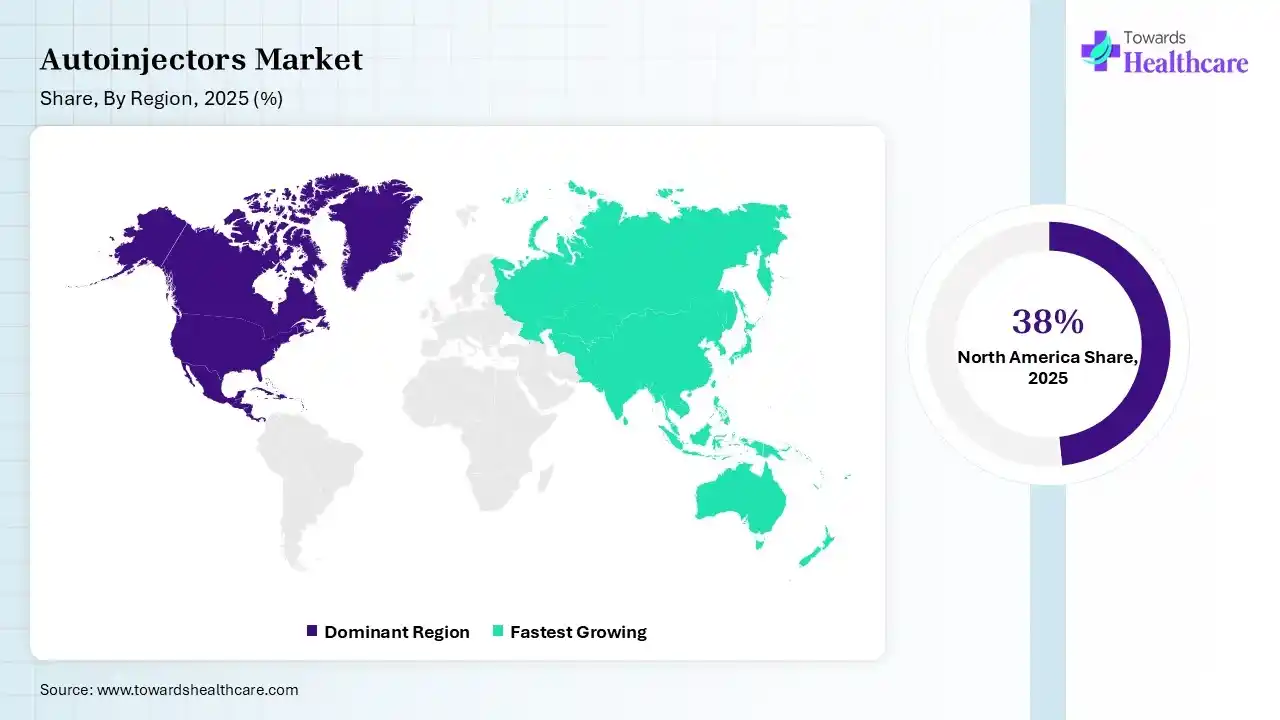

In 2025, North America dominated the autoinjectors market with a share of 38% in 2025, due to increasing chronic conditions like cardiac disease, cancer, stroke, and diabetes, which are expensive and major causes of death and disability in the US. Smart technologies are expected to radically alter care, lowering trips to the hospital and offering greater opportunities to live longer, improved lives at home. The FDA facilitates rapid approvals for novel medical devices, increasing innovation and faster entry for novel, advanced autoinjectors, which contributes to the growth of the market.

For Instance,

U.S. Market Trends

In the U.S., there is a strong preference for home-driven care over clinical visits, making user-friendly, disposable, and connected autoinjectors vital. The U.S. features a high concentration of pharmaceutical organizations investing in biologics and biosimilars, which need advanced, patent-protected, prefilled delivery tools.

Canada Market Trends

Canada's autoinjectors market is growing due to rising cases of diabetes, rheumatoid arthritis, and severe allergies. More than 4 million Canadians live with diabetes, increasing demand for self-injection devices. Competition includes global pharmaceutical companies and device manufacturers. Connected autoinjectors and user-friendly designs are becoming popular. Growth opportunities include home healthcare expansion, biologic drug adoption, digital monitoring, and improved reimbursement supporting wider patient access.

Asia Pacific held 23% share of the market, and is expected to have the fastest CAGR during the forecast period, due to a massive, increasing patient population suffering from chronic conditions such as diabetes and rheumatoid arthritis, joined with growing healthcare expenditure and enhanced infrastructure. The region is an increasing hub for biologics and biosimilars in oncology and immunology, which drives the growth of the market.

India Market Trends

India is significantly evolving into a worldwide hub for generic injectable drugs, driven by growing cases of illnesses, affordable production, and solid pharmaceutical exports. The healthcare manufacturing is encountering a significant increase due to the heightened advancement and generation of generic injectables. The growing need for the ease of drug administration, which increases the demand for autoinjectors.

China Market Trends

China is witnessing strong growth in the autoinjectors market because of increasing chronic disease cases and expanding biologic therapy use. The population exceeds 1.4 billion, creating significant demand. Competition includes domestic manufacturers and multinational pharmaceutical companies. Smart autoinjectors and reusable devices are gaining attention. Growth opportunities come from healthcare modernization, higher patient awareness, expanding insurance coverage, and increasing production of biologic medicines.

Europe has a mature autoinjectors market supported by widespread biologic therapy adoption and advanced healthcare systems. The region has more than 100 million people living with chronic diseases. Competition remains strong among global device manufacturers and pharmaceutical companies. Trends include connected autoinjectors and sustainable designs. Growth opportunities include home-based treatment, personalized medicine, and increasing biosimilar adoption across healthcare systems.

UK Market Trends

The UK autoinjectors market benefits from growing biologic therapy use and strong healthcare services. More than 5 million people live with diabetes, supporting demand for self-injection technologies. Competition includes global pharmaceutical companies and innovative device developers. Connected autoinjectors and patient-friendly designs are key trends. Growth opportunities include expanding home treatment, increasing biosimilar prescriptions, digital healthcare integration, and greater focus on improving medication adherence.

Germany Market Trends

Germany is a major autoinjectors market because of strong healthcare infrastructure and high biologic medicine usage. The country has over 7 million people living with diabetes, supporting demand for convenient drug delivery. Competition includes international pharmaceutical companies and medical device manufacturers. Trends include ergonomic devices and digital connectivity. Growth opportunities come from expanding home care, rising autoimmune disease treatment, and increasing patient preference for self-administration.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | SHL Medical, Ypsomed, Haselmeier (medmix), West Pharmaceutical Services | Develop autoinjector platforms and injection technologies |

| Product Manufacturers | Becton Dickinson (BD), SHL Medical, Ypsomed, Owen Mumford, Gerresheimer | Manufacture commercial autoinjectors and device components |

| Service Providers | Phillips-Medisize, Nemera, Jabil Healthcare | Device engineering, design, industrialization, manufacturing support |

| Platform Providers | SHL Medical, Ypsomed, West Pharmaceutical Services, Haselmeier | Provide reusable and customizable autoinjector platforms |

| CROs/CDMOs | Recipharm, Phillips-Medisize, Nemera | Combination product development and commercialization services |

| Software Vendors | Phillips-Medisize, BD Digital Health | Connected-device integration and adherence monitoring solutions |

| Research Institutions | Massachusetts Institute of Technology, Karolinska Institute, Fraunhofer Institute | Advanced injectable delivery research |

| End-User Industries | Pharmaceuticals, Biotechnology, Healthcare Providers, Home Healthcare | Final users and purchasers of autoinjector systems |

R&D:

Manufacturing Processes:

Patient Services:

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 28% | 14% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Becton, Dickinson and Company (BD) | Franklin Lakes, New Jersey | USA | Largest global drug delivery device supplier with broad autoinjector portfolio | BD Physioject™, BD Intevia™, Self-Injection Systems |

| SHL Medical | Zug | Switzerland | World's largest dedicated autoinjector manufacturer serving major biopharma firms | Molly®, Rotaject®, Elexy™, Autoinjector Platforms |

| Ypsomed AG | Burgdorf, Bern | Switzerland | Leading independent autoinjector platform provider with extensive pharma partnerships | YpsoMate®, YpsoDose®, YpsoMate 5.5 |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| AbbVie Inc. | North Chicago, Illinois | USA | Major autoinjector usage through immunology franchise | Humira Pen®, Skyrizi Injector |

| Teva Pharmaceutical Industries | Petah Tikva | Israel | Commercial autoinjectors in neurology and specialty care | AJOVY® Autoinjector |

| Viatris Inc. | Canonsburg, Pennsylvania | USA | Owner of EpiPen franchise, one of the most recognized autoinjectors globally | EpiPen®, Generic EpiPen |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Gerresheimer AG | Düsseldorf, North Rhine-Westphalia | Germany | Growing autoinjector and containment systems provider | Gx Inbeneo®, Gx InnoSafe |

| West Pharmaceutical Services | Exton, Pennsylvania | USA | Leading containment and self-injection technology supplier | SmartDose®, Daikyo Components |

| Haselmeier (medmix Drug Delivery) | Rotkreuz, Zug | Switzerland | Specialized autoinjector platform developer | D-Flex®, DAI®, PiccoJect® |

In October 2025, “We are excited to introduce Brekiya autoinjector, making this innovative therapy broadly available to healthcare providers and patients. As the first and only self-administered, ready-to-use DHE autoinjector, Brekiya offers patients the ability to treat debilitating attacks in a convenient way and avoid visits to the emergency room. With our expanding neurology portfolio, Amneal is committed to supporting providers through comprehensive education and ensuring strong patient access as we bring Brekiya autoinjector to market,” said Joe Renda, Senior Vice President, Chief Commercial Officer – Specialty.

Strengths

Weakness

Opportunities

Threat

By Type

By Route of Administration

By Therapy Area

By Technology

By End User

By Distribution Channel

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar