Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

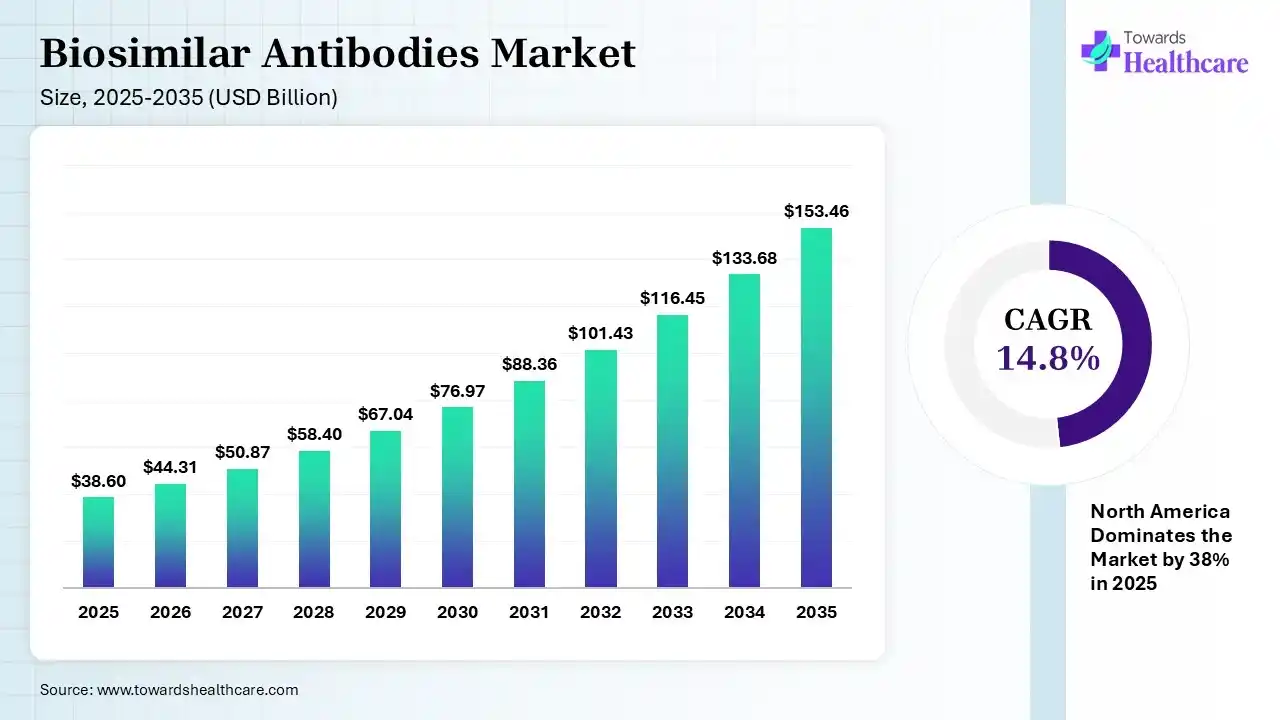

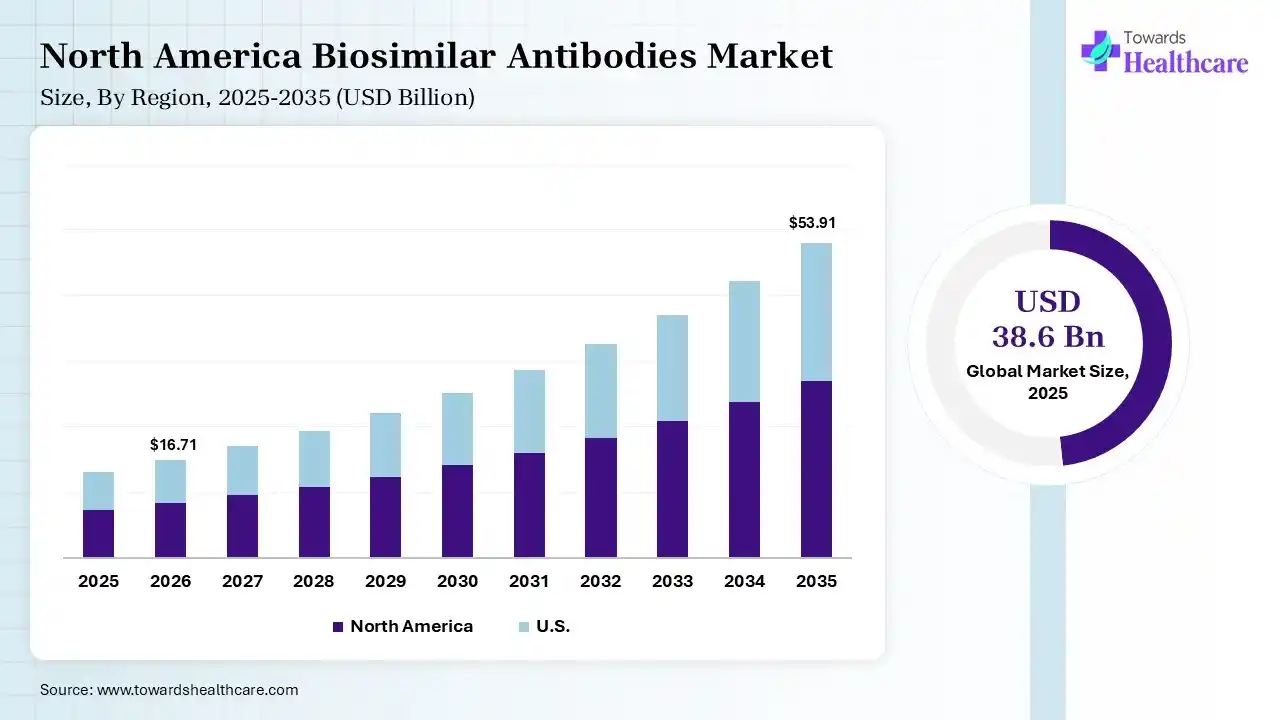

The global biosimilar antibodies market size was estimated at USD 38.6 billion in 2025 and is predicted to increase from USD 44.31 billion in 2026 to approximately USD 153.46 billion by 2035, expanding at a CAGR of 14.8% from 2026 to 2035. The market is expanding rapidly due to the growing loss of exclusivity of major biologic drugs and the increasing need for more affordable treatment options in cancer and autoimmune disorders. Adoption is higher in developed markets, while emerging regions are accelerating growth through supportive regulations and rising biologics demand.

")

Biosimilar antibodies are highly clinically equivalent versions of approved reference monoclonal antibodies, developed to match their safety, efficacy, and quality while offering a more cost-effective treatment option. The biosimilar antibodies market is growing due to increasing patient expectations of blockbuster biologics, rising demand for affordable cancer and autoimmune treatments, and expanding healthcare access worldwide. Supportive regulatory pathways, growing acceptance of biosimilars among physicians, and cost-containment pressure on healthcare systems are further accelerating adoption. Additionally, advancements in biomanufacturing are improving product quality and boosting market confidence globally.

AI is transforming the market by accelerating drug development, improving molecular similarity analysis, and optimizing manufacturing processes. It helps reduce development time and costs while ensuring high quality and consistency. Additionally, AI-driven data insights support regulatory compliance, clinical trial design, and market forecasting, enabling faster approvals and broader adoption of biosimilars.

| Table | Scope |

| Market Size in 2026 | USD 44.31 Billion |

| Projected Market Size in 2035 | USD 153.46 Billion |

| CAGR (2026 - 2035) | 14.8% |

| Leading Region | North America by 38% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Molecular Type, By Application, By Distribution Channel, By Region |

| Top Key Players | Roche, Mylan, Teva Pharmaceutical Industries, Biogen, Fresenius Kabi, Sandoz |

")

| Segment | Share 2025 (%) |

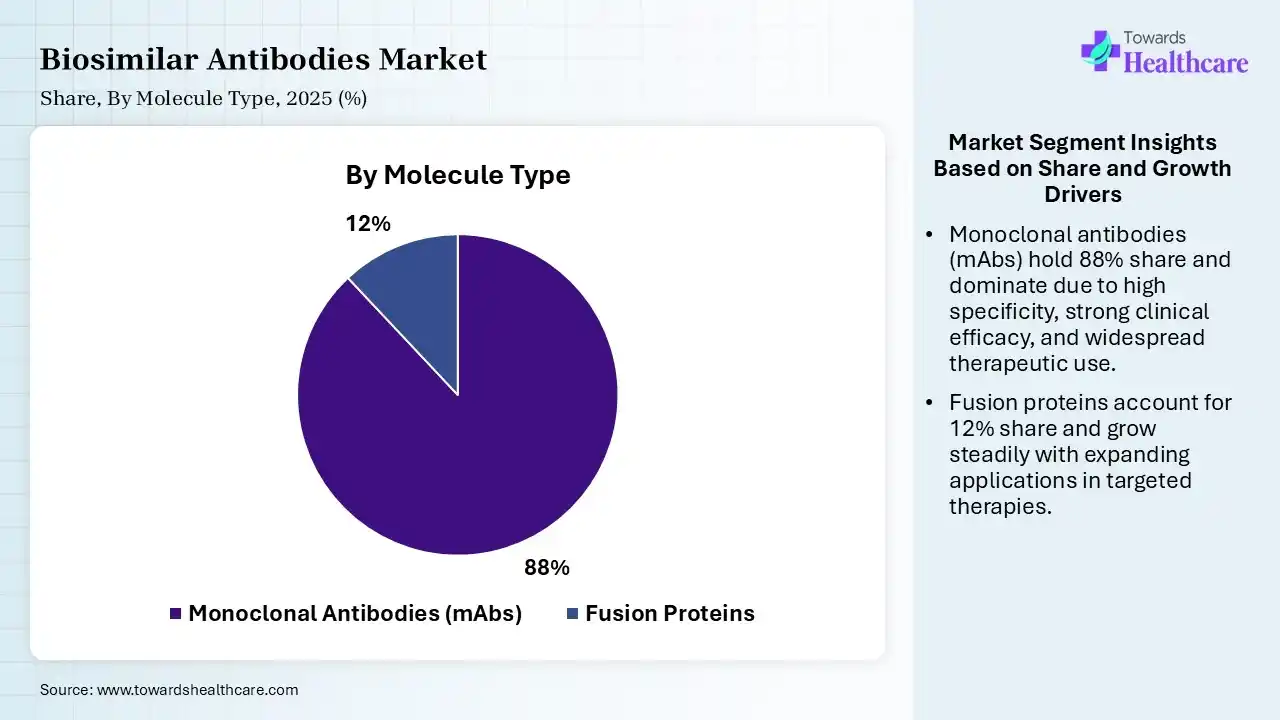

| Monoclonal Antibodies (mAbs) | 88% |

| Fusion Proteins | 12% |

The Monoclonal Antibodies (mAbs) Segment Dominated the Market in 2025

The monoclonal antibodies (mAbs) segment dominated the biosimilar antibodies market with a revenue share of 88% in 2025 due to their widespread use in treating cancer, autoimmune, and inflammatory diseases. High clinical effectiveness, strong demand for targeted therapies, and multiple patient experiences of leading mAb biologics drove biosimilar development. Additionally, established manufacturing processes and regulatory familiarity supported faster approvals, boosting their adoption and market share globally.

The fusion proteins segment held the second-largest share of 12% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to their strong use in autoimmune and inflammatory disease treatment, offering targeted action and improved stability. Growing demand for cost-effective biologics, along with patient expiration of key reference fusion therapies, is driving biosimilar development. Additionally, their proven clinical effectiveness and increased physician acceptance are supporting steady adoption and contributing to their significant market position.

")

| Segment | Share 2025 (%) |

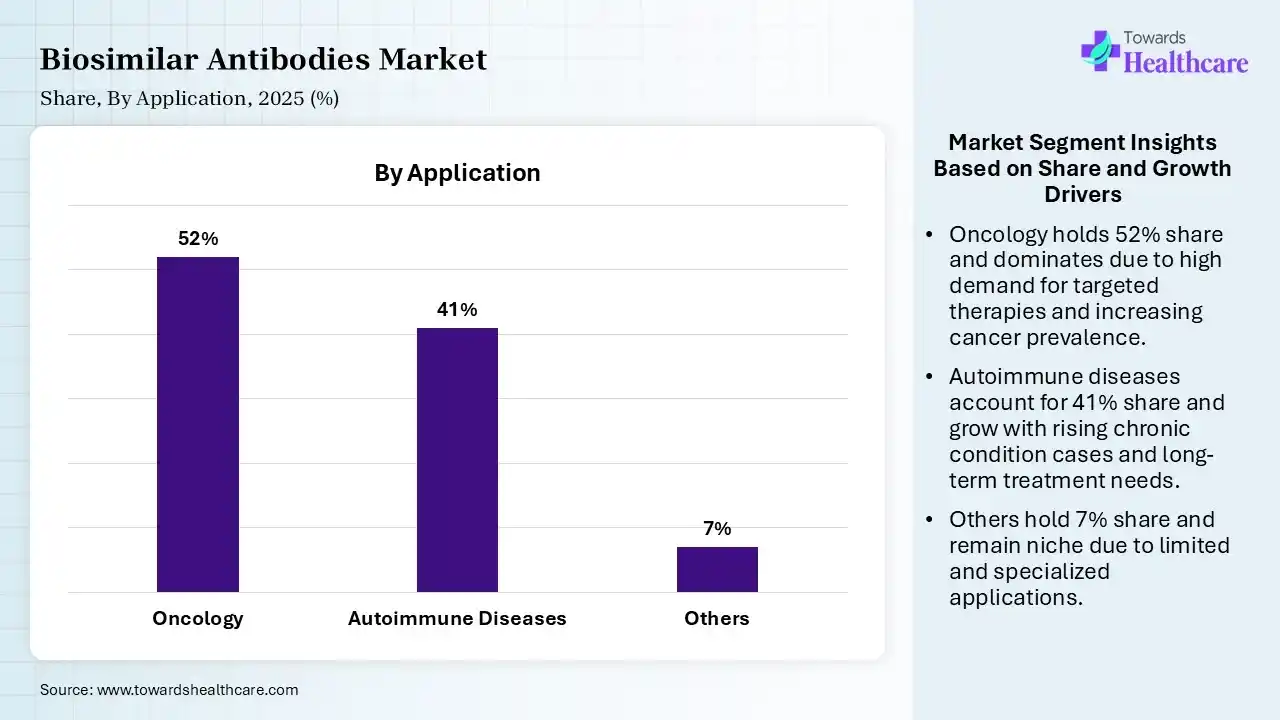

| Oncology | 52% |

| Autoimmune Diseases | 41% |

| Others | 7% |

The Oncology Segment Led the Market in 2025 with the Largest Share

The oncology segment held a dominant share of 52% in the biosimilar antibodies market in 2025 due to the high global burden of cancer and widespread use of biologic therapies in this treatment. Expiry of patents for major oncology biologics encouraged biosimilar entry of biosimilars, improving affordability and access. Strong clinical reliance on targeted monoclonal antibodies, along with increasing healthcare spending and early diagnosis rates, further supports the segment’s dominant market position.

The autoimmune diseases segment held the second-largest share of 41% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to the high prevalence of conditions like rheumatoid arthritis and psoriasis, which require long-term biologics therapy. Biosimilar antibodies offer more affordable alternatives, increasing patient access and adherence. Additionally, strong clinical effectiveness of anti-TNF and other targeted therapies, along with growing physical confidence and supportive reimbursement policies, is driving steady adoption in this segment.

")

| Segment | Share 2025 (%) |

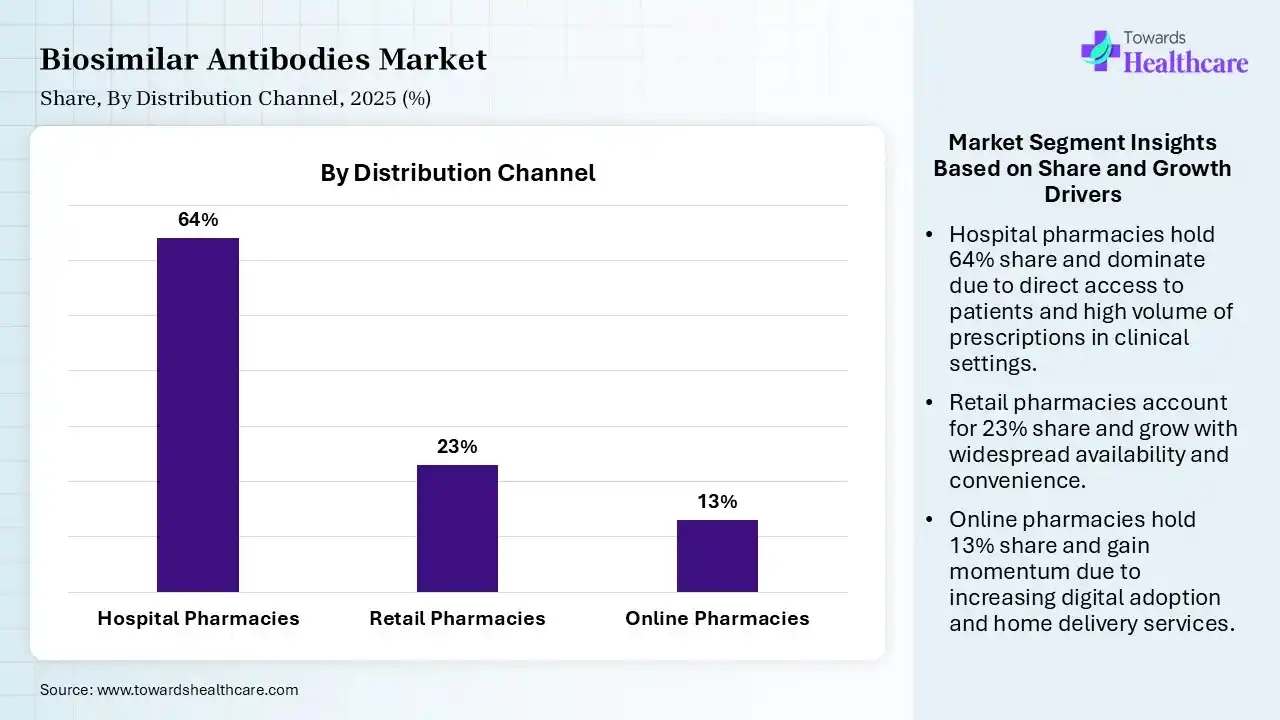

| Hospital Pharmacies | 64% |

| Retail Pharmacies | 23% |

| Online Pharmacies | 13% |

The Hospital Pharmacies Segment Led the Market in 2025 with the Largest Share

The hospital pharmacies segment led the biosimilar antibodies market with a share of 64% in 2025 because these therapies are often administered in clinical settings requiring specialized supervision. Hospitals manage high patient volumes in oncology and autoimmune care, ensuring controlled dispensing and monitoring. Favorable procurement system bulk purchasing, and strong integration with treatment protocols also support their dominance, while physician preference for hospital-based administration further drives this segment’s leading share.

The retail pharmacies segment held the second-largest share of 23% of the market in 2025 due to increasing availability of biosimilar antibodies for chronic conditions that can be managed outside hospitals. Growing patient preferences for convenient access, expanding pharmacy networks, and improved distribution channels support this growth. Additionally, rising awareness, physician prescriptions for maintenance therapies, and supportive reimbursement policies are driving steady adoption through retail pharmacy settings.

The online pharmacies segment held a 13% share in 2025 and is expected to grow at the fastest CAGR in the biosimilar antibodies market during the forecast period due to increasing digital adoption, convenience of home delivery, rising preference for remote healthcare services, expanding e-pharmacy platforms, and improved accessibility of biosimilar antibodies. Additionally, growing internet penetration and cost benefits are encouraging more patients to shift towards the online purchasing channel.

")

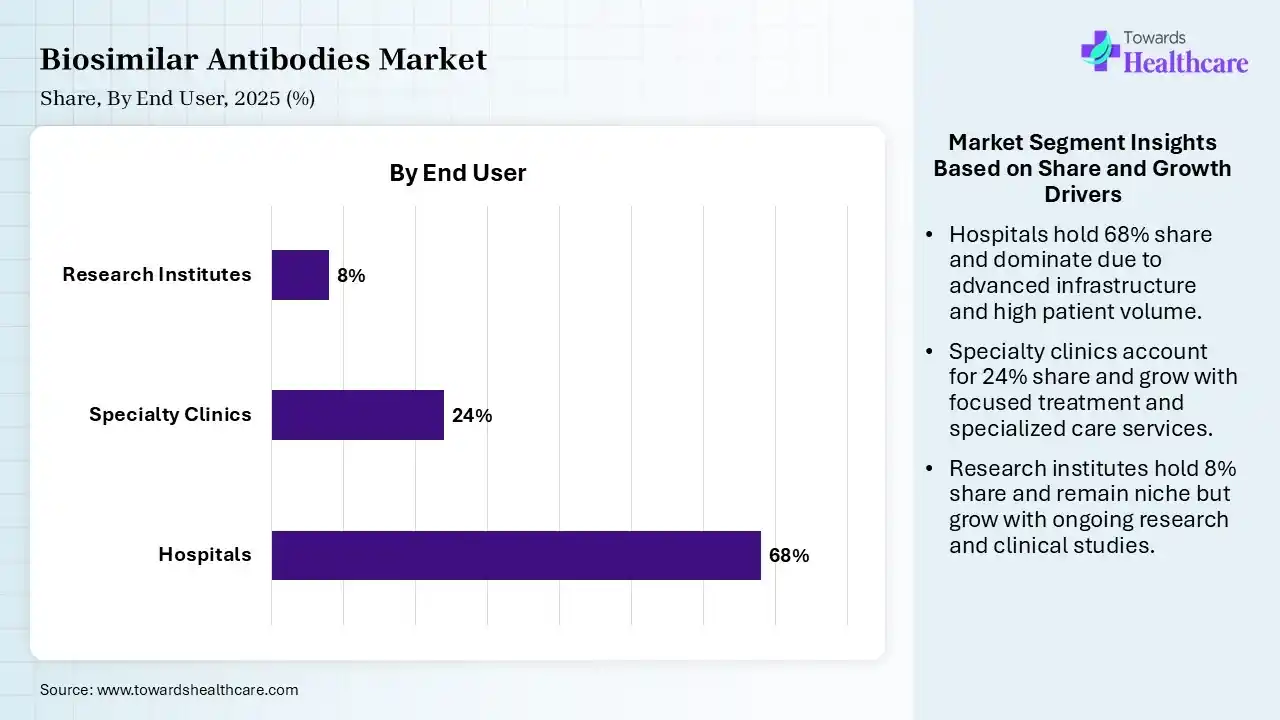

| Segment | Share 2025 (%) |

| Hospitals | 68% |

| Specialty Clinics | 24% |

| Research Institutes | 8% |

The Hospitals Segment held a Dominant Position in the Market in 2025

The hospitals segment held a dominant share of 68% in the biosimilar antibodies market in 2025 due to the high volume of patients requiring complex biologic treatment, particularly in oncology and autoimmune care. These therapies often need controlled administration, monitoring, and specialized supervision, which hospitals provide. Additionally, strong procurement systems, availability of advanced infrastructure systems, availability of advanced infrastructure, and physical preference for hospital-based treatment settings contribute significantly to their leading market share.

The specialty clinics segment held the second-largest share of 24% of the market in 2025 and is expected to grow at the fastest CAGR in the market during the forecast period due to their focused expertise in managing chronic and complex conditions like cancer and autoimmune diseases. These clinics offer targeted biologic therapies with personalized care and shorter wait times than hospitals. Increasing patient preferences for specialized treatment settings, along with expanding clinic networks and physician expertise, is driving steady adoption of biosimilar antibodies in this segment.

The research institutes segment held 8% of the biosimilar antibodies market share in 2025 due to increasing focus on biosimilar development, clinical trials, and advanced biologics research. Rising investments in biotechnology, collaborations with pharmaceutical companies, and government funding are supporting innovation in antibody therapies. Additionally, growing demand for analytical studies, comparability testing, and new biosimilar pipeline development is driving the expanding role if research institutes in the market.

")

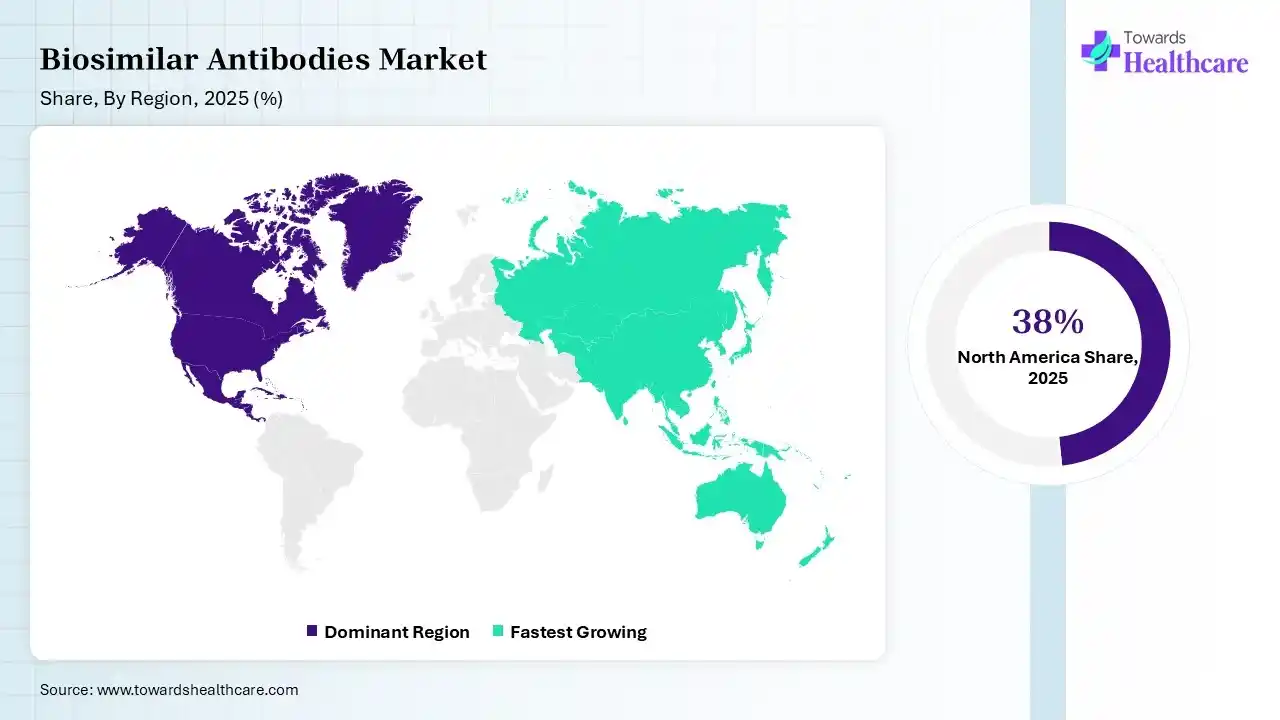

North America dominated the biosimilar antibodies market with 38% share in 2025 due to strong healthcare infrastructure, high adoption of advanced biologics, and early regulatory approvals. The presence of leading pharmaceutical companies, increasing patient expectations of key biologics, and rising healthcare spending support growth. Additionally, favorable reimbursement policies and growing awareness among physicians and patients drive widespread biosimilar uptake in this region.

U.S. Market Trends

The U.S. leads the market due to its advanced healthcare systems, strong presence of leading biopharmaceutical companies, and increasing approvals of biosimilars. High biologics spending and growing pressure to reduce treatment costs are accelerating adoption. Additionally, a supportive regulatory framework, expanding insurance coverage, and rising physician confidence in biosimilars are driving significant market growth across oncology and autoimmune therapies.

Asia Pacific held 23% of the total market share in 2025 and is expected to grow at the fastest CAGR in the biosimilar antibodies market due to increasing healthcare investments, expanding patient population, and rising demand for affordable biologics treatments. Supportive government initiatives, improving regulatory framework, and growing local biosimilar manufacturing capabilities are accelerating market expansion. Additionally, enhanced healthcare services and rising awareness are driving rapid adoption across emerging economies.

India: Emerging Powerhouse in Biosimilar Antibodies Market

India is expected to grow at the fastest CAGR due to its strong biopharmaceutical manufacturing base, cost-efficient production capabilities, and increasing demand for affordable biologics treatments. Government support, expanding healthcare infrastructure, and rising prevalence of chronic diseases are boosting adoption. Additionally, growing investments by domestic companies and improving regulatory pathways are accelerating biosimilar development and market expansion.

R&D

Clinical Trials

Regulatory Approvals

| Companies | Headquarters | Offerings |

| Roche | Basel, Switzerland | Focuses on oncology and immunology biologics, with biosimilar development through partnerships and strong expertise in monoclonal antibodies. |

| Mylan | Pennsylvania, USA | Broad biosimilar portfolio including monoclonal antibodies for oncology and autoimmune diseases, often developed in collaboration with global partners. |

| Teva Pharmaceutical Industries | Tel Aviv, Israel | Engages in biosimilar antibody development with a focus on oncology and immunology, leveraging large-scale manufacturing and global distribution. |

| Biogen | Massachusetts, USA | Develops and commercializes biosimilars primarily in immunology, with strong capabilities in biologics manufacturing and partnerships. |

| Fresenius Kabi | Bad Homburg, Germany | Offers a growing range of biosimilar monoclonal antibodies, focusing on oncology and autoimmune therapies with emphasis on hospital-based treatments. |

| Sandoz | Basel, Switzerland | A global leader in biosimilars, providing a wide portfolio of monoclonal antibodies across oncology and immunology, supported by strong R&D and commercialization capabilities |

Strengths

Weaknesses

Opportunities

Threats

By Molecular Type

By Application

By Distribution Channel

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar