Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

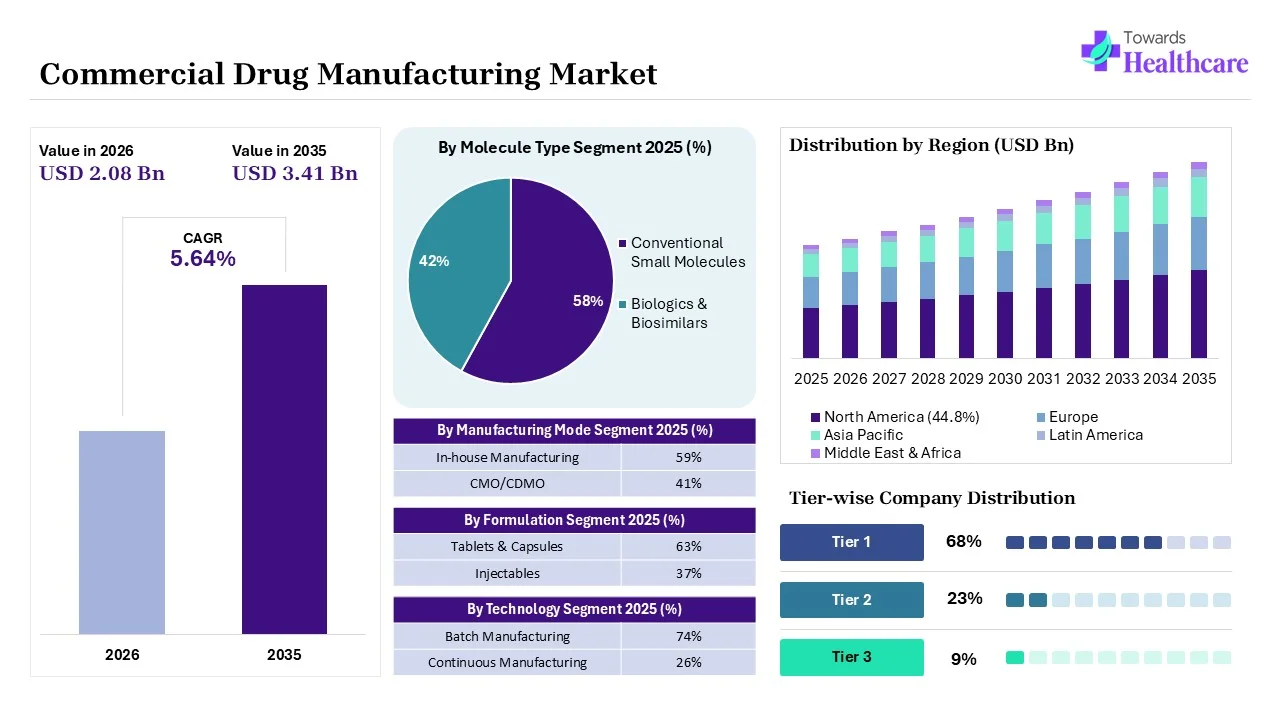

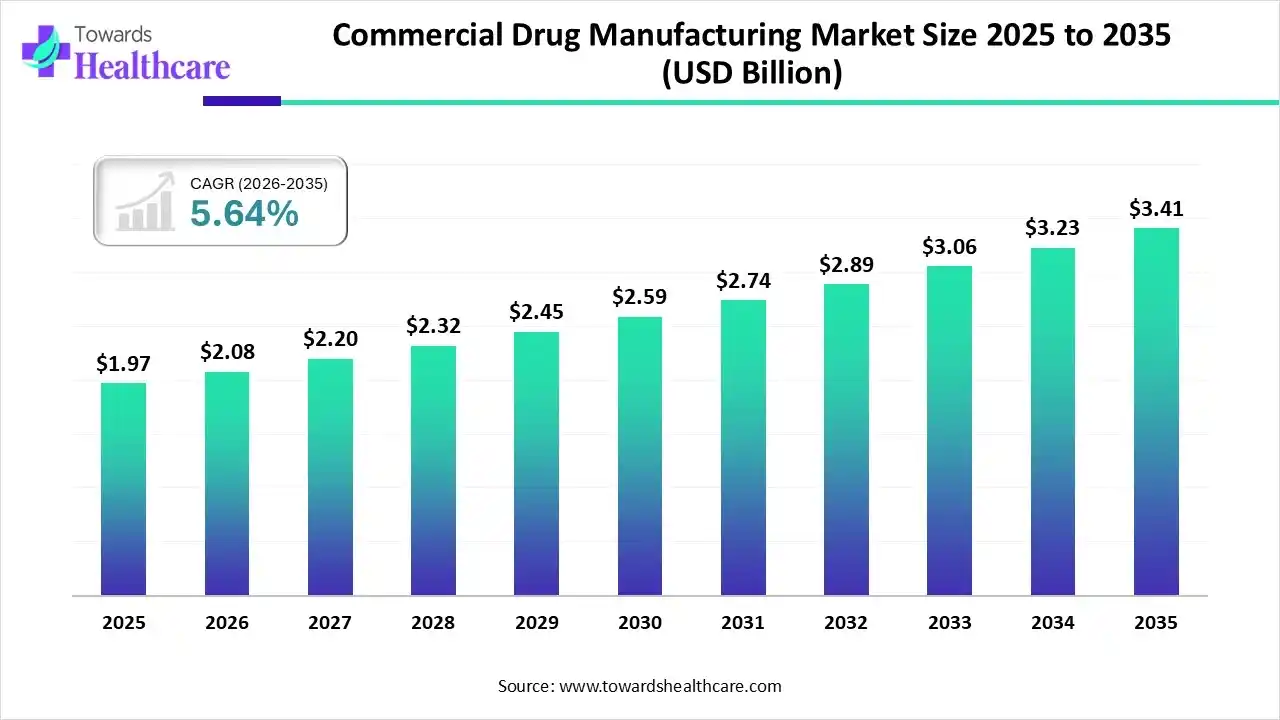

The global commercial drug manufacturing market size was estimated at USD 1.97 billion in 2025 and is predicted to increase from USD 2.08 billion in 2026 to approximately USD 3.41 billion by 2035, expanding at a CAGR of 5.64% from 2026 to 2035.

The market is expanding steadily, driven by rising medicine demand, increased outsourcing to CMO/CDMOs, technological advancement, and growing production of biologics, generic and complex pharmaceutical formulations worldwide.

Commercial drug manufacturing is the large-scale production of pharmaceutical products for market distribution including APIs, formulations, and biologics, in compliance with regulatory and quality standards. The commercial drug manufacturing market is growing due to rising global demand for affordable medicine, increasing prevalence of chronic diseases, and rapid expansion of generic and specialty drugs. Pharmaceutical companies are outsourcing manufacturing to CMOs and CDMOs to reduce costs and accelerate production. Additionally, advancements in manufacturing technologies, regulatory compliance capabilities, and growing focus on biologics and biosimilars are further supporting market expansion.

The commercial drug manufacturing market is growing fast as global health needs change. More pharmaceutical companies now use specialized external factories to make complex medicines. This shift includes modern, precise treatments like gene and cell therapies. These advanced drugs require highly clean and flexible workspaces to prevent errors. Therefore, many facilities now use single-use equipment to eliminate contamination risks. They also use smart software to monitor product quality in real time. This automated technology helps prevent costly mistakes and speeds up the entire production timeline. As a result, companies can create and package vital medicines much faster than before. These updated operational strategies keep the global drug supply chain steady during unexpected health crises. Most importantly, it helps get safe, life-saving treatments to diverse patient populations quickly. By modernizing these production processes, the entire industry becomes more efficient, secure, and reliable for everyone.

Artificial intelligence is transforming the commercial drug manufacturing market by improving process efficiency, quality control, and predictive maintenance. AI enables real-time monitoring, reduces production errors, accelerates scale-up, and supports regulatory compliance, helping manufacturers lower costs, improve consistency, and increase overall productivity across pharmaceutical manufacturing operations.

Rising Outsourcing to CMOs and CDMOs

Pharmaceutical companies are increasingly outsourcing manufacturing to specialized CMOs and CDMOs to reduce capital investment, enhance flexibility, and accelerate product launches, making outsourcing a long-term growth driver for the commercial drug manufacturing market.

Shift Toward Advanced and Complex Therapies

Growing demand for biologics, biosimilars, and specialty drugs is pushing manufacturers to invest in advanced facilities, single-use systems, and skilled expertise, shaping the future toward high-value, technology-driven pharmaceutical production.

Digital and Smart Manufacturing Adoption

The integration of automation, AI, and data-driven manufacturing is improving operational efficiency, quality assurance, and regulatory compliance, enabling manufacturers to optimize production processes and remain competitive in an evolving global pharmaceutical landscape.

| Key Elements | Scope |

| Market Size in 2026 | USD 2.08 Billion |

| Projected Market Size in 2035 | USD 3.41 Billion |

| CAGR (2026 - 2035) | 5.64% |

| Leading Region | North America by 44.8% |

| Key Applications | Drug substance manufacturing, drug product formulation, fill-finish operations, biologics production, scale-up manufacturing, commercial supply chain execution |

| Primary End Users | Pharmaceutical companies, biotechnology firms, generic drug manufacturers, government healthcare programs |

| Key Growth Drivers | Outsourcing trend in pharma, biologics pipeline expansion, cost optimization, patent expirations, complex molecule manufacturing demand, capacity constraints at pharma companies |

| Market Segmentation | By Molecule Type, By Manufacturing Mode, By Formulation, By Technology, By Region |

| Top Key Players | F. Hoffmann-La Roche Ltd., Novartis AG, GlaxoSmithKline plc, Pfizer, Inc., Merck & Co., Inc., AstraZeneca |

| Segments | Shares % |

| Conventional Small Molecules | 58% |

| Biologics & Biosimilars | 42% |

Why Did the Conventional Small Molecules Segment Dominate in the Market in 2025?

The conventional small molecules segment dominated the commercial drug manufacturing market with a share of approximately 58% in 2025 due to its established production processes, lower manufacturing costs, and wide application across chronic and acute therapies. Strong demand for generic medicines, patient expire of branded drugs, and easier regulatory pathways further supported large-scale production and market leadership of small-molecule drugs.

Biologics & Biosimilars

The biologics & biosimilars segment is expected to grow at the fastest CAGR during the forecast period due to rising prevalence of complex and chronic diseases, increasing adoption of targeted therapies, and strong demand for cost-effective biosimilars. Advancements in bioprocessing technologies, expanding regulatory approvals, and growing investments in biologics manufacturing capacity are further accelerating segment growth.

| Segments | Shares % |

| In-house Manufacturing | 59% |

| CMO/CDMO | 41% |

How the In-house Manufacturing Segment Dominated the Commercial Drug Manufacturing Market in 2025?

The in-house manufacturing segment dominated the market with a share of approximately 59% in 2025 as pharmaceutical companies prioritize greater control over production quality, intellectual property, and regulatory compliance. Established manufacturing infrastructure, improved capacity utilization, and the need to ensure supply chain reliability, especially for high-volume and critical drugs, supported continued reliance on internal manufacturing capabilities.

CMO/CDMO

The CMO/CDMO segment is expected to grow at the fastest CAGR during the forecast period as pharmaceutical companies increasingly outsource manufacturing to reduce capital investment and operational risk. CMOs and CDMOs offer scalable capacity, advanced technologies, and regulatory expertise, enabling faster product development and commercialization. Growing demand for biologics and speciality drugs further supports the accelerated growth of this segment.

| Segments | Shares % |

| Tablets & Capsules | 63% |

| Injectables | 37% |

Why the Tablets & Capsules Segment Dominated the Commercial Drug Manufacturing Market?

The tablets & capsules segment dominated the market by 63% share due to their cost-effective production, long shelf life, and ease of transportation. High patient preference, accurate dosing, and widespread use in treating chronic and acute conditions supported use in treating chronic and acute conditions supported large-scale manufacturing. Additionally, well-established production technologies and strong demand for generic oral formulations reinforced the segment’s market leadership.

Injectables

The injectables segment is expected to grow at the fastest CAGR during the forecast period due to increasing demand for biologics, biosimilars, vaccines, and oncology therapies that require parenteral administration. Rising prevalence of chronic and critical diseases, along with the need for faster therapeutic action and improved bioavailability, is driving injectable adoption. Additionally, advancements in sterile manufacturing, fill-finish capabilities, and regulatory support are further accelerating segment growth.

| Segments | Shares % |

| Batch Manufacturing | 74% |

| Continuous Manufacturing | 26% |

Why Did the Batch Manufacturing Segment Dominate in the Market in 2025?

The batch manufacturing segment led the commercial drug manufacturing market share of approximately 74% in 2025 due to its widespread adoption, operational flexibility, and suitability for producing a wide range of drug formulations. Its well-established regulatory acceptance, ease of quality control, and ability to manage variable production volumes made batch manufacturing the preferred technology for commercial drug production, particularly for generics and small-molecule drugs.

Continuous Manufacturing

The continuous manufacturing segment is expected to grow at the fastest CAGR during the forecast period due to its ability to improve production efficiency, reduce costs, and ensure consistent product quality. This technology enables real-time monitoring, faster scale-up, and lower material waste. Increasing regulatory support, adoption of advanced automation, and the need for flexible, high-throughput manufacturing are further accelerating the shift toward continuous manufacturing in the commercial drug manufacturing market.

")

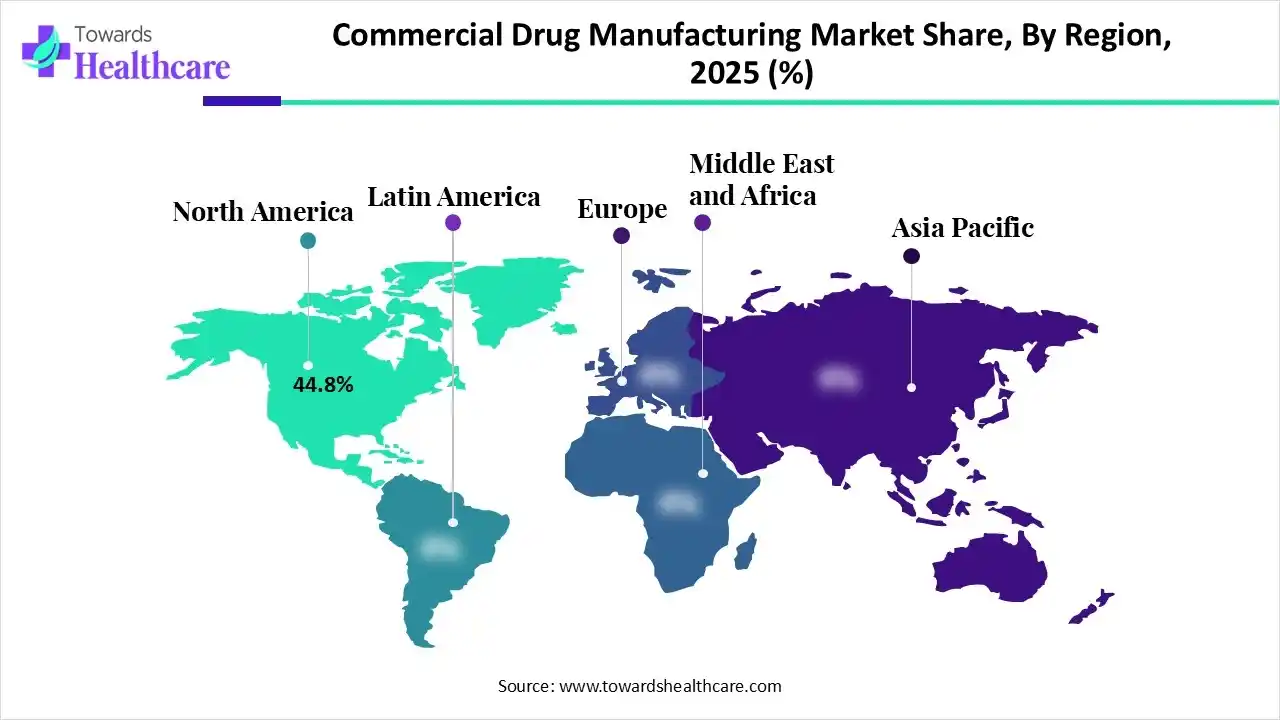

North America dominated the global commercial drug manufacturing market in 2025 with an approximate 44.8% share due to its strong pharmaceutical infrastructure, high R&D spending, and presence of leading drug manufacturers and CDMOs. Favourable regulatory frameworks, advanced manufacturing technologies, and strong demand for innovative, biologics, and specialty drugs further supported large-scale production and market leadership across the region.

US Market Leadership Driven by Innovation and Manufacturing Strength

The U.S. captured the largest revenue share in the commercial drug manufacturing market in 2025 due to its pharmaceutical innovation ecosystem, advanced manufacturing infrastructure, and high healthcare spending. The presence of major pharmaceutical companies and leading CDMOs, combined with. robust regulatory oversight and rapid adoption of advanced manufacturing technologies, supported large-scale production. Strong demand for branded, biologic, and specialty drugs further reinforced the market leadership.

Canada Market Trends

In Canada, the commercial drug manufacturing market expands due to heavy funding in local hubs. The country wants to protect its domestic medicine supplies following recent international shortages. As a direct result, modern biologics and specialized vaccines strongly lead this production expansion. Local companies are rapidly constructing smart facilities to produce treatments much faster. This targeted effort reduces dependence on foreign medical imports during major global health crises.

Asia-Pacific is anticipated to grow by 20% share at the fastest CAGR during the forecast period due to expanding pharmaceutical manufacturing capacity, lower production costs, and increasing outsourcing from global drug manufacturing. Rapid growth in generic drugs, rising healthcare demand, supportive government initiatives, and a skilled workforce in countries such as India and China are further accelerating regional market expansion.

India’s Rapid Rise in the Commercial Drug Manufacturing Market

India is anticipated to grow at a rapid CAGR during the forecast period due to its strong position in generic drug production, cost-competitive manufacturing, and a large base of regulatory-approved facilities. Increasing global outsourcing to Indian CMOs and CDMOs, expanding biologics and biosimilars capacity, supportive government initiatives, and rising domestic healthcare demand are further driving accelerated market growth.

China Market Trends

China is growing rapidly by shifting its entire focus toward highly advanced medicine production methods. The nation is moving away from basic generic drugs to manufacturing complex biologics and cell therapies. Massive, state-funded biotech parks are opening across major cities to accelerate these daily manufacturing timelines. Factories aggressively adopt digital automation tools to satisfy strict international standards. This massive growth lets China supply affordable medicines locally and worldwide.

Europe is anticipated to grow by 27.2 % share at a lucrative rate during the forecast period due to strong regulatory standards, advanced pharmaceutical manufacturing capabilities, and increasing focus on quality-driven production. Rising investments in biologics, biosimilars, and specialty drugs, along with expanding CDMO activities and supporting government initiatives, are strengthening Europe’s position in the global commercial drug manufacturing market.

UK’s Accelerated Growth in Commercial Drug Manufacturing Market

The UK is anticipated to grow at arapid CAGR during the forecast period due to its strong life science ecosystems, advanced manufacturing infrastrcturem and increasing investment in biologics and specialty drug production. The growing presence of CDMOs, a supportive regulatory framework, and strong collaboration between industry and research institutions are further accelerating innovation, capacity expansion, and market growth.

Germany Market Trends

Germany maintains its strong position as Europe's leading medicine manufacturer through constant high-tech innovation. German production facilities focus tightly on complex, small-batch formulas and highly personalized patient treatments. They integrate sophisticated robotic systems and continuous processing models to maximize quality while reducing manufacturing waste. Close collaboration between local research universities and private factories keeps their production lines efficient, secure, and globally competitive every day now.

| Ecosystem Category | Key Role in Market | Examples of Participants |

| Technology Providers | Provide bioprocessing, automation, and manufacturing technologies | Single-use bioreactors, chromatography systems, automation platforms |

| Product Manufacturers | Produce commercial-scale drug substances and finished dosage forms | CDMOs, pharmaceutical manufacturers |

| Service Providers | Offer regulatory support, analytical testing, and supply chain services | QA/QC labs, regulatory consultants |

| Platform Providers | Enable integrated biologics and gene therapy manufacturing platforms | Bioprocess platform innovators |

| CROs/CDMOs | Handle outsourced development + commercial-scale production | Full-service biologics and small molecule CDMOs |

| Software Vendors | Provide MES, LIMS, and manufacturing execution systems | Pharma manufacturing IT platforms |

| Research Institutions | Support process innovation and scale-up research | Bioprocess engineering institutes |

| End-User Industries | Purchase manufactured drug products | Pharma companies, hospitals, governments |

R&D

Clinical Trials

Packaging and Serialization

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 60% | 28% | 12% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza Group AG | Basel | Switzerland | Largest global biologics CDMO with strong mammalian cell culture and commercial biologics production | Biologics manufacturing, cell & gene therapy production, commercial drug substance manufacturing |

| Catalent, Inc. | Somerset, New Jersey | USA | Major global CDMO specializing in drug product development and large-scale commercial manufacturing | Oral solids, biologics fill-finish, drug delivery technologies, commercial supply |

| Thermo Fisher Scientific (Patheon) | Waltham, Massachusetts | USA | Integrated CDMO with global commercial manufacturing footprint across APIs and finished dosage forms | API manufacturing, sterile fill-finish, commercial biologics production |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Siegfried Holding AG | Zofingen | Switzerland | Strong global CDMO specializing in drug substance and finished dosage manufacturing | API production, formulation, commercial manufacturing services |

| Piramal Pharma Solutions | Mumbai, Maharashtra | India | Fast-growing CDMO with global facilities serving small molecules and biologics | Drug substance manufacturing, formulation development, commercial supply |

| Recipharm AB | Stockholm | Sweden | European CDMO with strong oral solid dosage and sterile manufacturing capabilities | Tableting, sterile injectables, commercial manufacturing |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Aenova Group | Starnberg | Germany | Mid-sized CDMO focused on solid dosage and semi-solid manufacturing | Oral solids, soft gels, commercial manufacturing |

| Ardena Holding NV | Ghent | Belgium | Specialized CDMO offering integrated development-to-commercial services | Drug development, GMP manufacturing, niche commercial supply |

| Sterling Pharma Solutions | Dudley | United Kingdom | API-focused CDMO with strong chemical synthesis capabilities | API manufacturing, scale-up production, commercial APIs |

Strengths

Weaknesses

Opportunities

Threats

In June 2026, “Our Vizag site has become an increasingly important strategic hub,” Anant Barbadikar, President of PharmaZell Operations, said. “This consolidation reflects the technical expertise, operational excellence, and regulatory track record of our Indian teams.”

By Molecule Type

By Manufacturing Mode

By Formulation

By Technology

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar