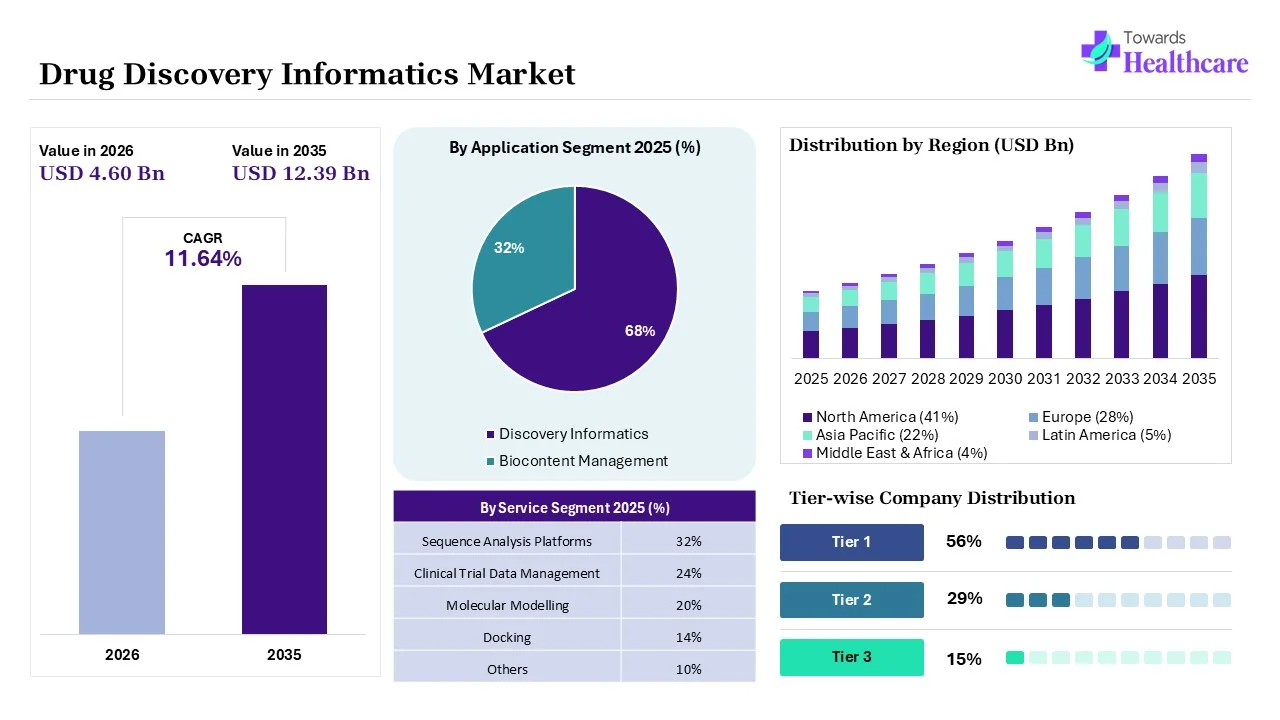

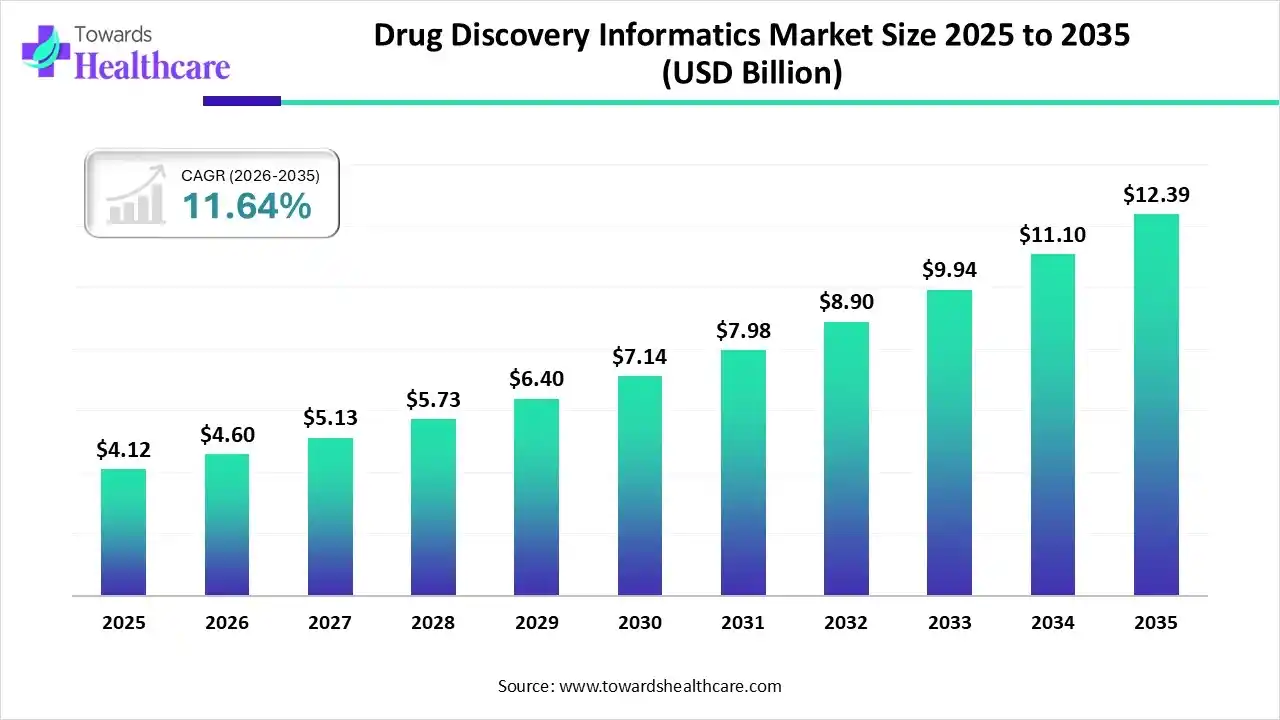

The global drug discovery informatics market size was estimated at USD 4.12 billion in 2025 and is predicted to increase from USD 4.6 billion in 2026 to approximately USD 12.39 billion by 2035, expanding at a CAGR of 11.64% from 2026 to 2035.

")

The market is growing steadily as pharmaceutical companies adopt AI, big data, and computational tools to speed up target identification, reduce R&D costs, and improve decision-making across early-stage drug development.

Drug discovery informatics is the use of computational tools, data analytics, and digital platforms to manage, analyze, and interpret biological and chemical data to accelerate and improve drug development. The drug discovery informatics market is growing due to rising R&D complexity, increasing biomedical data volumes, and strong adoption of AI and cloud-based tools. These solutions help researchers accelerate target identification, optimize lead selection, reduce development costs, and improve success rates. Growing demand for precision medicines and faster drug pipelines further supports market expansion.

")

AI is transforming the drug discovery informatics market by enabling faster data analysis, predictive modeling, and automated screening of drug candidates. It improves target identification, reduces trial-and-error in R&D, shortens development timelines, and lowers costs. AI-driven insights also enhance decision-making accuracy, increasing success rates and accelerating the launch of innovative therapies.

| Table | Scope |

| Market Size in 2026 | USD 4.6 Billion |

| Projected Market Size in 2035 | USD 12.39 Billion |

| CAGR (2026 - 2035) | 11.64% |

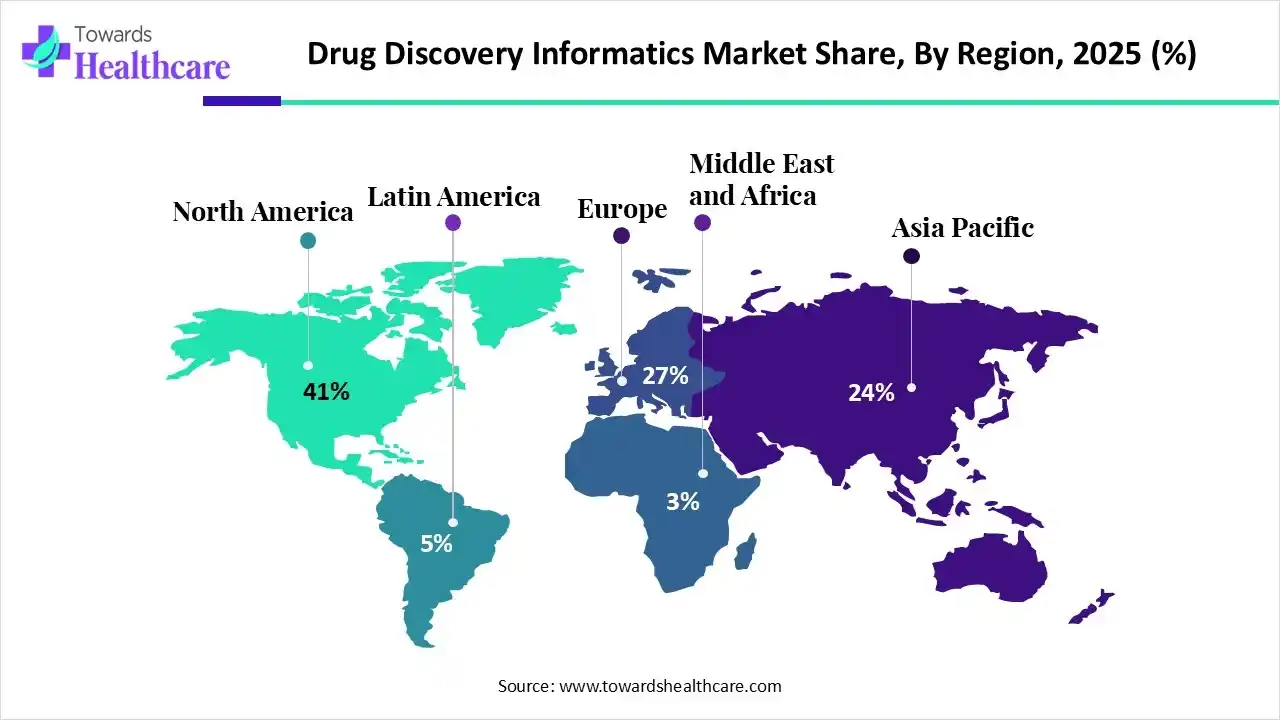

| Leading Region | North America by 41% |

| Key Applications | Sequence analysis, molecular modeling, molecular docking, compound screening, bioinformatics, chemical informatics, discovery data management, clinical research data integration |

| Primary End Users | Pharmaceutical companies, biotechnology companies, CROs, academic research institutes, research laboratories |

| Key Growth Drivers | Increasing pharmaceutical R&D spending, AI adoption in drug discovery, growing biomedical data volumes, precision medicine expansion, demand for faster drug development workflows |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service,By Application, By End Use, By Region |

| Top Key Players | Certara, Boehringer Ingelheim International GmbH, Infosys Ltd., Charles River Laboratories, Collaborative Drug Discovery, Inc. (CDD), Eurofins DiscoverX Products |

| Segments | Shares % |

| Sequence Analysis Platforms | 32% |

| Clinical Trial Data Management | 24% |

| Molecular Modelling | 20% |

| Docking | 14% |

| Others | 10% |

Why Did the Sequence Analysis Platforms Segment Dominate in the Market in 2025?

The sequence analysis platforms segment dominated the drug discovery informatics market by 32% share in 2025 due to the rapid increase in genomics and transcriptomic data generated from high-throughput sequencing technologies. These platforms enable efficient data processing, variant identification, and functional analysis, supporting target discovery, biomarker identification, and personalized drug development, which drove strong adoption across pharmaceutical and research organizations.

Molecular Modeling

The molecular modeling segment is expected to grow at the fastest CAGR as drug developers increasingly rely on simulation tools to predict molecular interactions, optimize lead compounds, and reduce dependence on costly laboratory experiments. These platforms help shorten discovery timelines, improve candidate accuracy, and support structure-based drug designs, driving higher adoption across pharmaceutical and biotechnology companies during the forecast period.

| Segments | Shares % |

| Discovery Informatics | 68% |

| Biocontent Management | 32% |

How the Discovery Informatics Segment Dominated the Drug Discovery Informatics Market in 2025?

The discovery informatics segment dominated the market by 68% shares in 2025 due to its critical role in managing and analyzing a large volume of biological and chemical data during early-stage research. These tools support target identification, hit-to-lead analysis, and compound optimization, enabling faster decision-making reduces R&D risks, and improving productivity for pharmaceutical and biotechnology companies.

Bigcontent Management

The bigcontent management segment is expected to grow at the fastest CAGR as drug discovery generates rapidly increasing volumes of complex research data documents and experimental records. These solutions enable efficient data storage, organization, retrieval, and regulatory compliance, while supporting collaboration across the research team, making them essential for streamlined workflows and improved knowledge management during the forecast period.

| Segments | Shares % |

| Pharmaceutical & Biotechnology Companies | 58% |

| CROs & CMOs | 24% |

| Academic & Research Institutes | 18% |

Why the Pharmaceutical & Biotechnology Companies Segment Dominated the Drug Discovery Informatics Market?

The pharmaceutical & biotechnology companies segment dominated the market by 58% shares due to their heavy investment in drug discovery R&D, and strong need to manage complex discovery data. These organizations widely adopt informatics tools to streamline workflows, improve target identification, reduce development timelines, and enhance success rates, making them the primary end users of advanced drug discovery informatics solutions.

Academic & Research Institutes

The academic & research institutes segment is expected to grow at the fastest CAGR due to increasing government funding, rising research collaborations, and expanding focus on basic and translational drug discovery. These institutions are adopting drug discovery informatics tools to manage large research datasets, support hypothesis-driven studies, and accelerate early-stage innovation, driving strong growth during the forecast period.

")

North America dominated the global market by 41% share in 2025 due to strong pharmaceutical and biotechnology presence, high R&D investments, and early adoption of advanced informatics solutions. This region benefits from robust research infrastructure, supportive regulatory frameworks, and extensive collaboration between industry and academic institutions, driving sustained demand for drug discovery informatics platforms.

U.S. Market Trends

The U.S. captured the largest revenue share in 2025 due to its strong concentration of pharmaceutical and biotechnology companies and substantial spending on drug research. Advanced research infrastructure, widespread adoption of informatics platforms, and active collaboration between industry and research further supported high market revenue and sustained leadership in drug discovery informatics.

Asia Pacific is anticipated to grow by 24% share at the fastest CAGR due to rising pharmaceutical R&D investments, expanding biotechnology sectors, and increasing adoption of digital research tools. Growing government support, improving research infrastructure, and a large talent pool are encouraging drug discovery activities, boosting demand for informatics solutions across emerging and developed economies in the region.

India Market Trends

India is anticipated to grow at a rapid CAGR due to increasing pharmaceutical R&D activities, a strong generic drug manufacturing base, and rising investments in biotechnology. Growing government support, expanding research collaborations, cost-effective operations, and increasing adoption of digital informatics tools are accelerating drug discovery efforts, driving strong market growth across the country during the forecast period.

Europe is expected to grow by 28% share at a notable CAGR during the forecast period due to strong pharmaceutical research capabilities, increasing focus on innovative drug development, and supportive regulatory initiatives. Rising investment in life sciences, expanding public-private research collaborations, and growing adoption of advanced informatics platforms across biotech hubs are driving steady demand for drug discovery informatics solutions across the region.

UK Market Trends

The UK is anticipated to grow at a rapid CAGR due to its strong pharmaceutical and biotechnology ecosystems, expanding research and development activities, and robust academic-industry collaborations. Increasing government funding, a focus on innovation in drug discovery, and growing adoption of advanced informatics platforms are accelerating research efficiency, supporting sustained market growth during the forecast period.

|

Ecosystem Category

|

Market Participants / Explanation |

| Technology Providers | Companies providing AI, computational biology, analytics, and research infrastructure for drug discovery workflows. Examples include IBM, Microsoft, and specialized life science technology providers. |

| Product Manufacturers | Companies developing commercial drug discovery informatics platforms, databases, simulation tools, and research software. |

| Service Providers | Organizations offering digital transformation, data analytics, informatics consulting, and laboratory data management services. |

| Platform Providers | Cloud-based and enterprise platforms supporting molecular data management, compound libraries, AI-based discovery, and collaboration. |

| CROs/CDMOs | Research organizations integrating informatics tools into discovery, screening, and preclinical development services. |

| Software Vendors | Specialized vendors offering cheminformatics, bioinformatics, modeling, simulation, and laboratory informatics solutions. |

| Research Institutions | Universities, government research centers, and biotechnology research organizations using informatics platforms for discovery programs. |

| End-User Industries | Pharmaceutical, biotechnology, academic research, precision medicine, and healthcare innovation sectors. |

R&D

Clinical Trials

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 56% | 29% | 15% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Dassault Systèmes | Vélizy-Villacoublay, France | France | Global leader in scientific software with strong presence in life sciences and drug discovery workflows. | BIOVIA Discovery Studio, molecular modeling, simulation, scientific collaboration platforms |

| Thermo Fisher Scientific | Waltham, Massachusetts, U.S. | United States | Major life sciences technology company supporting research informatics and laboratory workflows. | Digital science platforms, research data solutions, informatics systems |

| Certara | Princeton, New Jersey, U.S. | United States | Specialized leader in biosimulation and model-based drug development informatics. | D360™, Phoenix®, biosimulation and pharmacology modeling platforms |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Collaborative Drug Discovery, Inc. | Burlingame, California, U.S. | United States | Specialized drug discovery informatics provider focused on collaborative research data management. | CDD Vault, chemical and biological data management |

| Schrödinger | New York City, New York, U.S. | United States | Leading computational chemistry company supporting AI-driven drug discovery. | Molecular modeling, computational chemistry software |

| RevVity | Waltham, Massachusetts, U.S. | United States | Provides life science software and research informatics solutions. | Signals Research Suite, scientific data management |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| BIOVIA | San Diego, California, U.S. | United States | Specialized scientific informatics provider focused on molecular discovery workflows. | Discovery Studio, Pipeline Pilot |

| Aqemia | Paris, France | France | AI-native drug discovery company using computational approaches. | AI drug discovery platform, molecular design |

| Exscientia | Oxford, England, U.K. | United Kingdom | AI-driven drug discovery company using computational design technologies. | AI drug design platform |

Strengths

Weaknesses

Opportunities

Threats

By Service

By Application

By End Use

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar