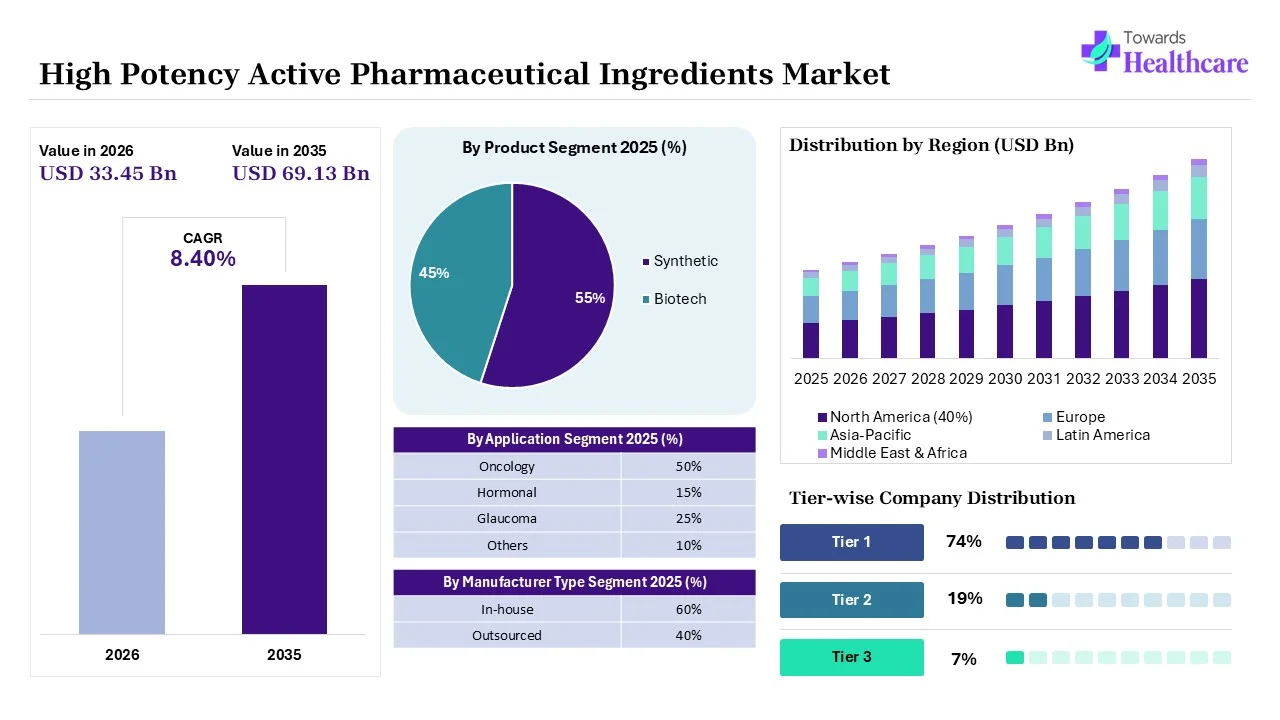

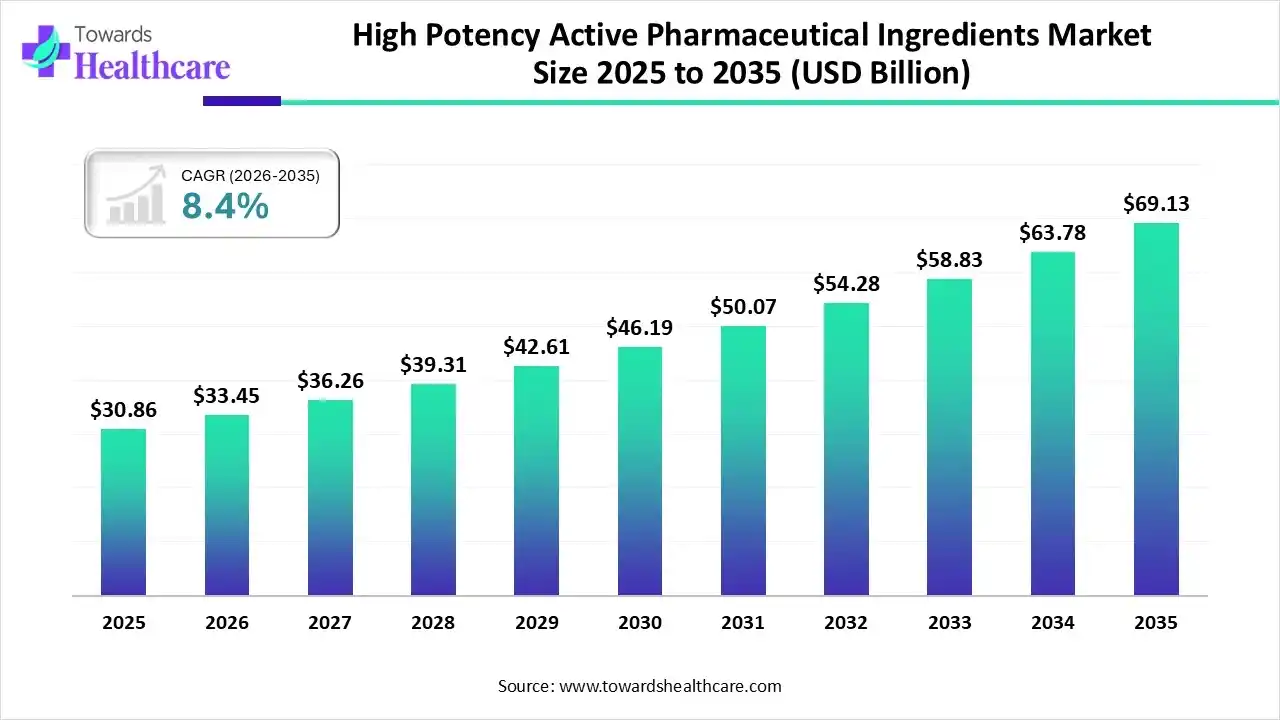

The global high potency active pharmaceutical ingredients market size was estimated at USD 30.86 billion in 2025 and is predicted to increase from USD 33.45 billion in 2026 to approximately USD 69.13 billion by 2035, expanding at a CAGR of 8.4% from 2026 to 2035.

The market is growing steadily, driven by rising demand for oncology, hormone, and targeted therapies, along with increased outsourcing to specialized CDMOs and stricter regulatory compliance requirements.

High-potency active pharmaceutical ingredients (HPAPIs) are highly potent drug substances effective at very low doses, requiring specialized handling, manufacturing, and containment due to their toxicity and pharmacological activity. The high potency active pharmaceutical ingredients market is expanding due to the rising prevalence of targeted and precision therapies, and strong growth in oncology drug pipelines. Advances in containment technologies, greater outsourcing to specialized CDMOs, and stricter regulatory standards further support market growth by ensuring a safe, scalable, and compliant HPAPI market.

For Instance,

Artificial intelligence can transform the high potency active pharmaceutical ingredients market by accelerating drug discovery, optimizing process development, and improving yield prediction for complex, high-potency compounds. AI-driven analytics enable better risk assessment, real-time quality monitoring, and faster scale-up, while automation and predictive maintenance enhance safety, regulatory compliance, and cost efficiency across HPAPI manufacturing and supply chains.

| Key Elements | Scope |

| Market Size in 2026 | USD 33.45 Billion |

| Projected Market Size in 2035 | USD 69.13 Billion |

| CAGR (2026 - 2035) | 8.4% |

| Leading Region | North America by 40% |

| Key Applications | Oncology drugs, antibody-drug conjugates (ADCs), targeted cancer therapies, hormone treatments, immunology drugs, cardiovascular drugs, CNS therapies |

| Primary End Users | Pharmaceutical companies, biotechnology companies, oncology drug developers, CROs, CDMOs, research laboratories |

| Key Growth Drivers | Rising cancer incidence, expansion of targeted therapies, growth of ADC pipelines, outsourcing of HPAPI manufacturing, increasing investment in oncology R&D |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By Manufacturer Type, By Drug Type, By Application, By Region |

| Top Key Players | BASF SE, CordenPharma, BristolMyers Squibb, CARBOGEN AMCIS AG, Pfizer, Inc., Boehringer Ingelheim, Dr. Reddy’s Laboratories |

By Product Insights

By Product Insights| Segments | Shares % |

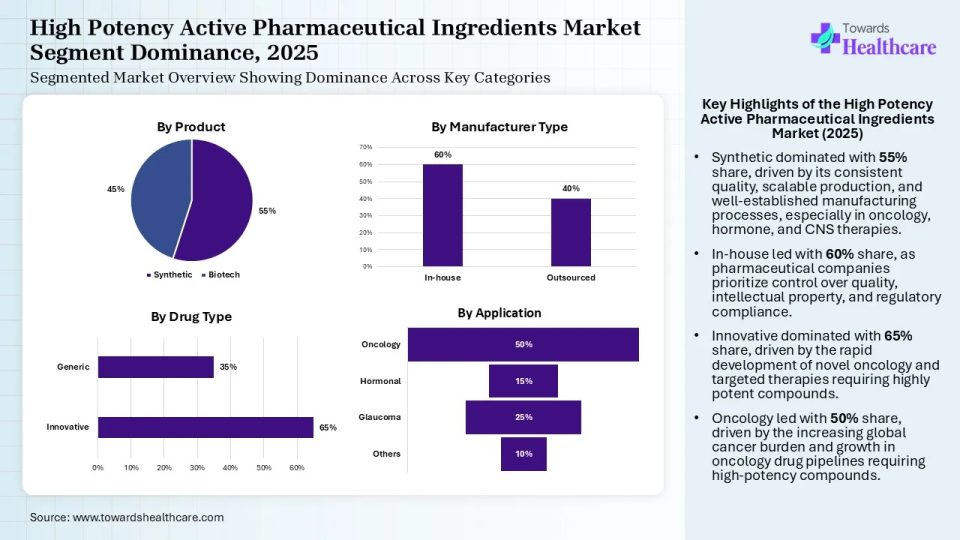

| Synthetic | 55% |

| Biotech | 45% |

Explanation

Why Did the Synthetic Segment Dominate in the Market in 2025?

The synthetic segment dominated the high potency active pharmaceutical ingredients market with a share of 55% during the forecast period due to its wide use in oncology, hormone, and CNS therapies. Synthetic HPAPIs offer consistent quality, scalable production, and well-established manufacturing processes. Their compatibility with advanced chemical synthesis and strong regulatory acceptance further supported higher adoption compared to biotech-derived alternatives.

Biotech

The biotech segment is expected to grow at the fastest CAGR during the forecast period due to increasing development of biologics, antibody drug conjugates, and targeted therapies. Rising investments in biotechnology, advances in cell and gene engineering, and growing demand for precision oncology treatment are accelerating adoption. Additionally, strong clinical pipelines and improved bioprocessing technologies are supporting the rapid commercialization of biotech-based HPAPIs.

| Segments | Shares % |

| In-house | 60% |

| Outsourced | 40% |

Explanation

How the In-house Segment Dominated the Market in 2025?

The in-house segment dominated the high potency active pharmaceutical ingredients market with a share of 60% in 2025 as large pharmaceutical companies prioritize control over quality, intellectual property, and regulatory compliance. In-house production enables better process optimization, secure handling of high-potency compounds, and reliable supply for oncology and chronic disease pipelines, reducing dependency on external manufacturers.

Outsourced

The outsourced segment is expected to grow at the fastest CAGR during the forecast period as pharmaceutical companies seek efficiency and faster time-to-market. Specialized CDMOs offer advanced containment infrastructure, regulatory expertise, and scalable HPAPI capabilities. The growing complexity of potent molecules, coupled with rising clinical pipelines and limited in-house capacity, is further accelerating outsourced adoption.

| Segments | Shares % |

| Innovative | 65% |

| Generic | 35% |

Explanation

Why the Innovative Segment Dominated the Market?

The innovative segment dominated the high potency active pharmaceutical ingredients market share of 65% due to the rapid development of novel oncology and targeted therapies. These drugs require highly potent compounds to deliver therapeutic effects at low doses. Strong R&D investments, expanding clinical pipelines, and increased approvals for first-in-class and specialty medicines further drove demand for innovative HPAPIs.

Generic

The generic segment is expected to grow at the fastest CAGR during the forecast period due to patent expirations of several high-potency oncology and hormone drugs. Rising demand for cost-effective therapies, increasing cancer prevalence, and wider access to affordable medicines are driving generic adoption. Additionally, improving manufacturing capabilities and regulatory approvals for generic HPAPIs are supporting rapid market expansion.

| Segments | Shares % |

| Oncology | 50% |

| Hormonal | 15% |

| Glaucoma | 25% |

| Others | 10% |

Explanation

Why Did the Oncology Segment Dominate in the Market in 2025?

The oncology segment led the high potency active pharmaceutical ingredients market with share of 50% in 2025 due to the rising global cancer burden and strong growth in oncology drug pipelines. Many cancer therapies require highly potent compounds to achieve targeted efficacy at low doses. Increased approvals of novel anticancer drugs and sustained investment in oncology research further reinforced the market-leading position.

| Year | Oncology Approval (Drug/API) |

| 2024 | Osimertinib with chemotherapy (Tagrisso) |

| Lifileucel (Amtagvi) | |

| Tepotinib (Tepmetko) | |

| Irinotecan liposome (Onivyde combo) | |

| Erdafitinib (Balversa) | |

| Nivolumab + hyaluronidasenvhy (Opdivo Qvantig) | |

| Encorafenib + cetuximab + mFOLFOX6 | |

| 2025 | Acalabrutinib + bendamustine + rituximab (Calquence combo) |

| Brentuximab vedotin + lenalidomide & rituximab (Adcetris combo) | |

| Vimseltinib (Romvimza) | |

| Pembrolizumab + chemo (Keytruda combos) |

Glaucoma

The glaucoma segment is expected to grow at the fastest CAGR during the forecast period due to the rising aging population and increasing prevalence of eye disorders worldwide. High-potency APIs are widely used in ophthalmic drugs to achieve efficacy at low doses. Advancements in targeted eye therapies, improved drug delivery, and growing awareness about early drug delivery systems and growing awareness about early glaucoma treatment are further accelerating market growth.

")

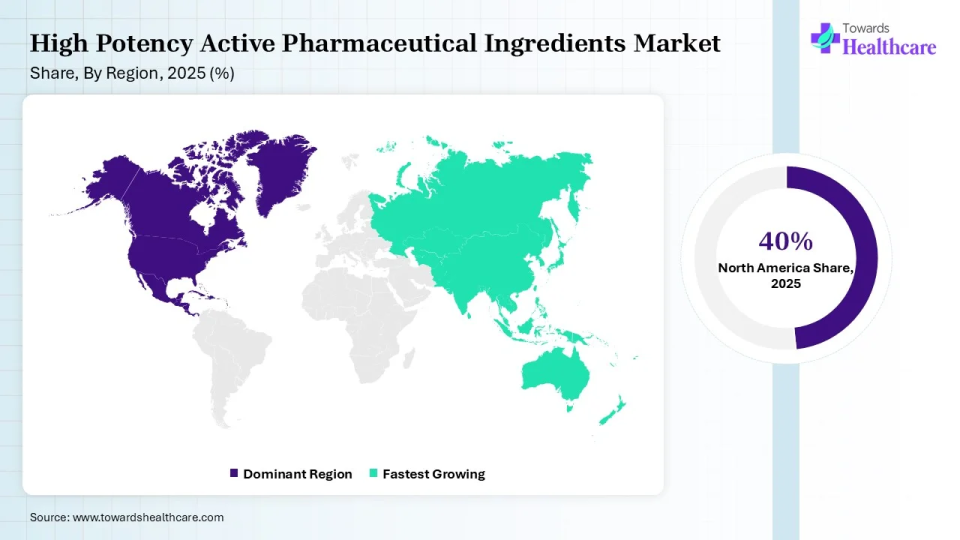

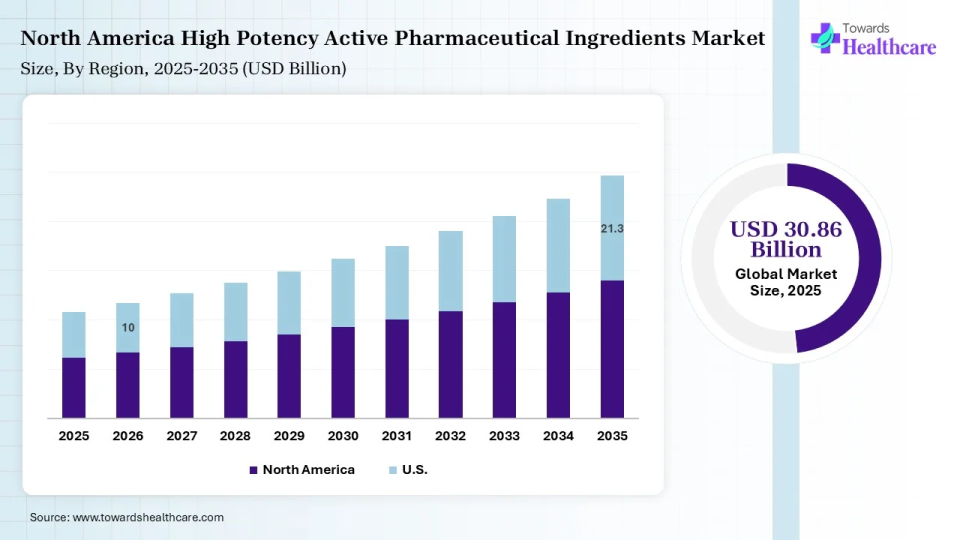

North America dominated the global high potency active pharmaceutical ingredients market by 40% share in 2025 due to strong pharmaceutical R&D investments, a robust oncology drug pipeline, and the presence of leading pharma and CDMO players. Advanced manufacturing infrastructure, strict regulatory frameworks ensuring quality and safety, and high adoption of innovative and targeted therapies strengthened the region's market leadership.

North America dominated the global high potency active pharmaceutical ingredients market by 40% share in 2025 due to strong pharmaceutical R&D investments, a robust oncology drug pipeline, and the presence of leading pharma and CDMO players. Advanced manufacturing infrastructure, strict regulatory frameworks ensuring quality and safety, and high adoption of innovative and targeted therapies strengthened the region's market leadership.

Key Factors Behind the U.S. Market Leadership in 2025

The U.S. captured a revenue share of the high potency active pharmaceutical ingredients market in 2025 due to its strong concentration of leading pharmaceutical companies, extensive oncology and specialty drug pipelines, and high R&D spending. Advanced manufacturing capabilities, early adoption of innovative therapies, favorable regulatory pathways, and the presence of major HPAPI-focused CDMOs further supported the country’s market leadership.

Asia Pacific is anticipated to grow by 21% share at the fastest CAGR during the forecast period due to expanding pharmaceutical manufacturing capacity, rising cancer prevalence, and increasing demand for affordable therapies. Growing investment in API production, cost-efficient manufacturing, and rapid expansion of CDMOs in countries like China and India are accelerating market growth. Supportive government initiatives and improving regulatory frameworks further enhance the region's growth potential.

India emerging as a High-Growth HPAPI Powerhouse

India is anticipated to grow at a rapid CAGR during the forecast period due to its strong position as a global API manufacturing hub and expanding capabilities in high-potency compounds. Rising investment in oncology drug production, increasing outsourcing from global pharmaceutical companies, and cost-efficient manufacturing are key drivers. Additionally, government support for pharmaceutical exports, improving regulatory compliance, and the growing presence of HPAPI-focused CDMOs are accelerating market growth.

Europe is anticipated by 30% share to grow at a notable CAGR during the forecast period due to increasing investments in oncology and speciality drug development, advanced pharmaceutical infrastructure, and stringent regulatory standards that ensure high-quality HPAPI production. The presence of leading pharmaceutical companies, rising adoption of innovative therapies, and expansion of contract manufacturing organizations further support the region’s steady market growth.

UK Set to Achieve Rapid Growth in the HPAPI Market

The Uk is anticipated to grow at a rapid CAGR during the forecast period due to its strong pharmaceutical R&D ecosystems, increasing focus on oncology and specialty therapies, and well-established HPAPI manufacturing capabilities. Supportive government policies, expansion of contract development and manufacturing organizations, and growing adoption of innovative high-potency drugs are driving the country’s accelerated market growth.

|

Category

|

Key Players / Explanation |

| Technology Providers | Companies providing containment systems, isolators, specialized reactors, filtration, and safety technologies for HPAPI manufacturing. Examples include GEA, Dec Group, Bosch Packaging Technology. |

| Product Manufacturers | Pharmaceutical companies developing and producing HPAPI-based drugs, especially oncology and targeted therapies. |

| Service Providers | Specialized pharmaceutical manufacturing partners offering HPAPI development, analytical testing, and production services. |

| Platform Providers | Companies providing drug development platforms, ADC technologies, formulation technologies, and analytical platforms. |

| CROs/CDMOs | Major ecosystem segment providing HPAPI synthesis, scale-up, clinical manufacturing, and commercial production. |

| Software Vendors | Digital manufacturing, quality management, laboratory information systems, and regulatory software providers supporting HPAPI operations. |

| Research Institutions | Universities and cancer research organizations developing highly potent therapies and drug delivery technologies. |

| End-User Industries | Pharmaceutical, biotechnology, oncology therapeutics, specialty pharma, and contract manufacturing sectors. |

R&D

Clinical Trials

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 74% | 19% | 7% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Lonza Group | Basel, Switzerland | Switzerland | One of the world's largest CDMO companies with strong HPAPI manufacturing capabilities and oncology drug expertise. | HPAPI development, ADC manufacturing, highly potent drug substance production |

| Thermo Fisher Scientific | Waltham, Massachusetts, USA | USA | Global pharmaceutical services leader with extensive HPAPI CDMO capabilities through Patheon. | HPAPI development, clinical manufacturing, commercial production |

| CordenPharma | Plankstadt, Germany | Germany | Specialized CDMO with strong presence in highly potent compounds and oncology manufacturing. | HPAPI API manufacturing, peptide APIs, oncology APIs |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Cambrex Corporation | East Rutherford, New Jersey, USA | USA | Specialized API manufacturer with strong capabilities in potent compounds. | HPAPI development, API manufacturing, analytical services |

| Piramal Pharma Solutions | Mumbai, Maharashtra, India | India | Global CDMO offering high-potency API development and manufacturing. | HPAPI synthesis, oncology API services, ADC services |

| Recipharm | Stockholm, Sweden | Sweden | Global CDMO with expertise in potent pharmaceutical manufacturing. | HPAPI manufacturing, sterile and oral dosage services |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Nitto Denko Avecia Pharma Services | Milford, Massachusetts, USA | USA | Specialized CDMO focusing on complex pharmaceutical molecules. | HPAPI manufacturing, oligonucleotide and specialty API services |

| WuXi AppTec | Shanghai, China | China | Large pharmaceutical services company with API development and manufacturing capabilities. | HPAPI process development, API production |

| Hovione | Loures, Portugal | Portugal | Specialist in inhalation technology and complex API manufacturing. | High-potency APIs, particle engineering |

Strengths

Weaknesses

Opportunities

Threats

By Product

By Manufacturer Type

By Drug Type

By Application

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar