Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

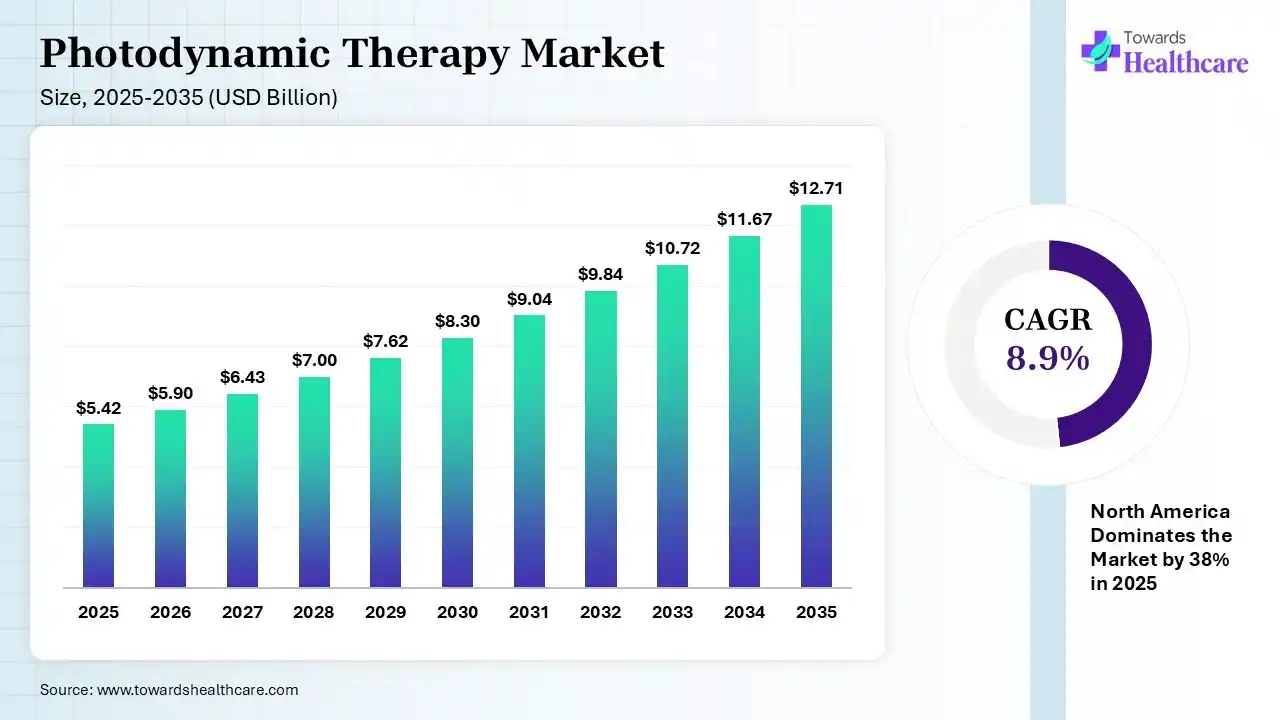

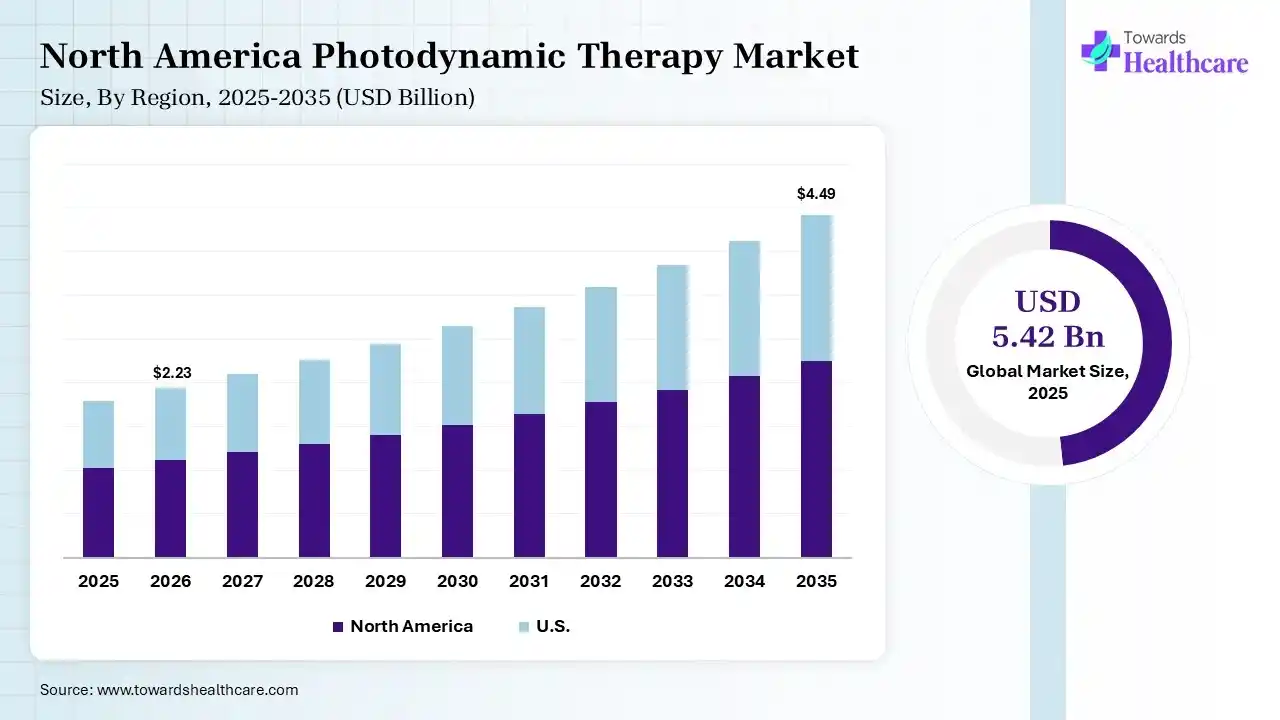

The global photodynamic therapy market size was estimated at USD 5.42 billion in 2025 and is predicted to increase from USD 5.9 billion in 2026 to approximately USD 12.71 billion by 2035, expanding at a CAGR of 8.9% from 2026 to 2035. The market is witnessing steady growth due to increasing cases of cancer and skin disorders, along with rising preference for minimally invasive and targeted treatment options. Advancements in photosensitizing agents and light-based technologies are further driving its adoption across oncology, dermatology, and often clinical applications.

")

Photodynamic therapy is a medical treatment that uses a light-activated drug and a specific wavelength of light to destroy abnormal or cancerous cells. The photodynamic therapy market is expanding due to the rising incidence of cancer and skin diseases, along with increasing demand for minimally invasive and targeted treatments. Advancements in photosensitizing agents, improved light delivery systems, and growing awareness of non-surgical treatment options are further boosting adoption. Its effectiveness in reducing damage to healthy tissues also supports wider clinical acceptance.

The photodynamic therapy market is expanding as healthcare providers increasingly adopt minimally invasive treatments for cancer, dermatological disorders, and ophthalmic diseases. Growing awareness of targeted therapies and continuous improvements in photosensitizing agents and light delivery systems are supporting wider clinical use. Research is exploring new applications in antimicrobial therapy and combination treatments, creating additional growth opportunities. Companies are investing in advanced devices, innovative drug formulations, and clinical studies to improve treatment outcomes and patient safety. Strategic collaborations between pharmaceutical companies, medical device manufacturers, and research institutions are accelerating product development. The competitive landscape features established healthcare companies, specialized therapy developers, and emerging innovators focused on technology advancement, product expansion, regulatory approvals, and partnerships to strengthen their global presence.

AI can significantly enhance the market by improving patient selection, optimizing light dosage, and enabling precise treatment planning. It supports real-time monitoring and predictive outcomes, increasing treatment effectiveness and safety. Additionally, AI-driven drug discovery accelerates the development of advanced photosensitizers, while automation and data analytics streamline clinical workflows and expand adoption across healthcare settings.

| Table | Scope |

| Market Size in 2026 | USD 5.9 Billion |

| Projected Market Size in 2035 | USD 12.71 Billion |

| CAGR (2026 - 2035) | 8.9% |

| Leading Region | North America by 38% |

| Key Applications | Cancer Treatment, Actinic Keratosis, Basal Cell Carcinoma, Head & Neck Cancer, Esophageal Cancer, Lung Cancer, Acne Treatment, Age-Related Macular Degeneration (AMD) |

| Primary End Users | Hospitals, Cancer Centers, Dermatology Clinics, Ophthalmology Clinics, Ambulatory Surgical Centers, Research Institutes |

| Key Challenges | High treatment costs, limited reimbursement in some regions, variable treatment efficacy, requirement for specialized equipment and trained professionals |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Application, By End User, By Drug Type, By Route of Administration, By Region |

| Top Key Players | Galderma S.A., Sun Pharmaceutical Industries Ltd., Biofrontera, Novartis AG, Bausch Health Companies Inc., Quest Pharmatech Inc. |

")

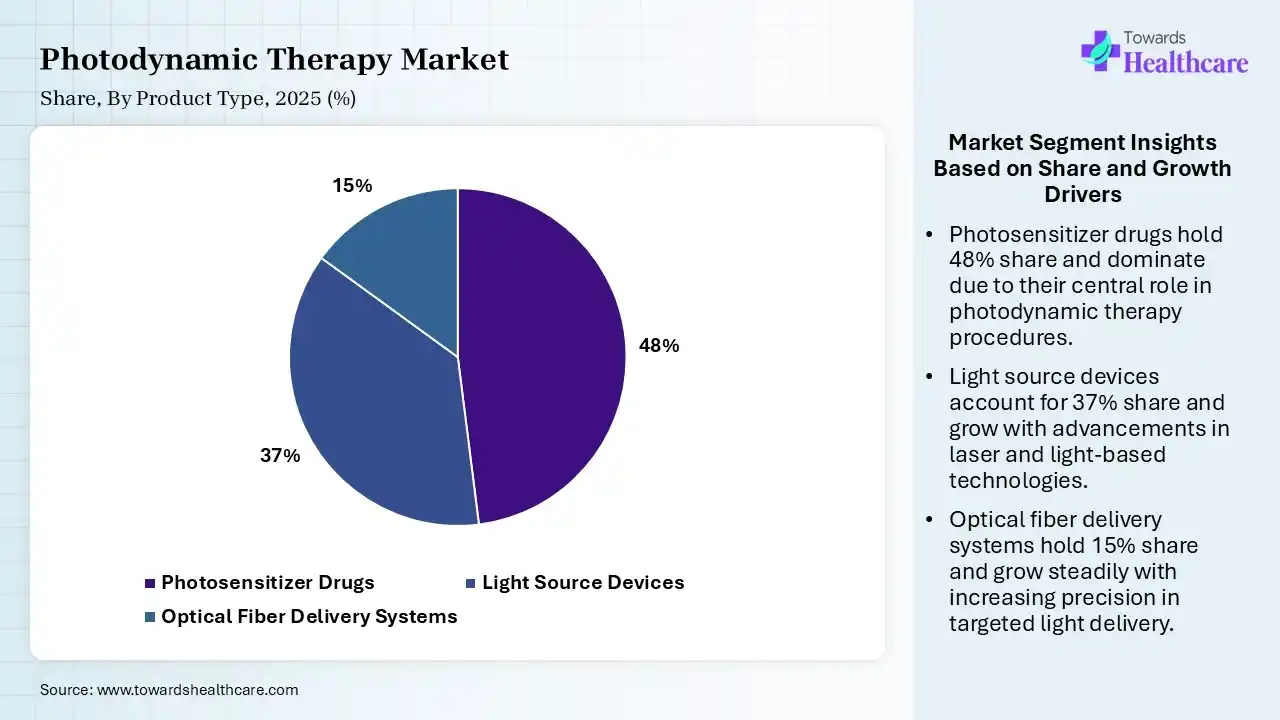

| Segment | Share 2025 (%) |

| Photosensitizer Drugs | 48% |

| Light Source Devices | 37% |

| Optical Fiber Delivery Systems | 15% |

The Photosensitizer Drugs Segment Dominated the Market in 2025

The photosensitizer drugs segment dominated the photodynamic therapy market with a revenue share of 48% in 2025 due to their essential role in initiating the therapeutic effect by selectively accumulating in abnormal cells. Their continuous advancements, improved efficacy, and expanding clinical applications in oncology and dermatology drive strong demand. Additionally, increasing approvals and availability of novel photosensitizers further support their widespread use, making them a critical component of photodynamic therapy procedures.

The light source devices segment held the second-largest share of 37% of the market in 2025 and is expected to grow at the fastest CAGR of 9.3% in the market during the forecast period, as they are essential for activating photosensitive drugs and ensuring effective treatment outcomes. Growing adoption of advanced light technologies, including lasers and LEDs, enhances precision and safety. Increasing availability of portable and cost-effective devices, along with rising clinical use across dermatology and oncology, further drives the demand for these systems in photodynamic therapy procedures.

The optical fiber delivery systems segment held a 15% of the photodynamic therapy market share in 2025 due to its ability to deliver light precisely to internal or hard-to-reach tissues, improving treatment accuracy and effectiveness. Increasing minimally invasive procedures and expanding applications in oncology support its demand. Technological advancements in flexible and efficient fiber systems, along with rising preference for targeted therapies, further contribute to the segment’s steady growth in photodynamic therapy.

")

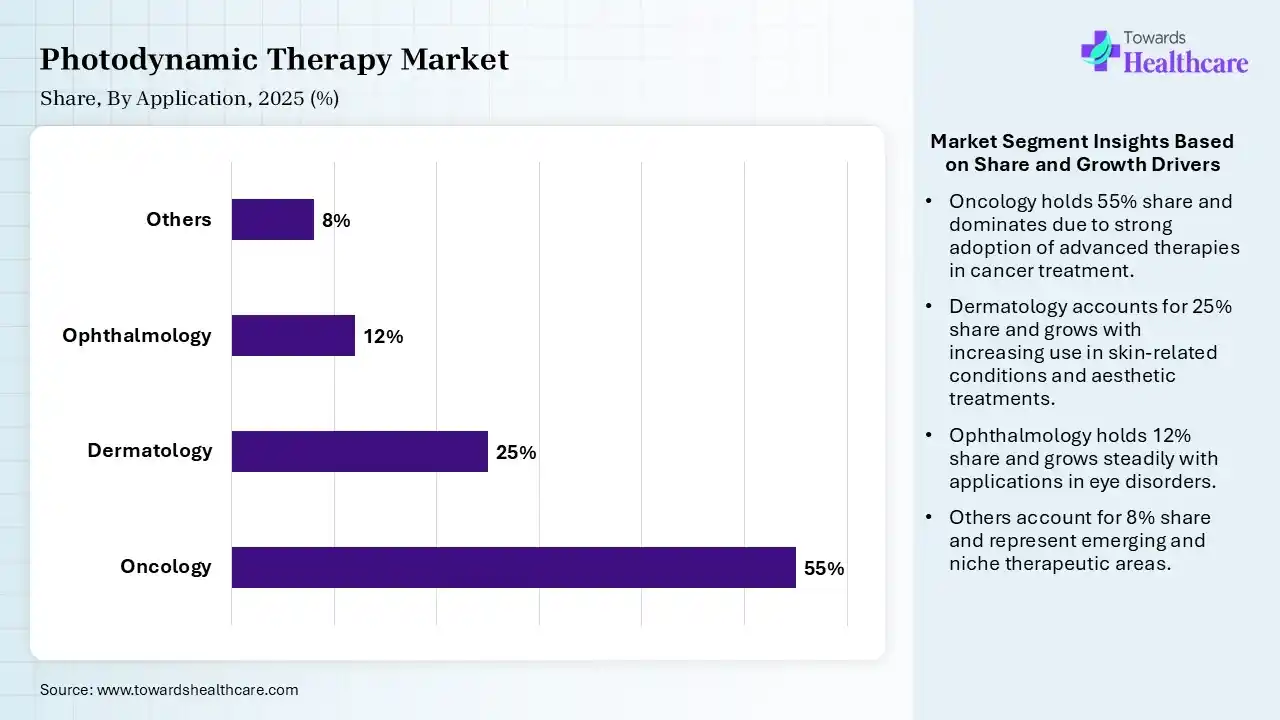

| Segment | Share 2025 (%) |

| Oncology | 55% |

| Dermatology | 25% |

| Ophthalmology | 12% |

| Others | 8% |

The Oncology Segment Led the Market in 2025 with the Largest Share

The oncology segment held a dominant share of 55% in 2025 due to the rising global burden of cancer and the growing need for targeted, minimally invasive treatments. Photodynamic therapy offers effective tumor destruction with limited damage to surrounding healthy tissue, making it suitable for early-stage and localized cancers. Increasing clinical adoption, ongoing research, and expanding approvals for cancer indication further strengthened its leading position in the market.

The dermatology segment held the second-largest share of 25% of the photodynamic therapy market in 2025 and is expected to grow at the fastest CAGR of 9.8% in the market during the forecast period due to the high prevalence of skin conditions such as acne, psoriasis, and precancerous lesions. Photodynamic therapy is widely preferred in dermatology for its non-invasive nature, cosmetic benefits, and minimal screening. Increasing demand for aesthetic treatments, growing awareness, and the availability of outpatient procedures further support its strong adoption in dermatological applications.

The ophthalmology segment held 12% of the photodynamic therapy market share in 2025 due to increasing cases of age-related macular degeneration and other disorders. Photodynamic therapy offers a targeted, minimally invasive approach to managing abnormal blood vessel growth while preserving surrounding tissues. Rising awareness, improving clinical outcomes, and expanding use in vision-related conditions, along with advancements in light delivery techniques, are further supporting its adoption in ophthalmic care.

")

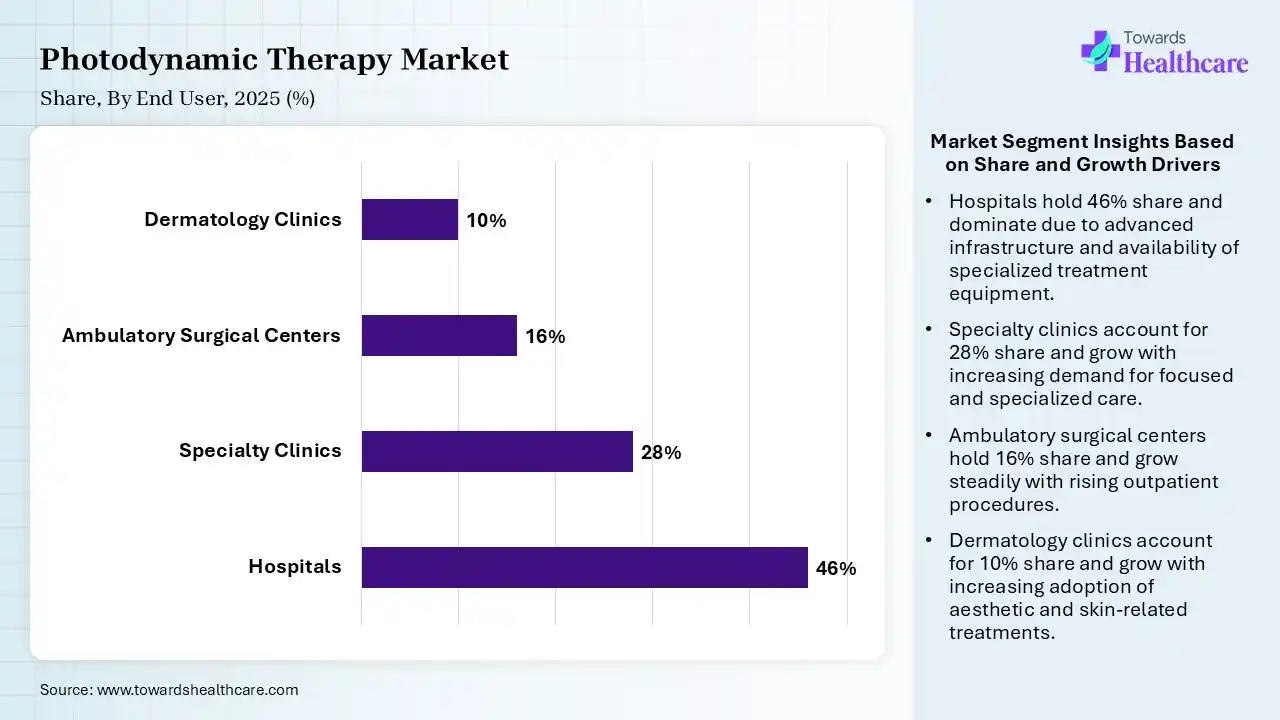

| Segment | Share 2025 (%) |

| Hospitals | 46% |

| Specialty Clinics | 28% |

| Ambulatory Surgical Centers | 16% |

| Dermatology Clinics | 10% |

The Hospitals Segment Led the Market in 2025 with the Largest Share

The hospitals segment held a dominant share of 46% in 2025 due to their advanced infrastructure, availability of specialized equipment, and access to skilled healthcare professionals required for photodynamic therapy procedures. Hospitals handle a higher volume of cancer and complex cases, supporting greater treatment adoption. Additionally, better reimbursement policies, multidisciplinary care, and the ability to manage complications make hospitals the primary choice for photodynamic therapy treatments.

The specialty clinics segment held the second-largest share of 28% of the photodynamic therapy market in 2025 and is expected to grow at the fastest CAGR of 9.4% in the market during the forecast period due to its strong focus on dermatology and oncology procedures, where photodynamic therapy is commonly used. These clinics provide efficient, cost-effective outpatient treatments with shorter waiting times. Their access to skilled, specialized, and patient preference for convenient, targeted care settings further contribute to the growing adoption of photodynamic therapy in specialty clinics.

The ambulatory surgical centers segment held a 16% of photodynamic therapy market share in 2025 due to the increasing demand for cost-effective, same-day procedures and minimally invasive treatments like photodynamic therapy. These centers offer hospital stays, reduced treatment costs, and faster patient turnaround. Advancements in portable light-based devices and rising preference for outpatient care settings are further encouraging the adoption of photodynamic therapy in ambulatory surgical centers.

The dermatology clinics segment held a 10% of the photodynamic therapy market share in 2025 due to the rising prevalence of skin disorders and increasing demand for aesthetic and non-invasive treatment. Photodynamic therapy is widely used for acne, actinic keratosis, and other skin conditions, offering effective results with minimal downtime. Growing awareness, improved accessibility, and patient preference for specialized skincare services further support the segment’s steady growth.

")

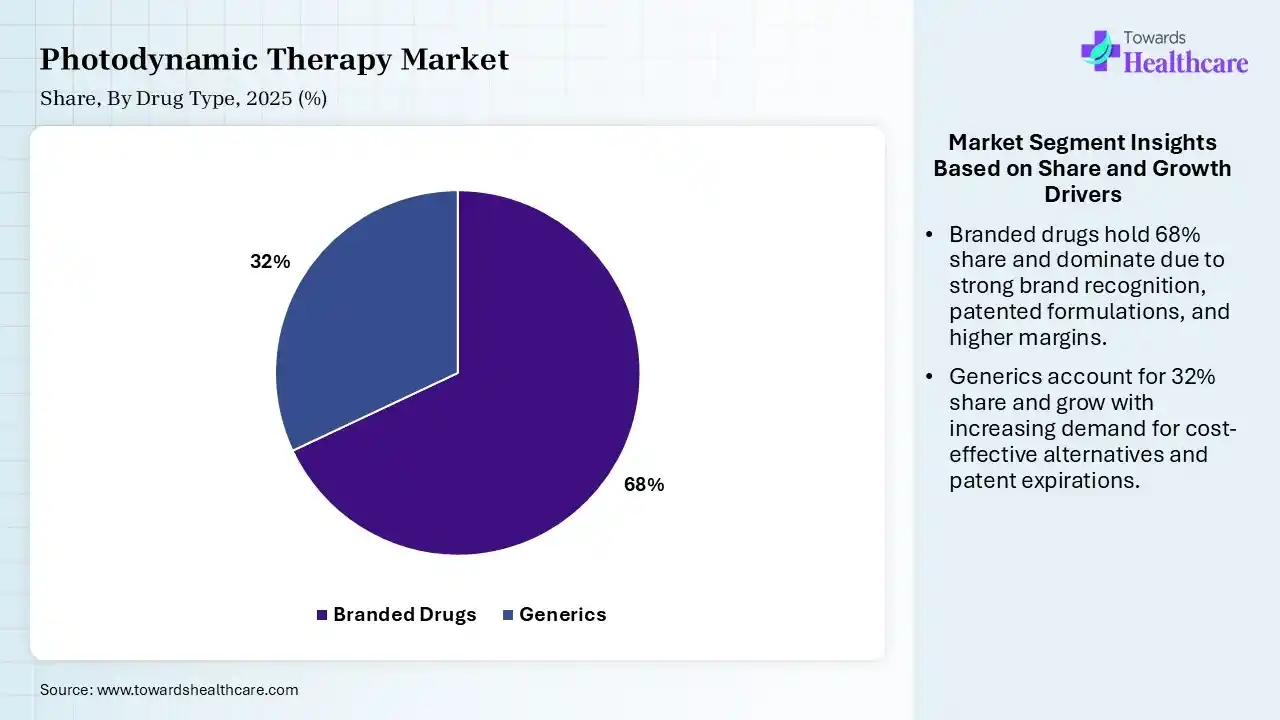

| Segment | Share 2025 (%) |

| Branded Drugs | 68% |

| Generics | 32% |

The Branded Drugs Segment Led the Market in 2025 with the Largest Share

The branded drugs segment led the photodynamic therapy market with a share of 68% in 2025 due to their proven clinical efficacy, strong safety profiles, and established regulatory approvals. Physicians often prefer these drugs for reliable and consistent treatment outcomes in photodynamic therapy. Additionally, continuous innovation, patent protection, and strong marketing by key pharmaceutical companies support their widespread adoption, reinforcing their dominant position over generic alternatives in the market.

The generics segment held the second-largest share of 32% of the photodynamic therapy market in 2025 and is expected to grow at the fastest CAGR of 9.7% in the market during the forecast period due to its cost-effectiveness and increasing availability after patent expirations of branded drugs. The offer comparable therapeutic outcomes, making them attractive for price-sensitive markets and broader patient access. Growing healthcare cost pressures, supportive regulatory pathways, and rising adoption in emerging regions further contribute to the steady demand for generic photosensitizing drugs in photodynamic therapy.

")

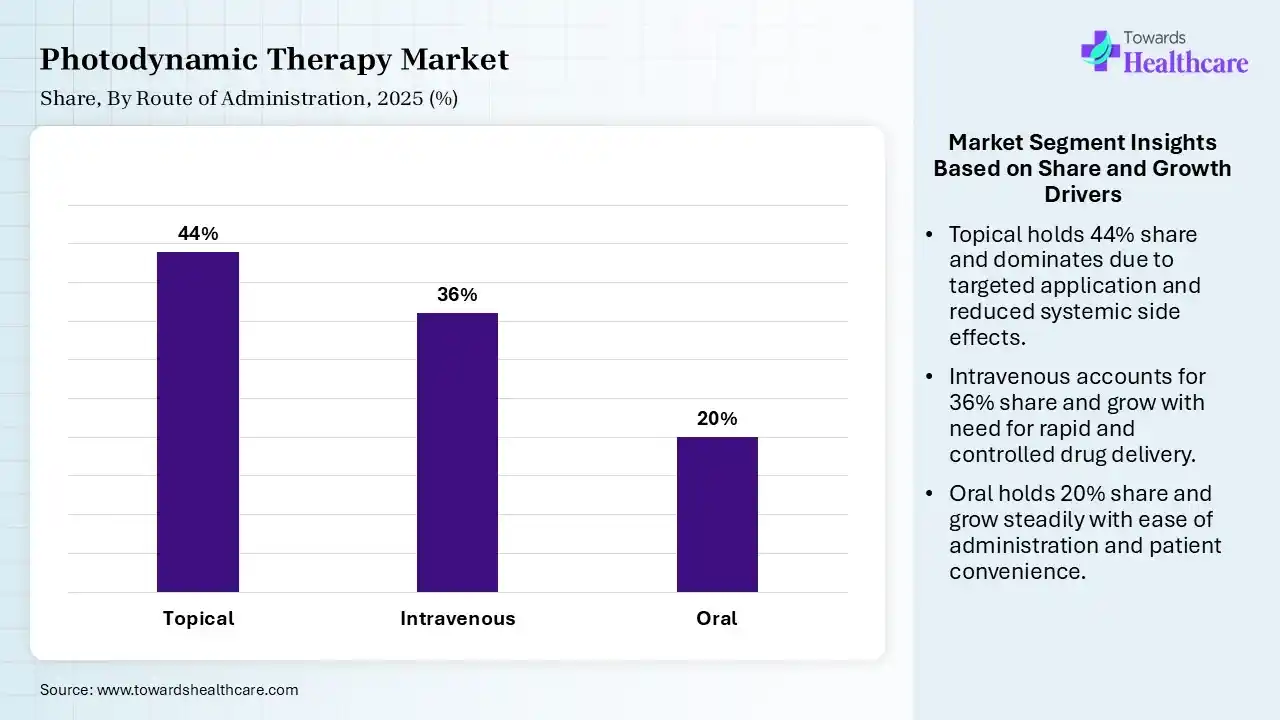

| Segment | Share 2025 (%) |

| Topical | 44% |

| Intravenous | 36% |

| Oral | 20% |

The Topical Segment Led the Market in 2025 with the Largest Share

The topical segment held a dominant share of 44% in 2025 and is expected to grow at the fastest CAGR of 9.2% in the market during the forecast period due to its non-invasive nature, ease of application, and strong patient compliance. It enables targeted treatment with minimal systemic side effects, making it ideal for dermatological conditions. increasing demand for outpatient care, rising aesthetic procedures, and advancements in topical formulations further accelerate its adoption and future growth.

The intravenous segment held 36% of the photodynamic therapy market share in 2025 due to delivering photosensitizing drugs systemically, making it suitable for treating deeper internal tumors. It ensures controlled dosing and higher drug concentration at the target sites, improving treatment effectiveness. Increasing use of oncology, along with advancements in drug formulation and hospital-based procedures, is further supporting the adoption of intravenous administration in photodynamic therapy.

The oral segment held a 20% of the photodynamic therapy market share in 2025 due to its convenience, ease of administration, and high patient compliance compared to invasive methods. It allows systemic delivery of photosensitizing agents, making it suitable for certain internal conditions. Growing preference for at-home or less. Complex treatment options, along with advancements in oral drug formulations and improved bioavailability, are further supporting its increasing adoption in photodynamic therapy.

")

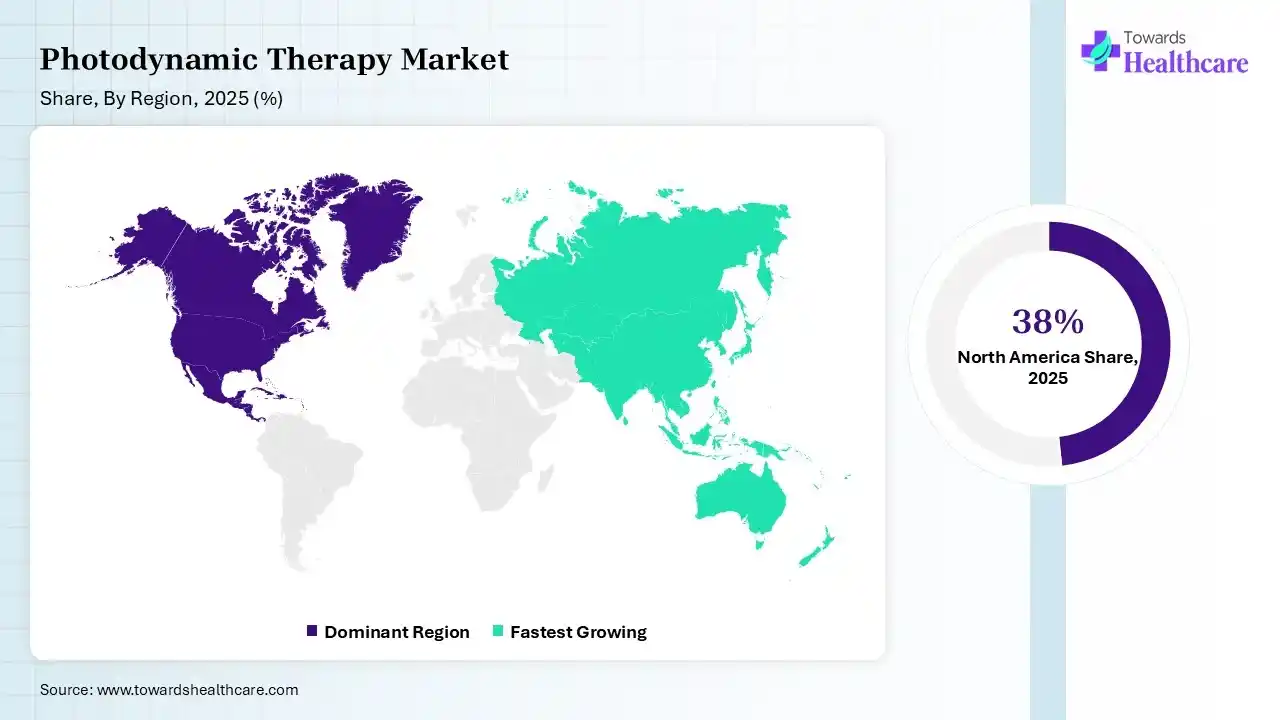

North America dominated the global photodynamic therapy market with 38% share in 2025 due to its advanced healthcare infrastructure, high adoption of innovative e-therapies, and strong presence of key market players. Rising prevalence of cancer and skin disorders, along with favorable reimbursement policies, support the widespread use of photodynamic therapy. Additionally, continuous research, early regulatory approvals, and increasing awareness among patients and physicians further strengthened the region’s leading position.

U.S. Market Trends

The U.S. photodynamic therapy market is driven by a high prevalence of cancer and dermatological conditions, along with strong adoption of advanced, minimally invasive treatments. robust healthcare infrastructure, favorable reimbursement policies, and the presence of leading pharmaceutical and medical devices companies support market growth. Continuous clinical research, early technology adoption, and increasing awareness further strengthen the country’s dominant position.

Canada Market Trends

Canada is strengthening its photodynamic therapy market through growing investments in cancer research and advanced healthcare services. Hospitals and research institutions are increasing the use of minimally invasive treatment options for selected cancers and skin disorders. Government support for medical innovation encourages clinical research and technology development. Collaborations between healthcare providers and industry participants continue expanding. Canada offers strong opportunities for companies developing innovative photodynamic therapy products and devices.

Mexico Market Trends

Mexico is gradually expanding its photodynamic therapy market as healthcare facilities improve access to advanced treatment options. Rising awareness of early disease diagnosis and minimally invasive procedures supports market development. Public and private healthcare investments are strengthening medical infrastructure across major cities. International companies are forming partnerships with local distributors and healthcare providers. These developments are improving the availability of photodynamic therapy technologies and expanding treatment opportunities for patients.

Asia Pacific captured 22% of the market share in 2025 and is anticipated to grow at the fastest CAGR of 10.2% in the market due to rising healthcare investment, increasing prevalence of cancer and skin disorders, and improving access to advanced treatments, growing awareness, expanding medical infrastructure, and a large patient population drive demand. Additionally, supportive government initiatives and increasing adoption of minimally invasive therapies further accelerate market growth across emerging economies.

India Market Trends

India is expected to grow at the fastest CAGR in the photodynamic therapy market due to its large patient population, increasing prevalence of cancer and skin disorders, and improving healthcare infrastructure. Rising awareness of minimally invasive treatments, expanding access to advanced technologies, and growing investment in healthcare further drive demand. Additionally, supportive government initiatives and the rapid expansion of specialty clinics contribute to accelerating market growth.

China Market Trends

China is experiencing strong growth in the photodynamic therapy market due to rising healthcare spending and expanding cancer treatment services. Hospitals are adopting advanced medical technologies to improve patient outcomes. Domestic companies are increasing research and developing innovative photodynamic therapy products. Government support for biotechnology and healthcare innovation encourages further investment. China continues attracting international collaborations, creating new opportunities for manufacturers, researchers, and healthcare providers across the country.

Japan Market Trends

Japan remains a key market for photodynamic therapy because of its advanced healthcare system and strong focus on medical innovation. Hospitals continue to adopt modern treatment technologies for cancer and ophthalmic diseases. Research institutions and pharmaceutical companies actively develop improved photosensitizers and treatment devices. Close collaboration between industry and healthcare providers supports clinical adoption. Japan offers a favorable environment for innovation, high-quality care, and continued market development.

| Ecosystem Segment | Key Participants | Role in Market |

| Technology Providers | Biofrontera, Lumibird Medical, Modulight | Develop PDT laser systems, illumination technologies, and treatment platforms |

| Product Manufacturers | Sun Pharmaceutical, Galderma, Biofrontera, Rakuten Medical | Manufacture photosensitizers and PDT treatment products |

| Service Providers | Mayo Clinic, Cleveland Clinic, Memorial Sloan Kettering Cancer Center | Deliver PDT procedures across oncology and dermatology applications |

| Platform Providers | Modulight, Rakuten Medical | Integrated platforms combining drugs, devices, and treatment protocols |

| CROs | ICON plc, Parexel, Syneos Health | Clinical trial management for PDT drug and device development |

| CDMOs | Lonza Group, Catalent, Recipharm | Manufacturing support for photosensitizers and biologics used in PDT |

| Software Vendors | Elekta, Varian Medical Systems | Treatment planning and imaging integration for PDT procedures |

| Research Institutions | National Cancer Institute, Roswell Park Comprehensive Cancer Center, University College London | Clinical research, PDT innovation, translational studies |

| End-User Industries | Oncology, Dermatology, Ophthalmology, Academic Research | Adoption and commercialization of PDT technologies |

R&D

Clinical Trials

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Sun Pharmaceutical Industries Ltd. | Mumbai, Maharashtra | India | Global PDT leader through Levulan franchise | Levulan Kerastick (ALA PDT) |

| Biofrontera AG | Leverkusen, NRW | Germany | Leading dedicated PDT company | Ameluz®, BF-RhodoLED® |

| Galderma SA | Zug | Switzerland | Strong dermatology PDT portfolio | Metvix®, Dermatology PDT solutions |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Rakuten Medical Inc. | San Diego, California | USA | Commercializing photoimmunotherapy technologies | Alluminox™ platform |

| Modulight Corporation | Tampere | Finland | Precision laser systems for PDT | ML7710 PDT platform |

| Steba Biotech N.V. | Luxembourg City | Luxembourg | Developer of Foscan PDT products | Foscan® |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Theralase Technologies Inc. | Toronto, Ontario | Canada | Advanced oncology PDT platform development | Rutherrin® PDT |

| Asieris Pharmaceuticals Co., Ltd. | Shanghai | China | Expanding PDT applications in oncology | APL-1702 PDT |

| Photocure ASA | Oslo | Norway | Light-activated cancer diagnostics and therapy expertise | Hexvix®/Cysview® platform |

Strengths

Weaknesses

Opportunities

Threats

In May 2025, "As physicians, our goal is to put ourselves out of business by treating and curing disease. As a dermatologic surgeon, I prefer to treat AKs before they become skin cancer," said Dermatology Times Editorial Advisory Board Member Aaron Farberg, MD, FAAD, in a recent interview. "The approval of the new illuminator is advancing the technology and treatment of the field therapy of AK's with PDT. It demonstrates a commitment to our field and allows us to best help our dermatology patients.

By Product Type

By Application

By End User

By Drug Type

By Route of Administration

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar