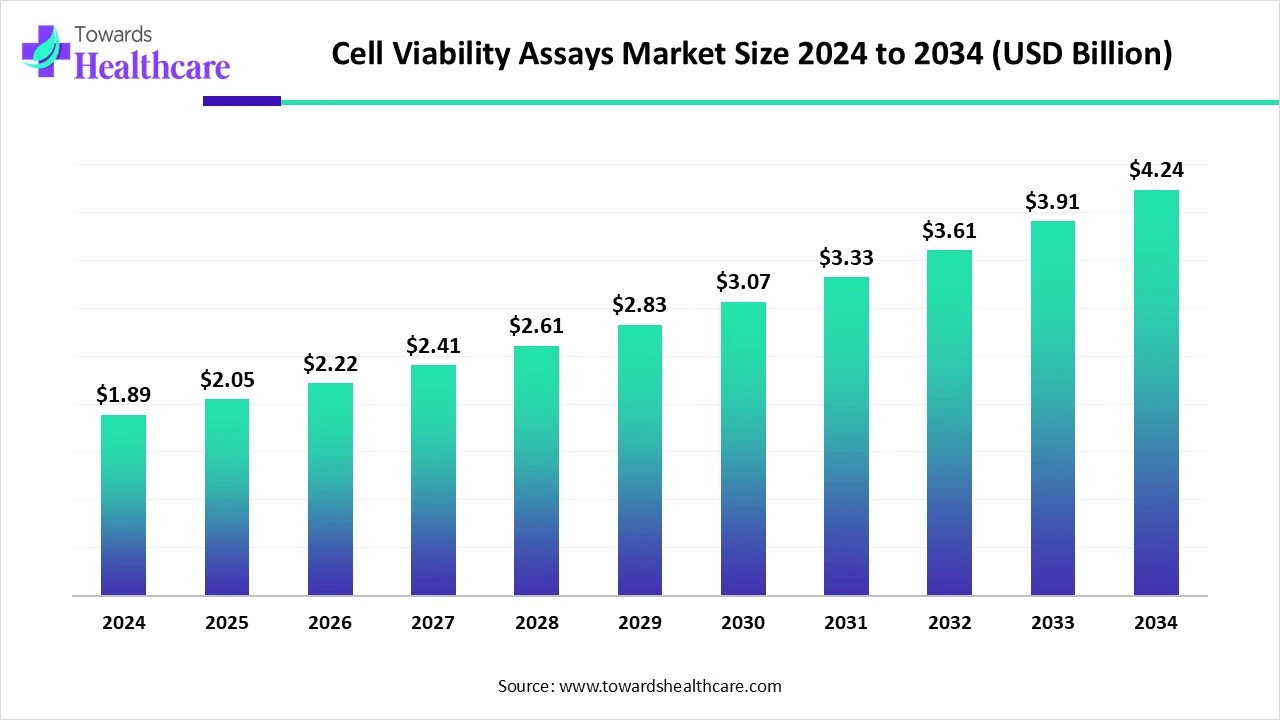

The global cell viability assays market size is calculated at USD 2.05 billion in 2025, grew to USD 2.23 billion in 2026, and is projected to reach around USD 4.66 billion by 2035. The market is expanding at a CAGR of 8.54% between 2026 and 2035.

The cell viability assays market is primarily driven by the growing research and development activities and increasing R&D investments. Several regulatory agencies mandate cytotoxicity tests to assess the toxicity profile of drug products. The rising prevalence of cancer, metabolic disorders, and other disorders facilitates market growth. The future looks promising, driven by automation in cell viability assays and the growing demand for personalized medicines.

The cell viability assays market refers to the global market for analytical techniques and reagents used to assess the health, proliferation, and survival of cells in biological and pharmaceutical research. These assays measure the number of living cells in a sample and are crucial for drug discovery, toxicology studies, cancer research, and other biomedical applications. They provide insights into cellular metabolic activity, membrane integrity, and enzyme function, helping researchers understand cytotoxicity, proliferation, and cellular responses to treatments.

Numerous factors influence market growth, including the rising prevalence of chronic disorders and cancer, as well as growing research and development activities. The burgeoning pharmaceutical and biotechnology sectors contribute to market growth. Stringent regulatory policies regarding cytotoxicity test results for new drug compounds are expected to favor market growth. Technological advancements drive the latest innovations in cell viability assays by introducing automation.

Artificial intelligence (AI) plays a vital role in cell viability assays by introducing automation and improving accuracy. It provides real-time monitoring of assays, enabling researchers to make proactive decisions. Live-cell assays generate multiple data points from a single well over time. AI can enhance the efficiency, accuracy, and reproducibility of viability assays, allowing researchers to focus on result interpretation over conducting laborious manual tasks. Additionally, it can assist researchers in data interpretation, avoiding complex calculations. Thus, AI can overcome the significant challenges of conventional assay procedures.

Driver

Growing Cancer Research

The major growth factor for the cell viability assays market is the growing field of cancer research. The rising prevalence of cancer and its severity lead to increased cancer research activities. The World Health Organization (WHO) estimates that about 1 in 5 people develop cancer in their lifetime, and approximately 1 in 9 men and 1 in 12 women die from cancer. (Source - WHO) Researchers identify novel targets and biomarkers that are involved in disease progression. This enables them to design novel drugs and test those drugs for their cytotoxicity profile.

Restraint

Lack of Qualitative Data

Cell viability assays provide only quantitative data. They are unable to distinguish between different forms of cell death or derive the mechanism of cell death. This leads to insufficient data about cell viability, restricting market growth.

Opportunity

What is the Future of the Cell Viability Assays Market?

The market future is promising, driven by the increasing demand for personalized medicines. Personalized medicines are developed to address rapidly changing demographics and deliver targeted treatment. Advancements in genomics also support the development of personalized medicines. Stem cells, gene therapy, monoclonal antibodies, and recombinant proteins are the most common examples of personalized medicines. Cell viability assays are essential for stem cell research to assess their cell health and proliferation, especially when evaluating treatments or culture conditions. These assays help quantify the number of live cells, providing insights into cell survival, metabolic activity, and potential cytotoxicity.

| Metric | Details |

| Market Size in 2026 | USD 2.23 Billion |

| Projected Market Size in 2035 | USD 4.66 Billion |

| CAGR (2026 - 2035) | 8.54% |

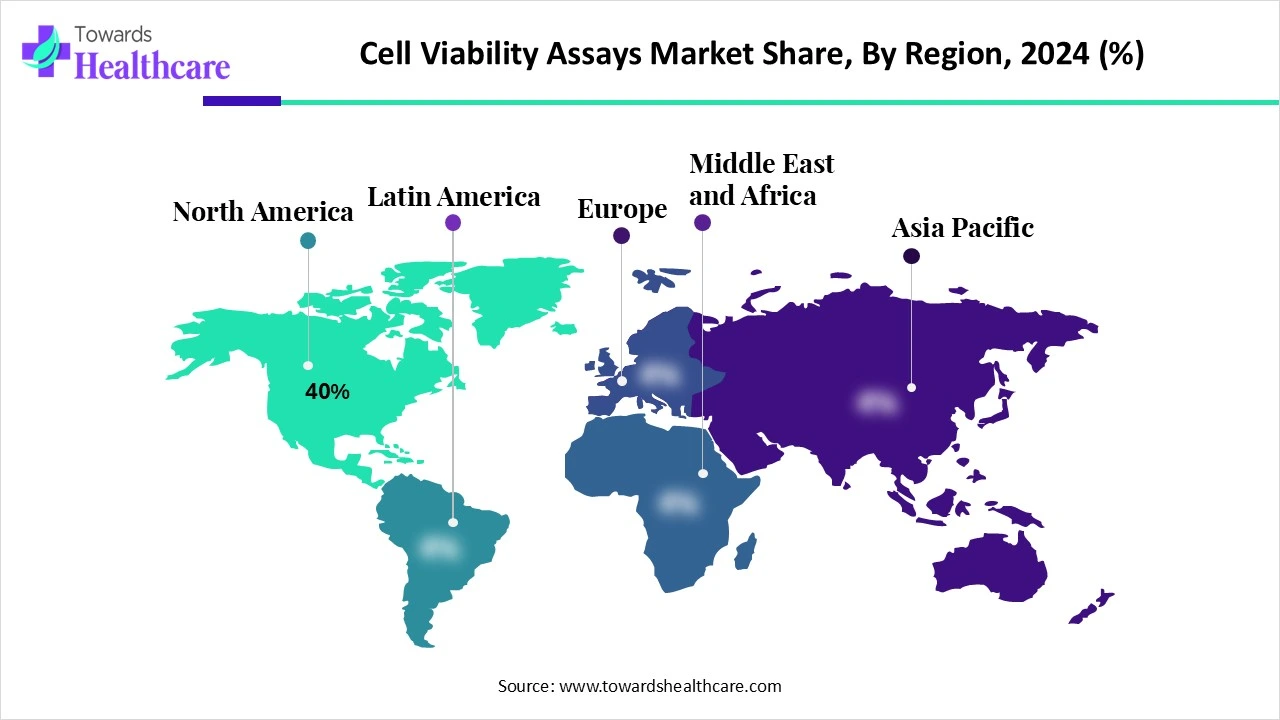

| Leading Region | North America Share by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product Type, By Assay Type, By Application, By End-Use, By Technology, By Region |

| Top Key Players | Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), Bio-Rad Laboratories, PerkinElmer Inc., Promega Corporation, Lonza Group AG, Abcam plc, BD Biosciences, Agilent Technologies, Roche Diagnostics, Takara Bio Inc., GE Healthcare Life Sciences, Enzo Life Sciences, Qiagen N.V., Corning Incorporated, Sigma-Aldrich (part of Merck), Sartorius AG, Tecan Group Ltd., Luminex Corporation, Cellular Technology Limited (CTL) |

")

Which Product Type Segment Dominated the Cell Viability Assays Market?

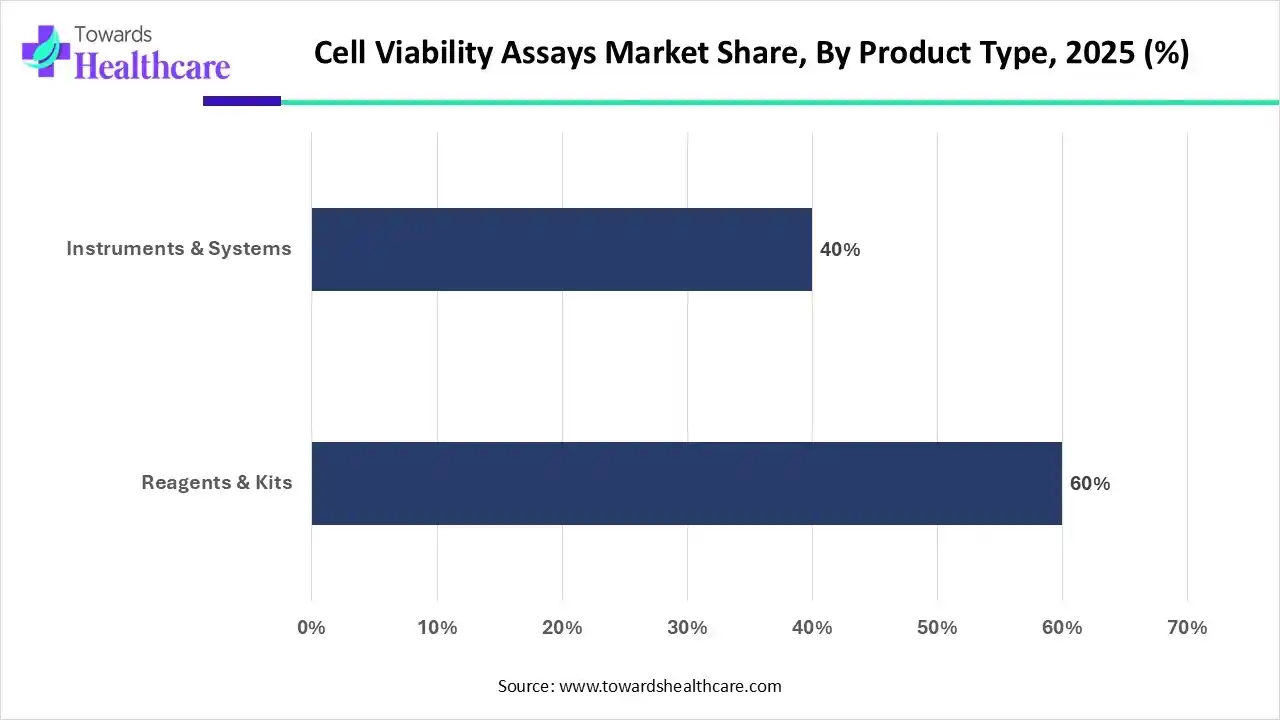

By product type, the reagents and kits segment held a dominant presence in the market by 60% in 2025. This segment dominated due to the continuous requirements of reagents and kits for assays. Several companies provide kits and reagents at affordable rates, enabling researchers to meet their research requirements. They are more cost-effective than instruments and do not require specialized infrastructure. They enable researchers to develop accurate and reproducible results.

By product type, the instruments & systems segment is expected to grow at the fastest CAGR in the market during the forecast period. Instruments provide advanced services and results, and are integral parts of cell viability assays. Technological advancements drive the latest innovations in instruments to derive accurate results. Instruments, such as microplate readers, fluorescence microscopes, flow cytometers, and cell imaging systems, aid in data analysis and interpretation.

Why Did the Metabolic Activity-Based Assays Segment Dominate the Cell Viability Assays Market?

By assay type, the metabolic activity-based assays segment held the largest revenue share of the market by 45% in 2025. This is due to the ease of measuring cell metabolites and the simple procedure. Metabolites are directly linked to cellular energy, the generation of cellular building blocks, and signaling pathways. Metabolic activity-based assays help researchers to measure glucose uptake, lactate, glutamine, oxidative stress, and dinucleotide detection assays. These tests assess enzymatic activity as a marker for cell viability. An increase in enzyme activity is an indication of enhanced cell proliferation.

How the Pharmaceutical & Biotech Research Segment Dominated the Cell Viability Assays Market?

By application, the pharmaceutical & biotech research segment contributed the biggest revenue share of the market in 2025. This segment dominated due to the growing research and development activities in the pharma and biotech sectors. New drug discovery and stem cell research necessitate cell-based assays to assess cell cytotoxicity. Cell viability assays are used to evaluate drug safety and efficacy, optimize culture conditions, and screen drug candidates. This enables researchers to identify potential drug candidates before testing on animals. The increasing emphasis of several government organizations on reducing animal testing potentiates the demand for cell viability assays.

By application, the clinical diagnostics segment is expected to grow with the highest CAGR in the market during the studied years. The rising prevalence of chronic disorders and the increasing demand for early disease diagnosis augment the segment’s growth. Cell viability assays are used to determine the health and metabolic state of cells. The growing need for point-of-care diagnostics promotes the use of cell viability assays. These assays offer high specificity and sensitivity in diagnosing several chronic disorders.

Which End-Use Segment Led the Cell Viability Assays Market?

By end-use, the pharmaceutical & biotech companies segment led the global market in 2025. The segmental growth is attributed to favorable infrastructure and suitable capital investments, enabling pharma & biotech companies to perform cell viability assays within their facilities. This also saves cost for indigenously performing assays. These companies mainly focus on developing novel drug candidates to expand their pipeline, necessitating the use of cell viability assays.

By end-use, the contract research organizations (CROs) segment is expected to expand rapidly in the market in the coming years. Numerous large and small-scale pharma companies prefer outsourcing their research activities to CROs due to the presence of skilled professionals and specialized equipment. CROs provide customized solutions to research problems. The increasing collaboration with CROs enables companies to focus primarily on product sales and marketing.

What Made Colorimetric the Dominant Segment in the Cell Viability Assays Market?

By technology, the colorimetric segment held a major revenue share of the market in 2025. The colorimetric method is most widely preferred as it can quantify viable cells easily using a formazan dye. This method accounts for visual changes in assay procedures and cell proliferation. It eliminates the need for using specialized equipment to measure cell viability. It involves the use of a variety of tetrazolium reagents, including XTT, MTT, CCK-8/WST-8, etc. The color intensity of the reagents is analyzed using a UV spectrophotometer.

By technology, the luminescent segment is expected to witness the fastest growth in the market over the forecast period. Luminescence-based assays quantify ATP that signals the presence of metabolically active cells. The amount of ATP present is directly proportional to the number of cells present. This assay is based on the luciferase reaction, which has a half-life of more than five hours. This eliminates the need for constant reagent injectors, providing greater flexibility for reagent procedures.

")

North America dominated the global market share by 40% in 2025. The availability of state-of-the-art research and development facilities, the presence of key players, and favorable government support are the major growth factors of the market in North America. Government organizations provide funding to conduct pharma & biotech research. Research institutions and companies in North America have skilled professionals to perform assays.

U.S. Market Trends

Key players, such as Thermo Fisher Scientific, Sigma Aldrich, and Promega Corporation, are the major contributors to the cell viability assays market in the U.S. There are currently 542 research institutions in the U.S. The National Institute of Health (NIH) provides funding for various research activities and is made up of 27 Institutes and Centers, focusing on particular diseases. NIH invests around $48 billion annually.

Canada Market Trends

The Ontario Institute for Cancer Research (OICR) launched the “Drug Discovery Program”, which is one of the largest programs of its kind in Canada. The OICR’s Cancer Therapeutics Innovation Pipeline (CTIP) awards funded $300,000 over 2 years to help advance promising drug discovery research for the development of new cancer drugs.

Asia-Pacific is expected to grow at the fastest CAGR in the cell viability assays market during the forecast period. The burgeoning pharmaceutical and biotech sectors and growing research activities bolster market growth. Increasing R&D investments and collaborations among key players facilitate access to advanced technology. Numerous private and public research institutions conduct seminars and workshops at national and international levels to educate and train researchers and students about cell viability assays.

China Market Trends

China is emerging as a global leader in clinical and pharmaceutical research. China led in the total number of drug approvals from 2019 to 2023, with 256 new drug approvals. The Chinese government also provides funding for the development of new drugs and encourages innovation in domestic pharmaceutical companies.

India Market Trends

The Indian government has launched the Rs 5,000 crore Scheme for Promotion of Research and Innovation in Pharma MedTech Sector (PRIP). The government aims to invest approximately Rs 17,000 crore in pharma R&D by FY28, focusing on cancer research, lifestyle disease prevention, medical technology, and niche segments like orphan drugs.

Europe is expected to grow at a notable CAGR in the cell viability assays market in the foreseeable future. Research institutions in European nations have favorable infrastructure to conduct cell viability assays. The funding cut in research by the U.S. government opens doors for American scientists to conduct their experiments in Europe. Favorable government support by the European government and the rising adoption of advanced technologies promote market growth.

Germany Market Trends

Germany hosts around 700 pharmaceutical companies, employing a total of 133,000 people. The German government recently launched the National Pharma Strategy to secure the supply of pharmaceuticals, accelerating access to innovations and boosting Germany’s competitiveness in the pharma industry.

UK Market Trends

The Association of the British Pharmaceutical Industry (ABPI) reported that the industry contributed to almost 5,000 research papers from 2019 to 2023, supporting 283 patent applications. 11% of such papers were in the top 1% of the most referenced scientific papers. The UK government announced ten-year funding for pharmaceutical R&D.

South America is expected to grow significantly in the cell viability assays market during the forecast period, due to growing R&D activities. The growing biopharmaceutical manufacturing and government investments are also increasing the adoption of cell viability assays for the development of vaccines and biologics, enhancing the market growth.

Brazil Cell Viability Assays Market Trends

Brazil consists of well-developed industries and institutes, which are increasing the use of cell viability assays for their growing innovations. Additionally, increasing outsourcing trends, government funding, and technological advancements are also increasing their advancements and adoption rates.

MEA is expected to show lucrative growth in the cell viability assays market during the forecast period, due to expanding R&D infrastructure, which is increasing the use of cell viability assays for R&D purposes such as drug screening and toxicity testing. Increasing use of biologic and advanced therapies are also increasing their demand, promoting the market growth.

Saudi Arabia Cell Viability Assays Market Trends

The growing government health initiatives across Saudi Arabia are encouraging the utilization of the cell viability assays for various R&D activities. The growing healthcare investments are also increasing their use for the development of vaccines and biologics, where the growing collaborations among companies are increasing their innovations.

1. R&D

The R&D of the cell viability assays focuses on the development of label-free, real-time, and non-destructive monitoring systems with AI-driven image analysis.

Key players: Thermo Fisher Scientific, Agilent Technologies, Promega.

2. Clinical Trials and Regulatory Approvals

The analytical validity involving reproducibility, accuracy, and precision, along with the potency, is evaluated in the clinical trials and regulatory approvals of the cell viability assays.

Key players: Beckman Coulter, Thermo Fisher Scientific, Promega.

3. Formulation and Final Dosage Preparation

The formulation and final dosage preparation of the cell viability assays involves the development of the ready-to-use lyophilized powders and stabilized liquid reagents with enhanced stability.

Key players: Thermo Fisher Scientific, Agilent Technologies, Promega.

4. Packaging and Serialization

The light-protected temperature-controlled primary containers integrated with GS1-compliant 2D barcodes are utilized in the packaging and serialization of the cell viability assays.

Key players: Thermo Fisher Scientific, Stevanato Group, Promega.

5. Distribution to Hospitals, Pharmacies

The highly specialized cold-chain logistics networks are responsible for the distribution of the cell viability assays to the hospitals and pharmacies.

Key players: Thermo Fisher Scientific, McKesson Corporation, Cardinal Health.

6. Patient Support and Services

Comprehensive technical training, clinical interpretation tools, and real-time troubleshooting are provided in the patient support and services of the cell viability assays.

Key players: Thermo Fisher Scientific, Agilent Technologies, Promega.

James Atwood, General Manager of Opentrons Robotics, commented that the company’s newly launched automation marketplace serves as a one-stop shop, providing convenient access to products and services. The company aims to expand its marketplace offerings through strategic partnerships, especially in genomics, proteomics, and cell-based assays, ensuring customers can effortlessly address all their needs in one centralized location.

By Product Type

By Assay Type

By Application

By End-Use

By Technology

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar