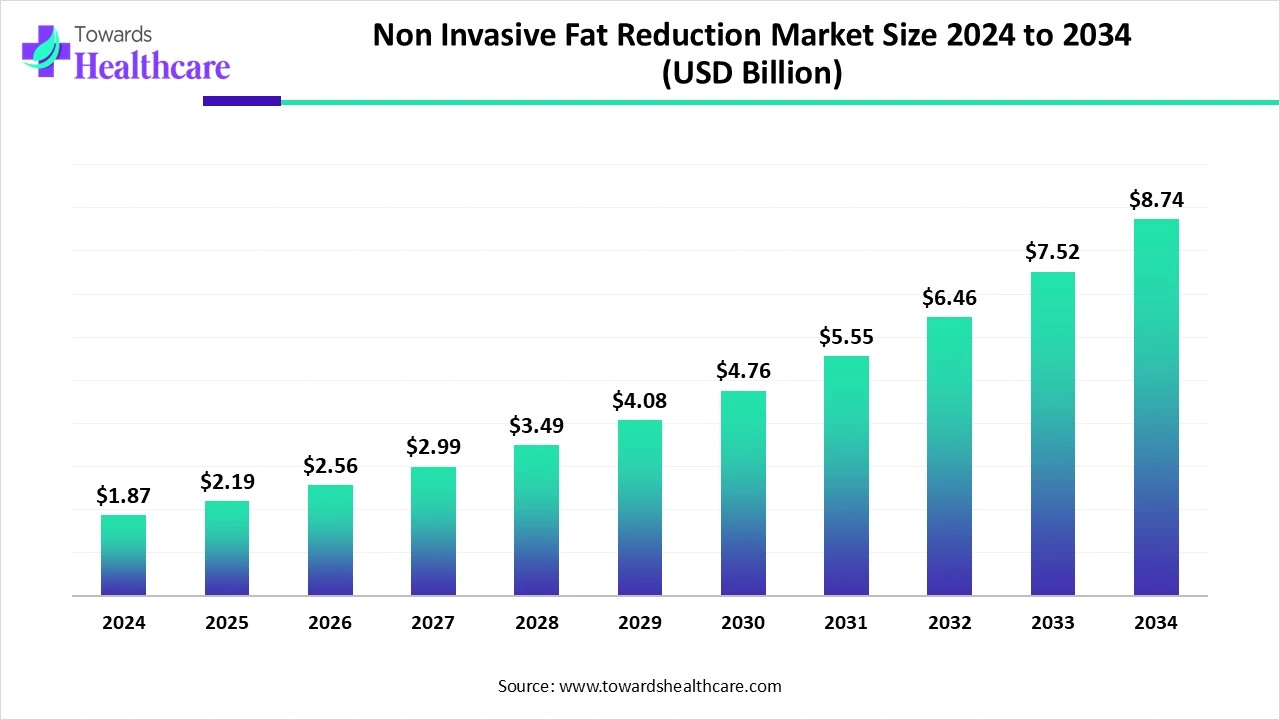

The global non-invasive fat reduction market size is calculated at US$ 1.87 billion in 2024, grew to US$ 2.19 billion in 2025, and is projected to reach around US$ 8.74 billion by 2034. The market is expanding at a CAGR of 17.04% between 2025 and 2034.

")

The non-invasive fat reduction market is expanding quickly worldwide because physical appearance is important and body image awareness is developing due to urbanisation, changing lifestyles, and media influence. Both sexes are looking for non-surgical ways to improve their appearance and self-esteem. An increasingly common societal tendency is the desire to seem young and fit. There is a growing need for non-invasive fat reduction procedures due to the desire to seem young and fit.

| Table | Scope |

| Market Size in 2025 | USD 2.19 Billion |

| Projected Market Size in 2034 | USD 8.74 Billion |

| CAGR (2025 - 2034) | 17.04% |

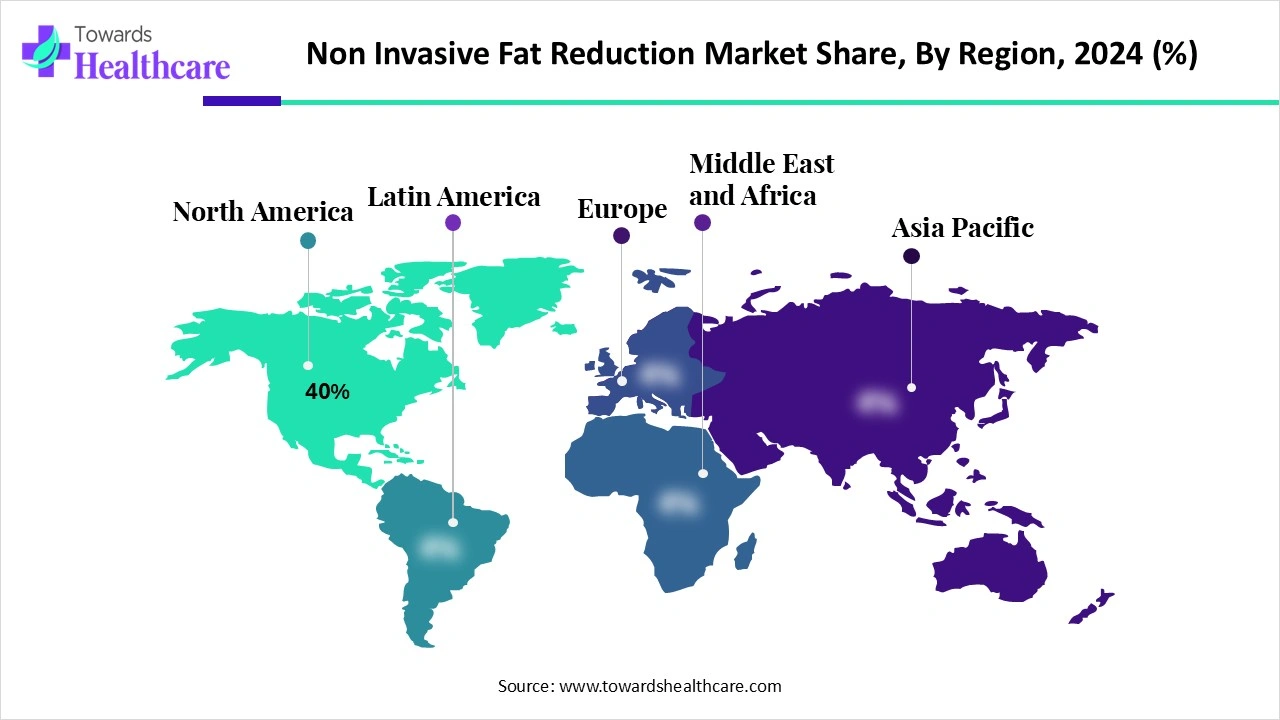

| Leading Region | North America Share 40% |

| Market Segmentation | By Technology/Modality, By Treatment Area, By End User/Practice Type, By Revenue Model, By Patient Demographic, By Distribution Channel, By Region |

| Top Key Players | AbbVie, Zeltiq, Cynosure, BTL Aesthetics, Candela, Cutera, Alma, Lumenis, Venus Concept, InMode, Zimmer MedizinSysteme, Cocoon Medical, Classys, DEKA (El.En.), Jeisys Medical, Bison Medical, Hironic, Sinclair, Wontech, Deleo (France), Allurion |

The non-invasive fat reduction market covers energy-based body-contouring treatments that reduce subcutaneous fat without incisions, anesthesia, or downtime. Core modalities include cryolipolysis, laser lipolysis (1060 nm), radiofrequency (RF / RF-microwave), and focused ultrasound (HIFU). These systems induce adipocyte apoptosis or lipolysis with controlled thermal or mechanical energy, followed by natural metabolic clearance. Demand is driven by rising aesthetic procedure volumes, DSO/med-spa expansion, improving comfort and treatment times, and broader candidacy across Fitzpatrick skin types.

AI is revolutionising slimming clinic operations, and the outcomes are amazing. AI-powered body composition scans are able to identify minute variations in the composition of muscle and fat, down to the millimetre. AI is able to assess body composition and suggest the best slimming regimen, which may be extensively customised. Clients at contemporary slimming clinics using AI technologies are undergoing amazing, noticeable changes. The entire strategy has changed from relying on hunches and broad goals to using precise facts.

Rise in Obesity

The non-invasive fat reduction market is expanding as a result of the increased demand for non-invasive methods of treating obesity. According to the World Obesity Federation's 2024 World Obesity Atlas, estimates for 2035 indicate that 1.53 billion individuals will suffer from obesity and over 1.77 billion will be overweight. This will be equivalent to 54% of all adults globally. A sizable fraction of these people will reside in nations with low and moderate incomes. More than 1 billion people are obese as of 2024, and overweight or obesity is a contributing factor in 1 in 8 fatalities from non-communicable illnesses

High Procedure Cost

One major obstacle to the market's expansion is the high cost of research and development for fat-reduction drugs, as well as the absence of funding. Longer-term research and development projects as well as clinical studies to assess medications further raise total expenses. Global market expansion may be hampered by the dangers and limitations presented by the high development costs of obesity treatments.

What is the Future of the Non-Invasive Fat Reduction Market?

With the development of technology, the market's future is still changing. More accuracy, comfort, and outcomes are available with emerging therapies. Combination treatments, which use many devices in one therapy, are becoming more and more common as a result of their improved results. Keeping up with these developments guarantees that your practice will continue to be competitive and provide patients with the greatest outcomes.

By technology/modality, the cryolipolysis segment was dominant in the non-invasive fat reduction market in 2024. Following clearance by the U.S. Food and Drug Administration (FDA), cryolipolysis gained popularity and is now one of the most often used noninvasive cosmetic treatments worldwide. Cryolipolysis is a long-lasting, easy, and safe fat reduction solution. Cryolipolysis is presently one of the most widely used noninvasive cosmetic procedures, with over 4 million treatments completed worldwide.

By technology/modality, the radiofrequency & RF-microwave segment is estimated to be the fastest-growing in the non-invasive fat reduction market during the upcoming period. High-intensity focused electromagnetic (HIFEM) and radiofrequency-based technologies have shown promise in the safe and efficient contouring of the abdominal body. Adipose tissue is known to be reduced by radiofrequency, whereas muscle definition is achieved with HIFEM therapy. One of the most exciting developments in this area is the application of microwave energy. Deeper tissue penetration, more accurate targeting, and increased effectiveness in body sculpting procedures are all made possible by microwave-based technologies.

By treatment area, the abdomen & flanks segment held the largest share of the non-invasive fat reduction market in 2024. The need for non-surgical fat removal techniques has increased dramatically as the difficulties of eliminating flank and abdominal fat using conventional treatments become more obvious. CoolSculpting and other non-invasive body sculpting techniques have become more popular because they may target certain fat deposits without requiring surgery. With less discomfort and downtime than traditional treatments, these procedures provide a safe and efficient substitute.

By treatment area, the submental (double chin) segment is anticipated to witness the highest CAGR in the non-invasive fat reduction market during 2025-2035. In patients of all ages, both male and female, submental fat is an aesthetic concern. The usage of non-surgical fat reduction techniques is growing in popularity as patients and doctors look for less intrusive approaches. These novel methods include injectable chemical lipolysis, laser approaches, high-intensity focused ultrasound, percutaneous radiofrequency, and submental cryolipolysis.

By end-user/practice type, the physician-led aesthetic clinics segment captured the major revenue of the non-invasive fat reduction market in 2024. When it comes to receiving an aesthetic treatment, patients are given additional peace of mind by physician-led aesthetic clinics. In order to comprehend each patient's distinct medical history and demands, doctors do thorough health exams. In order to prevent potential consequences and customise therapy for each patient, this step is essential. Physicians are highly qualified professionals who follow stringent ethical and professional standards.

By end-user/practice type, the medical spas/aesthetic chains segment is expected to achieve the highest growth in the non-invasive fat reduction market during the predicted time frame. Social media's growth and the increased emphasis on self-care are driving the medical spa sector's expansion. With their outstanding services and robust online presence, leading businesses like VIO Med Spa, Venus Med Spa, and LaserAway are raising the bar. In addition to providing excellent services, a strong brand guarantees client credibility and confidence.

By revenue model, the capital equipment sales segment held the largest share of the non-invasive fat reduction market in 2024. Capital equipment sales in non-invasive fat removal are developing significantly, driven by customer demand for minimally invasive cosmetic operations and increased awareness of wellbeing. Hospitals and specialised aesthetic centres are major purchasers in the sector, which is witnessing substantial investment from both startups and well-established businesses. The emergence of GLP-1 weight loss medications, which emphasise the need for body contouring options, and the increasing popularity of laser-based technologies and cryolipolysis (fat freezing) are important market drivers.

By revenue model, the pre-procedure disposables/applicator use-fees segment is anticipated to be the highest growing in the non-invasive fat reduction market during 2025-2034. Applicator use-payments are fees for specialised single-use or reusable applicators for devices like laser hair removal or radiofrequency treatments, whereas disposable pre-procedure goods in the medical aesthetics sector include single-use items like syringes, needles, or wipes. certain expenses, which cover the cost and specialised handling of certain materials and improve efficiency and safety by avoiding cross-contamination, are included in the process fee.

By patient demographic, the female segment was dominant in the non-invasive fat reduction market in 2024. The International Society of Aesthetic Plastic Surgery (ISAPS) published the findings of its yearly worldwide survey on cosmetic and aesthetic operations in June 2025. For women, liposuction remained the most popular surgical treatment. With 98% of stomach tuck and 94% of liposuction patients being female, women continue to be the primary consumers of these procedures.

By patient demographic, the male segment is estimated to be the fastest-growing in the non-invasive fat reduction market during the predicted period. The field of cosmetic surgery has seen a discernible change in recent years. More males are increasingly pursuing surgical procedures to improve their looks and confidence, so it is no longer a field mostly occupied by women. Liposuction is one such operation that is becoming more and more popular among males. There are a variety of reasons why more and more men are choosing liposuction, from cultural influences to individual desires for a toned, more defined figure.

By distribution channel, the direct OEM sales to clinics segment held the major revenue of the non-invasive fat reduction market in 2024. OEMs have the chance to build stronger relationships with their target market, get insightful data, and provide individualised experiences catered to each person's tastes and requirements. OEMs may put themselves at the forefront of innovation and adjust to the shifting dynamics of the medical device market by adopting the D2C model.

By distribution channel, the leasing, managed-service & pay-per-use programs segment is anticipated to expand at the highest rate in the non-invasive fat reduction market during the studied duration. Clinics that offer a subscription or package deal for continuous non-surgical fat reduction procedures, such as CoolSculpting or laser lipolysis, are probably using a managed-service, pay-per-use model for fat reduction procedures. This model offers a fixed monthly fee or per-session cost for a predetermined number of treatments and individualised management. In contrast to surgical treatments like liposuction, this offers clients continuous care and maybe greater value than typical, single-procedure prices.

")

North America dominated the non-invasive fat reduction market share 40% in 2024. The region's rising obesity rate, higher R&D expenditures, highest per capita disposable income, expanding use of new technology, and continuous awareness campaigns all contribute to this. The increasing need for physical characteristics that exude confidence and a faultless appearance in the major areas of work is propelling the regional market's growth. The advancement of the country is aided by easy access to medical facilities and the development of convenient procedures.

According to recent studies, 49.2% of American people will be obese by 2030, or over half. At least 35% of people in each state will have a body mass index of at least 30, which is the cutoff point for obesity. In 2030, it is predicted that 21.1% of American males and 27.6% of American women would be seriously obese.

The Canadian Adult Obesity Clinical Practice Guideline, created by Obesity Canada and the Canadian Association for Bariatric Physicians and Surgeons, is regarded as a premier resource for managing obesity on a global scale. Healthcare professionals acquire useful, research-based techniques to help patients who are obese. This globally recognised guideline is transforming care standards and guaranteeing that patients receive the assistance and respect they are entitled to.

Asia Pacific is estimated to host the fastest-growing non-invasive fat reduction market during the forecast period. driven by growing middle-class populations and metropolitan areas' increased emphasis on beauty. Despite macroeconomic turbulence, China leads the world in volume, with 91% of surveyed aesthetic consumers planning to continue or increase spending. Japan is a leader in innovation, as demonstrated by robotic applicator arms that reduce session setup time by 40%. South-east Asia has embraced combination treatment blueprints thanks to South Korea's export of K-beauty regimens. India's youthful population and fast expansion of private hospitals provide substantial opportunities once import taxes are reduced.

Understanding the mechanisms of fat cell destruction (such as cooling or heating), creating devices (such as cryolipolysis, radiofrequency, ultrasound, and laser), demonstrating their safety and selective efficacy on fat cells without causing harm to other tissues, conducting clinical trials to demonstrate efficacy in humans, and improving the technology for patient comfort, efficiency, and a variety of applications, including enhancing skin texture after treatment, are all part of research and development for non-invasive fat reduction.

Key Companies: Cynosure, BTL Industries, Cutera, Candela Corporation, Venus Concept, and Alma Lasers

Clinical trials for non-invasive fat reduction follow traditional pharmaceutical phases to show safety and efficacy, including Phase I (safety), Phase II (efficacy), Phase III (compared to existing therapies), and Phase IV (post-market surveillance). Thorough testing is necessary to guarantee the safety and efficacy of the therapy for its intended purpose before receiving regulatory clearance, which is frequently granted by the U.S. Food and Drug Administration (FDA) for medications or devices. This entails preclinical testing, human clinical trials, and the submission of trial results for regulatory agency assessment.

Key Companies: Cynosure LLC, Candela Corporation, BTL Group, Cutera, Venus Concept, Solta Medical (Bausch Health), and Alma Lasers.

Support for non-invasive fat reduction for patients consists of comprehensive medical evaluations and consultations to manage expectations and evaluate candidature, followed by a technique that may use ultrasonic energy, heating, or cooling to break down fat cells. In order to provide comfort during the minimally invasive procedure with little to no downtime, services frequently include patient education about the operation, potential hazards, and post-treatment care.

Key Companies: Cutera, Candela, Alma Lasers, Bausch Health (via Solta Medical), and Cynosure.

In November 2024, our unwavering dedication to innovation and the best possible patient outcomes is embodied by the launch of CoolSculpting® ELITE in Canada, stated Carolina Martin, General Manager, Allergan Aesthetics Canada. Being the pioneer of the body contouring market, we take pride in being at the forefront of innovation and providing clinics and patients nationwide with the skills and resources they need to achieve outstanding outcomes.

By Technology/Modality

By Treatment Area

By End User/Practice Type

By Revenue Model

By Patient Demographic

By Distribution Channel

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar