The global next-generation therapies market is on an upward trajectory, poised to generate substantial revenue growth, potentially climbing into the hundreds of millions over the forecast years from 2025 to 2034. This surge is attributed to evolving consumer preferences and technological advancements reshaping the industry.

The demand for the use of next-generation therapies is increasing to combat the rising diseases. At the same time, the industries and institutes are researching and developing various innovative approaches to enhance their applications. Moreover, growing collaboration among the companies is leading to new such developments and launches. The use of AI is also enhancing their development. Moreover, their demand in different regions is also increasing due to a variety of factors. Thus, these growing advancements in next-generation therapies are promoting the market growth.

The market refers to cutting-edge therapeutic modalities that go beyond traditional small-molecule drugs and biologics. These include gene therapy, cell therapy, RNA-based therapy, and genome editing technologies aimed at treating previously untreatable or rare diseases. These therapies are often highly personalized, curative in intent, and leverage advances in genomics, synthetic biology, and delivery platforms. Their application spans oncology, rare genetic diseases, neurology, hematology, and immunology, as well as they are reshaping the future of medicine.

The use of AI in the next-generation therapies is increasing as it helps in predicting diseases, potential targets, as well as therapy responses. It also helps in developing therapies with enhanced precision and minimized errors. Moreover, a large volume of genomic, proteomic, or transcriptomic data is analyzed efficiently, which can be used in the development of personalized medications. At the same time, it also helps the scientists in decision-making. Thus, it helps in the development of therapies with improved safety and efficacy.

Growing Use of Cell and Gene Therapy

The growing chronic diseases is increasing the use and demand for cell and gene therapies. These therapies help in replacing or correcting the defective genes as well as show targeted action, reducing the side effects. At the same time, growing research and development are also enhancing their applications. This, in turn, is increasing their use in cancer, neurological diseases, and cardiovascular diseases as well. Moreover, personalized therapies are also being provided to the patients. Thus, all these factors are driving the next-generation therapy market growth.

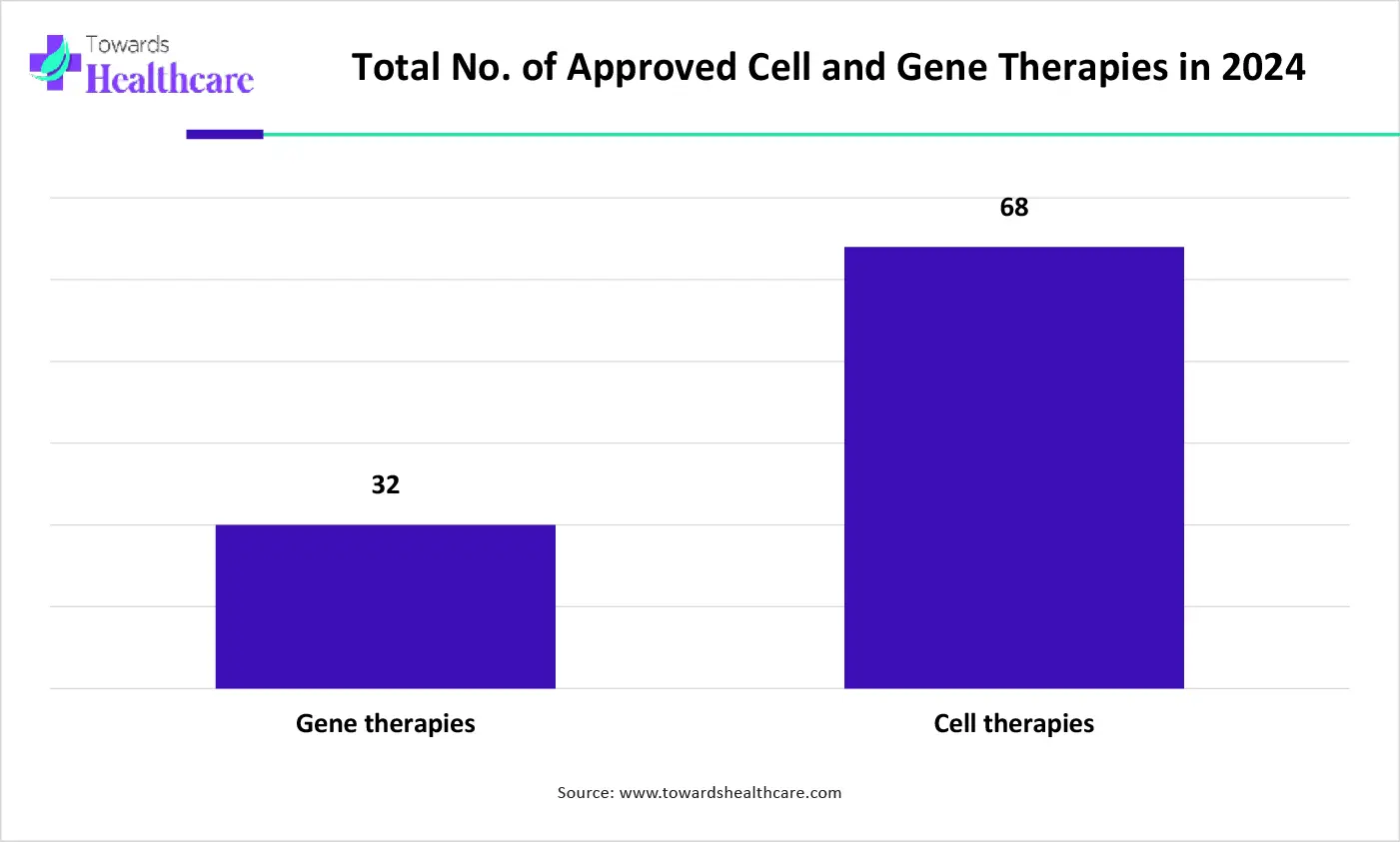

The graph represents the total number of approved gene and non-genetically modified cell therapies in 2024. It indicates that there is a rise in the development of next-generation therapies for the effective management of increasing diseases. Thus, this in turn will ultimately promote the market growth.

Complex Procedures

The formulation development process of the next-generation therapies is often complex. Thus, this increases the need for expertise or specialized personnel. Moreover, it also requires specialized instruments and infrastructure. Additionally, it may include lengthy or multi-step procedures, delaying the development of therapies. Thus, these factors may restrict the market growth.

New Developments in RNA-Based Therapies

The growing genetic disorders are increasing the use of RNA-based therapies, which in turn, are driving their innovative developments. New RNA-based therapies are being developed for cancer, as well as infectious diseases and rare diseases. Moreover, due to their advantage of not altering the DNA or combining with genomes, their use is increasing. Furthermore, personalized therapies are also being provided to the patients. At the same time, growing research for targeting neurological diseases is also being conducted. Thus, all these developments are promoting the next-generation therapy market growth.

For instance,

By therapy type, the gene therapy segment held the largest share in the market with ~38% in 2024. The gene therapies provided targeted action, which increased their use in genetic diseases. At the same time, it also showed improved safety and efficacy, which increased its acceptance rates. It was also used in cancer treatment. Thus, this contributed to the market growth.

By therapy type, the RNA-based therapy segment is expected to show the fastest growth rate at a notable CAGR during the predicted time. The use of RNA-based therapy is increasing for the treatment of infectious diseases and cancer. Moreover, personalized therapy options are also being developed, with improved effectiveness.

By application type, the oncology segment led the market with ~46% in 2024. Different types of next-generation therapies were used for the treatment of cancer. Thus, due to their advantages with minimized side effects, their use increased. Similarly, new developments were also conducted to improve their stability.

By application type, the rare genetic disorders segment is expected to show the fastest growth rate during the forthcoming years. Due to the lack of treatment approaches and growing incidences of rare genetic disorders, there is a rise in the use of next-generation therapies. Their development and approval are further being supported by the government and regulatory bodies.

By vector type, the adeno-associated virus (AAV) vectors segment held the largest share in the market with ~40% in 2024. The adeno-associated virus (AAV) vectors were widely used as they were non-pathogenic. Thus, they were used to deliver the genes to the targeted site and provided long-term effects. Thus, this enhanced the market growth.

By vector type, the non-viral vectors segment is expected to show the highest growth during the upcoming years. Their use is increasing as they don’t show any adverse immune reactions. Moreover, they can easily deliver multiple or large genes to the targeted site effectively. Thus, their use in RNA therapies is increasing.

By route of administration type, the intrathecal/intracerebral segment led the market in 2024. The use of the intrathecal/intracerebral route of administration increased as it helped in delivering the therapies directly to the spinal cord or brain. This enhanced its action and efficacy. Moreover, this route was preferred in the treatment of neurological disorders.

By route of administration type, the intramuscular segment is expected to show the fastest growth rate during the upcoming years. The use of the intramuscular route to deliver next-generation therapies is increasing as it does not require advanced facilities. Furthermore, it shows minimal systemic side effects. Thus, its acceptance rate is increasing.

By end user, the hospitals & specialty clinics segment held the dominating share in the global market with ~51% in 2024. Hospitals & specialty clinics provide a wide range of next-generation therapies with advanced technologies and skilled personnel. Moreover, it enhanced the patient outcomes by monitoring their treatment. This promoted the market growth.

By end user, the homecare segment is expected to show the highest growth during the predicted time. The patients are shifting towards home care as it promotes self-administration of the therapies and provides comfort. At the same time, it also reduces the number of hospital visits and charges, enhancing the convenience of the patients.

")

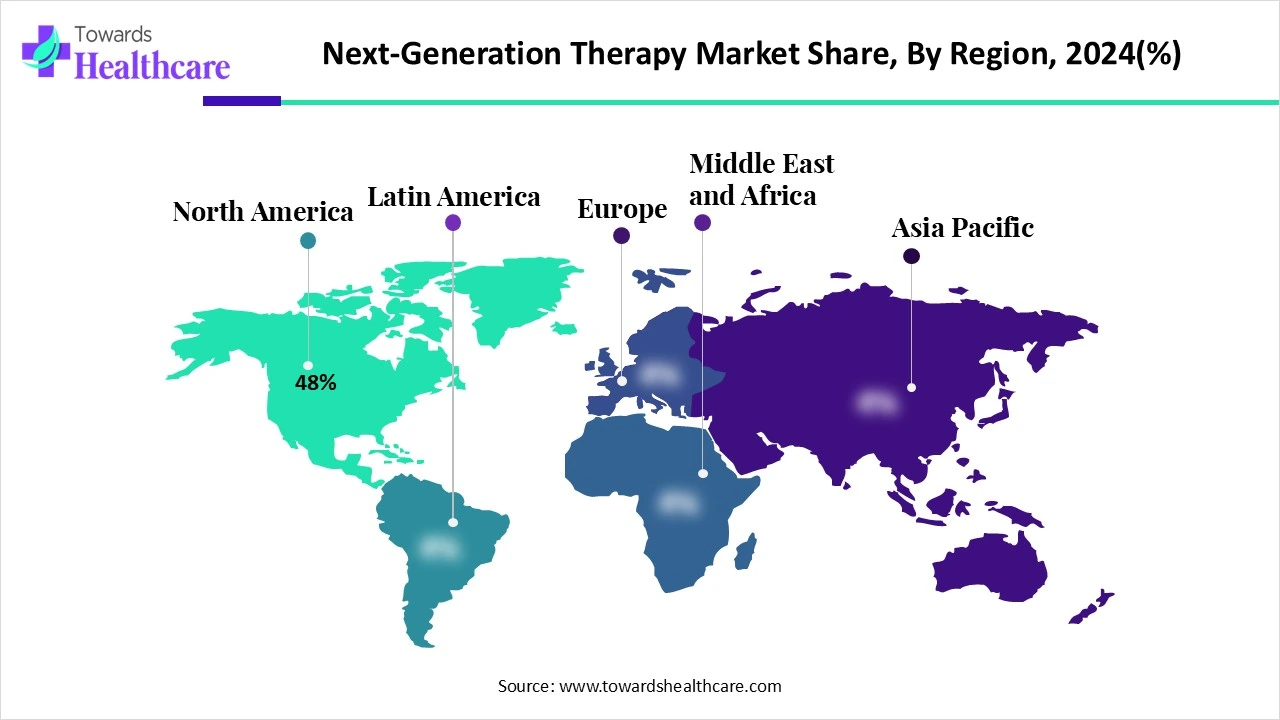

North America dominated the next-generation therapy market share by 48% in 2024. North America consisted of well-developed, robust industries that were focusing on the development of various next-generation therapies to treat rising diseases. Moreover, the use of CAR-T therapy was observed to have increased. This contributed to the market growth.

The biotech industries in the U.S. are developing new cell or gene therapies. At the same time, to support them, funding from various sources is also being provided. Thus, this is driving their research and development for next-generation therapies, as well as collaboration among them.

The industries as well as institutes in Canada are innovating novel therapies to tackle various diseases. Moreover, these developments are also supported by the regulatory bodies and the government by granting fast approvals and implementing policies. At the same time, the hospitals are increasing the use of cell and gene therapies.

Asia Pacific is expected to host the fastest-growing next-generation therapy market during the forecast period. Asia Pacific is experiencing a rise in the incidence of various chronic diseases. Hence, to deal with this growing burden, the industries and institutions are developing different next-generation therapies. Thus, this enhances the market growth.

The industries in China are focusing on the development of next-generation therapies. At the same time, they are utilizing advanced technologies that are enhancing their development as well as production. Furthermore, these developments are also supported by the initiative of the government and regulatory agencies.

The growing incidence of diseases in India is increasing the research and development for next-generation therapies. At the same time, the expanding healthcare sector is also adopting advanced technologies, which are improving its development process. Moreover, the growing investment and funding are also contributing to the same.

Europe is expected to grow significantly in the next-generation therapy market during the forecast period. Europe consists of well-developed industries and institutes that are researching and formulating several next-generation therapies. These therapies are leading to new launches in the market. Thus, these innovative launches are promoting the market growth.

The increasing diseases in Germany has increased the use of next-generation therapies for their proper management. At the same time, the industries are manufacturing new cell and gene therapies to deal with different types of cancer and genetic diseases. Moreover, to enhance their access, the government is also providing support.

Due to the growing interest, the industries as well as institutions of the UK are developing next-generation therapies. This, in turn, is also leading to new collaborations among them. Funding and advanced technologies, as well as growing awareness, are further driving their development.

By Therapy Type

By Application

By Vector Type (for Gene Therapy)

By Route of Administration

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar