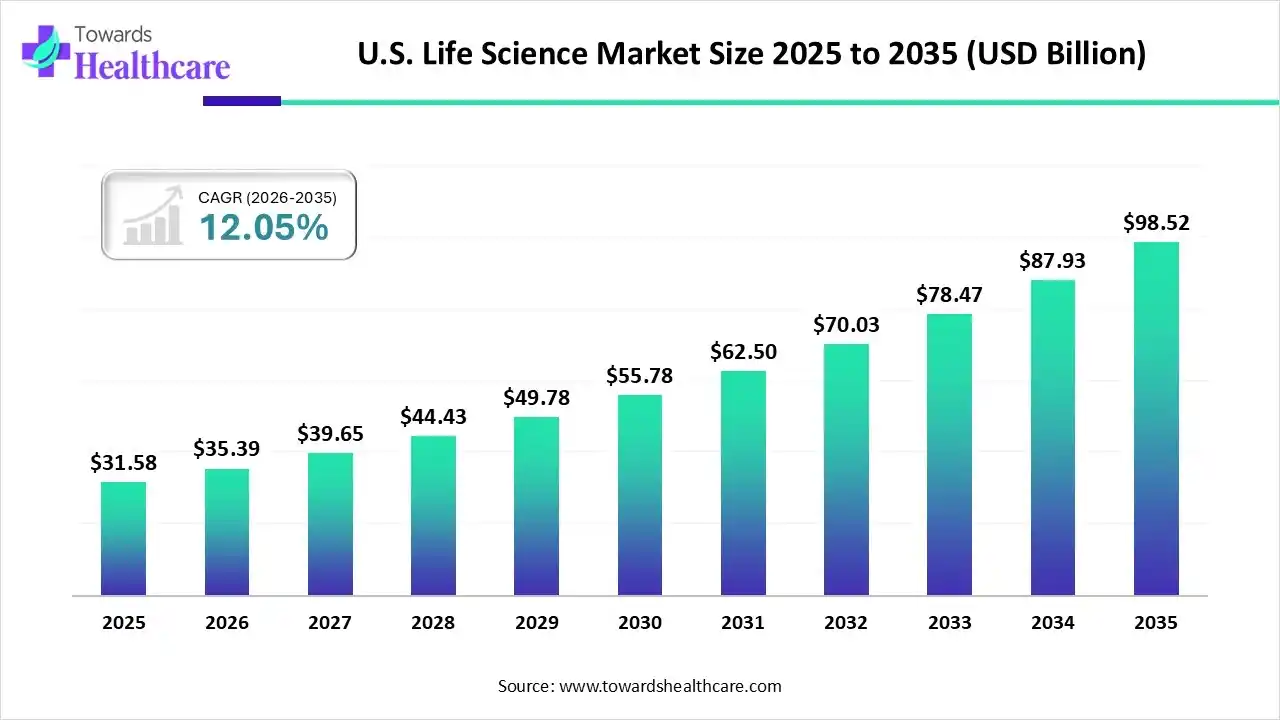

The U.S. life science market size in 2025 was US$ 31.58 billion, expected to grow to US$ 35.39 billion in 2026 and further to US$ 98.52 billion by 2035, backed by a robust CAGR of 12.05% between 2026 and 2035.

")

The future of technology and healthcare is significantly shaped by the life sciences sector. The industry is developing at an unprecedented rate thanks to the quick uptake of technologies like next-generation sequencing (NGS), CRISPR gene editing, and artificial intelligence (AI). The need for life sciences applications has increased significantly since the pandemic because to the increased emphasis on personalised treatment, early diagnosis, and preventative healthcare. The rising incidence of infectious and chronic illnesses, the growing need for personalised medicine and biologics, and biotechnology breakthroughs are some of the major reasons propelling the life sciences industry.

The U.S. life science market encompasses industries involved in the research, development, manufacturing, and commercialization of products and services aimed at improving human health and life processes. This includes sectors such as biopharmaceuticals, medical devices, diagnostics, laboratory technologies/instruments, genomics, contract services (CROs, CDMOs), and analytical tools & reagents (e.g., consumables, instrumentation, analytics, etc.).

Key Steps Taken by Market Players: The life science market in the U.S. is growing significantly due to the strong presence of key market players. These market players in the U.S. a taking key steps in drug discovery, therapy development, drug testing, precision medicine, etc.

For instance,

Growing R&D Activities

The R&D activities across the U.S. life science sector are increasing, driving advancements in diagnostics, personalized medicines, genomics, biologics, and biomarkers, where the growing R&D investments are also increasing their innovations.

Increasing Health Awareness

There is a rise in health awareness due to growing chronic diseases, which is increasing the demand for precision medicine, specialty drugs, and other novel treatment options, creating new opportunities for U.S. life sciences.

Healthcare Digitalization

The rapid digital transformation in the healthcare sector is increasing the adoption of various advanced technologies, which is accelerating and enhancing numerous U.S. life sciences processes, from drug discovery to their clinical trials.

The biological sciences are also seeing advancements thanks to artificial intelligence, a game-changing technology that is already changing organisations across industries. There is no denying AI's influence on the life sciences sector. Artificial intelligence is accelerating medication research and discovery, improving the efficiency of clinical trials, and establishing personalised medicine as a standard procedure.

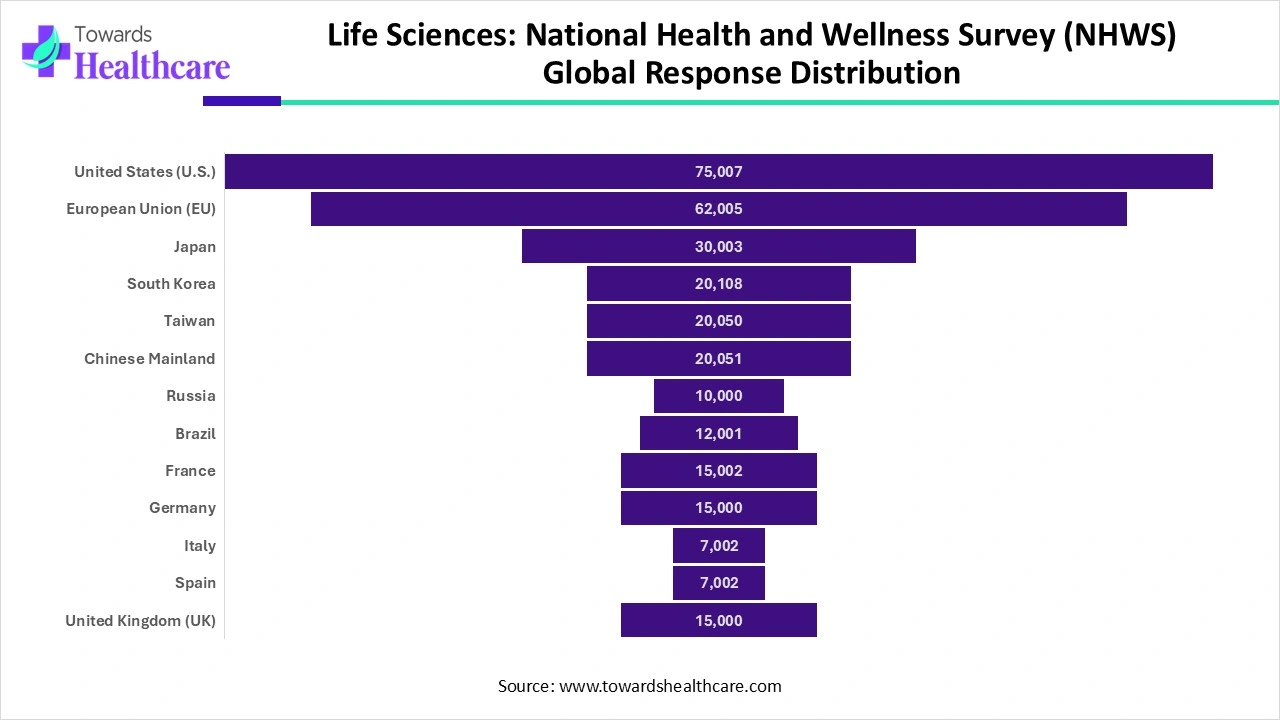

Global Response Distribution")

Rising Healthcare Needs are Driving the U.S. Life Science Market

An ageing population increases the prevalence of illnesses, which indicates a growing demand for cutting-edge medical technology, novel treatment approaches, and biotechnology solutions. The potential for investments, expansion, and development will only increase with the abundance of options. In addition, the growing prevalence of chronic illnesses like cancer is driving up healthcare demands.

Supply Chain Hindrance

Numerous reasons, such as geopolitical events and climate change, have brought attention to supply chains' present shortcomings and an excessive reliance on foreign suppliers or single production locations. Because of this and the effects of legislation, life sciences organisations need to reevaluate their supply chain strategy.

Precision Medicine Initiatives and Biopharma Research

The rise of the life science sector in the U.S. is being driven by innovation and research. New drug development platforms and diagnostic technologies are being invested in by biotechnology and pharmaceutical corporations. Spending on life science product R&D has surged globally, with a focus on targeted medicines and genomic medicine in particular. This funding grew as new infectious illnesses appeared and as companies created cutting-edge treatments and diagnostic tools. Demand is being driven by precision medicine and biomarker development, with a predilection for expensive equipment and very sensitive detection methods.

Because the life sciences sector uses a lot of energy and resources, it nevertheless has a significant influence on the environment. Specifically, the pharmaceutical sector contributes 4.4% of world emissions, and if left unchecked, its carbon footprint is expected to treble by 2050. As proponents of using knowledge to improve the world, researchers frequently have strong feelings about reducing climate change and its profound effects on ecosystem and human health. They want to reduce packaging, consumable, and hazardous waste as much as they can; increase lab energy efficiency; and prolong the life of their instruments before recycling or discarding them.

| Table | Scope |

| Market Size in 2026 | USD 35.39 Billion |

| Projected Market Size in 2035 | USD 98.52 Billion |

| CAGR (2026 - 2035) | 12.05% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product/Service, By Region |

| Top Key Players | Johnson & Johnson, Eli Lilly, AbbVie, Amgen, Thermo Fisher Scientific, IQVIA, McKesson Corporation, Regeneron Pharmaceuticals, Laboratory Corporation of America, Teva Pharmaceutical Industries, CSL Limited, Baxter International, Moderna, Novo Nordisk, Roche, Pfizer, Vertex Pharmaceuticals, BioMarin Pharmaceutical, Genmab, CRISPR Therapeutics |

")

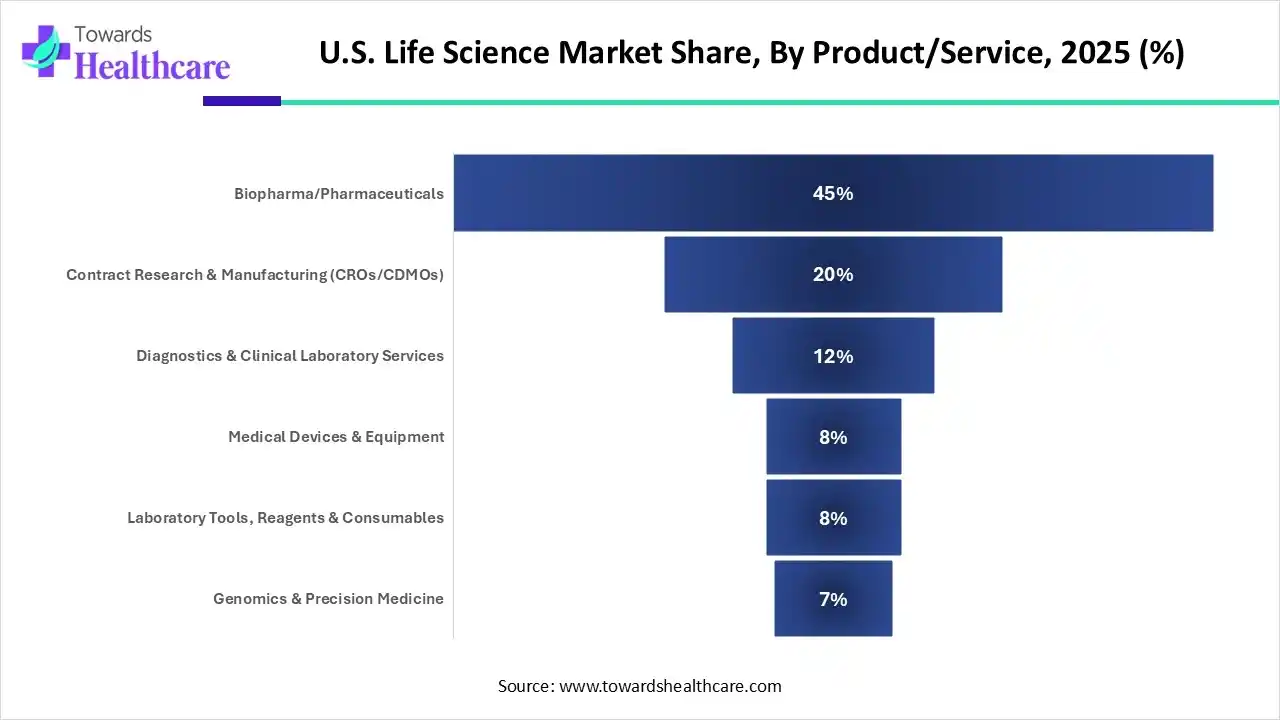

Why was the Biopharma/Pharmaceuticals Segment Dominant in the Market?

By product/service, the biopharma/pharmaceutical segment held the major share of the U.S. life science market by 45% in 2025. The desire for novel and life-saving treatments is driving organisations throughout the pharmaceutical and life sciences sectors to expand their investments in pharmaceutical and biopharmaceutical development. There is a general demand for high-value, application-appropriate solutions for big and small molecule analysis in these quickly changing sectors.

By product/service, the contract research & manufacturing (CROs/CDMOs) segment is expected to grow at the highest CAGR in the U.S. life science market during the upcoming time frame. The pharmaceutical, biotech, and medical device sectors rely heavily on CROs and CDMOs. Research, testing, refinement, manufacturing, and marketing of pharmaceuticals, drug products, and medical devices are all supported by CROs and CMOs for their clients. The CRO industry is becoming more competitive as leading CRO firms like Covance, Parexel, and IQVIA expand businesses' capabilities and worldwide reach through mergers and acquisitions.

In 2024, the life sciences sector in the U.S. had a very active year. As the public markets grew, there was a rise in venture capital and initial public offerings (IPOs), indicating a return of investor confidence and a continued interest in biotech research.

In the past two decades, clinical trials in the United States have expanded rapidly, and in 2024, the number of registered studies hit a new high. Although later-stage trials are often larger, life science businesses may require more room if their medications are in any stage of development. Although financing for clinical trials comes from a variety of sources, the National Institutes of Health and private investment are the main providers.

Through the third quarter of 2024, the FDA authorised 59 medications, setting a near-record year. The creation of new medications and therapies may be a game-changer for biotech firms, many of which require additional space for research, development, and production. Industry sources estimate that between 12 and 14 percent of medications that go through clinical trials are eventually approved by the FDA.

A significant component of the American life science ecosystem is federal financing for medical research and development. Therefore, it should come as no surprise that states with developed life sciences sectors receive the most NIH funding grants. In fiscal year 2024, 45.3% of NIH funding went to the top five states, with California at the top.

The global life science market is valued at US$ 88.2 billion in 2024, expected to grow to US$ 98.63 billion in 2025, and projected to reach about US$ 269.56 billion by 2034, expanding at a CAGR of 11.82%.

")

R&D

Clinical Trials and Regulatory Approvals

Packaging and Serialization

Distribution to Hospitals, Pharmacies

Patient Support and Services

Read further to see how top players are redefining the U.S. life science landscape: https://www.towardshealthcare.com/companies/us-life-science-company-profile

| U.S. Companies | Headquarters | Life Science Solutions |

| Eli Lilly | Indianapolis, IN | Mounjaro/Zepbound, Verzenio, and Donanemab |

| Pfizer | New York | Comirnaty, Padcev, and Paxlovid |

| Amgen | Thousand Oaks, CA | Enbrel, Repatha, and Lumakras |

| Gilead Sciences | Foster City, CA | Trodelvy, Biktarvy, and Veklury |

| Moderna | Cambridge, MA | mRNA-based cancer vaccines and Spikevax |

| AbbVie | North Chicago, IL | Humira and Skyrizi, Venclexta, and Imbruvica |

| Bristol Myers Squibb | Princeton, NJ | Opdiva, Revlimid, Eliquis, and Abecma |

| Regeneron | Tarrytown, NY | Dupixent, Libtayo, and Eylea |

| Intuitive Surgical | Sunnyvale, CA | da Vinci Surgical Systems |

| Illumina | San Diego, CA | NovaSeq 600/X Series |

In April 2025, Avner Schlessinger, PhD, Professor of Pharmacological Sciences and Associate Director of the Mount Sinai Centre for Therapeutics Discovery at the Icahn School of Medicine at Mount Sinai, who will serve as the Center's leader, says, "We at Mount Sinai are committed to redefining the future of medical innovation." Artificial intelligence combined with state-of-the-art biology and chemistry can significantly speed up drug development and create novel therapies for some of the most difficult and urgent illnesses.

By Product/Service

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar