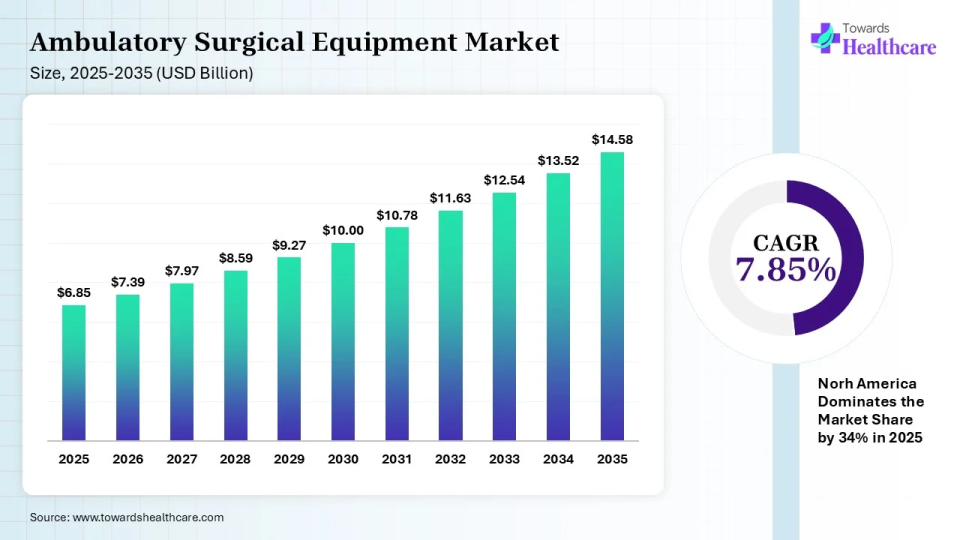

The global ambulatory surgical equipment market size was calculated at USD 6.85 billion in 2025 and is predicted to increase from USD 7.39 billion in 2026 to approximately USD 14.58 billion by 2035, expanding at a CAGR of 7.85% from 2026 to 2035.

")

Improvements in surgical technology and a greater focus on patient-centered care are driving the ambulatory surgical equipment market. Patient monitoring systems are essential for the recovery after ambulatory surgery because they allow for the real-time evaluation of vital signs and the early identification of problems. Protocols for outpatient surgery are standardising, with a primary emphasis on infection control and patient satisfaction measures.

The ambulatory surgical equipment market is driven by technological advancements and the inclusion of AR and VR. The ambulatory surgical equipment market includes medical capital equipment, consumables, and support systems used in ambulatory surgical centers (ASCs), outpatient/ambulatory surgery suites, and same-day procedure clinics. Includes surgical tables, OR lights, anesthesia machines & ventilators, patient monitors, electrosurgical units, endoscopy/laparoscopy towers and instruments, imaging & C-arm systems for intraoperative imaging, sterilization/washers, suction/aspiration, surgical power tools, patient positioning & transfer devices, warming & fluid-warming systems, instrument trays & disposables, HVAC/laminar flow solutions, plus installation, maintenance and value-added services tailored to outpatient surgical workflows.

Surgery is changing as a result of artificial intelligence (AI), which increases accuracy and improves patient outcomes. Real-time intraoperative navigation, precise preoperative planning, and efficient postoperative care are made possible by AI-driven technologies. Thanks to these developments, surgeons can now more accurately navigate intricate anatomical systems, make fewer mistakes, and use predictive analytics to improve recovery times.

Rising collaboration among key players: Major companies are collaborating in order to provide innovative products and market expansion.

For instance,

| Phase | Key Focus |

| Visioning | Establish a strategic direction in line with the demographic and therapeutic objectives. |

| Development of Equipment List | Determine the equipment requirements in conjunction with the clinical personnel. |

| Designing | Equipment should be integrated with facility design and legal requirements. |

| Procurement | Choose and purchase equipment according to compatibility, pricing, and quality. |

| Commissioning | Provide, set up, test, and prepare for operation |

| Continuous Maintenance | Over time, maintain, improve, and sustain the performance of the equipment. |

| Table | Scope |

| Market Size in 2026 | USD 7.39 Billion |

| Projected Market Size in 2035 | USD 14.58 Billion |

| CAGR (2026 - 2035) | 7.85% |

| Leading Region | North America by 34% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Product, By End User, By Deployment/Integration Level, By Technology/Connectivity, By Purchase Model/Commercial Model, By Region |

| Top Key Players | Arthrex, Baxter/Hillrom (patient support & perioperative solutions), B. Braun Melsungen AG, ConMed Corporation, Drägerwerk AG & Co. KGaA, GE Healthcare, Johnson & Johnson (Ethicon), Karl Storz, Medtronic, Olympus Corporation, Philips Healthcare, STERIS Corporation, Stryker Corporation, Smith & Nephew, Zimmer Biomet |

")

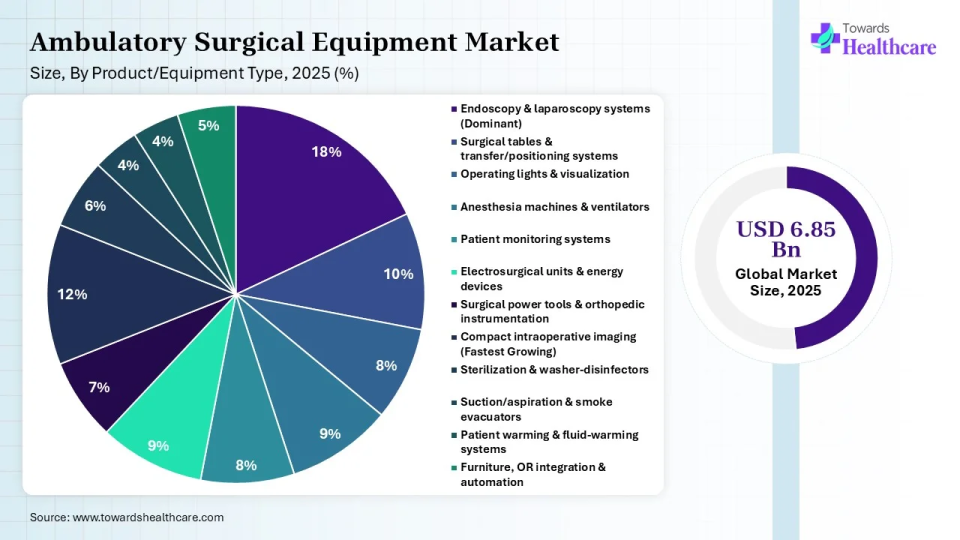

| Segments | Shares % |

| Endoscopy & laparoscopy systems (Dominant) | 18% |

| Surgical tables & transfer/positioning systems | 10% |

| Operating lights & visualization | 8% |

| Anesthesia machines & ventilators | 9% |

| Patient monitoring systems | 8% |

| Electrosurgical units & energy devices | 9% |

| Surgical power tools & orthopedic instrumentation | 7% |

| Compact intraoperative imaging (Fastest Growing) | 12% |

| Sterilization & washer-disinfectors | 6% |

| Suction/aspiration & smoke evacuators | 4% |

| Patient warming & fluid-warming systems | 4% |

| Furniture, OR integration & automation | 5% |

Explanation

Which Product/Equipment Type Segment Dominated the Market in 2025?

By product/equipment type, the endoscopy & laparoscopy systems segment held the largest share of the ambulatory surgical equipment market by 18% shares in 2025. Endoscopy and laparoscopy are both medical procedures that have both surgical and diagnostic purposes. These operations are less intrusive, require less time to recuperate after the treatment, and are less expensive than standard surgery.

By product/equipment type, the compact intraoperative imaging segment is estimated to be the fastest-growing during 2025-2034. These small, low-radiation, battery-powered imaging devices provide high-quality images and are especially useful for intraoperative imaging. It makes it possible to assess right away, guaranteeing the best possible implant location and enabling real-time adjustment if necessary.

")

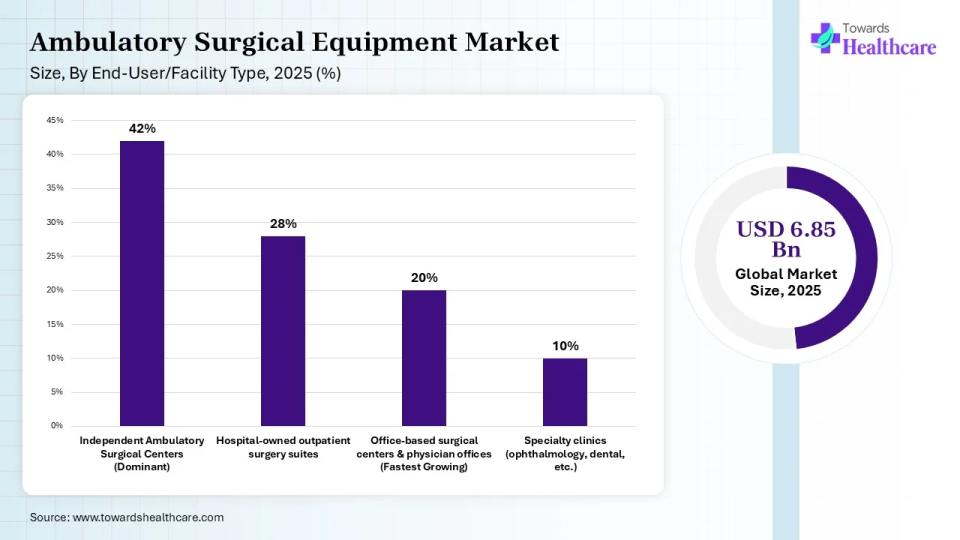

| Segments | Shares % |

| Independent Ambulatory Surgical Centers (Dominant) | 42% |

| Hospital-owned outpatient surgery suites | 28% |

| Office-based surgical centers & physician offices (Fastest Growing) | 20% |

| Specialty clinics (ophthalmology, dental, etc.) | 10% |

Explanation

Which End-User/Facility Type Segment Dominated the Market in 2025?

By end-user/facility type, the independent ambulatory surgical centers segment held the largest share 42% of the ambulatory surgical equipment market in 2025. Independent ASCs are state-of-the-art medical facilities dedicated to same-day surgery, as well as preventative and diagnostic medical services. With a proven track record of providing high-quality treatment and achieving favourable patient outcomes, ASCs have revolutionised the outpatient experience by providing a more affordable, individualised, and convenient option to hospitals.

By end-user/facility type, the office-based surgical centers & physician offices segment is estimated to be the fastest-growing during 2025-2034. Instead of handing up income to a hospital or surgery centre where they have little financial claim, office-based surgical practices allow doctors to invest in themselves. Physicians also have better quality of life and more control over their schedule.

")

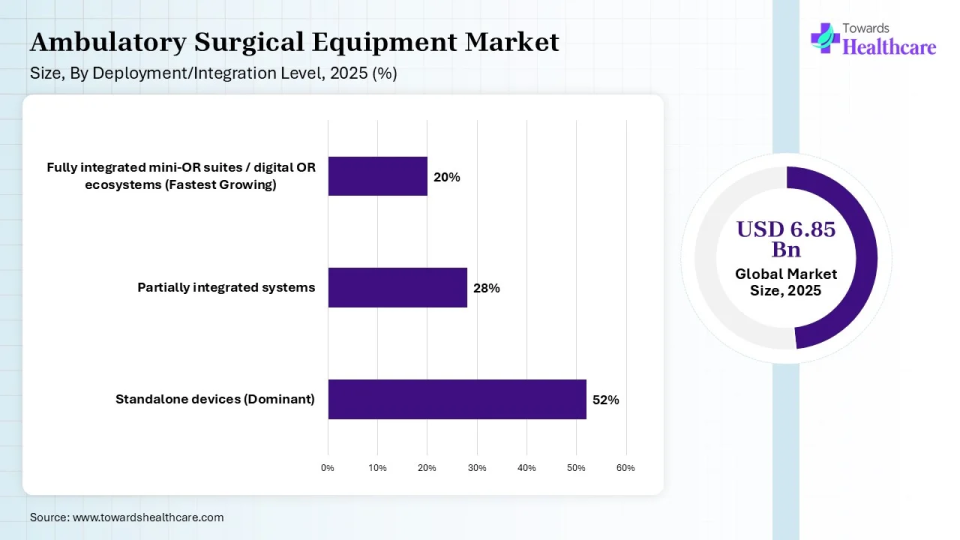

| Segments | Shares % |

| Standalone devices (Dominant) | 52% |

| Partially integrated systems | 28% |

| Fully integrated mini-OR suites / digital OR ecosystems (Fastest Growing) | 20% |

Explanation

Why was the Standalone Devices Segment Dominant in 2025?

By deployment/integration level, the standalone devices segment held 52% the largest share of the ambulatory surgical equipment market in 2025. All of the resources and parts required for standalone technologies are combined into a single device. This makes it possible to carry out its operations without relying on outside connections or dependencies. Standalone devices may function independently and are self-sufficient.

By deployment/integration level, the fully integrated mini-OR suites/digital OR ecosystems segment is estimated to be the fastest-growing during 2025-2035. A digital OR ecosystem is the whole, networked system of partners and technologies that coordinate patient care, whereas a fully integrated mini-OR suite is a small operating room with cutting-edge, linked technology. Within a hospital's wider, networked digital environment, the mini-OR operates as a single, incredibly effective unit.

")

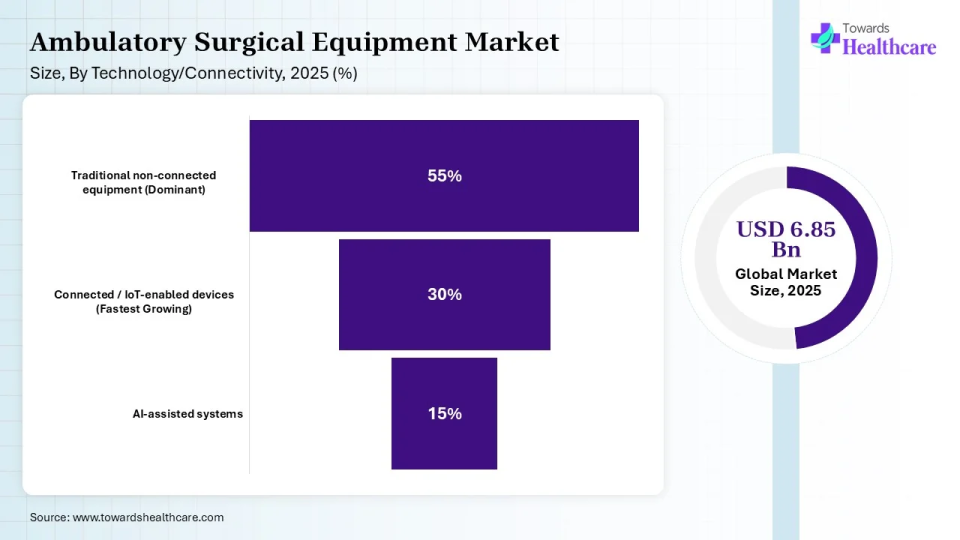

| Segments | Shares % |

| Traditional non-connected equipment (Dominant) | 55% |

| Connected / IoT-enabled devices (Fastest Growing) | 30% |

| AI-assisted systems | 15% |

Explanation

Which Technology/Connectivity Segment Dominated the Market in 2025?

By technology/connectivity, the traditional non-connected equipment segment held 55% the largest share of the ambulatory surgical equipment market in 2025. During outpatient care, this equipment is crucial for preserving accuracy, patient safety, and cleanliness. It differs from the large, intricate gear seen in a main hospital operating room.

By technology/connectivity, the connected/IoT-enables devices segment is estimated to be the fastest-growing during 2025-2034. Smart medical devices are connected by the Internet of Medical Things (IoMT), creating an integrated network that allows safe and unrestricted flow of healthcare data. By enabling device collaboration, this network makes monitoring, diagnostic, and treatment systems more intelligent. IoMT promotes individualised treatment and quicker responses by connecting healthcare systems and resources.

")

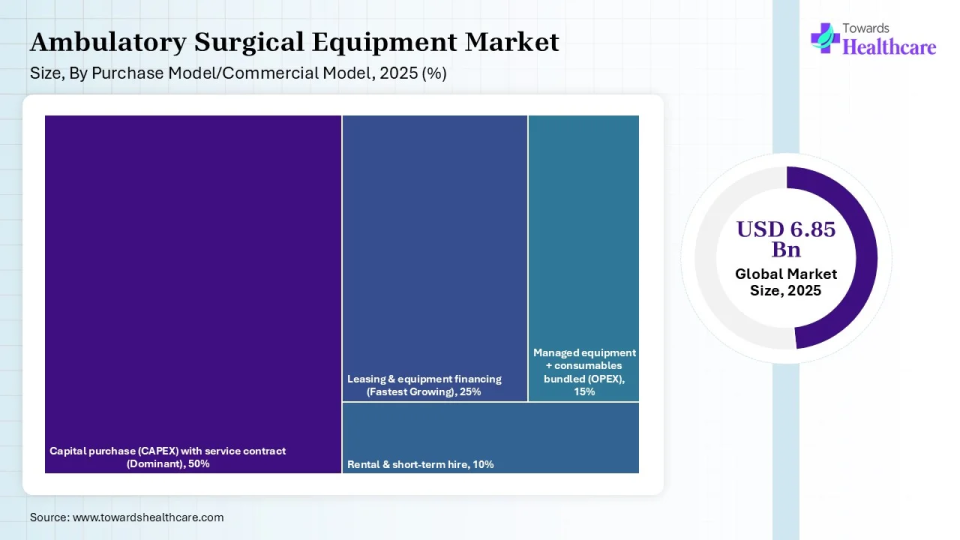

| Segments | Shares % |

| Capital purchase (CAPEX) with service contract (Dominant) | 50% |

| Leasing & equipment financing (Fastest Growing) | 25% |

| Rental & short-term hire | 10% |

| Managed equipment + consumables bundled (OPEX) | 15% |

Explanation

Which Purchase Model/Commercial Model Segment Dominated the Market in 2025?

By purchase model/commercial model, the capital purchase (CAPEX) with service contract segment held the largest share of the ambulatory surgical equipment market by 50% in 2025. In order to ensure a company's long-term growth and sustainability, capital spending is crucial. By extending their physical footprint, acquiring new technology, or replacing their antiquated equipment, it enables enterprises to keep their competitive edge.

By purchase model/commercial model, the leasing & equipment financing segment is estimated to be the fastest-growing during 2025-2034. Leasing has become a well-liked choice in recent years for ASCs looking to save costs up front. Healthcare practitioners can acquire specialist surgical instruments or cutting-edge diagnostic equipment through leasing arrangements without having to pay the entire purchase price up front. ASCs have more freedom to update as technology advances thanks to this strategy.

")

")

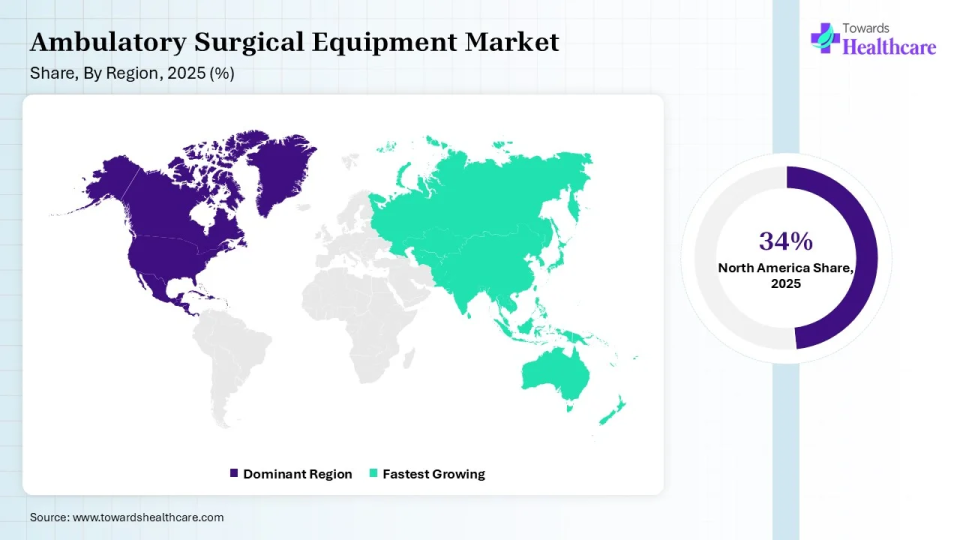

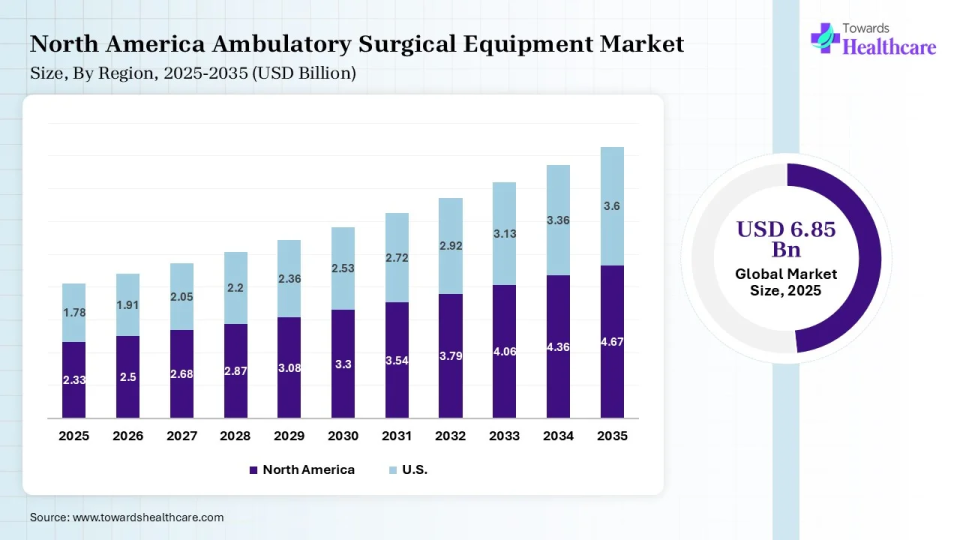

North America dominated the ambulatory surgical equipment market by 34% in 2025. This is explained by how quickly technologically advanced items are adopted in the area. Growing government funding for primary care and outpatient care expansion are the main drivers of the ambulatory surgery centre market's growth in North America.

U.S. Ambulatory Surgical Equipment Market Trends

In September 2025, Distalmotion and the Healthcare Equipment Finance business of First Citizens Bank established a new financing programme that would offer leasing and lending options for Distalmotion's cutting-edge robotic surgery equipment to hospitals, ambulatory surgical centres, and other healthcare providers. With more than $200 billion in assets, parent firm First Citizens BancShares, Inc. is a Fortune 500TM member and a top 20 financial institution in the United States.

Canada Ambulatory Surgical Equipment Market Trends

In June 2025, the number of privately financed community surgical and diagnostic facilities in Ontario is growing. The province is spending $155 million over the next two years to build 57 new sites for gastrointestinal endoscopy and MRI and CT scan services, according to Premier Doug Ford.

Asia Pacific is estimated to host the fastest-growing ambulatory surgical equipment market by 24% share during the forecast period. The growing incidence of chronic illnesses, the ageing of the population, and improvements in healthcare infrastructure are the main drivers of this development. Furthermore, it is anticipated that expanding nations like China and India, as well as the growing attention of industry players in these nations, would drive the regional sector.

R&D

Like all medical devices, ambulatory surgical equipment must go through a systematic research and development (R&D) process to guarantee that the final product is safe, efficient, and complies with legal requirements. The risk categorisation of the gadget determines how demanding the R&D process is; the most risky devices need the most thorough testing and certification.

Distribution to ASCs

Include determining the equipment needs strategically, acquiring and integrating it into facility layouts efficiently, and providing strong post-installation management, including training and maintenance, to guarantee patient safety and operational preparedness.

Patient Support and Services

An organised method that guarantees a patient's safety and wellbeing before to, during, and following an outpatient surgery is an ambulatory surgical equipment patient support and services plan. To maximise healing at home, steps include thorough pre-operative examination, thorough patient education, and diligent post-operative follow-up. Add this: Additionally, many ambulatory surgical centers emphasize the importance of having key medical and legal documents prepared before undergoing any outpatient procedure. Patients are increasingly encouraged to understand what to include in an advance directive form, as this document outlines their healthcare preferences and designates a trusted individual to make medical decisions on their behalf if needed.

By Product/Equipment Type

By End-User/Facility Type

By Deployment/Integration Level

By Technology/Connectivity

By Purchase Model/Commercial Model

By Region

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar