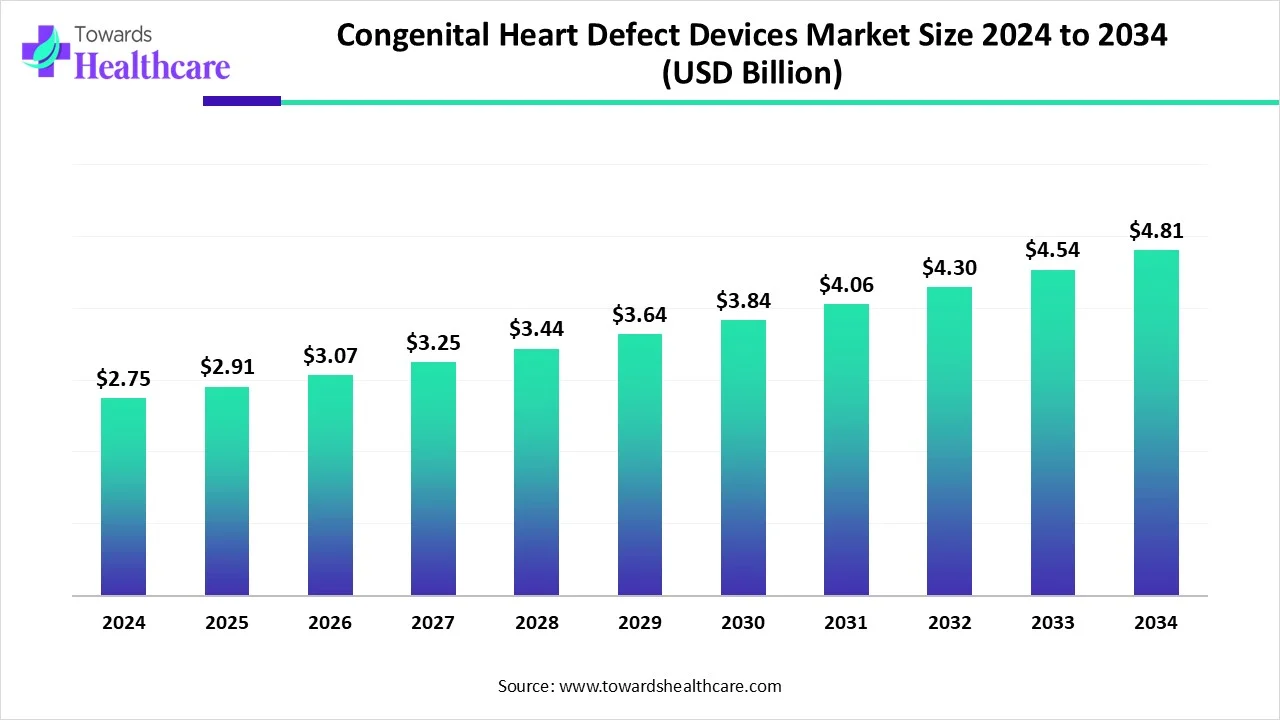

The global congenital heart defect devices market size is calculated at USD 2.75 billion in 2024, grew to USD 2.91 billion in 2025, and is projected to reach around USD 4.81 billion by 2034. The market is expanding at a CAGR of 5.74% between 2025 and 2034.

The congenital heart defect devices market is mainly driven by the rising prevalence of congenital heart diseases. The increasing risk of chronic disorders among pregnant women also potentiates the risk of such diseases in the infants. Owing to these, government organizations launch initiatives to encourage people to undergo prenatal screening and early diagnosis of congenital heart diseases.

The future of the market looks promising with advancements in medical technologies and the integration of AI and ML in medical devices. Advances in genomics and sequencing technologies also offer future growth opportunities to market players.

| Metric | Details |

| Market Size in 2025 | USD 2.91 Billion |

| Projected Market Size in 2034 | USD 4.81 Billion |

| CAGR (2025 - 2034) | 5.74% |

| Leading Region | North America |

| Market Segmentation | By Device Type, By Defect Type, By Technology Type, By Patient Group, By End-User, By Region |

| Top Key Players | Abbott Laboratories, AstraZeneca, Biotronik, BrightHeart, Edwards Lifesciences, GE Healthcare, Japan Lifeline Co., Ltd., Lepu Medical Technology (Beijing) Co., Ltd., Medstar Health, OpHeart, PFM Medical, Inc., Renata |

A congenital heart defect is a condition in babies related to the heart at birth. Some common defects are a hole in the heart valve, issues with blood vessels, and problems with heart valves that control blood flow. There are generally two types of congenital heart diseases: cyanotic and acyanotic congenital heart disease. These defects are usually caused by abnormal genetics, drinking alcohol or smoking during pregnancy, or taking medications for chronic disorders. The devices used to diagnose these disorders include an electrocardiogram (ECG), echocardiogram, heart catheterization, and MRI.

The rising prevalence of congenital heart defects and the increasing need for prenatal screening promote the market. Advancements in medical technologies have led to the development of innovative medical devices for the diagnosis and treatment of congenital heart defects. The rapidly expanding medical device sector and increasing investments by government and private organizations boost market growth.

Artificial intelligence (AI) plays a vital role in imaging, electrophysiology, interventional procedures, and intensive care monitoring of infants with congenital heart defects. Integrating AI in MRI and ECG enhances the efficiency of diagnosis and aids in imaging segmentation and processing. AI and machine learning (ML) algorithms analyze vast amounts of diagnostic data and improve anatomic diagnosis, reducing human errors. They can also assess cardiac function and predict long-term outcomes. They aid in real-time monitoring of patients’ conditions through heart devices, enabling healthcare professionals to get real-time insights into the infant’s heart functioning and make proactive decisions. AI and ML can also predict complications related to the device in an infant.

Rising Prevalence of Congenital Heart Defect

The major growth factor of the congenital heart defect devices market is the rising prevalence of congenital heart diseases. Heart defects are the most common form of congenital disorders, with the highest prevalence rate. According to a systematic review and meta-analysis report published in the Journal of Neonatal Nursing, about 2.78 per 1000 or 27.8 per 10,000 births are estimated to have congenital heart anomalies in infancy globally. (Source - Science Direct) Among all the different types of congenital heart diseases, a ventricular septal defect has the highest prevalence. These are mainly caused when the heart or blood vessels don’t form correctly in utero.

Lower Accessibility in Rural Areas

Some people living in developing and underdeveloped countries or in rural areas are unaware of prenatal screening. They also lack access to cutting-edge technologies and advanced medical devices for infants with congenital heart defects. This limits the use of such devices in infants from such areas, restricting market growth.

What is the Future of the Congenital Heart Defect Devices Market?

The future of the market is promising, driven by advances in genomics. The growing research and development activities encourage researchers to identify novel candidate genes in congenital heart diseases. This also helps them to better detect and characterize disease variants. The evaluation of epigenetic markers, such as DNA methylation, and the use of advanced long-read sequencing techniques offer immense potential for early diagnosis of congenital heart diseases. These efforts also enable researchers to develop novel medical devices for personalized treatment. Moreover, the use of miniature pacemakers potentiates the chance of minimally invasive surgery. The development of devices that elicit minimal or no immune response also offers future opportunities for scientists.

By device type, the catheters segment held a dominant presence in the market in 2024 and is expected to grow at the fastest CAGR in the market during the forecast period. This segment dominated because catheters increase the volume of blood flow into the heart’s chambers. Catheters can help surgeons repair heart defects without open-heart surgery. The growing demand for minimally invasive surgery promotes the use of catheters for congenital heart defects. They are used for a wide range of defects, including closing a hole in the heart, widening a narrowed vessel or stiff valve, and closing abnormal blood vessels.

By device type, the pacemakers segment is expected to witness significant growth in the market over the forecast period. Many researchers are developing novel pacemakers to enhance their functioning and reduce complications in patients. Pacemakers are used to regulate the heart’s electrical signals and ensure it beats at a normal rate and rhythm. Innovative techniques are developed to implant pacemakers even without the need for minimally invasive surgery. This enhances patient comfort and leads to shorter recovery times.

By defect type, the ventricular septal defect segment dominated the market in 2024 and is expected to grow with the highest CAGR in the market during the studied years. The segment dominated due to the rising prevalence of ventricular septal defect (VSD) and its increasing severity. VSD is the most common condition among infants with congenital heart disease, and occurs when the wall between the two ventricles does not develop fully. The CDC reported that every year, 16,800 babies are born with a VSD in the U.S.

By defect type, the tricuspid atresia segment is expected to show lucrative growth in the market in the coming years. Tricuspid atresia is the second most common congenital heart defect that results in cyanosis due to the absence of communication between the right atrium and ventricle caused by agenesis of the tricuspid valve. It is estimated that around 1.2 per 10,000 babies are born with tricuspid atresia in the U.S. annually. The major causes of tricuspid atresia are genetic factors and abnormal heart development during pregnancy.

By technology type, the self-expanding closure devices segment dominated the global market in 2024 and is expected to expand rapidly in the market in the coming years. The rising prevalence of congenital heart disorders and technological advancements boost the segment’s growth. Self-expanding devices are usually made of nitinol (nickel-titanium alloy) or woven wires. They possess the ability to automatically close the hole in the heart. They are also used to seal blood vessel puncture sites after heart surgeries. Self-expanding devices eliminate the need for extra requirements, such as a balloon or other expansion mechanism.

By technology type, the mechanical closure devices segment is expected to grow notably over the coming years. Mechanical closure devices require a mechanical approach to close a puncture site. The most common type of mechanical closure device is the vascular closure device, which is primarily used for the closure of the femoral artery access site. The demand for vascular closure devices, due to an excellent operational success rate, lower vascular and puncture site complications, and reduced patient time to ambulation, improving patient comfort.

By patient group, the pediatric segment held the dominant share of the market in 2024. The pediatric segment dominated due to the increasing risk of congenital heart defects in children and the need for prenatal screening. These defects cause problems in a baby’s development. Timely diagnosis and treatment of these disorders in pediatric patients can improve the quality of life of individuals and reduce the risk of long-term health issues. Heart defects are easier to deal with in infancy or early childhood.

By patient group, the adults segment is estimated to grow at the fastest rate in the forecast period. Complete cure of congenital heart disorders is difficult, and hence, most adults suffer from such disorders. Further surgery or catheter interventions are necessary in adult populations with congenital heart diseases. Some diseases need to be treated only after a patient reaches a certain age, or once their organs are fully grown and developed. Numerous researchers are working on developing stents and other devices that grow with aging. One such example is the recently FDA-approved Minima stent.

By end-user, the hospitals segment registered its dominance over the global market in 2024 and is expected to grow at the fastest rate during the coming years. The segmental growth is attributed to the presence of skilled professionals and advanced healthcare infrastructure. The availability of suitable capital investment also facilitates the adoption of advanced instruments for the diagnosis and treatment of congenital heart disorders. Patients mostly prefer hospitals due to favorable reimbursement policies, which increases the accessibility for a larger patient population.

North America held a major revenue share of the market in 2024. The presence of key players and the growing awareness of prenatal screening are the major growth factors of the market in North America. The increasing cases of congenital heart defects and the rising adoption of advanced technologies lead to the use of devices. Several government organizations also launch initiatives to promote prenatal screening and treatment of congenital disorders.

The Centers for Disease Control and Prevention (CDC) estimates that around 1% of about 40,000 births per year are affected by heart defects. Key players, such as Abbott Laboratories, AstraZeneca, and Medstar Health, majorly contribute to market growth in the U.S. Annually, more than 2 million women undergo prenatal screening in the U.S.

The prevalence rate of congenital heart disorders in Canada is 12.3 per 1,000 births every year, accounting for approximately 4,400 babies affected out of an annual birth tally of 358,000. (Source - Born Ontario) Currently, 257,000 people are living with CHD in Canada.

Asia-Pacific is expected to witness the fastest CAGR of growth in the congenital heart defect devices market during the predicted timeframe. The growing research and development activities and increasing collaborations among academic researchers and key players augment market growth. The increasing population and sedentary lifestyles raise the risk of developing congenital disorders in neonates. Numerous government and private organizations held seminars and conferences to create awareness among the general public about prenatal screening and diagnosis of congenital disorders.

In China, the proportion of pregnant women undergoing non-invasive prenatal testing is approximately 25% to 49%. (Source - hiro)The birth rate in China was 6.77 per 1,000 people in 2024, an increase of 0.38 per 1,000 from 2023. In April 2025, the 2025 National Congenital Heart Disease (CHD) Surgery Conference was held at the Nanjing International Expo Convention Center.

The Indian government launched the “Unique Methods of Management and Treatment of Inherited Disorders” (UMMTID) initiative to ensure proper treatment for children and create awareness amongst the masses, and find solutions for all disorders. It is estimated that approximately 29 million live births were reported in India in 2024.

Europe is expected to grow at a notable CAGR in the congenital heart defect devices market in the foreseeable future. The presence of a robust healthcare infrastructure and favorable government support boosts the market. The increasing awareness of the early diagnosis of congenital disorders also favors market growth. In May 2025, the Trump Administration abruptly stopped the funding of a $6.7 million grant for a research project developing heart pumps for newborns. This shows positive signs for the European market due to the presence of state-of-the-art research and development facilities and increasing investments by government and private organizations.

The German government formed the “Competence Network for Congenital Heart Defects”, a network structure that enables reliable and independent research. About 6,000-7,000 children are born with a congenital heart disease annually. Currently, 300,000 people are living with this disorder across Germany. (Source - Kompetenzntez)

Christopher Gordella, Chief Technical Officer for BrightHeart, commented that most congenital heart defects occur in pregnancies that are considered low risk. This is because most of the patients visit an OB-GYN instead of a maternal-fetal medicine subspecialist. The company’s AI software helps elevate detection rates, even among non-specialists, and drive earlier diagnosis to improve outcomes. (Source - News Medical Life Science)

By Device Type

By Defect Type

By Technology Type

By Patient Group

By End-User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar