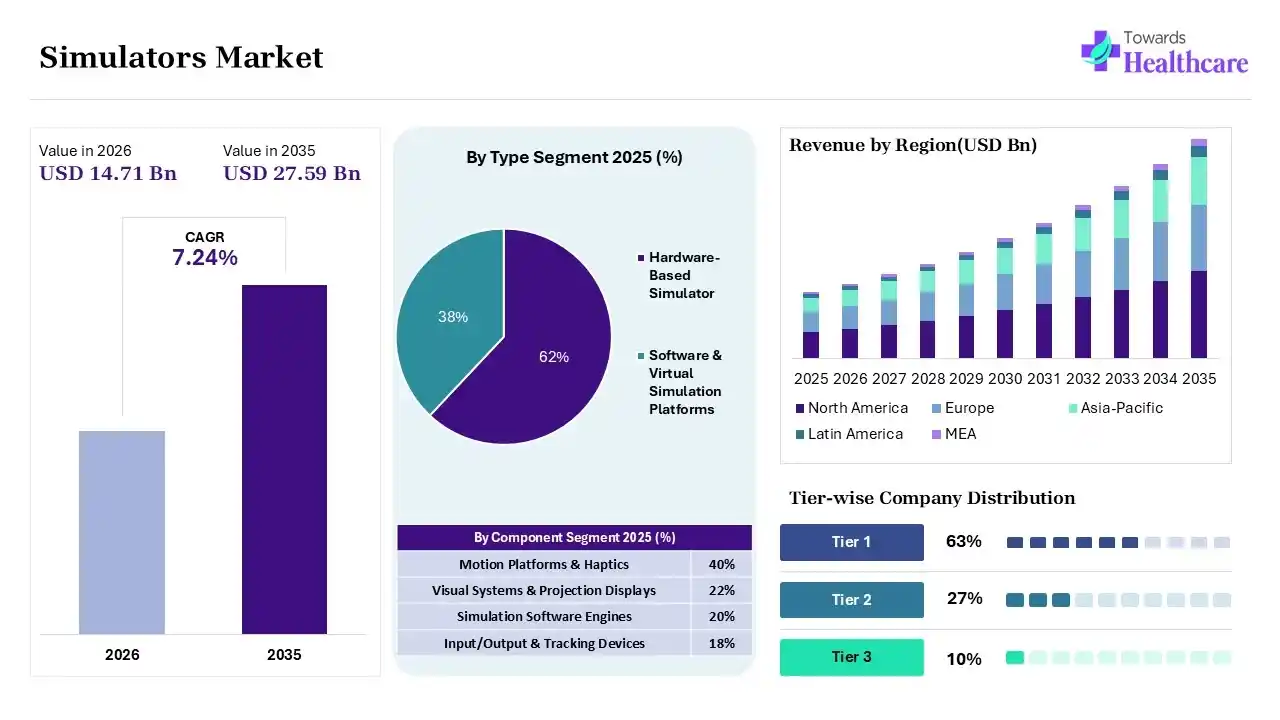

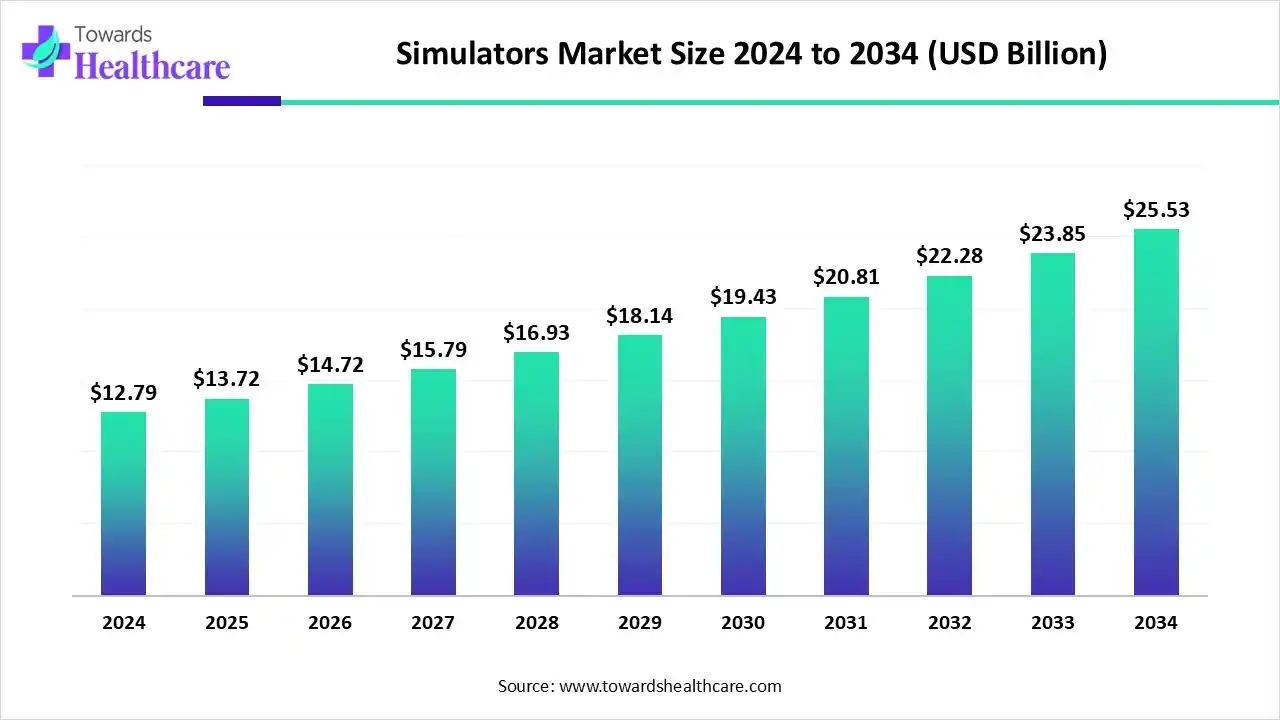

The global simulators market size is calculated at US$ 13.72 billion 2025, grew to US$ 14.71billion in 2026, and is projected to reach around US$ 27.59 billion by 2035. The market is expanding at a CAGR of 7.24% between 2026 and 2035.

Diverse Indian, Chinese, and Indonesian hospitals are fostering the adoption of hands-on training options, including innovative virtual reality simulators and other platforms in the simulators market. Moreover, the emergence of advanced haptic devices is providing tactile sensations to replicate the feel of real-life procedures, which are utilized in surgical and procedural training. These developments are further integrating with various technologies, like AI, VR/AR/XR, and hardware (cockpits, haptics, sensors), which promote novel applications in the medical and healthcare sector.

The simulators market refers to systems and platforms that replicate real-world conditions to train personnel, test equipment, or analyze scenarios in a safe, controlled, and cost-efficient environment. Market growth is driven by rising safety requirements, cost savings in training, technological advances (VR/AR, AI-based adaptive learning), and increased adoption across defense, civil aviation, automotive, healthcare, and energy sectors. These include flight, driving, military, medical, maritime, and industrial process simulators. Simulators integrate hardware (cockpits, haptics, sensors), software, AI, and extended reality (XR/VR/AR) technologies to deliver immersive training and analytics.

Focus On Patient Safety

The focus on enhancing patient safety is increasing the adoption of the simulator across hospitals and institutes to reduce clinical errors and enhance patient outcome along with professional development by offering risk free environment.

Increasing Applications

The growing application of the simulators across emergency care, trauma care, nursing skill development, obstetrics training, cardiovascular procedure training, disaster preparedness training, and interdisciplinary team-based simulations are also increasing their adoption rates.

Growing Training Programs

The growing number of healthcare professionals is increasing the use of simulators, where their growing medical and nursing training programs are also increasing their adoption rates for educational purposes and skill enhancements, which are further supported by healthcare investments.

Growing Technological Innovations

The technological advancements are driving the development of new cloud-based simulation platforms, along with the adoption of AR and VR technologies to enhance accessibility, learning outcomes, and remote medical training.

In the respective market, the empowerment of AI algorithms in supporting realistic dialogue with virtual characters, tailored learning pathways that adapt to user proficiency, and the application of generative design for quicker concept exploration in engineering and product development. Additionally, the widespread adoption of Large Language Models (LLMs) in creating realistic, dynamically responding virtual patient dialogues, simulating patient anxieties, and improving communication skills, which are significant in healthcare.

Driver

A Surge in Healthcare Expenses & Other Developments

Primarily, various regions are widely contributing their major role in expanding healthcare expenditures, and they are highly seeking to lower hospital stays and complications. This further makes simulations an affordable choice with a strong training method in the global simulators market. Ongoing technological advances in Virtual Reality (VR) and Augmented Reality (AR) platforms are evolving innovative and engaging approaches for health education. Moreover, a rise in demand for minimally invasive procedures is fostering the use of medical simulators for training surgeons in complex surgical procedures.

Restraint

Greater Initial Investment

A major challenge in the market is the need for a high initial investment for high-fidelity simulators and the necessary equipment, such as monitoring systems and synthetic fluids. This mainly possesses a price of up to $200,000. Operating these labs also incurs crucial operational costs for maintenance, updates, and consumables.

Opportunity

Breakthroughs in Cloud-based Platforms & AI

During 2025-2034, the global simulators market will encompass diverse opportunities in advancing cloud-based platforms and AI solutions. This will assist in moving from hardware-centric models to flexible, cloud-driven platforms, which will offer extensive training beyond conventional campus settings. In the case of AI, it will be employed in the assessment and analysis of clinician performance, facilitating feedback and transforming skill acquisition. However, current use of sophisticated haptic devices will offer tactile sensations to replicate the feel of real-life procedures, which are vital for surgical and procedural training.

| Table | Scope |

| Market Size in 2026 | USD 14.71 Billion |

| Projected Market Size in 2035 | USD 27.59 Billion |

| CAGR (2026 - 2035) | 7.24% |

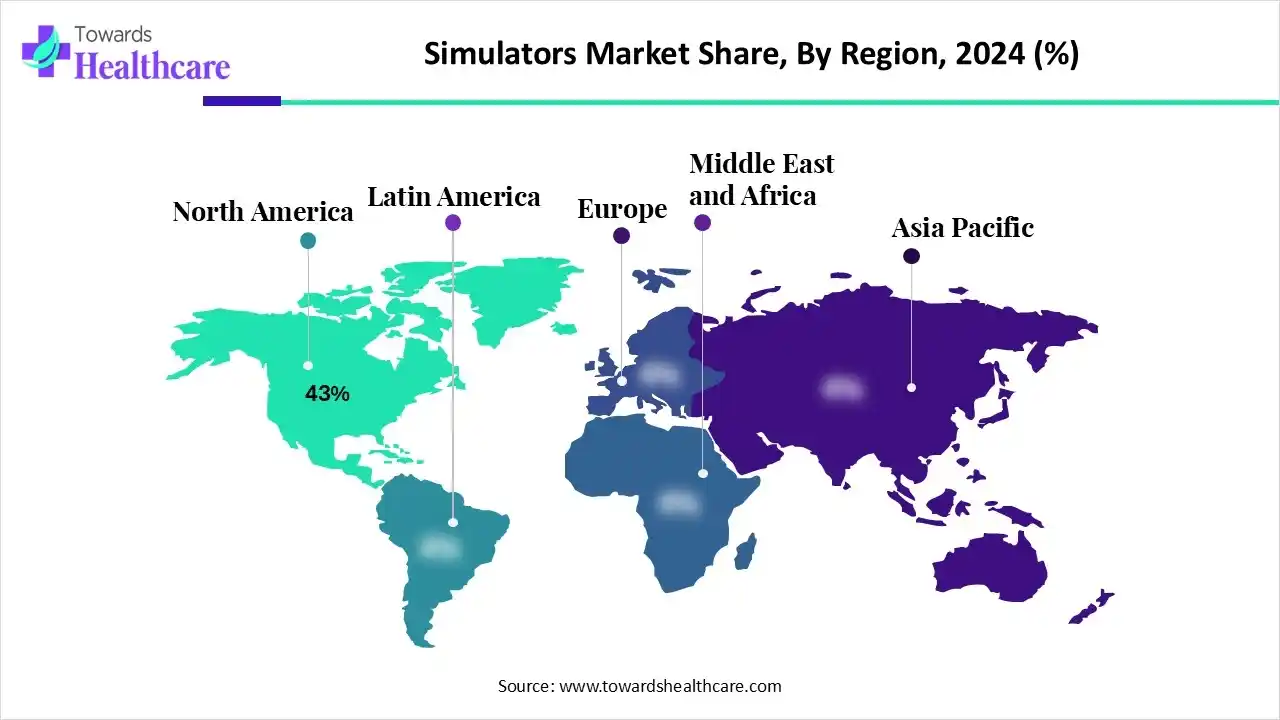

| Leading Region | North America by 43% |

| Key Applications | Flight Training, Military Training, Maritime Simulation, Driving Simulation, Medical Simulation, Industrial Process Training, Emergency Response Training |

| Primary End Users | Airlines, Defense Forces, Healthcare Institutions, Maritime Operators, Automotive Companies, Educational Institutions, Industrial Enterprises |

| Key Growth Drivers | Defense modernization, pilot shortages, aviation safety regulations, VR/AR integration, digital twins, autonomous systems training |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Type, By Application/End Market, By Technology, By Component, By End User, By Region |

| Top Key Players | Gaumard Scientific, Surgical Science Sweden, Limbs & Things Ltd., 3D Systems, Inc., Inovus Medical, 3B Scientific GmbH, Biomed simulation, Operative Experience Inc. |

")

| Segments | Shares % |

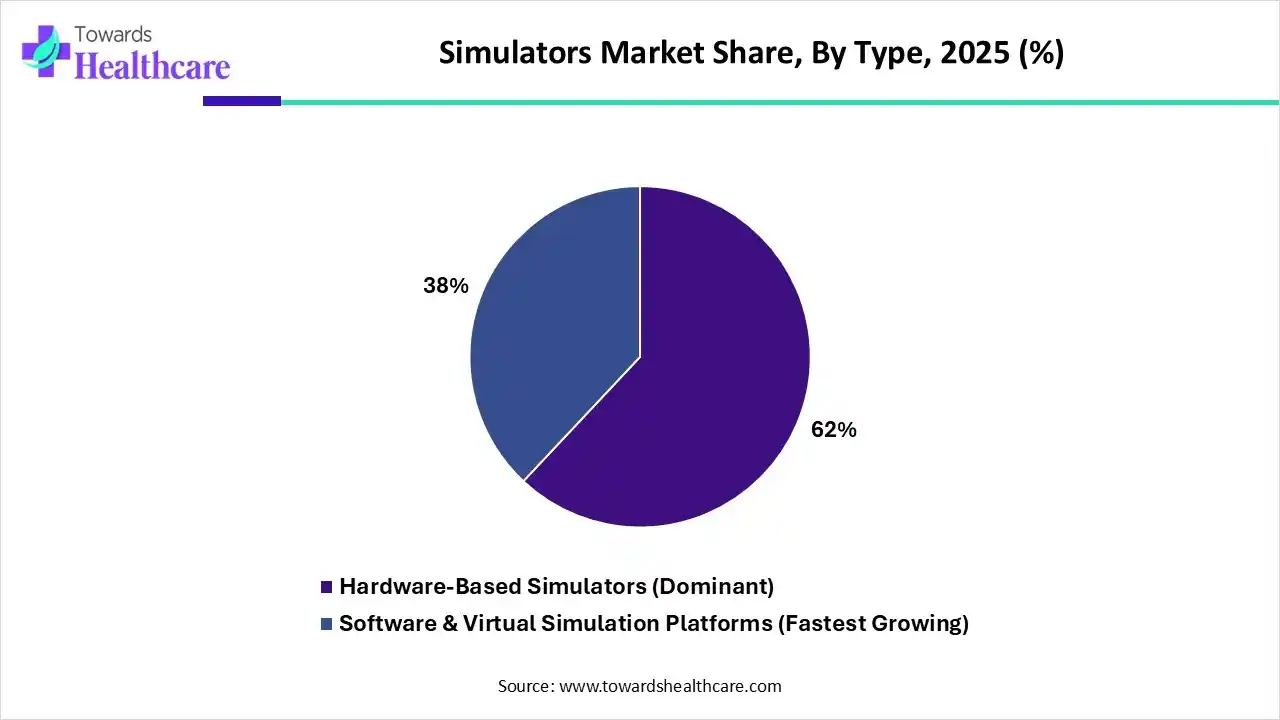

| Hardware-Based Simulators (Dominant) | 62% |

| Software & Virtual Simulation Platforms (Fastest Growing) | 38% |

Why did the Hardware-Based Simulators Segment Dominate the Market in 2025?

In 2025, the hardware-based simulators segment accounted for nearly 62% share of the simulators market. The segment is mainly driven by a growing emphasis on the reduction of medical errors and enhancing patient outcomes through hands-on practice in a risk-free environment. Moreover, the emergence of this type in the accelerating aging population, which needs specific training, and the progression of military and emergency response simulation programs. Currently, 3D printing for anatomical models and Computational Modeling and Simulation (CM&S) are increasingly used for medical device development and patient-specific planning.

Although the software & virtual simulation platforms segment will expand with the highest CAGR in the coming era, factors like the wider need for improvements in patient safety, addressing the increasing complexity of medical procedures, and boosting the quality of medical education and training will fuel further market expansion. These kinds of platforms are providing vast, comprehensive libraries of reviewed clinical scenarios, with user-friendly tools to evolve and personalize unique, situation-specific training modules.

| Segments | Shares 2025 % |

| Aerospace & Defense | 32% |

| Healthcare & Medical Simulation | 18% |

| Automotive & Transportation | 14% |

| Industrial & Energy | 12% |

| Maritime | 10% |

| Education & Research | 14% |

Which Application/End Market is Growing in the Simulators Market in 2025?

The healthcare & medical Simulation segment held the second-largest share of the market by 18% in 2025, which was approximately 18%. The segment is mainly propelled by the increasing focus on the reduction of medical errors, a lack of well-trained healthcare professionals, and the need for standardized training. Involvement of the latest approaches, such as the Next Generation Harvey, a cardiopulmonary simulator that possesses optimized physical exam features and peripheral pulses, patient communication in trauma situations, and the management of a variety of communities. Alongside, the adoption of high-fidelity human patient simulators, virtual dissection tables, and electronic medical record simulations to practice workflows is also bolstering the comprehensive solutions in this segment.

Whereas, the education & research segment is expected to grow at the highest CAGR in the simulators market in the studied years. Certain regions are facing a lack of healthcare professionals, for which medical institutions are widely adopting competency-based training models, which are perfectly aligned with simulation-based education. This further accelerates skill assessment and mastery in a standardized manner. Continuous application of VR/AR and AI is supporting simulation in several fields, mainly STEM education and teacher training, while also emphasizing boosting global access to simulation-based training.

| Segments | Shares % |

| Traditional Motion & Hardware-Driven Simulation (Dominant) | 54% |

| Virtual Reality (VR) Simulation (Fastest Growing) | 20% |

| Mixed Reality (MR) & Extended Reality (XR) | 14% |

| Artificial Intelligence & Digital Twin-Based Simulation | 12% |

How did the Traditional Motion & Hardware-Driven Simulation Segment Dominate the Market in 2025?

In 2025, the traditional motion & hardware-driven simulation segment led with nearly 54% share of the simulators market. The segment is propelled by the greater need for affordable and realistic training, and the breakthrough of hardware technologies, including high-fidelity manikins and motion platforms. Majorly, high-fidelity mannequins are led by Laerdal and Harvey, which offer realistic physiological responses, consisting of palpable pulses, heart and lung sounds, and reactive eyes, expanding realism for different clinical skills.

And, the virtual reality (VR) simulation segment will witness rapid growth with the highest CAGR. Currently, sophisticated VR solutions are being employed for pre-operative planning to improve surgical accuracy and minimize errors, and also facilitate non-invasive therapy options for patients. The greater adoption of VR simulations in specialized areas comprises EYESI, which enables modular training for diverse ophthalmic surgeries. Also, the training for complex procedures like ultrasound-guided regional anesthesia (UGRA) provides a safer and more effective learning environment for interns.

| Segments | Shares % |

| Motion Platforms & Haptics (Dominant) | 40% |

| Visual Systems & Projection Displays | 22% |

| Simulation Software Engines (Fastest Growing) | 20% |

| Input/Output & Tracking Devices | 18% |

Which Component Held a Major Share of the Simulators Market in 2025?

The motion platforms & haptics segment accounted for approximately 40% revenue share of the market in 2025. A surge in demand for robotic surgical systems is assisting the expansion of haptic feedback systems, as they are important for replicating the sensation of touch and force during robotic procedures. Recent transformations include compact and high-resolution haptic actuators like vibrotactile and shape memory alloy (SMA) systems, the integration of Extended Reality (XR), which further escalates scalability and assessment.

The simulation software engines segment will expand rapidly during the forecast period. Involvement of different engines, like physiology engines, which offer core physiological models and behaviors, enabling simulations to precisely demonstrate bodily functions and reactions to interventions. As well as the contribution of 3D modeling and rendering are using tools like iMSTK with 3D Slicer are employed in the establishment of insightful 3D anatomical models from medical scans for realistic visualization.

| Segments | Shares % |

| Defense & Military Training Centers (Dominant) | 38% |

| Commercial Aviation Training Organizations | 20% |

| Automotive OEMs & Testing Labs | 14% |

| Industrial / Energy Companies | 12% |

| Hospitals & Medical Universities (Fastest Growing) | 10% |

| Academic / Research Institutions | 6% |

Which End-User Segment is Expected to Achieve the Fastest CAGR?

The hospitals & medical universities segment is expected to expand at the highest CAGR in the simulators market by 10% during 2026-2035. Incorporation of greater healthcare demand, global healthcare workforce limitations, technological advancements in AI and VR/AR, and regulatory landscapes for expanded training standards are propelling the overall growth. Hospitals are putting efforts into realistic setups of intensive care units, operating rooms, or emergency bays equipped with actual medical equipment. Universities are emphasizing digital anatomy tables to represent 3D datasets of the human body, attributed to anatomy teaching, surgical planning, and even virtual autopsies.

")

Due to the presence of strong defense, aviation training, and advanced VR development, North America dominated with nearly 43% share of the market in 2025. The leading players are focusing on revolutionary digital twin technology to enable real-time process simulation and modeling of complex systems, such as nuclear power plants, expanding training and operational planning.

For instance,

U.S. Simulators Market Trends

In September 2025, Anatomy Warehouse, a leading distributor of anatomical education tools, partnered with Erler-Zimmer to foster innovative 3D printed anatomical models to schools and training facilities across the U.S.

Canada Simulators Market Trends

In June 2025, New Georgian, Brightshores collaborated to advance palliative care simulation training to a diverse group of health care providers in Grey-Bruce

Ongoing civil aviation expansion, healthcare simulation adoption, and defense modernization in the Asia Pacific are predicted to expand at a nearly 22% CAGR in the simulators market. Moreover, a significant contribution of OCTET Training Systems in Singapore is merging inexpensive simulation tools, which are specifically advantageous for healthcare systems with developing infrastructure. Additionally, the widespread adoption of simulators in Indian, Chinese, and Indonesian hospitals for hands-on training is also influencing the comprehensive market transformation.

China Simulators Market Trends

In September 2025, Shanghai-based Zhongshan Hospital, affiliated with Fudan University, launched its Meta Medical Simulation Laboratory is shifting towards intelligent healthcare and detailed its exploration of the meta-medical field.

India Simulators Market Trends

In December 2024, Fujifilm India, a company in medical technology, launched the innovative Mikoto Colon Model, a cutting-edge endoscopy simulation technology, in Chennai.

In this era, Europe is experiencing a notable growth in the simulators market. Primarily, this region's population is increasingly stepping towards hybrid learning models, which encompass the integration of e-learning with hands-on simulation to accelerate reach and feasibility for healthcare workers. Along with this, European governments are facilitating incentives for digital medical education and access to EU funding through public-private collaborations that bolster a dynamic innovation ecosystem.

For instance,

UK Simulators Market Trends

The growing clinical training and focus on patient safety are increasing the adoption of simulators in the UK. Moreover, to overcome the shortage of skilled personnel, their use is increasing, where the growing technological advancements and healthcare investments are also driving their innovations.

MEA is expected to grow significantly in the simulators market during the forecast period, due to expanding healthcare infrastructure, which is increasing the adoption of simulators to improve clinical training. The growing government initiatives, training programs, collaboration, and technological advancements are also increasing their adoption, enhancing the market growth.

Saudi Arabia Simulators Market Trends

The expanding healthcare infrastructure is increasing the demand for skilled personnel, which is increasing the use of simulators in Saudi Arabia. The growing healthcare digitalization is also increasing their adoption as well as encouraging their innovations, which are further supported by government investments.

South America is expected to show lucrative growth in the simulators market during the forecast period, due to increasing focus on the patients' safety, where the simulators are being utilized to enhance their outcomes. Additionally, increasing demand for skilled personnel and minimally invasive treatment options are also increasing their use, promoting market growth.

Brazil Simulators Market Trends

The growing medical training centres across Brazil are increasing the use of simulation to reduce medical errors and enhance quality care. They are also being used to enhance surgical skills, where the growing development of advanced simulation tools is also increasing their adoption rates.

| Ecosystem Category | Key Participants | Role in Market |

| Technology Providers | Thales, CAE, RTX Collins Aerospace, Saab | Develop simulation technologies, visual systems, AI-based training platforms |

| Product Manufacturers | CAE, L3Harris, Rheinmetall, Boeing, Indra | Manufacture full-mission simulators and training systems |

| Service Providers | FlightSafety International, CAE Training Services, SIMCOM | Deliver training, certification, and simulator-based education |

| Platform Providers | CAE, Boeing, Thales, Saab | Provide integrated simulation ecosystems and training environments |

| Software Vendors | Ansys, Siemens Digital Industries, Presagis, VSTEP | Develop simulation software, modeling tools, and digital twin platforms |

| Research Institutions | NATO STO, U.S. Naval Research Laboratory, DLR Germany | Conduct simulation research and validation studies |

| End-User Industries | Aviation, Defense, Healthcare, Maritime, Automotive, Energy | Utilize simulators for training, testing, certification, and operational readiness |

| Tier 1 | Tier 2 | Tier 3 | |

| Competitive Influence Share | 63% | 27% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| CAE Inc. | Saint-Laurent, Quebec | Canada | World's leading simulation and training company with extensive aviation and defense simulator footprint | Full Flight Simulators, Military Training Systems, Healthcare Simulators |

| L3Harris Technologies | Melbourne, Florida | USA | Major defense and aviation simulation provider | Flight Simulators, Mission Rehearsal Systems, Tactical Training |

| Thales Group | Paris | France | Global defense and aerospace simulation leader | Military Simulators, Flight Training Systems, Synthetic Environments |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Saab AB | Stockholm | Sweden | Strong military training and combat simulation portfolio | Live-Virtual-Constructive (LVC) Simulation |

| Rheinmetall AG | Düsseldorf | Germany | Major military and vehicle simulator supplier | Land Combat Simulators, Tactical Training Systems |

| Indra Sistemas S.A. | Madrid | Spain | European leader in defense and air traffic simulation | Air Traffic Control Simulators, Defense Training |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| TRU Simulation + Training | Tampa, Florida | USA | Specialized aviation simulator manufacturer | Business Jet and Military Simulators |

| Frasca International | Urbana, Illinois | USA | Leading flight training simulator specialist | Flight Training Devices |

By Type

By Application/End Market

By Technology

By Component

By End User

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar