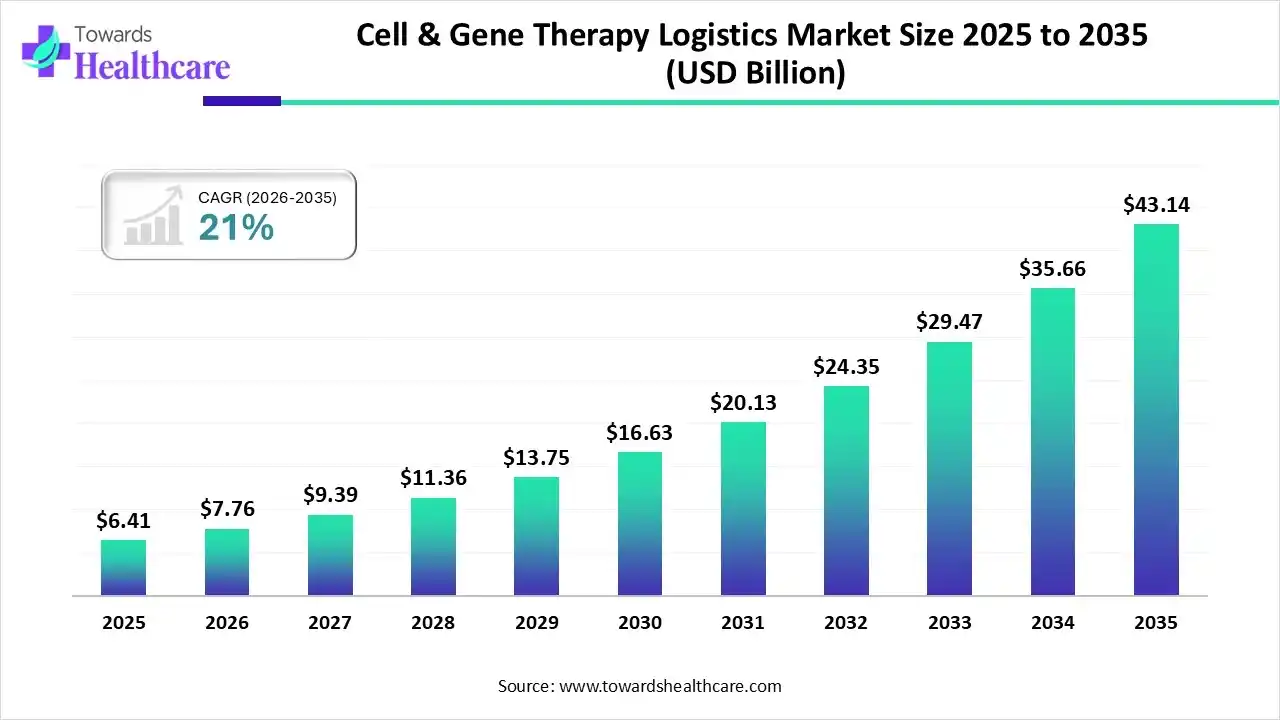

The global cell & gene therapy logistics market size is estimated at US$ 6.41 billion in 2025, is projected to grow to US$ 7.76 billion in 2026, and is expected to reach around US$ 43.14 billion by 2035. The market is projected to expand at a CAGR of 21% between 2026 and 2035.

The cell & gene therapy logistics market is expanding rapidly due to the growing demand for targeted and advanced treatment. These therapies need highly specialized logistics that include temperature control, transportation, cryogenic storage, and real-time tracking to maintain product quality. North America is dominating the market an increase in clinical trials and government approvals. Asia Pacific is the fastest growing market a strong presence of leading players and advancement in biotechnology.

| Table | Scope |

| Market Size in 2025 | USD 6.41 Billion |

| Projected Market Size in 2035 | USD 43.14 Billion |

| CAGR (2026 - 2035) | 21% |

| Leading Region | North America |

| Market Segmentation | By Service Type, By Therapy Type, By Customer / End User, By Component (Revenue Stream), By Deployment / Business Model, By Region |

| Top Key Players | Cryoport, Inc., Marken (a UPS Company), World Courier / AmerisourceBergen, Thermo Fisher Scientific / Patheon, Catalent, Inc., BioLife Solutions, Brooks Life Sciences, DHL / Cryopdp, Lonza / CDMO partners, Almac Group / Arvato Supply Chain Solutions, Biocair, Vineti, TrakCel, SAVSU Technologies / Hypertrust Patient Data Care, Stafa Cellular Therapy / Stafa Logistics, Be The Match BioTherapies, Modality Solutions, Biostor / Yourway Biopharma Services, Haemonetics / McKesson specialty logistics arms, Cryogenic shipper manufacturers & suppliers |

Cell & gene therapy logistics covers the specialized end-to-end cold-chain, handling, tracking, and services required to move living cells, viral vectors, and other biologic starting materials and final products between clinics, manufacturing sites, biobanks, and patients. Because many cell & gene products are temperature-sensitive, patient-unique (autologous) and regulated, the market includes cryogenic shippers and storage, validated temperature-controlled transport, chain-of-identity/chain-of-custody documentation, rapid reverse-logistics and IT platforms for orchestration and visibility. Demand is driven by the rise of autologous CAR-T and other personalized therapies, expanding clinical trials, and emerging commercial CGT approvals.

Increasing government funding in the cell and gene therapy logistics to support the high costs and long development timelines associated with these therapies, which contributes to the growth of the market.

For instance,

Increasing partnership among the government organizations and biotech companies contributes the growth of the growth of the market.

For Instance,

Integration of AI in medical transcription software drives the growth of the market, as AI-based technology applications in cell and gene therapy logistics support automated processes such as inventory tracking, lower human error, and enhance the awareness of supply chain systems. AI-driven technologies drive the development of a novel therapy by the R&D value chain in different stages, containing payload design optimization, target identification, translational and clinical development, and end-to-end (E2E) digitization. With each stage of cell and gene therapy advancement creating large amounts of information, AI plays a significant role in transforming this data into actionable insights. AI-driven technology production is more efficient and affordable.

For Instance,

Increasing Cases of Genetic Disorders

A growing number of genetic disorders is due to the high rate of traditional consanguineous marriages, which increases the occurrence of autosomal recessive disorders. Additionally, the birth rate of infants with chromosomal disorders related to older mothers, such as Down syndrome and other trisomies, is relatively high. The birth rate of infants with malformations due to new dominant mutations related to older fathers is also relatively high. This all drives demand for cell and gene therapy (CGT) logistics, as these therapies can potentially cure previously untreatable conditions.

Major Challenges of Cell and Gene Therapy Logistics

Supply chains for clinical trials are based on uncertainty. Factors like recruitment speed, patient dropouts, maximum tolerable doses, and patient attributes are unpredictable, making it tough to run the supply chain efficiently. This, in turn, limits the growth of the cell & gene therapy logistics market.

Recent Advancements in Cell and Gene Therapies

Cell and gene therapies have evolved by combining genetic engineering and cellular manipulation to treat a wide range of diseases. Initially, they were experimental, but they've progressed to clinical success with FDA-approved therapies. For example, CAR-T cell treatments for cancer are now a reality. Advances in gene editing tools like CRISPR have increased their potential. Cell and gene therapies have gone from theoretical promise to real-world medical solutions. This gives hope for previously untreatable conditions, including genetic disorders and various cancers, which creates an opportunity for growth in the cell & gene therapy logistics market.

For Instance,

By service type, the cold-chain transportation & cryogenic shippers segment led the cell & gene therapy logistics market, because cold-chain solutions support maintaining the potency, integrity, and quality of the cell and gene therapy medicine by keeping them at the precise temperature range. These therapies are tremendously temperature sensitive, and modest differences might outcome in the loss of therapeutic potentials. Appropriate storage and transport prevent exposure to potentially dangerous external components and avoid contamination. This confirms product quality and eventually precautions the safety of the patients.

On the other hand, the clinical trial logistics & patient return/reverse logistics segment is projected to experience the fastest CAGR from 2025 to 2034, as CGT trials are intended to adapt to every patient’s genetic profile or healthcare condition. Gene therapies are planned to manage narrowly defined patient groups with disorders at the genetic level. Logistics management is a significant element of operationalizing cell and gene therapy (CAGT) trials. There are exclusive logistics needs for autologous cell therapy modalities and allogeneic cell therapies, also for in vivo and ex vivo gene therapies and gene editing.

By therapy type, the autologous cell therapies segment is dominant in the cell & gene therapy logistics market in 2024, as autologous cell therapy is a quickly growing therapeutic modality that comprises immuno-oncology and regenerative medicine uses. This ground-breaking medical process involves utilizing a patient's cells or tissues to treat various ailments like cancer and cardiovascular disease. Autologous cell therapy generally begins with extracting cells or tissues from the patient’s body, such as blood sampling or bone marrow.

The allogeneic cell therapies segment is projected to grow at the fastest CAGR from 2025 to 2034, as allogeneic cell therapy provides many benefits over the autologous counterpart. These cells are derived from young healthy donors, removing any comorbidities related to disease states. Allogeneic cells are grown and kept in stem cell banks; therefore, they are available for instant delivery. These allogeneic cells support patients in avoiding invasive processes as well as reducing overall treatment time and discomfort.

By customer/end user, the pharma/biotech innovators & CDMOs segment led the cell & gene therapy logistics market in 2024, as cell and gene therapy logistics ensure the safe, compliant, and continuous delivery of gene therapies by leveraging progressive logistics solutions intended to meet stringent regulatory standards and reduce challenges of each stage. This technology has a lower cost, rapid supply of manufactured products in response to medical demand, and standard organization and transport of cellular material.

The clinical trial CROs & research institutes segment is projected to experience the fastest CAGR from 2025 to 2034, as collaboration with CRO and cell and gene therapy partners in the advancement to better integration of services and capabilities at every stage, providing continuous support, and an improved experience for every stakeholder in the clinical trial landscape. CROs are progressively providing real-time clinical trial programs, containing virtual site monitoring, telemedicine, and eConsent. Cell & gene therapy attributed contract research organizations (CROs) play a significant role in conducting and managing clinical trials for these ground-breaking therapies.

By component, the transportation & shipments segment led the cell & gene therapy logistics market in 2024, as cell and gene therapy products are shipped and stored unfrozen. This is predominantly true of current marketed cell therapy products. To preserve the precise temperature range needed for cell and gene therapies, use a range of advanced technologies. Use specifically intended temperature-controlled packaging to safeguard these sensitive products throughout transport.

On the other hand, the IT & orchestration software segment is projected to experience the fastest CAGR from 2025 to 2034, as this software automates manual processes, recovers productivity, improves supply chain visibility, and advances scalability. This solution supports life sciences companies in organizing, planning, and executing cell and gene therapy treatments. By orchestrating real-time information and connecting shareholders, it supports organizations in improving operational efficiency, reducing challenges, and accelerating time to treatment.

By deployment/business model, the third-party logistics providers (3PLs) & specialty couriers segment led the cell & gene therapy logistics market in 2024, as the supply of commercial CGTs rises, third-party logistics (3PL) providers require offering specialized storage and transport, with complete cold-chain solutions, so that the life-saving therapies reach patients safely. With CGT supply chains spanning major countries and landmasses, 3PL providers offer a significant solution. Confirming safe implementation and transportation, stringent quality control measures, these servicers comply with governing standards so that all shipments are perceptible and safe.

On the other hand, the managed service & hybrid models segment is projected to experience the fastest CAGR from 2025 to 2034, as a broad range of cell and gene therapy services, including regulatory maintenance, regulatory intelligence, and lifecycle support. The Cell and Gene Therapy (CGT) Access Model's goal is to enhance the lives of people living with severe and rare diseases by enhancing access to potentially transformative treatments.

Text Box 2, TextboxNorth America is dominant in the market in 2024, with a strong presence of biotech and pharma companies in this region, such as Modality Solutions LLC and BioLife Solutions, Inc., Catalent, Inc., and Thermo Fisher Scientific, all of which drive the research and development of cell and gene therapy logistics. Growing substantial spending in healthcare research to enhance the health and well-being of the nation. Growing the number of clinical trials and increasing cell and gene therapies approvals drive the growth of the market.

In the U.S., a growing healthcare revolution is being driven by spending heavily in research, which has led to novel treatments and medical devices. Furthermore, it provides a healthcare education system that drives highly dedicated providers, who administer patient-centric care rooted in a patient’s choice of freedom. The presence of a mature cold chain and bio logistics ecosystem drives the growth of the market.

In Canada, growing approval of cell and gene therapy and rising interest in targeted healthcare treatments drive the demand for the cell and gene therapy logistics market. Cell and gene therapies are effective in personalized treatment of chronic diseases and rare genetic disorders, supporting patients in Canada, which contributes to the growth of the market.

Asia Pacific is the fastest-growing region in the cell & gene therapy logistics market in the forecast period, as the increasing prevalence of chronic diseases has contributed to the growing demand for medical care products necessitating well-organized logistics solutions. There are more than 650 cell and gene therapy clinical trials ongoing in the Asia Pacific region. Cell and gene therapies are gaining momentum in the Asia-Pacific, driven by increasing patient demand and a booming ecosystem of revolution, which contributes to the growth of the market.

Research and development of gene and cell therapy logistics includes preclinical testing in laboratories and animal models, followed by an investigational new drug (IND) application. If accepted, clinical trials are conducted in three phases to assess efficacy, safety, and dosage.

Key Players: Amgen, Biogen, Bristol-Myers Squibb, Novartis, and Gilead Sciences

Clinical trials for cell and therapy logistics include the process of supply and logistics includes sourcing, packaging, storing, labelling, and distributing investigational medicinal products (IMPs), and associated materials vital for a clinical trial.

Key Players: Biocair, Modality Solutions, BioLife Solutions, Marken, and Yourway

Cell and gene therapy logistics management requires these strategies, including understanding the protocol, the patient’s ailment stage, present comorbidities, the effectiveness of apheresis, tracking of cells, coordination of handling, shipping, and management to the patient, and reconciliation of the unused product.

Key Players: Krystal Biotech and CRISPR Therapeutics

In March 2025, Frederik Brabant, MD, Chief Medical Strategy Officer at Corti, stated, “Radiologists require extreme precision in highly technical language while dictating notes. Our specialized dictation technology meets these unique needs, enabling faster, more accurate reporting while reducing cognitive load - and the real-time component is crucial, as radiologists need to follow the cursor while dictating to maintain their train of thought.”

By Service Type

By Therapy Type

By Customer / End User

By Component (Revenue Stream)

By Deployment / Business Model

By Region

Principal Consultant

Deepa Pandey is a focused and detail-oriented market research professional with growing expertise in the healthcare sector, delivering high-quality insights across therapeutic areas, diagnostics, biotechnology and healthcare services.

Learn more about Deepa Pandey

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar