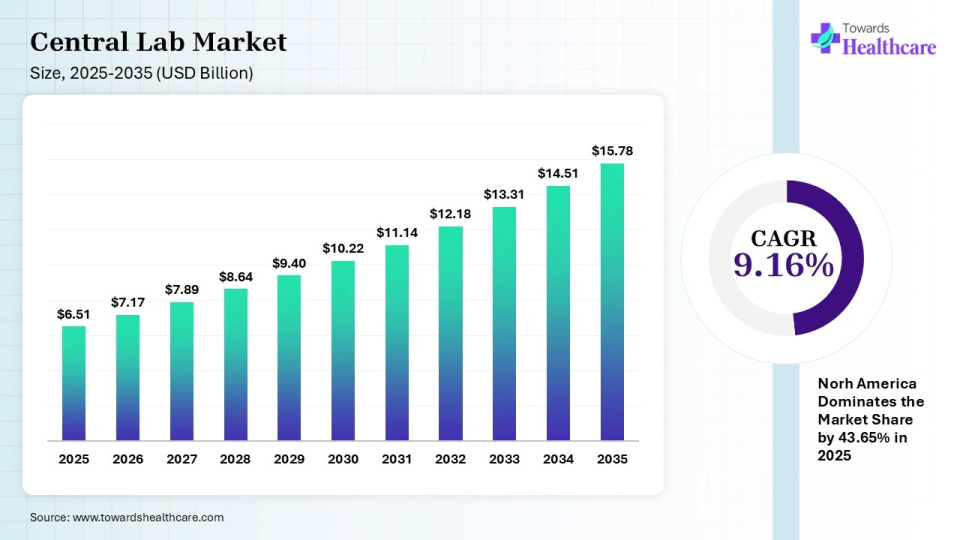

The global central lab market size is calculated at USD 6.51 billion in 2025 and is expected to be worth USD 15.78 billion by 2035, expanding at a CAGR of 9.16% from 2026 to 2035, as increasing clinical trials & increase in investment in research and development.

")

A central laboratory is a medical lab that provides services to numerous sites or institutions and this concept also covers off-site laboratories that provide support services to clinical laboratories housed in healthcare facilities, it exclusively serves one hospital or institution. The corporate-type labs and national reference laboratory systems are two more words that are used to describe central lab services. Central lab lowers costs for the pharmaceutical and biotechnology industries and also guarantees that results are delivered more quickly and accurately.

The pharmaceutical and biopharmaceutical firms have completely outsourced central labs. During the evaluation period, the worldwide central lab market will continue to have strong potential due to rising pharmaceutical and biotechnology company activity as well as the rising need for novel medications and vaccines. Moreover, from covid 19 pandemic crisis the demand for central laboratories is continuously driving an increase in research & development and conducting clinical trials.

The desire for affordable solutions is being further fueled by the high cost of treating the older population's many ailments. Some of the key factors propelling the global central lab market are the high complexity of clinical trials, rising disease prevalence around the world, growing demand for novel drugs and vaccines, the surge in the number of central labs, and the growing need to lower the cost of drug research and development processes. advantages they provide, such as their great efficiency and speed, decreased costs associated with product manufacture, and superior flexibility, central labs have become extremely popular all over the world. Due to the elimination of extra stages, these central labs let multinational corporations introduce new substances to the market more swiftly.

Delay in Results

Relying on central labs can lead to a delay in obtaining results. Researchers from local labs need to send the sample to a central lab for analysis. This delay can be problematic in some cases where an immediate result is required to allow dosing or entry into the trial. Thus, such a delay in obtaining results reduces confidence among researchers, restricting market growth.

Central lab boosting from covid & providing several opportunities from covid 19 central lab plays an important role in sample testing. The desire for affordable solutions is being further fueled by the high cost of treating the older population's many ailments. The more trending market for central labs worldwide is being overrun by a multitude of technology and software advances. Clinical trial laboratory service providers are assisting central labs with advances including next-generation flow cytometry result reporting automation, sample & consent tracking, and AI protocol reading.

| Key Elements | Scope |

| Market Size in 2026 | USD 7.17 Billion |

| Projected Market Size in 2035 | USD 15.78 Billion |

| CAGR (2026 - 2035) | 9.16% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Clinical Trial Phase, By Modality, By End-User |

| Top Key Players | ACM Global Laboratories, CIRION BioPharma Research, Eurofins Scientific, ICON plc, Intermountain Health, IQVIA, LabConnect, Labcorp, Medpace, Reprocell, SGS S.A., Thermo Fisher Scientific |

| By Service Type | 2025 (%) |

| Safety Testing | 29.75% |

| Specialty Testing & Biomarkers | 17.47% |

| Genomic & Molecular Testing | 19.56% |

| Pathology & Histology Services | 15.30% |

| Microbiology & Virology | 6.64% |

| Clinical Supply Chain & Biorepository | 11.28% |

Safety Testing Segment Dominated the Market in 2025

The safety testing segment held the largest revenue share of 29.75% of the central lab market in 2025. Growth is driven by increasing regulatory requirements for clinical trial safety monitoring, rising drug development activities, and demand for standardized testing services, which ensure compliance and patient safety across global trials and studies worldwide consistently.

The genomic & molecular testing segment held 19.56% market share in 2025 and is expected to grow with the highest CAGR of 10.77% in the market during the studied years. Expansion is supported by growing adoption of precision medicine, advancements in sequencing technologies, increasing prevalence of genetic disorders, and rising research funding, encouraging demand for accurate molecular diagnostics and personalized treatment approaches globally and rapidly.

The speciality testing & biomarkers segment captured 17.47% of the central lab market in 2025. Demand is rising due to increasing focus on targeted therapies, biomarker-driven drug development, and early disease detection, along with pharmaceutical companies investing heavily in companion diagnostics to improve clinical trial outcomes and success rates overall.

The pathology & histology services segment captured 15.30% of the market share in 2025. Growth is fueled by the rising incidence of chronic diseases, the need for accurate tissue diagnosis, and expanding clinical trials, alongside improvements in laboratory automation and digital pathology technologies, enhancing efficiency and diagnostic precision and reliability significantly.

| By Therapeutic Area | 2025 (%) |

| Oncology | 32.87% |

| Infectious Diseases | 20.39% |

| Cardiovascular & Metabolic Diseases (CVMD) | 18.56% |

| Neurology & Central Nervous System (CNS) | 13.47% |

| Immunology & Autoimmune Diseases | 9.78% |

| Rare Diseases & Genetic Disorders | 4.93% |

The Oncology Segment Dominated the Market in 2025

The oncology segment held the largest central lab market share of 32.87% in 2025. Growth is driven by the rising global cancer burden, increasing clinical trials for immunotherapies and targeted drugs, and the need for advanced diagnostic testing, encouraging pharmaceutical companies to invest heavily in oncology-focused research and development.

The infectious diseases segment captured 20.39% of the market share in 2025. Expansion is supported by the growing prevalence of infectious diseases, heightened awareness after global outbreaks, and increased demand for rapid diagnostic testing, along with continuous monitoring requirements in clinical trials and public health programs worldwide.

The cardiovascular & metabolic diseases (CVMD) segment captured 18.56% of the central lab market share in 2025. Growth is fueled by the increasing incidence of lifestyle-related conditions such as diabetes and heart disease, a rising aging population, and demand for routine monitoring and biomarker testing in clinical studies and long-term disease management strategies.

The rare diseases & genetic disorders segment held 4.93% market share in 2025, and is estimated to be the fastest-growing with 13.10% CAGR during the forecast period. Rapid growth is driven by advancements in genetic testing technologies, increasing focus on orphan drug development, supportive regulatory frameworks, and growing awareness, leading to higher diagnosis rates and demand for specialized laboratory testing services globally.

| By Clinical Trial Phase | 2025 (%) |

| Phase I & II (Early Phase) | 34.67% |

| Phase III (Late Phase) | 50.32% |

| Phase IV (Post-Marketing Surveillance) | 15.01% |

The Phase III Segment Dominated the Market in 2025

The phase III segment led with 50.32% central lab market share in 2025. This dominance is driven by the large scale of phase III trials, requiring extensive patient populations and comprehensive testing services, along with increased investments from pharmaceutical companies aiming to confirm efficacy and safety before regulatory approvals globally.

The phase I & II segment captured the second-largest market share of 34.67% in 2025. Growth is supported by rising early-stage drug development activities, an increasing number of investigational therapies, and demand for specialized testing to evaluate safety, dosage, and initial efficacy, encouraging continuous expansion of central lab services in these phases.

The phase IV held 15.01% market share and is expected to grow at the fastest CAGR Of 10.02% during the forecast period. Rapid growth is fueled by post-marketing surveillance requirements, increasing focus on long-term drug safety and effectiveness, and regulatory mandates, driving demand for ongoing real-world data collection and laboratory testing after product commercialization.

| By Modality | 2025 (%) |

| Small Molecules | 35.50% |

| Biologics (Large Molecules) | 36.16% |

| Advanced Therapies (ATMP) | 16.87% |

| Vaccines | 11.47% |

The Biologics Segment Dominated the Market in 2025

The biologics segment contributed the biggest revenue share of 36.16% of the central lab market in 2025. Growth is driven by increasing development of monoclonal antibodies, biosimilars, and protein-based therapies, along with rising demand for complex analytical testing, as biologics require specialized laboratory support for safety, efficacy, and regulatory compliance processes.

The small molecules segment captured the second-largest market share of 35.50% of the market in 2025. Expansion is supported by continued demand for conventional drugs, well-established manufacturing processes, and high volume of clinical trials, as small molecules remain widely used due to cost-effectiveness, scalability, and ease of administration across therapeutic areas.

The advanced therapies segment held 16.87% of the central lab market in 2025 and is expected to witness the fastest growth with 13.22% CAGR in the market over the forecast period. Rapid growth is fueled by rising investments in gene and cell therapies, increasing approvals, and demand for highly specialized testing services, as these therapies require complex handling, monitoring, and regulatory validation throughout clinical development stages.

The vaccines segment captured a significant share of 11.47% of the market in 2025. Growth is driven by ongoing immunization programs, increasing focus on infectious disease prevention, and rising development of new vaccines, along with demand for large-scale clinical trials and laboratory testing to ensure safety, efficacy, and quality standards globally.

| By End-User | 2025 (%) |

| Pharmaceutical & Biotechnology Companies | 61.17% |

| Contract Research Organizations (CROs) | 17.21% |

| Academic & Government Research Institutes | 12.76% |

| Clinical Diagnostic Laboratories | 8.86% |

Which End-User Dominated the Market in 2025?

The pharmaceutical & biotechnology companies segment contributed the biggest revenue share of 61.17% of the central lab market in 2025. Growth is driven by increasing drug development pipelines, rising R&D investments, and growing demand for outsourced laboratory services, as companies seek efficient, scalable, and compliant testing solutions to accelerate clinical trials and regulatory approvals globally.

The contract research organizations (CROs) segment held 17.21% share in 2025 and is expected to witness the fastest growth of 10.52% in the market over the forecast period. Expansion is supported by increasing outsourcing trends, cost optimization strategies, and the need for specialized expertise, enabling CROs to provide comprehensive clinical trial support services, including central lab testing, improving efficiency, and reducing time to market.

The academic & government research institutes segment held 12.76% central lab market share in 2025. Growth is fueled by rising public funding for research, increasing collaborations with pharmaceutical companies, and a focus on innovation, driving demand for laboratory testing services to support clinical studies, epidemiological research, and the development of new treatment approaches.

The clinical diagnostic laboratories segment held 8.86% market share in 2025. Expansion is driven by increasing diagnostic testing demand, advancements in laboratory technologies, and integration with clinical trials, enabling laboratories to support patient recruitment, sample analysis, and data generation for research and therapeutic development activities.

")

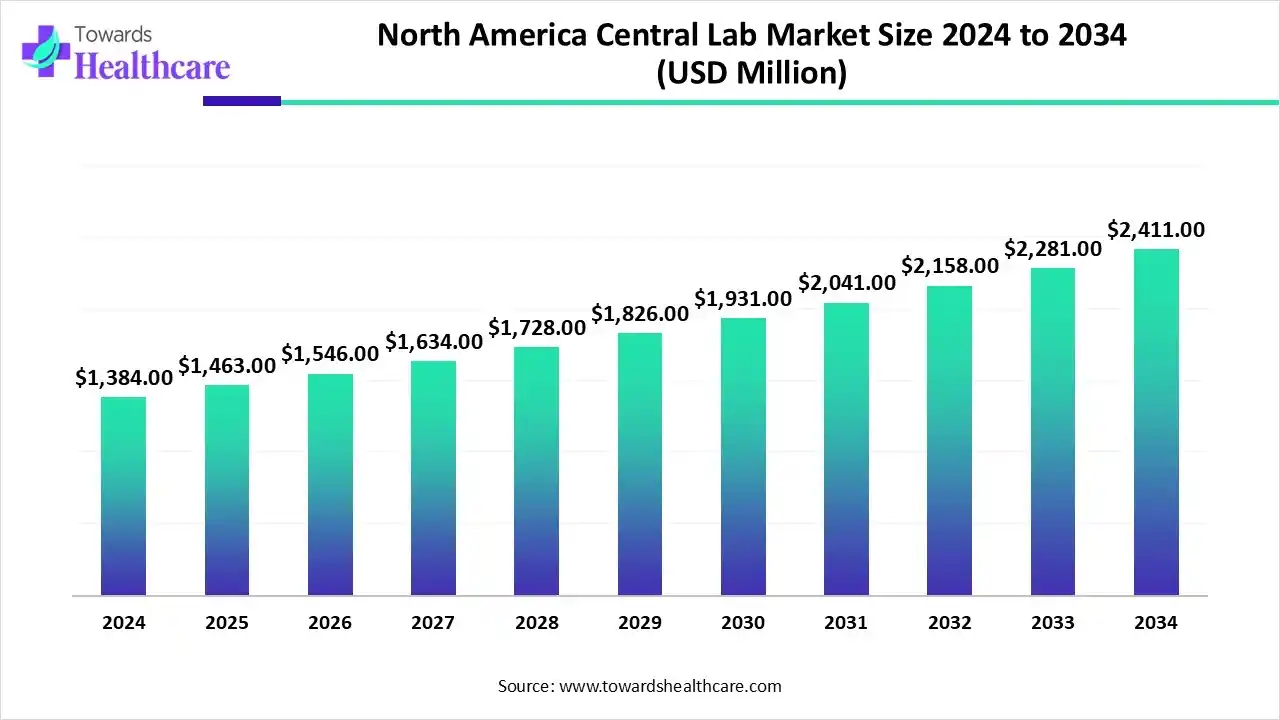

The North America central lab market size is calculated at USD 2.84 billion in 2025, grew to USD 3.11 billion in 2026, and is projected to reach around USD 6.37 billion by 2035. The market is expanding at a CAGR of 8.31% between 2026 and 2035.

")

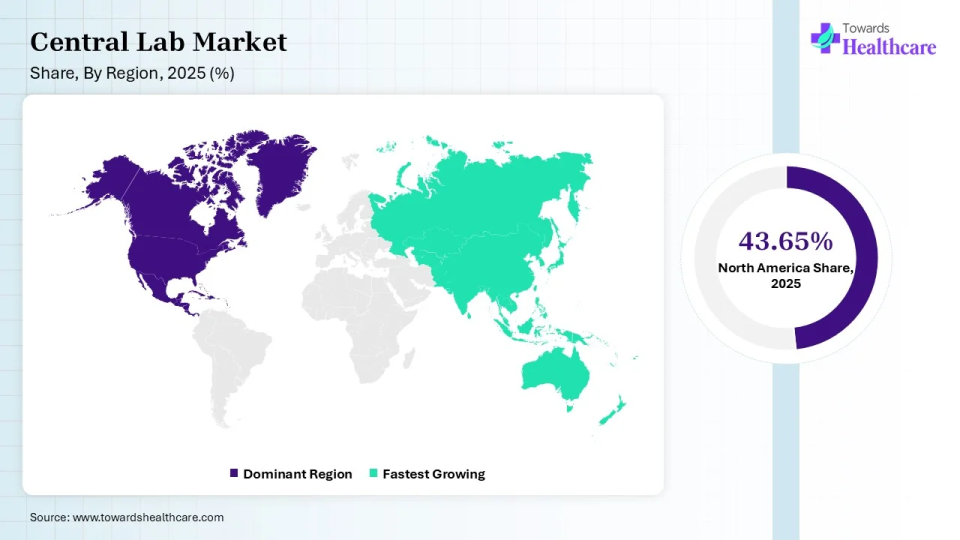

North America held a major revenue share of 43.65% of the central lab market in 2025. The central lab market is witnessing growth globally, with North America leading the market, followed by Europe and the Asia Pacific. The North American market is driven by factors such as the increasing number of clinical trials, the presence of key players, and a favorable regulatory environment. The presence of leading pharmaceutical and biotechnology companies in the region is also contributing to market growth. The U.S. conducts the highest number of clinical trials globally. According to the WHO International Clinical Trials Registry Platform (ICTRP), the number of trials conducted in the US from 1999 to 2022 was 168,520, whereas that in Canada was 34,041. While the total number of clinical trials in the entire North American region was around 11,935 in 2022.

U.S. Market Trends

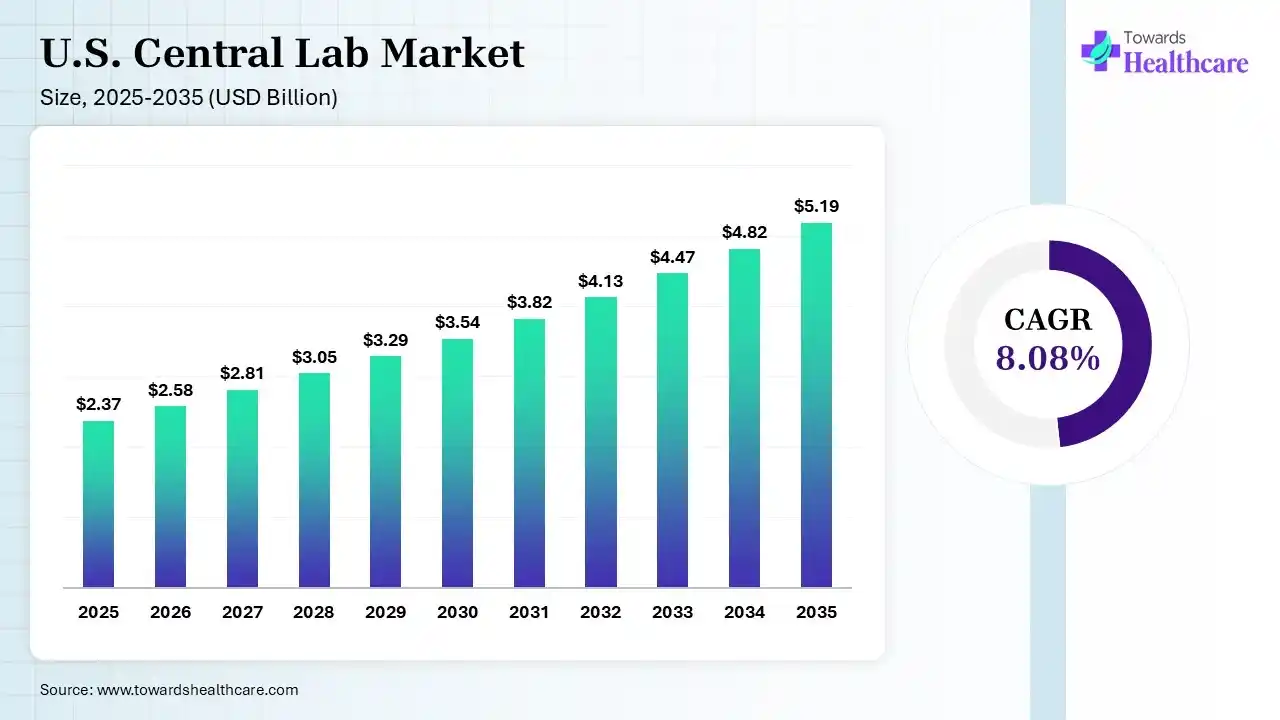

The U.S. central lab market size was estimated at USD 2.37 billion in 2025 and is predicted to increase from USD 2.58 billion in 2026 to approximately USD 5.19 billion by 2035, expanding at a CAGR of 8.08% from 2026 to 2035.

")

U.S. boasts a dominant position in the global central lab market, and this dominance is attributed to the strong healthcare infrastructure comprising a well-developed network of laboratories, research institutions, and academic medical centers. Being a major hub for clinical research, the U.S. not only offers high-quality central lab services but also enhances its operational efficiency and capabilities. The high investment in research and development in the pharmaceutical and biotechnology sectors led to the adoption of innovative laboratory technologies and testing methods

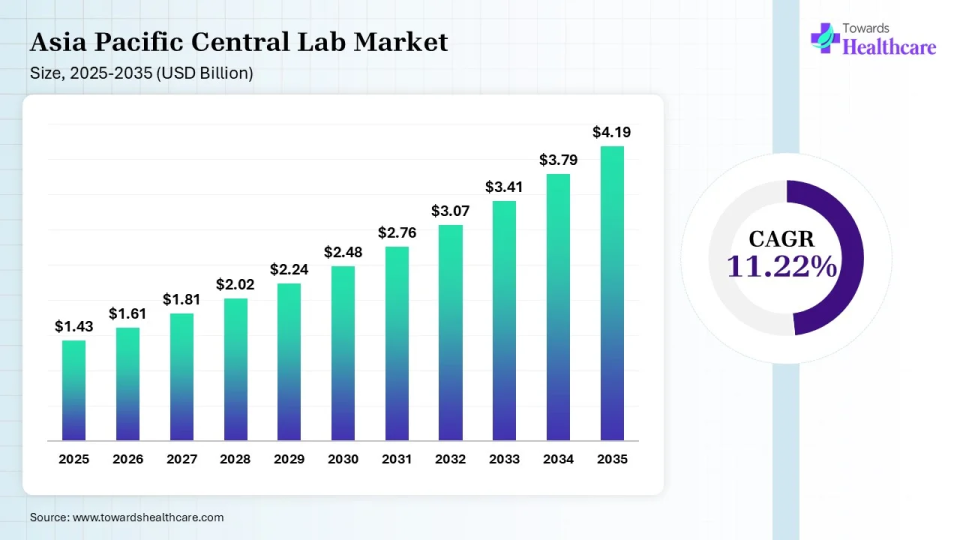

The APAC central lab market size was estimated at US$ 1.43 billion in 2025, projected to increase to US$ 1.61 billion in 2025 and reach US$ 4.19 billion by 2035, showing a healthy CAGR of 11.22% across the forecast years.

")

Asia-Pacific held 21.98% of the market share in 2025 and is expected to witness the fastest growth with a CAGR of 11.22% during the predicted timeframe. On the other hand, the Asia Pacific region is expected to emerge as a significant market for central lab services, owing to the increasing number of clinical trials in the region, growing healthcare infrastructure, and rising investments by pharmaceutical and biotechnology companies. The Asia Pacific market is expected to witness significant growth in countries such as China, India, and Japan, major clinical research hubs. Singapore has emerged as a hub for central labs in the Asia-Pacific region. The number of clinical trials in China, Japan, and India is rapidly rising. China conducted 94,193 clinical trials, whereas Japan and India conducted 63,499 and 54,891 clinical trials, respectively, from 1999 to 2022.

Furthermore, the increasing prevalence of chronic diseases, the growing geriatric population, and the rising demand for personalized medicine are expected to drive market growth in the region. The market is also expected to witness growth in emerging economies such as Brazil and South Africa, owing to the increasing number of clinical trials and the growing focus on healthcare infrastructure development.

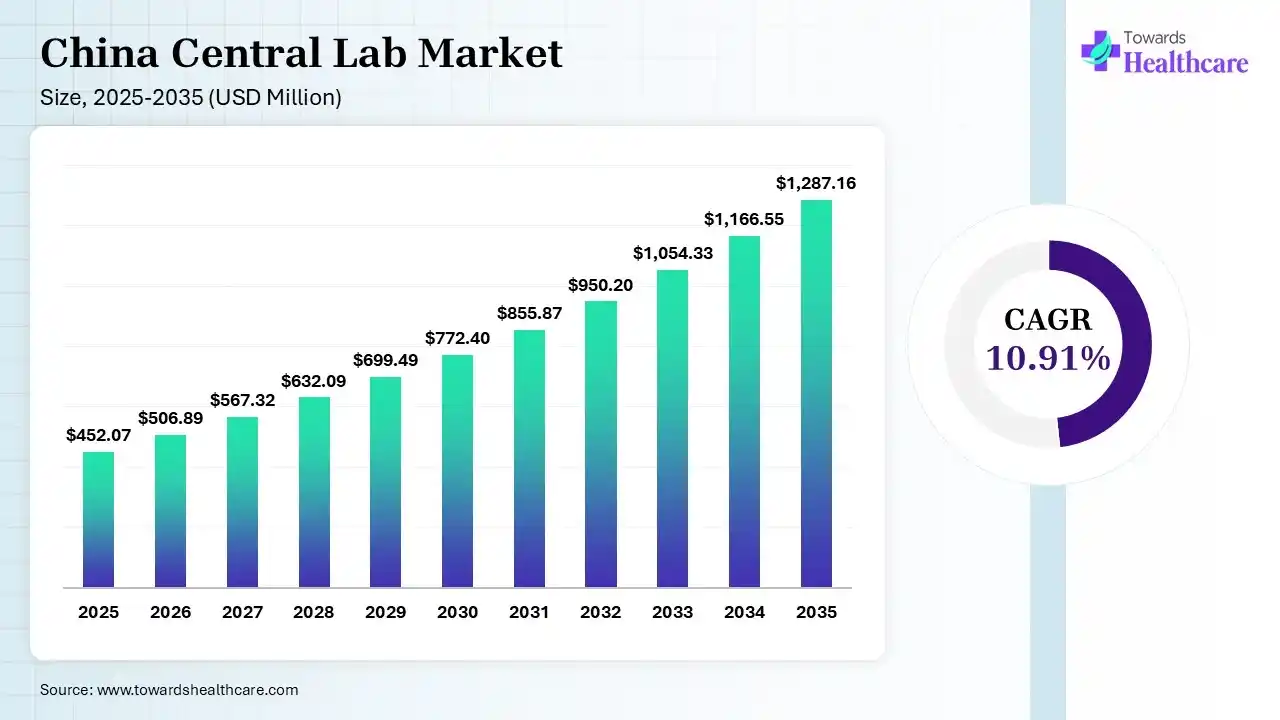

The China central lab market size was estimated at USD 452.07 million in 2025 and is predicted to increase from USD 506.89 million in 2026 to approximately USD 1287.16 million by 2035, expanding at a CAGR of 10.91% from 2026 to 2035.

")

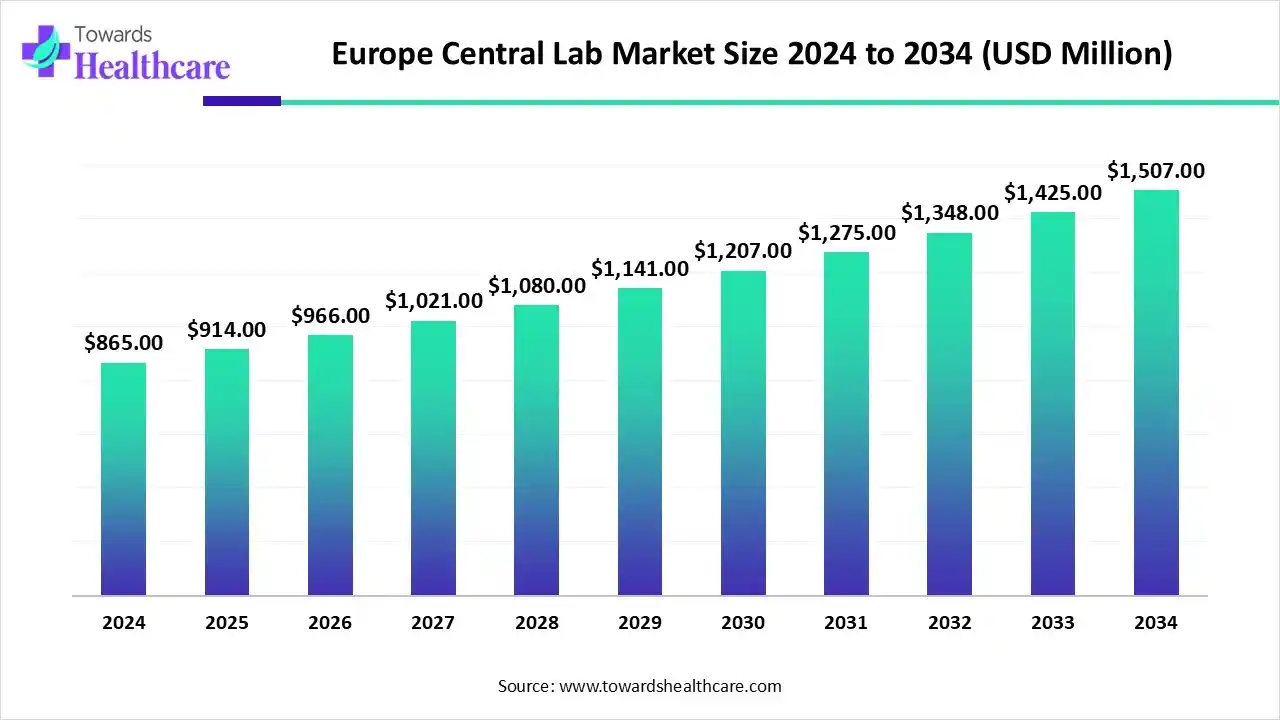

The Europe central lab market size was reported at US$ 1.77 billion in 2025 and is expected to rise to US$ 1.93 billion in 2026. According to forecasts, it will grow at a CAGR of 8.34% to reach US$ 3.98 billion by 2035.")

Europe captured the second-largest market share of 27.17% in 2025. Europe is considered the fastest-growing market for central lab services. The European market is driven by a strong life sciences ecosystem, which boasts a long history of pharmaceutical discovery and the life sciences industry. The adoption of electronic lab notebooks and lab automation in Europe is rising, and it is propelled by investments by prominent firms like LabWare and Merck. The significant investments by the region in the pharmaceutical industry for research and development also create a demand for central lab services, especially since the German market is experiencing rapid growth, fueled by increasing R&D investments and the development of new life sciences research centers.

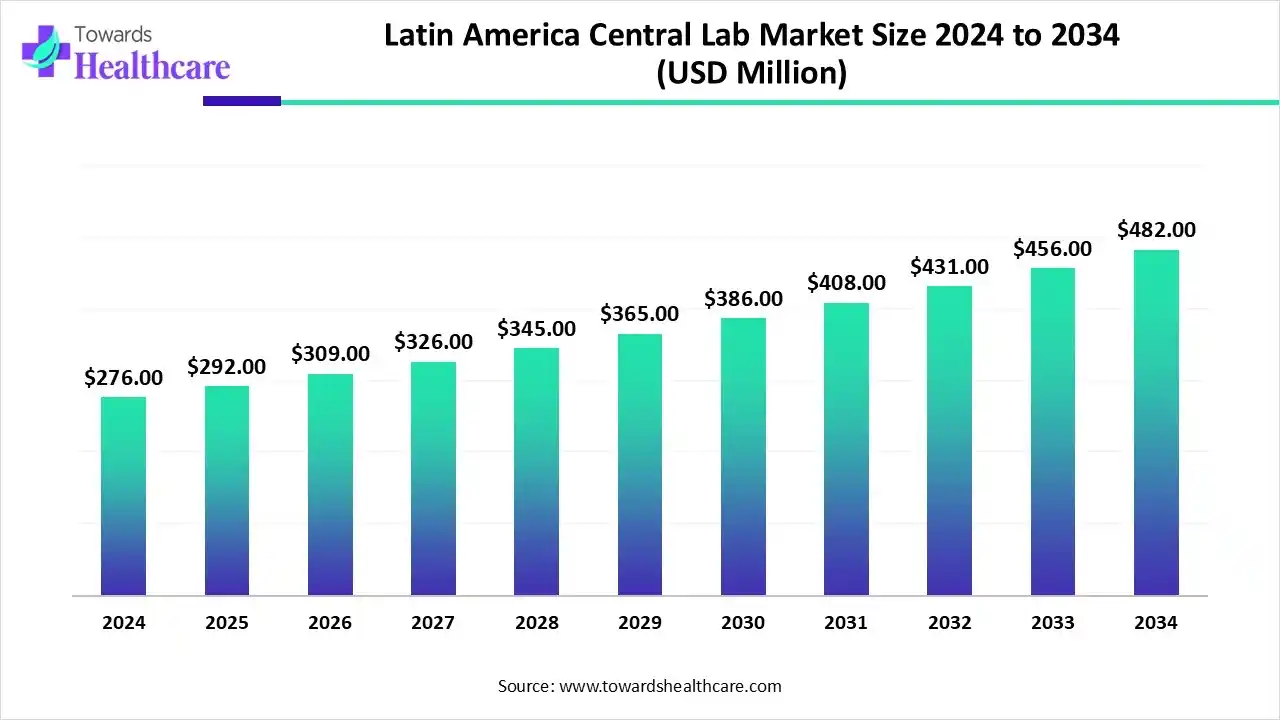

The Latin America central lab market size reached US$ 289.89 million in 2025 and is anticipate to increase to US$ 322.51 million in 2026. By 2035, the market is forecasted to achieve a value of around US$ 773.25 million, growing at a CAGR of 10.20%.

")

Latin America captured 4.45% of the total market share in 2025. The Latin America central lab market is experiencing steady growth, driven by the rising number of clinical trials, expanding pharmaceutical and biotechnology sectors, and improved regulatory frameworks. Growing demand for high-quality diagnostic services and standardized testing supports this trend. Among regional countries, Brazil dominates the market due to its advanced healthcare infrastructure, skilled workforce, and strong government initiatives to promote clinical research and innovation.

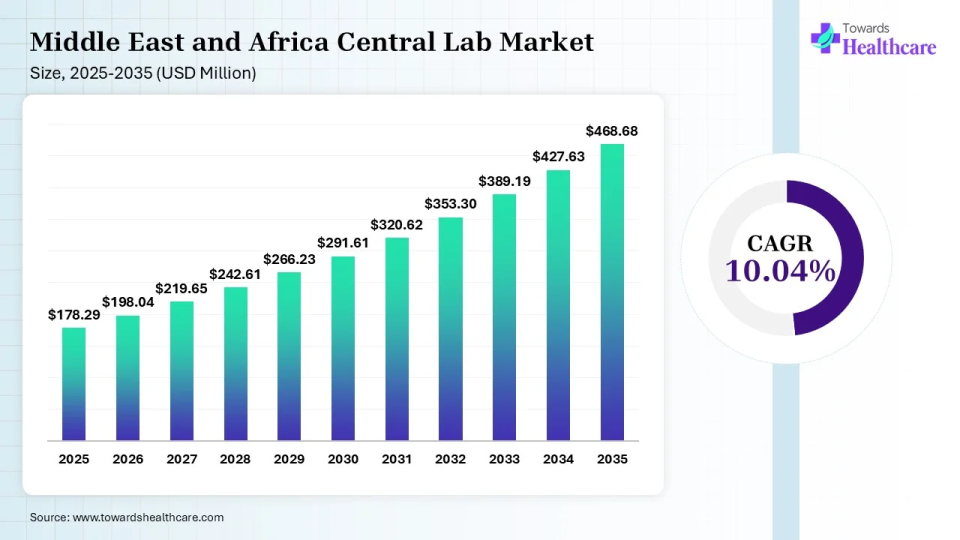

The Middle East & Africa central lab market size reached US$ 178.29 million in 2025 and is expected to increase to US$ 198.04 million in 2026. By 2035, the market is forecasted to achieve a value of around US$ 468.68 million, growing at a CAGR of 10.04%.

")

The Middle East and Africa Captured 2.75% of the total market share in 2025. The Middle East & Africa are considered to be a significantly growing area, due to the increasing number of clinical trials and favorable government support. The growing awareness of decentralized trials and the burgeoning pharma and biotech sectors augment the market. The rising demand for personalized medicines encourages companies to develop innovative biologics and conduct clinical trials, potentiating the demand for central lab services.

The Dubai Central Laboratory (DCL) Department in Dubai Municipality and the Abu Dhabi Quality and Conformity Council are some central labs in the UAE. These labs ensure the quality of materials and products and preserve the environment and public health. The increasing public-private partnerships also facilitate clinical trials and sample testing & analysis.

Strengths

Weaknesses

Opportunities

Threats

David Morris, Chief Operating Officer at IQVIA Laboratories, commented that Site Lab Navigator and its differentiated e-Requisition solution will significantly reduce administrative burden on sites and improve the quality and execution of clinical trials for its customers. He also said that the company streamlines workflows, improves data integrity, and accelerates the path to high-quality results by equipping investigator sites with cutting-edge tools.

By Service Type

By Therapeutic Area

By Clinical Trial Phase

By Modality

By End-User

By Geography

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar