Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

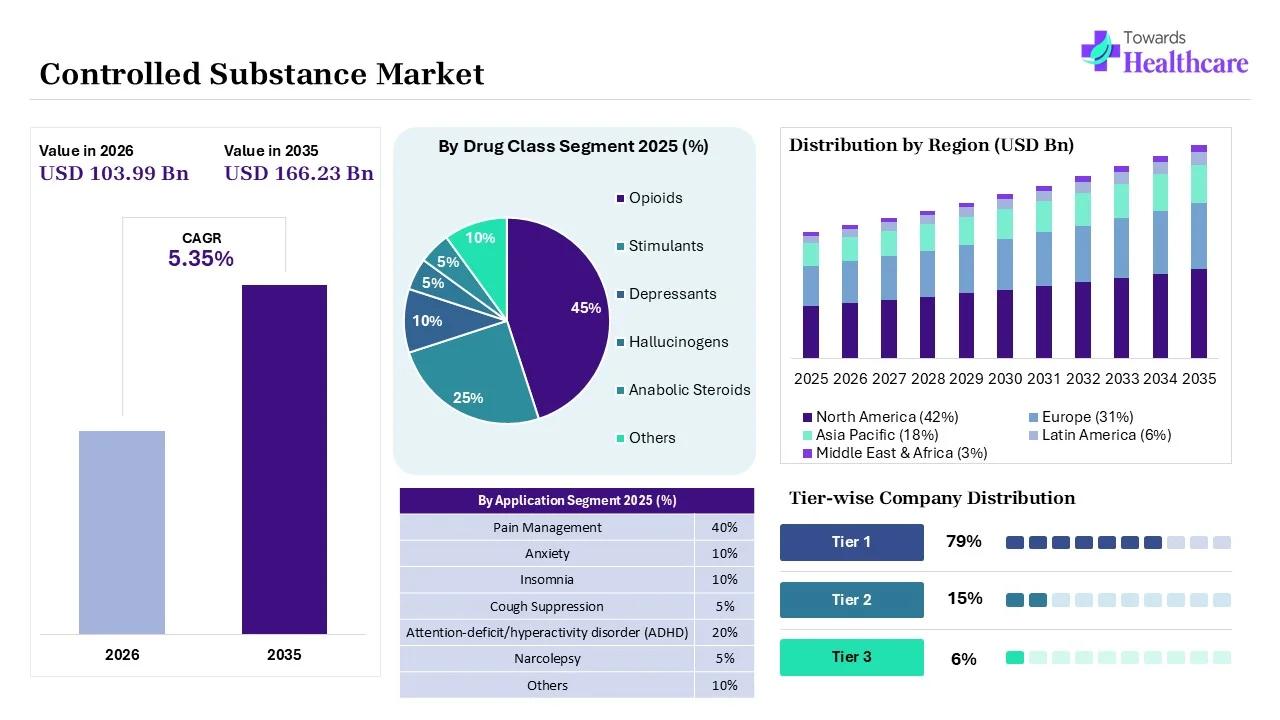

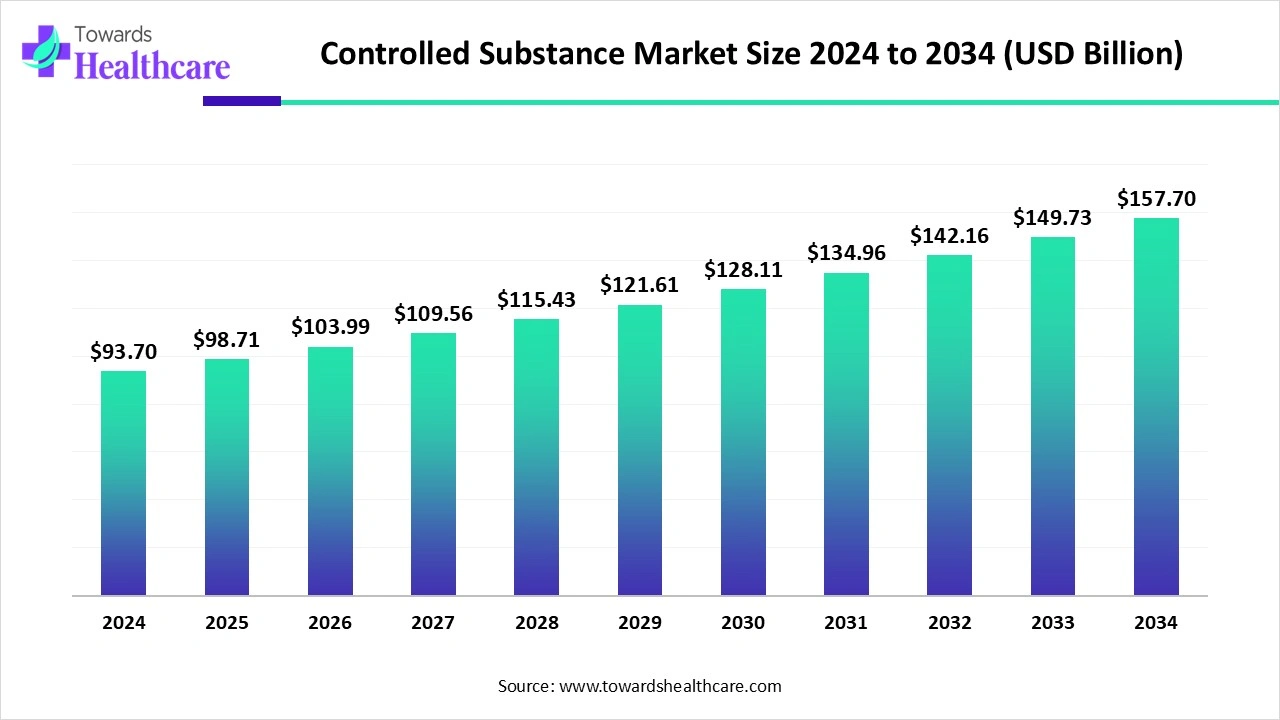

The global controlled substance market size marked US$ 98.71 billion in 2025 and is forecast to experience consistent growth, reaching US$ 103.99 billion in 2026 and US$ 166.23 billion by 2035 at a CAGR of 5.35%.

")

The controlled substance market is witnessing significant growth driven by the rising prevalence of chronic pain, neurological disorders, and mental health conditions, along with increasing demand for opioids, stimulants, and other regulated medications. Stringent government regulations and monitoring systems ensure safe distribution and use, while pharmaceutical innovations and new drug approvals expand treatment options. North America remains the dominant region due to well-established healthcare infrastructure, high awareness of controlled substance management, advanced regulatory frameworks, and strong R&D investment by pharmaceutical companies, supporting market leadership.

The controlled substance is a drug or chemical whose manufacture, possession, use, and distribution are regulated by government laws due to its potential for abuse, addiction, or harmful effects. These substances include opioids, stimulants, depressants, hallucinogens, and certain prescription medications. They are classified into schedules based on their medical use, potential for abuse, and safety profile. Controlled substances are strictly monitored to prevent misuse, diversion, and illegal distribution. Regulatory authorities, such as the U.S. Drug Enforcement Administration (DEA), oversee compliance, ensuring that these drugs are used safely for legitimate medical, scientific, or industrial purposes.

Controlled substances are prescription drugs and chemicals regulated by government authorities due to their potential for abuse, dependence, or misuse, while remaining essential for legitimate medical, scientific, and research purposes. The controlled substances market is expanding due to the increasing prevalence of chronic pain, neurological disorders, cancer, and mental health conditions requiring regulated medications. Growing implementation of electronic prescribing systems, AI-enabled prescription monitoring, blockchain-based supply chain security, and digital inventory management is improving regulatory compliance and reducing diversion risks. Rising investments in secure pharmaceutical distribution, automated dispensing technologies, and advanced analytics are enhancing operational efficiency across healthcare settings. Future growth opportunities are supported by expanding healthcare infrastructure, stronger regulatory oversight, increasing adoption of real-time monitoring solutions, and continuous innovation in secure drug management technologies, ensuring safe access to controlled medications while maintaining patient safety and supply chain integrity.

Policy Reforms

Policy reforms in the market are actively reshaping regulatory landscapes in 2025. A significant development occurred when, in August 2025, the Drug Enforcement Administration (DEA) proposed rescheduling cannabis from Schedule I to Schedule III, acknowledging its medical uses and lower abuse potential, though the final decision is pending.

Adoption of Inorganic Growth Strategies

Inorganic strategies like acquisitions and partnerships are propelling growth in the controlled substance market by enhancing R&D capabilities, expanding product portfolios, and improving regulatory compliance. For instance, in August 2025, Aurobindo Pharma's acquisition of Lannett Company for US$250 million enables entry into non-opioid controlled substances, particularly ADHD therapeutics, and provides access to a compliant U.S. manufacturing facility. Similarly, in September 2025, Strides Pharma's partnership with Kenox Pharmaceuticals focuses on developing nasal spray products, accelerating the delivery of affordable, high-quality medicines in the U.S. These strategic moves enhance market competitiveness and align with regulatory standards.

Growing Regulatory and Legal Pressure

Growing regulatory and legal pressure on pharmacies is reshaping the controlled substance market by enforcing stricter compliance and safer dispensing practices, which ultimately builds trust among patients, providers, and regulators. Tighter monitoring reduces misuse and diversion, encouraging broader acceptance of controlled medications for legitimate medical needs. This also compels pharmaceutical companies to innovate safer formulations and improve supply chain transparency, fueling growth. For instance, in 2025, the U.S. Department of Justice filed a lawsuit against Walgreens for allegedly filling unlawful opioid prescriptions, underscoring heightened oversight that is pushing the industry toward more responsible, sustainable, and growth-oriented practices.

AI integration can significantly improve the controlled substance market by enhancing efficiency, safety, and compliance across the value chain. In manufacturing, AI-driven predictive analytics optimize production processes, reduce errors, and ensure regulatory compliance. In market and distribution, AI supports real-time monitoring of prescription patterns, helping to detect misuse and ensure accurate supply chain management. For healthcare providers, AI enables precision prescribing by analyzing patient data, improving treatment outcomes while minimizing risks of abuse. Additionally, AI-powered drug discovery accelerates R&D, enabling faster identification of new compounds and delivery methods, ultimately driving innovation and sustainable growth in the controlled substance industry.

The controlled substances market is influenced by a combination of internal and external factors. Internally, advancements in pharmaceutical manufacturing, secure supply chain management, electronic prescribing systems, automated dispensing technologies, AI-driven compliance monitoring, and digital inventory management are improving operational efficiency and regulatory compliance.

Externally, the rising prevalence of chronic pain, cancer, neurological disorders, and mental health conditions, along with stringent government regulations, increasing healthcare expenditure, expanding hospital infrastructure, and growing awareness of safe medication practices, are driving market growth. However, strict regulatory requirements, concerns over drug misuse and diversion, and complex compliance procedures remain key challenges affecting the market.

Driver

Expanding Therapeutic Applications

Expanding therapeutic applications are significantly driving the growth of the controlled substance market. As medical research uncovers new uses for controlled substances, such as opioids, stimulants, and cannabinoids, their role in treating various conditions is broadening. This expansion not only increases the demand for these substances but also encourages pharmaceutical companies to invest in developing new formulations and delivery methods. For instance, in 2025, the U.S. Food and Drug Administration (FDA) recommended classifying the compound 7-OH, found in vapes, as a Schedule I controlled substance due to its opioid-like properties and widespread availability in consumer products. This move underscores the evolving understanding of controlled substances and their potential therapeutic applications, further fueling market growth.

Restraint

Social Stigma & Limited Access in Emerging Regions

The key players operating in the market are facing issues due to limited access in emerging regions, which is estimated to restrict the market growth. Patients may avoid using certain controlled drugs due to fear of addiction or social judgment, reducing demand. Poor healthcare infrastructure and a lack of trained professionals restrict distribution and adoption in developing countries.

Opportunity

Advancement in Drug Formulation and Delivery Systems

Advancements in drug formulation and delivery systems are significantly driving the growth of the controlled substance market. Innovations such as controlled-release formulations, transdermal patches, and nasal sprays enhance the efficacy and safety of controlled substances by ensuring precise dosing and reducing side effects. These advancements improve patient compliance and expand therapeutic applications.

For instance, in 2025, a team of scientists developed a silk nanogel injector for targeted drug delivery, which received a patent from the Controller General of Patents, Designs, and Trademarks. This technology utilizes biocompatible, biodegradable materials for localized and sustained drug release, particularly benefiting cancer therapy, wound healing, and regenerative medicine. Such innovations not only enhance treatment outcomes but also open new avenues for the application of controlled substances in various medical fields.

| Table | Scope |

| Market Size in 2026 | USD 103.99 Billion |

| Projected Market Size in 2035 | USD 166.23 Billion |

| CAGR (2025 - 2036) | 5.35% |

| Leading Region | North America |

| Key Applications | Pain management, anesthesia, ADHD treatment, opioid dependence therapy, psychiatric disorders, palliative care, surgical procedures |

| Primary End Users | Hospitals, clinics, pharmacies, specialty treatment centers, government healthcare agencies, research institutions |

| Key Challenges | Strict regulatory frameworks (DEA, FDA, EMA), opioid crisis litigation risks, diversion and abuse control, supply chain compliance complexity, stigma around opioid prescribing, pricing pressure |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Drug Class, By Applications, By Sales Channel, By Region |

| Top Key Players | Johnson & Johnson Services, Inc., Pfizer Inc., Sanofi, Merck & Co., Inc., Gilead Sciences, Inc., Amgen Inc., Novartis Pharmaceuticals Corporation, AbbVie Inc., GSK PIc., AstraZeneca, Bristol-Myers Squibb Company, Eli Lilly and Company, Teva Pharmaceutical Inc., Bayer AG, Novo Nordisk A/S, Takeda Pharmaceutical Company Limited, Boehringer Ingelheim International GmbH, Aspen Holdings, Astellas Pharma Inc. |

| Segments | Shares % |

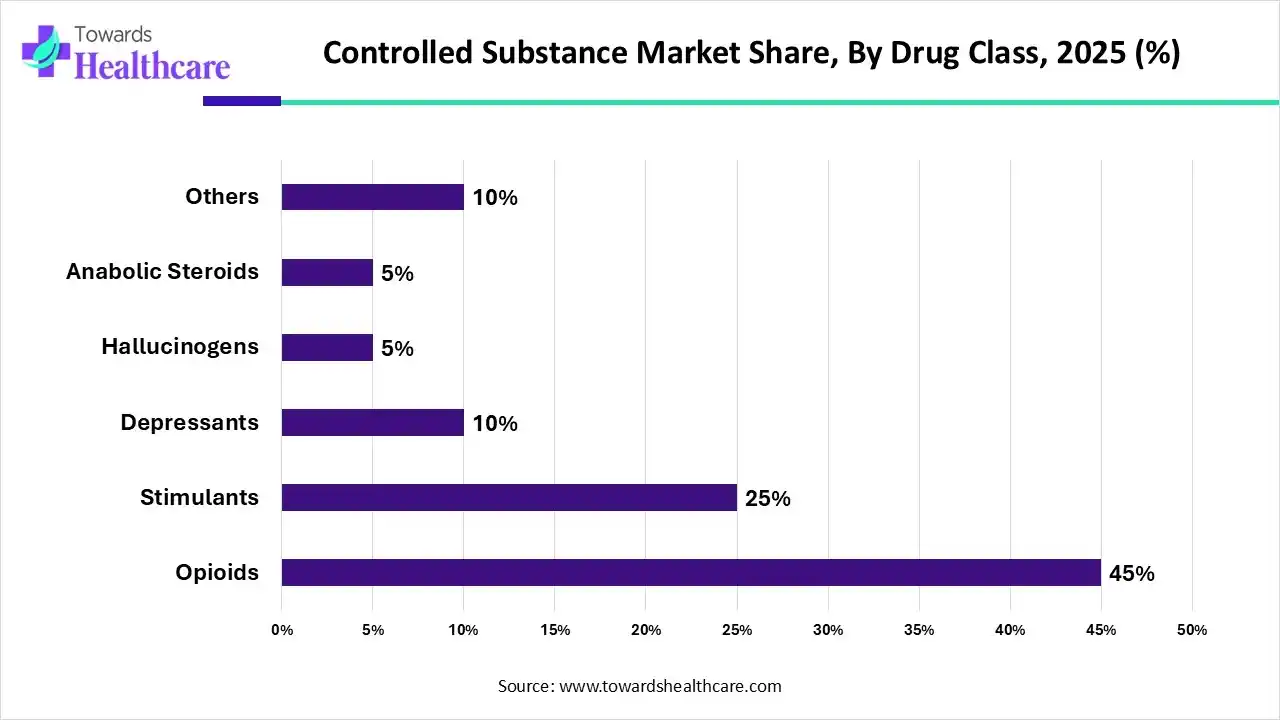

| Opioids | 45% |

| Stimulants | 25% |

| Depressants | 10% |

| Hallucinogens | 5% |

| Anabolic Steroids | 5% |

| Others | 10% |

")

Which Drug Class Segment Dominated the Controlled Substance Market?

The opioids segment represents the dominant segment in the market by 45%, primarily due to their widespread use in managing acute and chronic pain, post-surgical recovery, and cancer-related pain. Despite strict regulations, opioids remain the most prescribed controlled drugs globally because of their high therapeutic effectiveness. The growing prevalence of chronic pain conditions, aging populations, and the need for advanced palliative care sustain their demand. Moreover, continuous innovation in abuse-deterrent formulations and extended-release products strengthens their position. While stimulants, hallucinogens, and anabolic steroids have specific applications, opioids’ broad medical necessity makes them the leading segment in the market.

The stimulants segment is anticipated to be the fastest-growing in the controlled substance market, driven by the rising prevalence of Attention Deficit Hyperactivity Disorder (ADHD), narcolepsy, and certain mental health conditions. Increased diagnosis rates in both children and adults, coupled with greater awareness and acceptance of treatment, are fueling demand for stimulant-based medications. Pharmaceutical advancements in extended-release and abuse-deterrent formulations are further supporting safer use and compliance. Additionally, expanding therapeutic applications beyond ADHD, along with strong prescription adoption in North America and growing acceptance in emerging markets, make stimulants the fastest-growing drug class segment in the market.

| Segments | Shares % |

| Pain Management | 40% |

| Anxiety | 10% |

| Insomnia | 10% |

| Cough Suppression | 5% |

| Attention-deficit/hyperactivity disorder (ADHD) | 20% |

| Narcolepsy | 5% |

| Others | 10% |

Why Did the Pain Management Segment Dominate the Controlled Substance Market?

The pain management segment is the dominant application segment in the market by 40%, largely due to the widespread use of opioids and related medications to treat acute, chronic, and cancer-related pain. The growing prevalence of musculoskeletal disorders, post-surgical pain, and palliative care needs further reinforce its dominance. Healthcare providers prioritize effective pain relief to improve quality of life, making controlled substances central to treatment protocols. Despite concerns of misuse, advancements in abuse-deterrent formulations and stringent monitoring programs sustain their adoption. Compared to anxiety, insomnia, ADHD, or narcolepsy, the broader and more frequent clinical use of pain management drugs secures its leading position.

The attention-deficit/hyperactivity disorder (ADHD) segment is estimated to be the fastest-growing application segment in the controlled substance market. Rising diagnosis rates in both children and adults, coupled with increasing awareness and acceptance of treatment, are driving strong demand for stimulant-based therapies. Pharmaceutical advancements, particularly in extended-release and non-addictive formulations, have improved patient compliance and broadened adoption. In addition, telemedicine and digital health platforms are making ADHD diagnosis and prescription management more accessible, further fueling growth. Compared to anxiety, insomnia, or narcolepsy, the rapidly expanding ADHD patient base and innovation in tailored treatments position it as the fastest-growing application segment.

| Segment | Share 2025 (%) |

| Hospitals & Clinics | 50% |

| Pharmacies | 40% |

| Others | 10% |

How the Hospitals & Clinics Segment Dominated the Controlled Substance Market?

The hospitals & clinics segment is the dominant sales channel in the market by 50%, as they serve as the primary point of prescription, administration, and monitoring for these highly regulated drugs. Controlled substances, particularly opioids and stimulants, require strict oversight, which hospitals and clinics provide through specialized healthcare professionals and prescription monitoring systems. Their direct involvement in pain management, surgical care, mental health treatments, and chronic disease management ensures safe distribution and compliance, making them the leading sales channel over retail pharmacies or other outlets.

The pharmacies segment is anticipated to be the fastest-growing sales channel in the controlled substance market, driven by rising prescription volumes, improved accessibility, and patient preference for convenience. Retail and specialty pharmacies play a critical role in dispensing controlled medications for pain, ADHD, and mental health conditions, while ensuring compliance with regulatory requirements through prescription monitoring systems. The expansion of e-pharmacies and digital health platforms in 2025 has further accelerated growth, making controlled drugs more accessible under strict oversight. This combination of accessibility, technology integration, and compliance positions pharmacies as the fastest-growing sales channel.

")

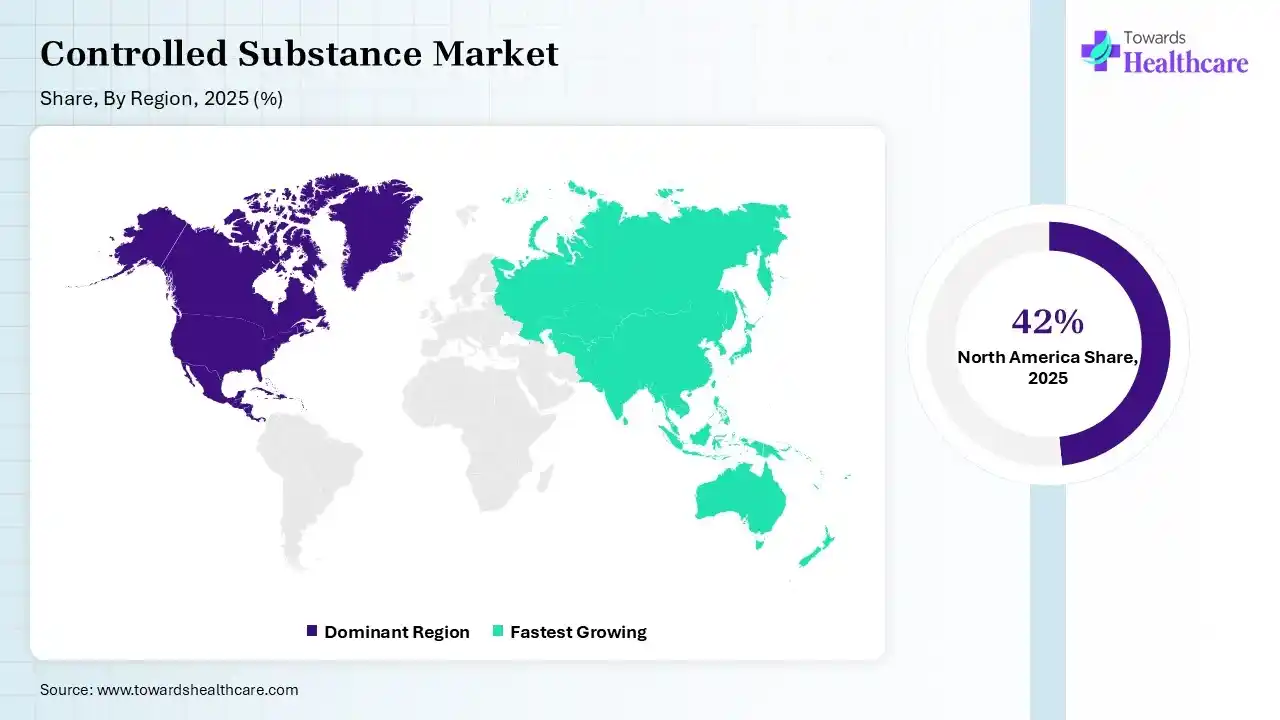

North America dominates the market by 42% share due to its well-established healthcare infrastructure, stringent regulatory frameworks, and advanced monitoring systems that ensure safe prescription and distribution of controlled drugs. Strong pharmaceutical R&D capabilities, coupled with significant investment in drug innovation and advanced delivery technologies, position the region as a leader in therapeutic solutions. High awareness among healthcare providers and patients regarding controlled substance management, alongside robust insurance coverage and government initiatives for chronic disease management, further strengthens market adoption. Additionally, strategic collaborations, partnerships, and a mature supply chain ecosystem enable efficient commercialization, reinforcing North America’s leadership in the controlled substance market.

U.S. Market Trends

The U.S. controlled substance market is valued at about US$ 52.3 billion in 2024 and is expected to rise to US$ 55 billion in 2025. Looking further ahead, the market could reach nearly US$ 84.95 billion by 2034, growing at a steady CAGR of 5.24% between 2025 and 2034.

")

The U.S. controlled substance market benefits from a robust healthcare system, high patient awareness, and stringent regulatory oversight, making it a global leader. Strong R&D infrastructure supports the development of innovative formulations, including opioids, stimulants, and non-opioid alternatives, while advanced delivery technologies improve safety and efficacy. Federal and state-level regulations, including prescription monitoring programs and DEA scheduling, ensure controlled distribution and reduce misuse. Additionally, strategic collaborations, mergers, and partnerships among pharmaceutical companies expand product portfolios and geographic reach. High adoption in chronic pain management, neurological disorders, and mental health treatments further drives market growth across the country.

Canada Market Trends

Canada’s controlled substance market is growing steadily due to the increasing prevalence of chronic pain, neurological, and mental health conditions, coupled with strong regulatory oversight. Federal policies, including Health Canada’s controlled substances framework and prescription monitoring initiatives, ensure safe use and distribution while supporting innovation. Canadian pharmaceutical companies focus on developing advanced formulations and delivery methods, including non-opioid alternatives and extended-release therapies, to enhance patient compliance. Collaborative ventures, partnerships, and acquisitions facilitate market expansion and technology adoption.

The Asia Pacific region is the fastest-growing market for controlled substances due to the rising prevalence of chronic pain, neurological disorders, and mental health conditions, coupled with increasing healthcare awareness and accessibility. Expanding healthcare infrastructure, a growing number of specialty clinics, and improving regulatory frameworks are enabling safer prescription and distribution of controlled drugs. Pharmaceutical companies are investing heavily in research, innovative formulations, and advanced delivery technologies tailored to regional needs. Additionally, rising disposable incomes, urbanization, and growing adoption of prescription medications across emerging economies such as China, India, and Japan are driving rapid demand, positioning the Asia-Pacific region as a key growth hub in the market.

India Strengthens Its Role in the Controlled Substances Market

India is witnessing significant growth in the controlled substances market due to expanding pharmaceutical manufacturing, increasing demand for regulated manufacturing, increasing demand for regulated pain management and anesthesia drugs, and strengthening regulatory oversight of narcotic medicines. Rising healthcare investments, growing hospital infrastructure, increasing adoption of digital prescription and inventory management systems, and expanding export of pharmaceutical products are further driving the demand for secure controlled substance manufacturing, distribution, and compliance solutions across the country.

China Market Trends

China dominates the global precursor chemicals market due to its advanced manufacturing, competitive prices, and extensive logistics network. As the leading chemical producer, China supports both legal and illegal precursor supply chains, with low production costs making it a key supplier for global pharmaceutical components. Its efficient shipping system further enhances global distribution.

| Category | Key Participants | Explanation |

| Technology Providers | Compliance tech vendors, serialization systems providers | Provide digital tracking, audit trails, and regulatory compliance tools for controlled substance handling |

| Product Manufacturers | Pharmaceutical companies (branded + generics) | Develop and produce controlled drugs such as opioids, stimulants, sedatives, and CNS therapeutics |

| Service Providers | Pharmacy benefit managers, distribution logistics firms | Manage dispensing, reimbursement, and secure distribution of regulated drugs |

| Platform Providers | Drug supply chain monitoring platforms | Enable real-time tracking of controlled substances across the supply chain |

| CROs/CDMOs | Contract manufacturing organizations | Manufacture controlled substances under strict regulatory licenses |

| Software Vendors | Regulatory compliance and e-prescription systems | Support prescription monitoring programs and controlled drug reporting |

| Research Institutions | Academic hospitals, neuropharmacology labs | Conduct clinical trials and addiction neuroscience research |

| End-User Industries | Healthcare providers, veterinary medicine, military medicine | Utilize controlled substances for clinical treatment and procedural applications |

R&D

Steps:

Clinical Trials and Approval

Steps:

Regulatory submission and approval

Organizations Involved:

U.S. FDA, Health Canada, EMA, Contract Research Organizations (CROs) like ICON, Parexel, and Covance, Patient Support and Services

Steps:

Strengths

Weaknesses

Opportunities

Threats

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 65% | 25% | 10% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Johnson & Johnson (Janssen Pharmaceuticals) | New Brunswick, New Jersey | USA | Strong CNS portfolio and legacy opioid and anesthesia-related therapeutics under Janssen division | Prescription opioids (legacy), anesthesia agents, CNS disorder therapies |

| Pfizer Inc. | New York, New York | USA | Major CNS and pain management portfolio; significant presence in regulated prescription drugs | Lyrica (pregabalin), CNS therapies, hospital injectable anesthetics |

| AbbVie Inc. | North Chicago, Illinois | USA | Large CNS and psychiatry drug portfolio supporting controlled prescription categories | Depakote, Vraylar, CNS and psychiatric controlled medications |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Mallinckrodt Pharmaceuticals | St. Louis, Missouri | USA | Historically one of the largest opioid manufacturers with controlled substance portfolio | Generic opioids, specialty pain medications, CNS drugs |

| Viatris Inc. | Pittsburgh, Pennsylvania | USA | Large-scale generic drug producer with controlled substance manufacturing capabilities | CNS generics, sedatives, pain management drugs |

| Sun Pharmaceutical Industries Ltd. | Mumbai, Maharashtra | India | Major global generic pharmaceutical company with CNS and controlled drug portfolio | Psychiatric generics, controlled CNS formulations |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Cambrex Corporation | East Rutherford, New Jersey | USA | CDMO specializing in controlled substance manufacturing under strict regulatory compliance | API manufacturing for controlled substances |

| Catalent Pharma Solutions | Somerset, New Jersey | USA | Major CDMO with controlled drug formulation and delivery capabilities | Controlled-release drug formulations, CNS drug manufacturing |

In June 2025, Co-Founder of Elkedonia and Delphine Charvin, Chief Executive Officer, stated that the Elkedonia SAS company has closed an oversubscribed seed funding round worth EUR 11.25 million. Argobio, Angelini Ventures, CARMA Fund, Capital Grand Est, and Sambrinvest participated in the round, which was co-led by Kurma Partners, WE Life Sciences, and the French Tech Seed fund run by Bpifrance on behalf of the French government as part of France 2030.

By Drug Class

By Applications

By Sales Channel

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar