Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

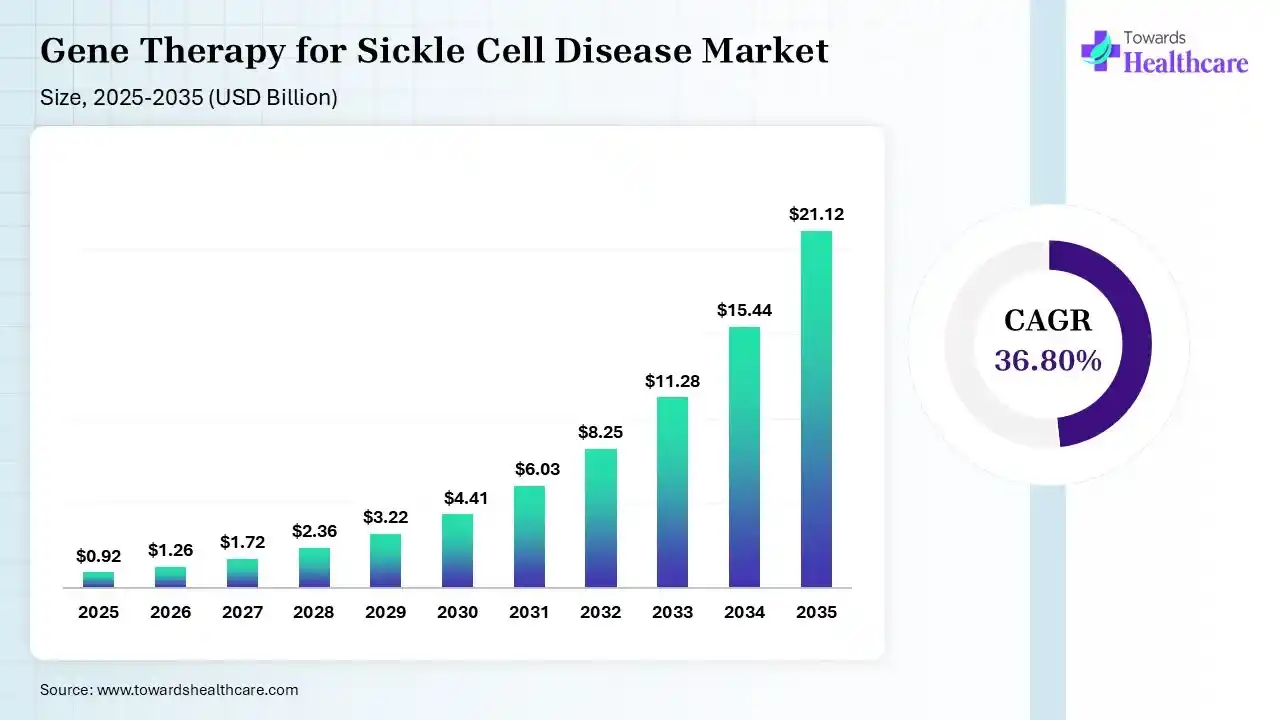

The worldwide gene therapy for sickle cell disease market stood at USD 0.92 billion in 2025, grew to USD 1.26 billion in 2026, and is forecast to reach USD 21.12 billion by 2035, expanding at a CAGR of 36.80% from 2026 to 2035.

")

Around the globe, ongoing major advancements in gene editing, especially CRISPR/Cas9 and other developments, are highly impacting the gene therapy for sickle cell disease market. Along with this, major novel approaches for direct correction of the specific sickle cell mutation within the DNA are another effort going on in the different research areas, acting as a significant growth factor in the adoption of revolutionary methods. These developments are boosting due to emerging heavy investments by several companies and robust regulatory support in the approval of groundbreaking gene therapies for SCD.

The gene therapy for sickle cell disease (SCD) market focuses on the development, manufacturing, and commercialization of genetic therapies aimed at treating or curing sickle cell disease by directly addressing its underlying genetic mutation. These therapies involve gene addition, gene editing, or gene silencing techniques to restore normal hemoglobin production, reduce vaso-occlusive crises, and improve patient outcomes. Major approaches include lentiviral vector-based gene addition, CRISPR/Cas9-mediated gene editing, and gene-modified hematopoietic stem cell (HSC) transplantation.

A surge in the development of more effective and permanent treatments, and expanded patient awareness, is widely impacting the overall market expansion.

In 2025, AI algorithms will play a major role in boosting customized treatment design, transforming gene therapy vector development, expanding clinical trial success, simplifying manufacturing processes, and enhancing patient risk stratification. Prospective research activities are focusing on the evolution of in vivo (directly within the body) therapies to omit the restraints of ex vivo (outside the body) modification and the need for expensive, complex conditioning regimens.

Driver

Ongoing R&D Activities and Widespread Applications

The global gene therapy for sickle cell disease market has been experiencing significant growth due to the increasing severity of sickle cell disease among people. This further assists in major investments in R&D activities to evolve next-generation therapies, including new gene therapies and other curative treatments. Along with this, other crucial advancements in the refinement of gene editing tools, especially CRISPR-Cas9, are transforming treatment possibilities, which ultimately enable the permanent correction of faulty hemoglobin genes.

Restraint

Limitations in the Production Process

The major production process for gene therapies comprises complex and time-consuming stages, which finally limit the number of treatments that can be manufactured and administered. Moreover, rising restrictions in lower- and middle-income countries, where the disease has a huge burden, where companies will pose several difficulties in conducting clinical trials for these therapies.

Opportunity

Empowerment in In Vivo Gene Therapy

The global gene therapy for sickle cell disease market will have several crucial opportunities in the coming years, such as a rise in emphasis on in vivo gene therapy. For this developing opportunity, diverse areas are emerging with novel therapies to deliver genetic change directly into the patient's body, probably omitting the need for ex vivo cell manipulation and chemotherapy conditioning. Whereas, recently developed gene silencing of BCL11A facilitates the body to produce fetal hemoglobin.

| Table | Scope |

| Market Size in 2026 | USD 1.26 Billion |

| Projected Market Size in 2035 | USD 21.12 Billion |

| CAGR (2026 - 2035) | 36.80% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By therapy type, By vector type, By treatment approach, By technology, By end user, By region |

| Top Key Players | Bluebird Bio, Vertex Pharmaceuticals, CRISPR Therapeutics, Editas Medicine, Sangamo Therapeutics, Beam Therapeutics, Graphite Bio, Novartis AG, Pfizer Inc., Intellia Therapeutics, Allogene Therapeutics, Orchard Therapeutics, Aruvant Sciences, Gilead Sciences, Precision BioSciences |

The gene addition therapy segment dominated with a major revenue share of the gene therapy for sickle cell disease market in 2025. Primarily, the segment is driven by its major focus on providing the body with a functional gene copy to produce healthy hemoglobin, which potentially enables a promising solution to the disease. Alongside, the emerging novel approaches in gene delivery, mainly in lentiviral vectors, which offer the effective and stable transfer of functional genes into HSCs, ultimately making gene addition therapy feasible.

Whereas the gene editing therapy segment is anticipated to witness the fastest growth in the predicted timeframe. The major driver for this segment expansion is phenomenal advancements in the technologies, such as CRISPR-Cas9 for accurate genetic modification, and the unmet medical requirement for a definitive cure for the disease. Apart from this, other developing aspects of CRISPR, like its fusion systems with other enzymes, including recombinases, polymerases, and ligases, are enabling larger and more complex gene edits.

In 2025, the lentiviral vectors segment accounted for a major share of the gene therapy for sickle cell disease market. The advantages of these kinds of vectors are the versatility and a safe approach for gene delivery to hematopoietic stem cells (HSCs). The huge adoption of lentiviral vectors is allowing the transduction of both dividing and non-dividing cells, with their accelerated capacity for stable integration into the host genome, and exclusive safety as compared to other vectors, as well as ongoing clinical trials, are assisting the comprehensive market expansion.

However, the adeno-associated viral (AAV) vectors segment is predicted to expand rapidly during 2025-2035. The major benefit of these vectors is their long-term gene expression for prolonged periods, making them favorable for treating chronic conditions, particularly SCD. Additionally, ongoing research activities in AAV serotypes and capsid engineering are improving tissue targeting and transduction efficacy for specific applications, like bone marrow-derived cells used in SCD therapy. As well as exo-AAVs and optimized brain delivery techniques are also influencing the segment’s development.

In the gene therapy for sickle cell disease market, the ex-vivo gene therapy segment captured the biggest revenue share in 2025. The segment is fueled by its wider range of adoption in the coverage of the unmet need for a cure, the breakthroughs in gene editing technologies (like CRISPR-Cas9), and promising clinical trial results for approved treatments. The ex-vivo gene therapy possesses targeted application, which is well-suited for targeting a specific organ or system, especially the blood-forming cells.

The in-vivo gene therapy segment is estimated to register rapid expansion during the forecast period. This approach comprises a major advantage, such as its robust affordability in cell harvesting, omitting expenses in ex-vivo manipulation, and complex manufacturing. Alongside, they are simpler, portable, and need less specialized infrastructure, which can dramatically boost access to treatment for patients, mainly in regions with high SCD cases but restricted healthcare resources. Also, it generates a more simplified and patient-friendly approach, which is frequently employed for ex vivo therapies and carries significant healthcare burdens.

By technology, the CRISPR/Cas9 segment led the gene therapy for sickle cell disease market in 2025. This technology encompasses the transforming properties, such as it is a precise, versatile, and revolutionary tool for genome engineering, which has a vast contribution for targeted gene correction and the reactivation of fetal hemoglobin (HbF). In addition, the accelerating investment from private and public organizations, like the National Institutes of Health, fosters the development of innovative CRISPR-based therapies and expands their clinical translation.

On the other hand, the base & prime editing segment is expected to expand rapidly during 2025-2035. The segment is propelled by its allowance for accurate single-point mutations to be corrected without causing double-strand breaks (DSBs), which are a risk in conventional CRISPR-Cas9 technologies. Whereas the prime edition is a highly versatile tool, which can be used in all types of point corrections, insertions, and deletions, with increased precision and minimal bystander edits. Nowadays, researchers are investing in PEmax and base editors with modified deaminase domains.

In 2025, the hospitals & transplant centers segment was dominant in the gene therapy for sickle cell disease market. An escalating SCD prevalence is increasingly enhancing the usage of novel gene therapy in these end-users. As these hospitals and transplant centers comprise the well-developed infrastructure and technology essential in complex gene therapy procedures and associated care, like blood transfusions and sterile environments, they are mainly driving the overall segment expansion. Furthermore, the presence of easy accessibility to a wider range of specialists, particularly hematologists and gene therapy experts, impacts their expansion.

Although the research institutes segment is estimated to grow at a rapid CAGR in the coming era. Combined factors contribute to the development of research institutes, such as ongoing advances, including CRISPR-based therapies are providing greater efficiency, and a supportive regulatory landscape, like the U.S. FDA, playing a vital role in the approval of innovative therapies for SCD. These institutes are recently merged plans for the insertion of a modified β-globin gene or editing the gene to functionally correct the SCD mutation. Besides this, the rising demand for tailored treatments for genetic disorders and the potential of gene therapy to facilitate sustainable or curative solutions are major market drivers.

In 2025, North America captured the biggest revenue share of the gene therapy for sickle cell disease market. This region has experienced immense growth due to the heavy investment in research and development of gene therapies by both large and small companies. This also further assists in the detection of new drug molecules for SCD. This kind of therapy offers a wider transforming approach for hereditary concerns, which further expands the focus on the management of symptoms to facilitate a possible one-time cure for patients in North America.

For instance,

U.S. Market Trends

The US is one of the crucial countries in North America in the gene therapy for sickle cell disease market development. Whereas the US’s supporting steps from various regulatory agencies, like the U.S. Food and Drug Administration (FDA), promote programs, such as Fast Track and Breakthrough Therapy Designation, which further escalate the development and approval of these novel treatments.

For this market,

Canada Market Trends

In Canada, the market is fueled by the emergence of both the FDA and Health Canada, which have approved therapies to enhance fetal hemoglobin (HbF) production, thereby preventing the effects of sickle cell disease. Nowadays, Canadian researchers are working on lipid nanoparticles as delivery vehicles to carry gene-editing tools into cells, which is a significant step toward in vivo gene editing.

During 2025-2034, Europe is estimated to register the fastest expansion in the gene therapy for sickle cell disease market. Eventually, Europe has been experiencing immense growth due to the presence of a robust pharmaceutical hub and technological advancements. These advances are further coupled with regulatory support, such as the European Medicines Agency (EMA) and other bodies are enabling simplified approval processes and incentives, like orphan drug status. European scientists are demonstrating a newer technique by applying CRISPR/Cas9 to eliminate an intermediate piece of DNA, gaining inactive, protective genes closer to genetic enhancers (switches) to restart their activity and compensate for the faulty gene causing SCD.

For instance,

R&D

The gene therapy for sickle cell disease market includes the identification of a gene target, the collection of a patient's blood-forming stem cells, and then the reinfusion of the modified cells into the patient after conditioning to make space in the bone marrow.

Key Players: Vertex Pharmaceuticals, CRISPR Therapeutics, Bluebird Bio, etc.

Clinical Trials and Regulatory Approvals

In this stage, subjects are recruited, and consent is obtained for a complex process in which their stem cells are going to be collected and modified for the detection of required safety, efficacy, and adverse effects. And, further, they will acquire the FDA's Biologics License Application (BLA) for approval.

Key Players: David Williams, Washington University School of Medicine, Essen Biotech, Memorial Sloan Kettering Cancer Center, etc.

Patient Support and Services

This can be done through pre-treatment consultation with physicians, long-term clinical follow-up (often 2-3 years in a hospital and ongoing outpatient visits), and the probability of community-based patient registries for tracking long-term results.

Key Players: Gates Foundation, Novartis, Precision BioSciences, etc.

By Therapy Type

By Vector Type

By Treatment Approach

By Technology

By End User

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar