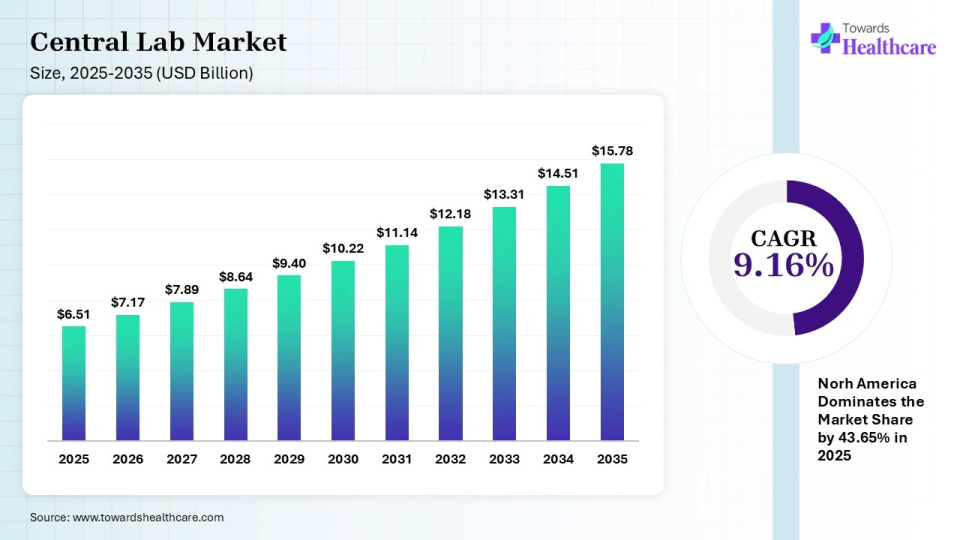

The global central laboratory market, valued at USD 7.17 billion in 2026, is projected to reach USD 15.78 billion by 2035, growing at a CAGR of 9.16% due to rising R&D investments and increasing demand for clinical trials.

")

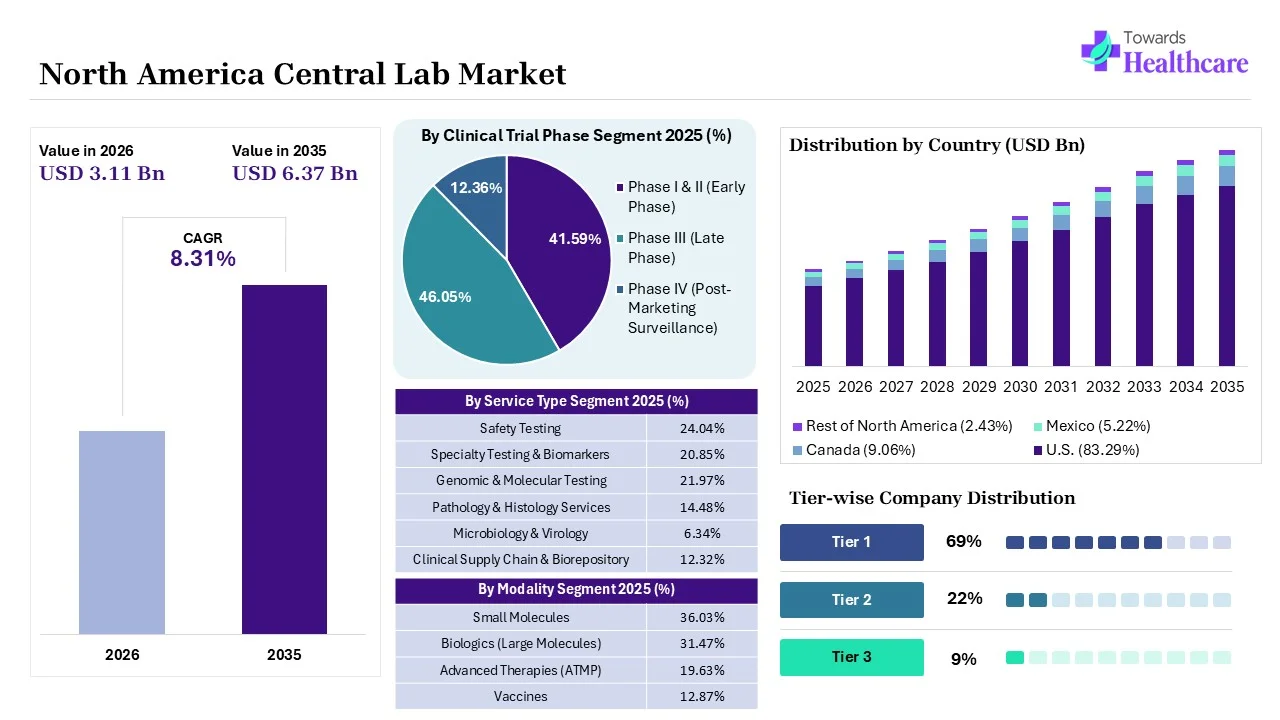

The North America central lab market size is calculated at USD 2.84 billion in 2025, grew to USD 3.11 billion in 2026, and is projected to reach around USD 6.37 billion by 2035. The market is expanding at a CAGR of 8.31% between 2026 and 2035.

")

The North America central lab market is primarily driven by the increasing number of clinical trials and favorable regulatory policies. North American countries have specialized infrastructure to set up central labs and perform complex experiments. Government organizations provide funding to support clinical trials and research activities. Prominent players collaborate to access advanced technologies and tailored services. Artificial intelligence (AI) and big data analytics are set to become more instrumental in clinical research.

The North America central lab market is experiencing robust growth, driven by the rising prevalence of chronic disorders, growing demand for personalized medicines, and technological advancements. It refers to providing a wide range of services related to clinical trials, from sample preparation and consistent testing procedures to quality control measures. A central lab is a large, specialized facility that is independent of the trial sponsor and processes the laboratory samples drawn from study participants

AI plays a vital role in central labs by introducing automation in laboratory operations, enhancing the efficiency and accuracy of research outcomes. Automation streamlines various tasks, including sample preparation, sample tracking and processing, data handling, and quality control management. AI and machine learning (ML) algorithms can analyze vast amounts of data and help researchers interpret complex datasets. They can also streamline the supply chain and logistics of clinical trial products, ensuring the timely delivery. AI can be used to oversee data tracking and integration across multiple trial sites, enabling accurate recording and transmission of sample data.

| Countries | Regulation | Objectives |

| United States | Clinical Laboratory Improvement Amendments (CLIA) | To ensure quality laboratory testing. Clinical labs require CLIA certification to accept human samples for testing. |

| Canada | Laboratories Canada's strategy | To strengthen federal science through collaboration, bringing scientists together in modern, sustainable laboratories specially designed to support their work. |

| Table | Scope |

| Market Size in 2026 | USD 3.11 Billion |

| Projected Market Size in 2035 | USD 6.37 Billion |

| CAGR (2026 - 2035) | 8.31% |

| Key Applications | Clinical trials, biomarker testing, companion diagnostics, genomic testing, safety monitoring, pharmacokinetic testing, pathology review |

| Primary End Users | Pharmaceutical companies, biotechnology firms, CROs, medical device companies, academic research organizations |

| Key Growth Drivers | Growth in clinical trials, precision medicine adoption, biomarker-driven drug development, increasing oncology studies, decentralized clinical trials, genomics expansion |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Therapeutic Area, By Clinical Trial Phase, By Modality, By End-User |

| Top Key Players | SGS SA, REPROCELL, Frontage Central Labs, LabConnect, IQVIA, ACM Global Laboratories, Celerion, MLM Medical Labs, Medpace, CTI Clinical Trial and Consulting Services, Inc., Central Testing Laboratory |

The Safety Testing Segment Led the Market in 2025

The safety testing segment led the North America central lab market with a 24.04% share in 2025 because of rising clinical trial volumes and strict regulatory requirements mandating thorough pharmacological evaluations. Expanding biopharmaceutical pipelines demands rigorous preclinical and clinical assessments to verify efficacy and prevent adverse reactions.

The genomic & molecular testing segment held a 21.97% share in 2025 & is predicted to grow at a 9.63% CAGR in the studied years. Respective expansion is fueled by the booming demand for tailored oncology, a rigorous clinical pipelines & ongoing immersive latest genetic testing unification. Alongside, numerous firms are fostering the adoption of Next-Generation Sequencing (NGS). These services serve as a backbone for complex multi-site clinical trials & targeted drug development.

The specialty testing & biomarkers segment held a 20.85% share of the North America central lab market in 2025. Growth was supported by increasing adoption of precision medicine, biomarker-driven clinical trials, and demand for advanced diagnostic insights across therapeutic areas. Pharmaceutical and biotechnology companies increasingly rely on specialized testing to improve patient stratification and treatment outcomes.

The pathology & histology services segment held a 14.48% share in 2025. Expansion was fueled by rising cancer cases, greater demand for tissue-based diagnostics, and growing clinical research activities. Histology and pathology assessments remain essential for disease diagnosis, therapeutic decision-making, and evaluation of treatment effectiveness in both routine healthcare and clinical trial settings.

The Oncology Segment Led in 2025

The oncology segment dominated with a 33.55% share of the North America central lab market in 2025. North America is experiencing a transition from traditional chemotherapy to targeted therapies, immunotherapies, & cell/gene therapies, which necessitates modern, highly specific diagnostic testing. Additionally, the market is emphasising the elimination of centralised oncology trials, particularly in large urban academic medical centres, where labs are adjusting workflows to process samples collected at remote or community sites.

The infectious diseases segment held a market share of 20.64% in 2025. Growth was driven by the persistent burden of infectious diseases, increasing demand for diagnostic testing, and expanding clinical research focused on emerging pathogens. Central laboratories play a critical role in supporting large-scale infectious disease studies, vaccine development programs, and surveillance initiatives, ensuring standardized testing, reliable data generation, and efficient trial management across multiple research sites.

The cardiovascular & metabolic diseases (CVMD) segment held a North America central lab market share of 20.64% in 2025. The segment benefited from the growing prevalence of cardiovascular disorders, diabetes, obesity, and related metabolic conditions throughout North America. Rising investments in clinical trials, increasing biomarker-based assessments, and demand for specialized laboratory services supported growth. Central laboratories provide comprehensive testing capabilities that enhance patient monitoring, disease evaluation, and treatment outcome assessments.

The rare diseases & genetic disorders segment held a 5.42% share in 2025 & is anticipated to witness rapid growth at a 11.95% CAGR in the coming years. A prominent driver is accelerating biopharmaceutical research into rare & inherited diseases, which require centralised laboratories to handle biomarker testing, standardise sample analysis, & support companion diagnostics across several clinical trial sites. Especially, the NORD Rare Disease Centers of Excellence, which simplify multi-site trials, & the RDCA-DAP platform.

The Phase III Segment Led the Market in 2025

The phase III segment dominated the North America central lab market with a 46.05% share in 2025. The segment's leadership was driven by the large number of late-stage clinical trials required to confirm safety and efficacy before regulatory approval. Pharmaceutical and biotechnology companies invest heavily in phase III studies because they involve extensive patient populations, multiple study locations, and comprehensive laboratory testing, creating substantial demand for central laboratory services.

The phase III segment held a 41.59% share of the market in 2025 and is expected to grow at the fastest CAGR of 8.85% during the forecast period. Growth is supported by rising drug development activities, increasing biologics and specialty therapeutics pipelines, and greater adoption of decentralized and hybrid clinical trial models. Sponsors continue expanding phase III programs to accelerate approvals, improve clinical outcomes, and address growing demand for innovative treatments across therapeutic areas globally.

The phase IV segment held a significant market share of 12.36% in 2025. The segment benefited from increasing post-marketing surveillance requirements and the need to monitor the long-term safety and effectiveness of approved therapies. Growing regulatory emphasis on real-world evidence, patient outcome tracking, and pharmacovigilance activities has increased demand for laboratory support services, enabling sponsors to collect valuable data after commercial product launches.

The Small Molecules Segment Dominated the Market in 2025

In 2025, the small molecules segment led with a 36.03% share of the North America central lab market in 2025. Dominance is propelled by their outstanding structural stability, oral bioavailability, & standardized chemical analysis. These molecules are playing a pivotal role in the growing cases of cardiovascular disease and Alzheimer's that demand large-scale trial networks.

The biologics segment captured a market share of 31.47% in 2025. The segment's strong performance was driven by the rising development of monoclonal antibodies, cell and gene therapies, and other advanced biologic treatments. Increasing investment in biologics research, growing prevalence of chronic diseases, and expanding clinical trial pipelines significantly boosted demand for specialized central laboratory testing and biomarker analysis services.

Whereas, the advanced therapies (ATMP) segment captured a 19.63% share in 2025 & is expected to show the fastest growth at a 12.10% CAGR in the coming years. This mainly covers diverse gene & cell therapies, which facilitate crucial benefits. Gradually, central labs are transforming to next-generation sequencing (NGS), digital pathology, & flow cytometry to control the intricate biological endpoints of therapies, such as CAR-T.

The vaccines segment captured a significant North America central lab market share of 12.87% in 2025. Growth in this segment was supported by continued focus on infectious disease prevention, expanding immunization programs, and increasing vaccine research activities. Pharmaceutical companies and research organizations relied heavily on central laboratories for immunogenicity testing, safety monitoring, and standardized sample analysis across multicenter vaccine clinical trials in North America.

The Pharmaceutical & Biotechnology Companies Segment Led the Market in 2025

In 2025, the pharmaceutical & biotechnology companies segment captured the largest share of 61.61% of the market in 2025. Specifically, large & developing biopharma players outsource to overcome the huge capital spending connected with building & maintaining certified, industrial-scale lab infrastructures. Well-established, these firms are providing advanced supply chain management, like secure kit provision, temperature-controlled sample tracking, & rapid delivery networks across the continent.

However, the contract research organizations (CROs) segment accounted for a 17.17% share in 2025 & is estimated to expand rapidly at a 9.83% CAGR in the predicted timeframe. They operate under stringent guidelines & further offer uniform testing across all clinical trial sites by maintaining standard operating procedures (SOPs), compliant data management systems, & specialized certifications, like ISO or CAP/CLIA. CROs are majorly accelerating the processing, analysis, & reporting of clinical data, expediting time-to-market for new therapeutics.

The academic & government research institutes segment captured an 11.40% share of the North America central lab market in 2025. The segment's growth was supported by increasing government-funded research programs, expanding clinical and translational studies, and rising collaborations between academic institutions and pharmaceutical companies. These organizations rely on central laboratory services for standardized testing, data consistency, and regulatory compliance, enabling efficient execution of large-scale research projects and multicenter clinical investigations.

The clinical diagnostic laboratories segment captured a 9.82% share in 2025. Growth in this segment was driven by increasing demand for specialized testing services, growing sample volumes, and the need for advanced laboratory capabilities. Clinical diagnostic laboratories frequently partner with central labs to access high-complexity testing, improve operational efficiency, ensure quality assurance, and support clinical trials requiring standardized and reliable laboratory data.

The rising prevalence of chronic disorders, the increasing number of complex clinical trials, and the growing demand for personalized medicines are the major factors that contribute to market growth. Favorable regulatory support facilitates the development of novel drugs, biologics, and medical devices. Government and private organizations provide funding and launch initiatives for revolutionizing research and clinical trial activities. Additionally, the rising adoption of advanced technologies in central labs fosters market growth.

U.S. Market Trends

In 2025, the U.S. held a major share of 83.29% of the North America central lab market. The presence of key players and the presence of a robust clinical trial infrastructure propel the market. Key players, such as LabCorp, PPD, and IQVIA, are the major contributors to the market in the U.S. As of September 2025, 185,901 clinical trials based in the U.S. were registered on the clinicaltrials.gov website. The National Institute of Health (NIH) invests approximately $30.1 billion in medical research every year.

Canada Market Trends

However, Canada captured a 9.06% share in 2025 & is predicted to witness rapid expansion at a 9.86% CAGR during the forecast period. Central Labs and Central Testing Laboratory Ltd. are the key laboratories that provide clinical trial testing services in Canada. There are 30,966 clinical trials in Canada registered on clinicaltrials.gov, as of September 2025. Canada ranks 6th in the global pharmaceutical market, with a global share of 2.1%. Additionally, Canada accounts for 4% of the global clinical trials and is a G7 leader in clinical trial productivity.

Mexico Market Trends

Mexico held a notable 5.22% share in 2025 & is estimated to expand at a 9.40% CAGR in the coming years. Its expansion is driven by broadening its public health capabilities through initiatives, such as the development of CEMPRE, the main training center for pandemic preparedness & response. Recently, the Central Laboratory at the Hospital General de México (HGM) explored an integration of over 35 high-performance automated analyzers, robotic sample transport belts, & sophisticted mass spectrometry in its bacteriology section.

| Ecosystem Segment | Description | Representative Participants |

| Technology Providers | Laboratory automation, diagnostics, genomic technologies, testing platforms | Thermo Fisher Scientific, QIAGEN, Illumina |

| Product Manufacturers | Reagents, assay kits, diagnostic instruments | Thermo Fisher Scientific, Bio-Rad, Agilent |

| Service Providers | Central laboratory testing and sample management services | Labcorp, Eurofins Scientific, ICON |

| Platform Providers | Clinical trial data integration and analytics platforms | IQVIA, Labcorp, Medidata |

| CROs | Integrated clinical trial execution and laboratory support | IQVIA, ICON, Medpace, Parexel |

| Specialty Central Labs | Biomarker, genomic, pathology, immunology testing specialists | ACM Global Laboratories, BioAgilytix, Frontage Laboratories |

| Software Vendors | Laboratory information management and clinical data systems | IQVIA Technologies, LabVantage, STARLIMS |

| Research Institutions | Clinical and translational research centers utilizing central lab services | Mayo Clinic, Cleveland Clinic, MD Anderson Cancer Center |

| End-User Industries | Pharma, biotech, medical devices, diagnostics, academia | Drug developers and research organizations |

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 69% | 22% | 9% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Labcorp | Burlington, North Carolina | USA | Largest and most recognized central laboratory provider supporting global clinical trials | Central laboratory services, biomarker testing, genomics, specimen management |

| IQVIA | Durham, North Carolina | USA | Leading integrated CRO and central laboratory provider | IQVIA Laboratories, clinical trial testing, data management |

| Thermo Fisher Scientific (PPD Central Labs) | Waltham, Massachusetts | USA | Extensive global clinical research and laboratory network | PPD Central Labs, specialty testing, bioanalysis |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services Related to Keyword |

| Medpace | Cincinnati, Ohio | USA | Strong CRO with integrated central lab infrastructure | Central lab testing, clinical trial support |

| Charles River Laboratories | Wilmington, Massachusetts | USA | Expanding translational and biomarker laboratory services | Biomarker testing, specialty laboratory services |

| SGS Life Sciences | Geneva | Switzerland | Significant central laboratory operations supporting global trials | Clinical trial laboratory services |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services Related to Keyword |

| ACM Global Laboratories | Rochester, New York | USA | Dedicated central laboratory provider with growing trial presence | Global central laboratory services |

| BioAgilytix | Durham, North Carolina | USA | High-growth bioanalytical and biomarker specialist | Biomarker and immunogenicity testing |

| Frontage Laboratories | Exton, Pennsylvania | USA | Expanding clinical trial laboratory services provider | Central lab and bioanalytical testing |

Our experts analyzed that the demand for central labs is booming in North America, with technological innovations and evolving regulatory landscapes. Countries like the U.S. and Canada are at the forefront of developing novel products, strengthening their global position in the clinical trial market. According to our analysis, the growing need for decentralized clinical trials and the development of an established central lab network across the continent positively impact market growth.

By Service Type

By Therapeutic Area

By Clinical Trial Phase

By Modality

By End-User

By Geography

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar