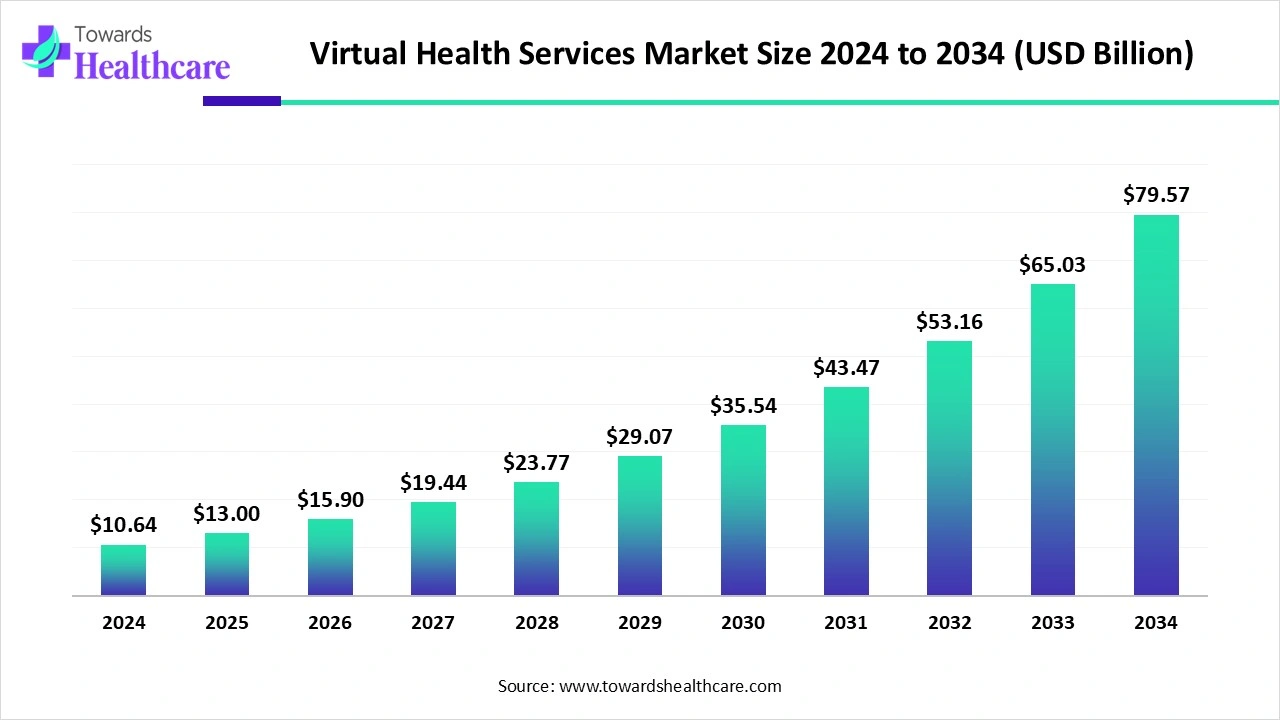

The global virtual health services market size reached USD 13.03 billion in 2025, grew to USD 15.95 billion in 2026, and is projected to hit around USD 98.65 billion by 2035, expanding at a CAGR of 22.44% during the forecast period from 2026 to 2035.

Virtual healthcare includes various remote healthcare services that use information and communication technology, clinical services, administration, medical education, and training for healthcare providers. Virtual care communication tools such as videoconferencing software, remote health monitoring, wearable devices, personal health records, etc., improve patient engagement and patient communication.

The expansion of telehealth and telemedicine is driven by different therapies, such as occupational therapy, speech-language therapy, physical therapy, and telehealth nurses. Virtual healthcare is advantageous in increasing patient accessibility and patient engagement, and decreasing costs and travel expenses for medical visits.

Virtual health services (telehealth/telemedicine) are digital delivery models that provide clinical care, monitoring, and health-related services remotely using audio/video consultations, asynchronous messaging, remote patient monitoring (RPM), virtual urgent care, telepsychiatry, and digital-first chronic care management. These services reduce geographic barriers, lower the cost of care, expand access for underserved populations, and integrate with in-person care pathways. Growth drivers include broadband/smartphone penetration, aging populations, value-based care models, clinician acceptance of telehealth workflows, and payer and regulatory support for remote-care reimbursement.

Artificial intelligence is significant in medical diagnosis, radiology, pathology, dermatology, ophthalmology, cardiology, and many other medical purposes. AI facilitates multimodal diagnosis and detection of infectious diseases. AI also plays a pivotal role in treatment planning, personalized medicine, oncology treatment, telemedicine, medical billing, and other versatile applications. It improves patient care through telemedicine platforms and keeps track of patient health.

The growing patient volumes and increasing chronic diseases are also increasing the demand for virtual health services for remote health monitoring, disease management, virtual consultation, and digital follow-ups.

Different types of wearable devices, cloud platforms, and mobile health apps are being developed to offer enhanced virtual health services like personalized treatment, real-time diagnostics, and predictive insights.

To make virtual health services more accessible and affordable, the companies are developing various hybrid models offering in-person and virtual services, which is increasing their acceptance rates.

What are the Various Trends Observed in the Virtual Health Services Market?

The key emerging trends, such as medical consultations using virtual and augmented reality, remote patient monitoring, and robust data security measures, drive the expansion of virtual healthcare platforms. Virtual reality is becoming valuable due to its therapeutic applications in mental health therapies, physical rehabilitation, pain management, and interactive experiences.

What are the Potential Challenges in the Virtual Health Services Market?

Some of the health systems are reducing or discontinuing virtual medical visits due to less need to take any health precautions for certain patients or a lack of adequate reimbursement to organizations. The growing interest in patients for in-person medical consultation and treatments presents limitations to virtual care among those patients. The changes to payment incentives also lead to reduced preferences for virtual care.

What is the Future of the Virtual Health Services Market?

In August 2025, the World Health Organization and Society of Robotic Surgery introduced a health innovation initiative for the expansion of access to telesurgery and virtual care.This new partnership also aims to promote equity through health systems innovation and telesurgery in remote and underserved regions. In July 2025, the WHO launched a new digital tool to support pregnant women in the self-monitoring of blood pressure.

| Table | Scope |

| Market Size in 2026 | USD 15.95 Billion |

| Projected Market Size in 2035 | USD 98.65 Billion |

| CAGR (2026 - 2035) | 22.44% |

| Leading Region | North America by 46% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Delivery Model/Provider Type, By Technology/Modality, By End User/Patient Segment, By Payer/Reimbursement Model, By Region |

| Top Key Players | Teladoc Health, Amwell, Doctor On Demand / Included Health, MDLive, Babylon Health, PlushCare, VA / U.S. Department of Veterans Affairs, Kaiser Permanente, UnitedHealth Group / Optum, CVS Health / MinuteClinic & CVS Virtual Care, Walgreens Boots Alliance / Care-centric partnerships, Babylon / local partners, Amwell competitors in specialty: DoctorSpring / Specialty telehealth vendors, Livongo / chronic care platforms, Philips, ResMed, BioTelemetry / Philips-owned cardiac & RPM services, Hims & Hers Health, Microsoft / Google Cloud, Epic / Cerner |

")

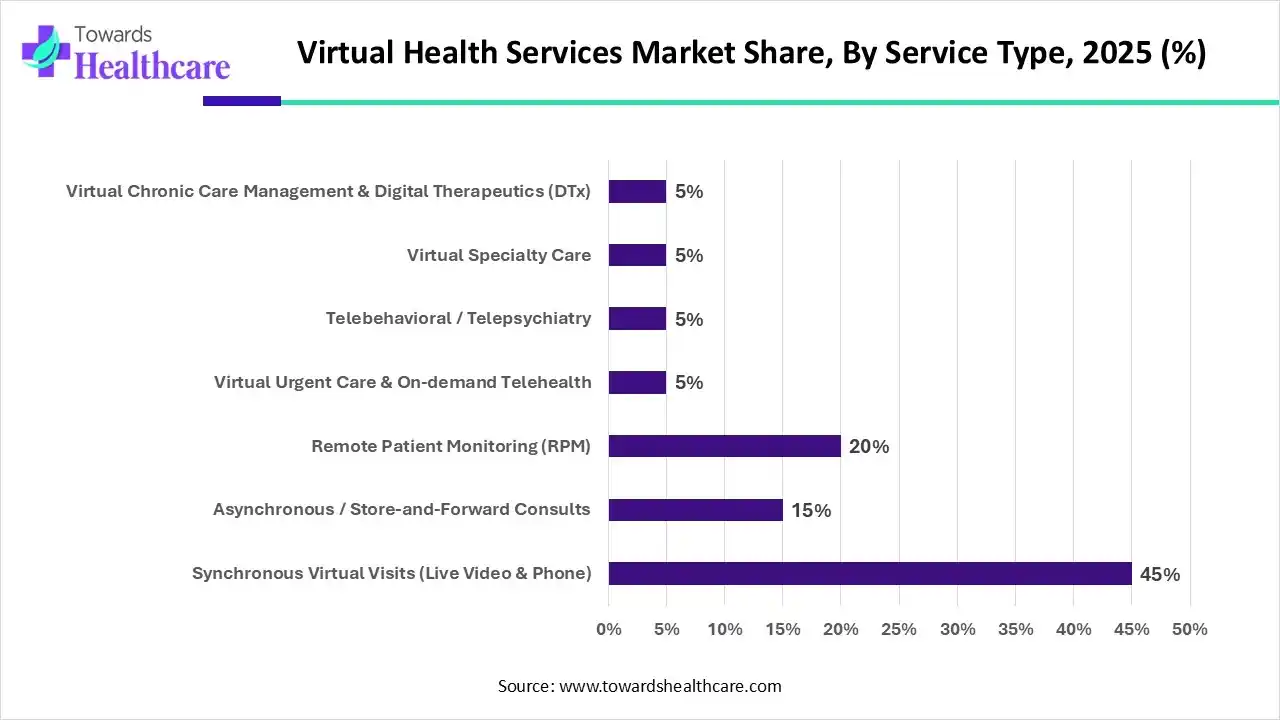

How does the Synchronous Virtual Visits Segment Dominate the Virtual Health Services Market in 2025?

The synchronous virtual visits segment dominated the market by 45% in 2025, owing to enhanced access to care and improved access to specialists. These medical visits result in enhanced patient engagement and increased patient privacy. Healthcare providers experience streamlined workflow, increased efficiency, and professional collaborations.

The remote patient monitoring segment is expected to grow at the fastest CAGR in the market during the forecast period due to its benefits in timely disease detection, improved chronic disease management, and increased access to care. Clinical healthcare providers improve their clinical decision-making and optimize clinical staff efficiency. Remote patient monitoring results in enhanced care coordination, reduced risk of infection, and enhanced patient education.

| Segment | Share 2025 (%) |

| Provider-to-Patient Platforms | 50% |

| Employer/Workplace Virtual Care Programs | 20% |

| Virtual-first Primary Care | 10% |

| Health System/Hub-and-Spoke Telehealth Networks | 10% |

What made Provider-to-Patient Platforms the Dominant Segment in the Virtual Health Services Market in 2025?

The provider-to-patient platforms segment dominated the market by 50% in 2025, owing to the benefits of remote healthcare to providers in terms of increased efficiency, productivity, expanded patient reach, and improved patient management. It enhances collaboration and communication and reduces administrative burden. The growth of these remote healthcare platforms is driven by the integration of telemedicine, remote patient monitoring, electronic health records, real-time communication, and many other factors.

The employer/workplace, employer/workplace virtual care programs segment is expected to grow at the fastest CAGR in the market during the predicted timeframe due to increased efforts for enhanced employee wellness and productivity. The focus is shifting towards improved mental health, work-life balance, and early access to primary care at the workplace. The lower healthcare costs and proactive health management are driving the virtual care programs at the workplace for employees.

How did the Video & Voice Communication Segment Dominate the Virtual Health Services Market in 2025?

The video & voice communication segment dominated the market by 48% in 2025, owing to the numerous benefits of telehealth and telemedicine for both patients and healthcare providers. These services and solutions facilitate flexible scheduling, reduced wait times, and increased access to healthcare for vulnerable populations. They strengthen the patient-provider relationship and allow more comfortable and open communication between the patient and provider.

The remote monitoring devices & wearables segment is expected to grow at the fastest CAGR in the market during the forecast period due to improved chronic disease management and enhanced patient engagement. These remote services and solutions facilitate reduced need for in-person visits and increased access to care. They offer personalized care, increased patient safety, and peace of mind for patients.

Which Segment in End User/ Patient Segment Dominated the Virtual Health Services Market in 2025?

The general acute care/adults segment dominated the market by 55% in 2025, owing to the reduced risk of nursing home admissions and improved patient care. Virtual care facilitates a shorter length of hospital stay, lower hospital costs, and lower post-discharge costs. It also allows a patient-centered and interdisciplinary team approach.

The behavioral health patients segment is expected to grow at the fastest CAGR in the market during the forecast period due to improved emotional and mental well-being of patients. Virtual healthcare offers enhanced self-esteem and self-worth for patients. Patients experience better moods, reduced anxiety, greater emotional regulation, and increased resilience.

How does the Fee-for-Service Telehealth Reimbursement Segment Dominate the Virtual Health Services Market in 2025?

The fee-for-service telehealth reimbursement segment dominated the market by 35% in 2025, owing to the increased revenue generation for providers and transparency in billing. It improves efficiency, cost savings, flexibility for patients, and patient choice. The providers are reimbursed for each service given, including telehealth services, through this traditional payment model.

The value-based/capitated programs segment is expected to grow at the fastest CAGR in the market during the forecast period due to improved patient outcomes, reduced healthcare costs, and enhanced patient satisfaction. These virtual care programs also provide increased access to care and improved care coordination. They are beneficial for healthcare providers, patients, payers, and the healthcare system.

")

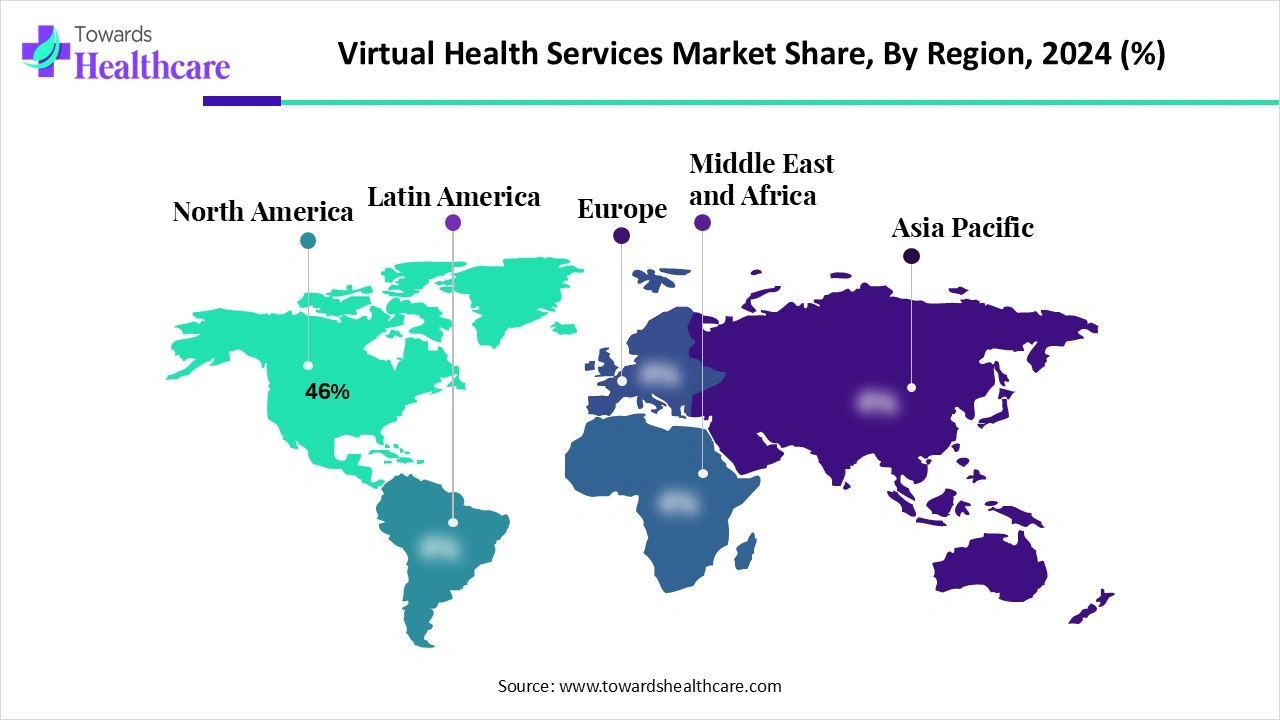

North America dominated the market share 46% in 2025, owing to the increased adoption of digital health and telehealth solutions. There is a favorable regulatory environment and reimbursement policies for telehealth services across this region. Governments, companies, and healthcare systems are focusing on cost-effectiveness and delivering efficient healthcare services. The Health Resources and Services Administration (HRSA) and the U.S. Government expanded telehealth access options for the health of the rural population and the behavioral health of patients. The American Hospital Association (AHA) makes efforts to permanently adopt expanded access to telehealth and expand the telehealth workforce. It also ensures adequate and fair telehealth reimbursement and supports telehealth for rural and medically underserved areas.

U.S. Market Trends

In November 2024, the U.S. Drug Enforcement Administration (DEA) and the Department of Health and Human Services (HHS) extended telemedicine capabilities. According to Deloitte, the top trends in U.S. healthcare in 2025 are regulatory changes and transformative technologies under health plans and workforce challenges and core business technologies under health systems. There is an increased focus on developing growth strategies to increase revenue and improve cost efficiency and productivity in U.S. healthcare.

Asia Pacific is expected to grow at the fastest CAGR in the market during the forecast period due to the increased focus on improving healthcare accessibility and affordability. The healthcare sector in the Asia Pacific is driven by clinical data powered by AI, GenAI, and Agentic AI. The other factors include AI-driven workflow automation that offers scaling efficiency and outcomes, and new patient-centric care models from telemedicine to hospital-at-home. The World Health Organization has set its global strategy on digital health for 2020-2025 to promote healthy lives and well-being for the global population.

Europe is expected to grow significantly in the virtual health services market during the forecast period, due to growing chronic diseases. The growing geriatric population and increasing government support are also increasing their adoption rates. Additionally, the expanding digital infrastructure and growing technological innovations are also enhancing the market growth.

UK Virtual Health Services Market Trends

The UK consists of a well-developed healthcare infrastructure, which is actively adopting advanced technology, promoting the use of virtual health services. The growing healthcare investments are also increasing their adoption rates as well as their innovations. The growing shift towards remote healthcare is also increasing their demand.

South America is expected to grow significantly in the virtual health services market during the forecast period, due to expanding digitalization. The growing smartphone penetration is also increasing the use of various virtual health services, where the expanding healthcare is also increasing their use to enhance their accessibility. The growing government initiatives and diseases are also increasing their use, promoting the market growth.

Brazil Virtual Health Services Market Trends

The growing demand for remote care is increasing the use of virtual health services in Brazil. At the same time, the increasing smartphone adoptions are also increasing their use, where the growing government initiatives are encouraging their adoption rates. The companies are also collaborating to develop new virtual health services platforms.

| Companies | Headquarters | Virtual Health Services |

| Teladoc Health | New York, U.S. | Whole person virtual care |

| Amwell | Massachusetts, U.S. | Telehealth platform, offering hybrid care delivery |

| Doctor On Demand | California, U.S. | 24/7 virtual access to board-certified physicians and licensed therapists |

| Babylon Health | London, UK | AI-driven symptom checking and digital-first primary care |

| MDLive | Florida, U.S. | Comprehensive virtual clinics |

| Hims & Hers Health, Inc. | California, U.S. | Multi-specialty telehealth platform |

In January 2025, Ido Schoenberg, M.D., Amwell chair and CEO, proclaimed that the deprivation of the Amwell Psychiatric Care business will enable the company to shift towards its unified and world-class digital care platform. The transaction strengthens the company’s balance sheet while considering the growing accretive software contribution to the company’s product mix.

By Service Type

By Delivery Model/Provider Type

By Technology/Modality

By End User/Patient Segment

By Payer/Reimbursement Model

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar