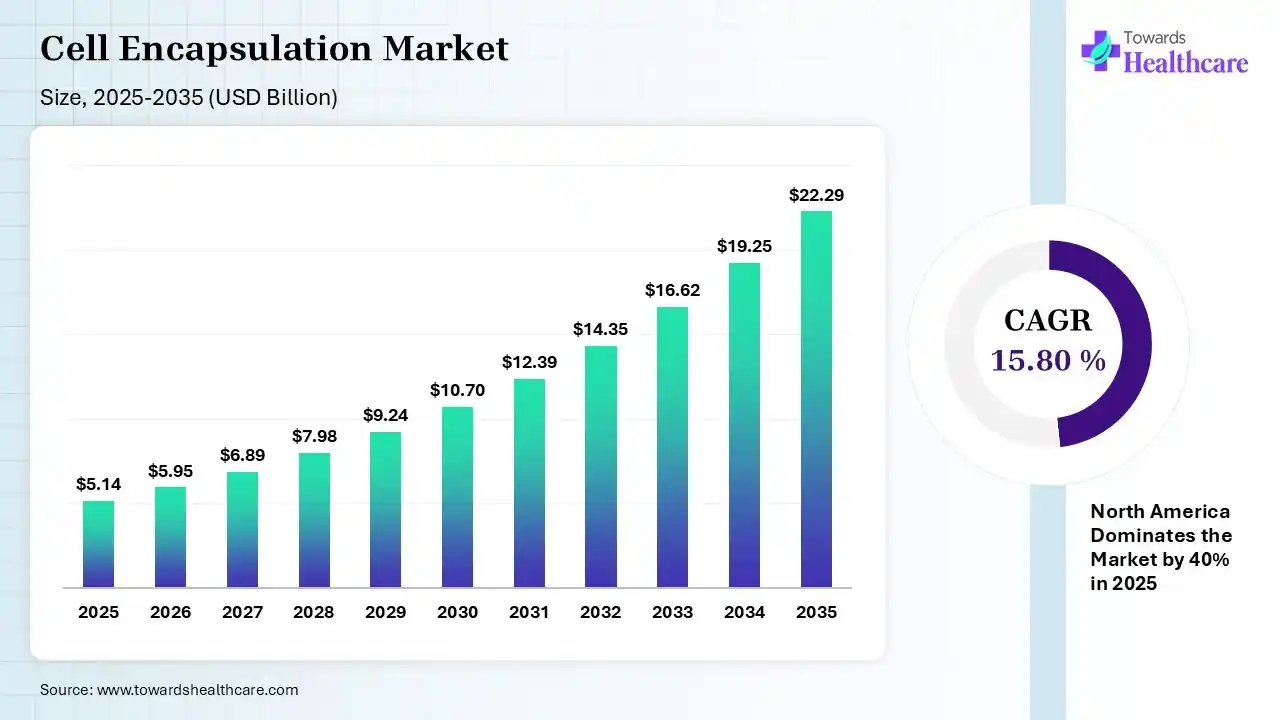

The global cell encapsulation market was estimated at USD 5.14 billion in 2025 and is predicted to increase from USD 5.95 billion in 2026 to approximately USD 22.29 billion by 2035, expanding at a CAGR of 15.80% from 2026 to 2035.

")

The worldwide market for cell encapsulation that focuses on medications and technology is being driven by the increasing demand for innovative treatment alternatives as well as advancements in cellular therapeutics. The necessity for customized medication and the rising prevalence of chronic diseases are two key factors propelling the market's expansion. The use of cell encapsulation technologies is becoming more and more common as researchers and companies search for novel ways to increase the efficacy of cell-based medications. The creation of innovative biomaterials and microencapsulation technologies is gradually gaining more industry attention.

Encased in a semipermeable membrane that protects the cells from mechanical stress and the host immune response, the immobilization of cells that release active therapeutic chemicals is the fundamental idea behind cell encapsulation technology. Based on the promising results of several studies in this field, this method has become a promising treatment option for a number of diseases, such as diabetes, heart failure, anemia, cancer, and central nervous system (CNS) problems. For this last use, the cell encapsulation technology has exceptional benefits since it allows the targeted therapeutic material to be delivered near the affected tissue in a direct, continuous, and permanent manner without crossing the blood-brain barrier (BBB).

As AI and machine learning are being used to predict therapeutic outcomes, enhance encapsulation procedures, and personalize treatments, the field is advancing. More and more applications, particularly in regenerative medicine and drug administration, are combining AI with cell encapsulation technologies to improve accuracy and efficiency. In microfluidic systems used for encapsulation, artificial intelligence (AI) may expedite processes like droplet and cell identification, predict biological activity in artificial cells, and improve material selection.

Shift Toward Commercialization

The market is shifting from research and development projects to approved clinical products, with significant advancements in treating conditions such as Type 1 diabetes. There is a growing emphasis on enhancing manufacturing processes using automated 3D bioreactors and closed systems, which replace manual, open-unit operations to maintain consistency.

Technological Advancements in Manufacturing

Electrostatic dripping is becoming widely adopted because it efficiently produces uniform, high-viability encapsulated cells. The live cell encapsulation market is progressing quickly due to innovations in microfluidics, 3D bioprinting, and automated, high-throughput manufacturing, all aimed at safeguarding therapeutic cells and enhancing their viability.

Driver

Rising Demand for Cell Therapy

These days, traditional treatment methods that depend on the oral intake of medicinal substances are insufficient to address many illnesses. Microencapsulation offers an enticing cell therapy option because of its shown survivability and efficacy, especially for diseases like diabetes where exact metabolite control is necessary. It offers a very practical means of delivering therapeutic elements and molecules that pharmaceutical drugs cannot replace.

Restraint

High Cost of Encapsulation

Encapsulation procedures are expensive, which is one of the factors limiting the cell encapsulation market's growth. Designing microcapsule systems and the associated production processes requires careful consideration of the energy cost of manufacturing microcapsules. Such microencapsulation systems should be created differently in light of recent considerations related to UN sustainability objectives. The goal is to create "ideal" microcapsules that are safe, effective, economical, and ecologically benign.

Opportunity

Live cell encapsulation application creates growth opportunity

Throughout the forecast period, the increasing usage of live cell encapsulation in developing treatment strategies for common chronic ailments, including diabetes, cancer, autoimmune disorders, etc., is also anticipated to help the market's growth. Furthermore, the growing prevalence of diabetes globally is expected to boost demand for live-cell encapsulation in order to create novel treatments, which will fuel market expansion. Therefore, market participants have a tremendous opportunity to provide a new live cell-encapsulated drug for therapy due to the increasing number of instances.

| Table | Scope |

| Market Size in 2026 | USD 5.95 Billion |

| Projected Market Size in 2035 | USD 22.29 Billion |

| CAGR (2026 - 2035) | 15.80% |

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Polymer Type, By Encapsulation Method, By Application, By Technology, By End User |

| Top Key Players | AUSTRIANOVA, Merck KGaA, Sphere Fluidics Ltd., ViaCyte, Inc., Blacktrace Holdings Ltd. (Dolomite Microfluidics), BIO INX, Living Cell Technologies Ltd., Sigilon Therapeutics, Inc., Isogen, Diatranz Otsuka Ltd. |

")

| Segments | Shares % |

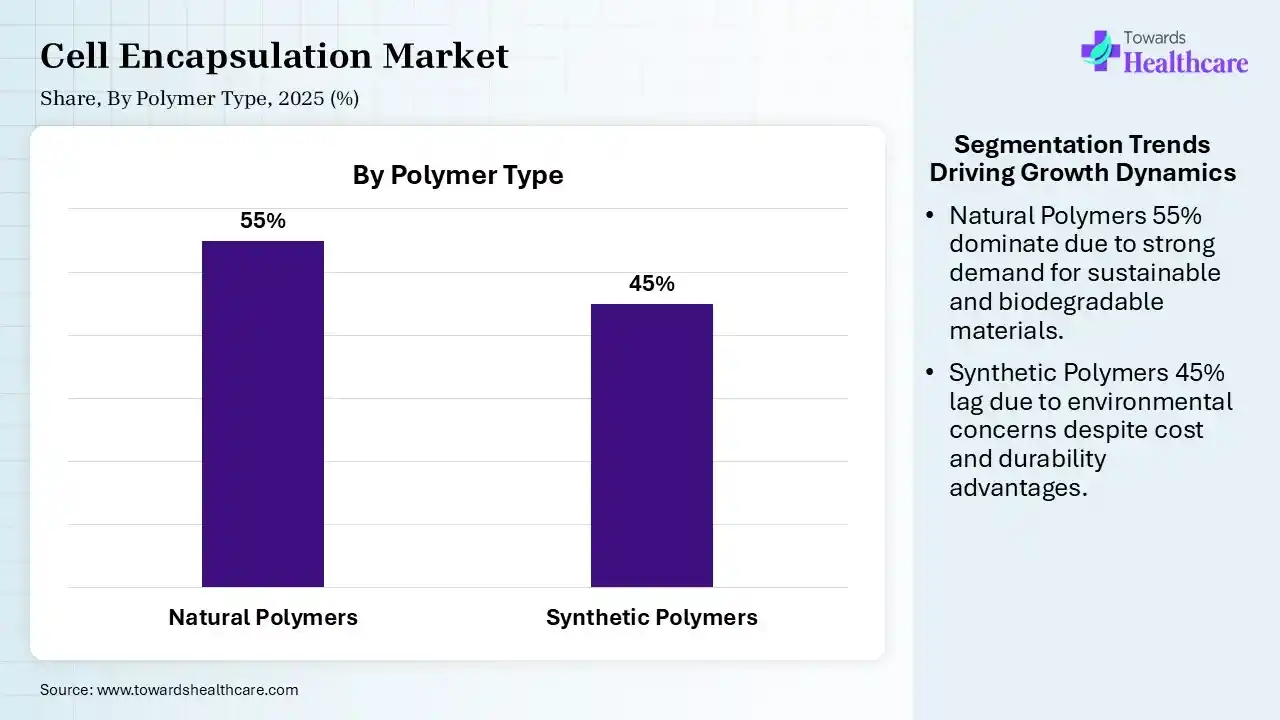

| Natural Polymers | 55% |

| Synthetic Polymers | 45% |

Why is the Natural Polymers Segment Dominant in the Cell Encapsulation Market in 2025?

By polymer type, the natural polymers segment dominated the cell encapsulation market by 55% in 2025. Naturally occurring polymers are the greatest choice for encapsulation. Flexible, biodegradable, low toxicity, biocompatible, and renewable properties are the main criteria used to choose natural polymers, which are high molecular weight macromolecules found in nature since they originated naturally, in microbes, plants, and animals.

By polymer type, the synthetic polymers segment is expected to grow at the fastest CAGR of 15.20% in the cell encapsulation market during the forecast period. Synthetic polymers such as covalently crosslinked PEG and polyacrylates have several advantages, including increased mechanical and chemical stability, enhanced repeatability due to reduced batch-to-batch variance, less nonspecific protein binding, ease of modification, and tunable characteristics. Theoretically, synthetic polymers provide a wider experimental range for deliberate modifications to the particle size, porosity, and membrane thickness.

")

| Segments | Shares % |

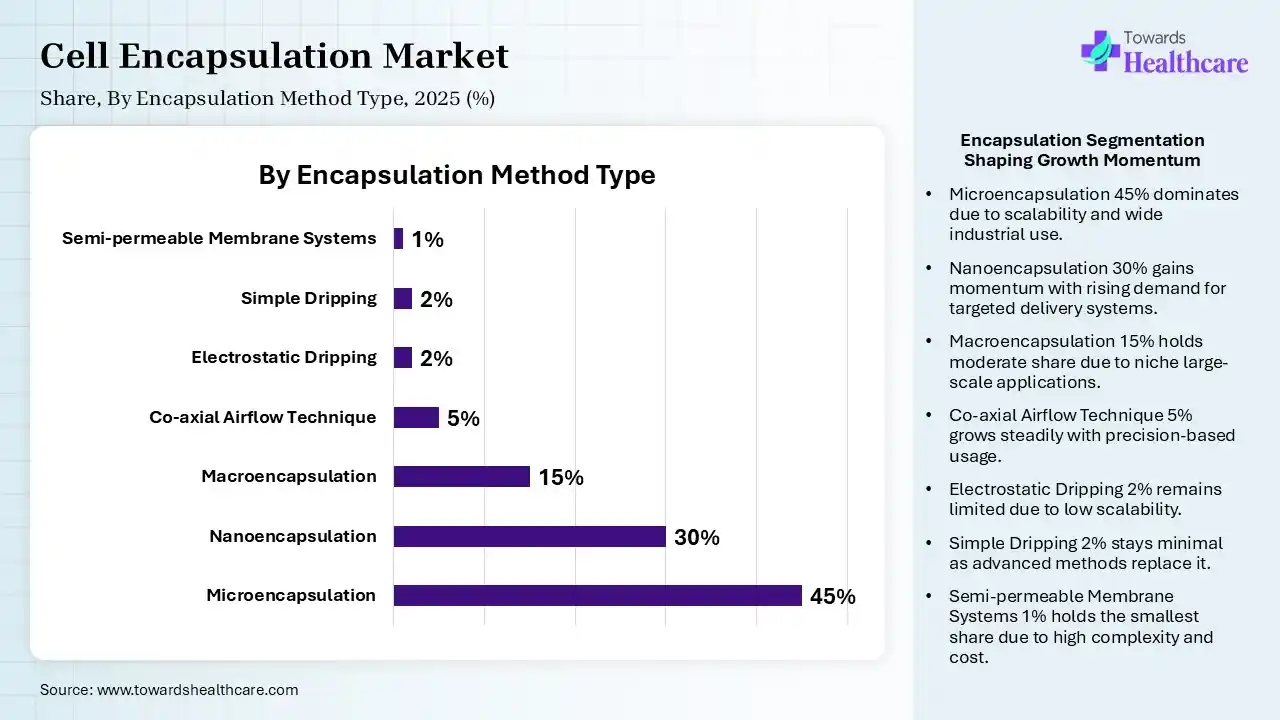

| Microencapsulation | 45% |

| Nanoencapsulation | 30% |

| Macroencapsulation | 15% |

| Co-axial Airflow Technique | 5% |

| Electrostatic Dripping | 2% |

| Simple Dripping | 2% |

| Semi-permeable Membrane Systems | 1% |

Which Encapsulation Method Dominated the Market in 2025?

By encapsulation method, the microencapsulation segment dominated the cell encapsulation market share of 45% in 2025. The process of microencapsulation has shown considerable promise in biotherapeutics and other areas. It has proven useful in immobilizing drugs, live bacterial and mammalian cells, and other biopharmaceutical molecules due to its capacity to provide material structuration, protect the enclosed product, and permit controlled release of the encapsulated contents, all of which can ensure safe and effective therapeutic effects.

By encapsulation method, the nanoencapsulation segment is expected to grow at the fastest CAGR of 18% in the cell encapsulation market during the forecast period. The recently developed technique that has the potential to entrap bioactive substances is nanoencapsulation. Because of their subcellular size, regulated and sustained release characteristics, and biocompatibility with tissue and cells, nanoencapsulation demonstrates site-specific targeted drug delivery and effective absorption via cells.

")

| Segments | Shares % |

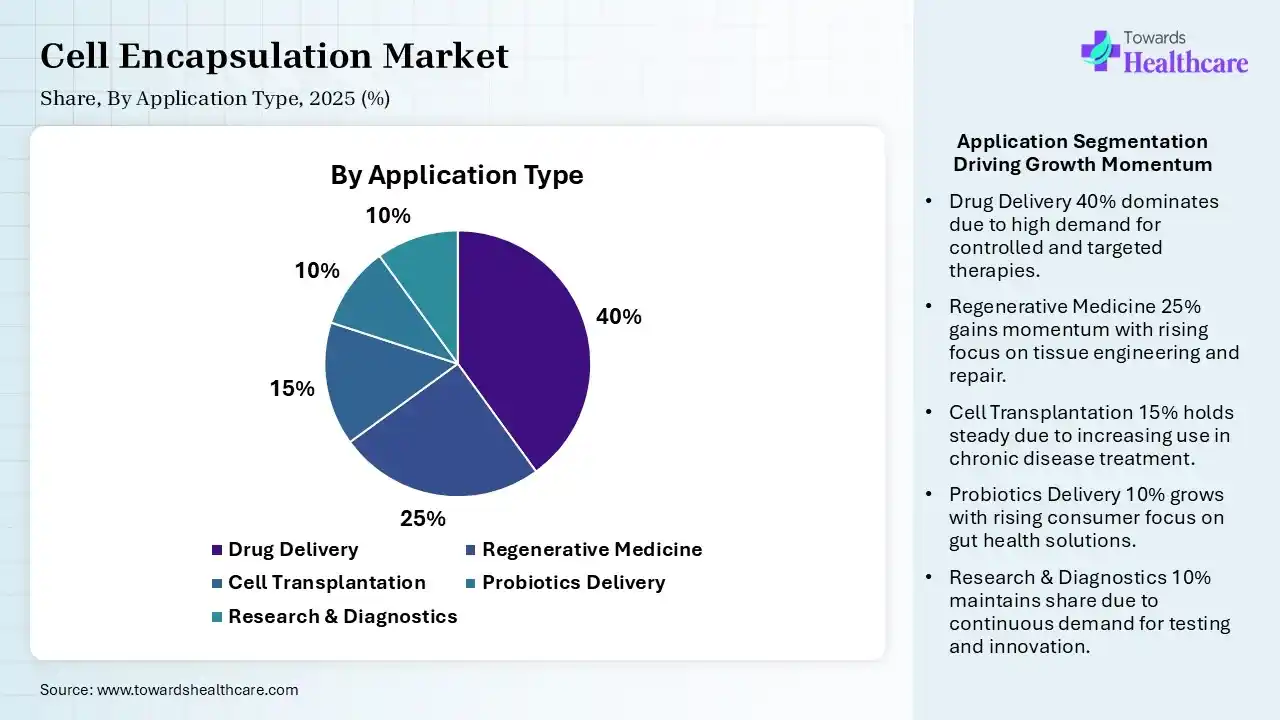

| Drug Delivery | 40% |

| Regenerative Medicine | 25% |

| Cell Transplantation | 15% |

| Probiotics Delivery | 10% |

| Research & Diagnostics | 10% |

Why is the Drug Delivery Segment Dominating the Cell Encapsulation Market?

By application, the drug delivery segment dominated the cell encapsulation market by share of 40% in 2025. For medications that are aggressive, fragile, or poorly soluble, encapsulation is an essential tactic that can increase therapeutic impact while reducing adverse effects. Since many medications have unique and varied characteristics, a wide variety of biopolymers and synthetic polymers are employed to encapsulate them. Drug encapsulation for anti-cancer treatments and nanoparticles has garnered a lot of attention in the past ten years.

By application, the regenerative medicine segment is expected to grow at the fastest CAGR of 15.20% in the cell encapsulation market during the forecast period. Research in regenerative medicine is expanding rapidly to address this emerging demand. In tissue engineering applications, cell encapsulation might be utilized to combat transplant rejection. Encapsulation of cells may lessen the requirement for long-term immunosuppressive drugs to control side effects after an organ transplant.

")

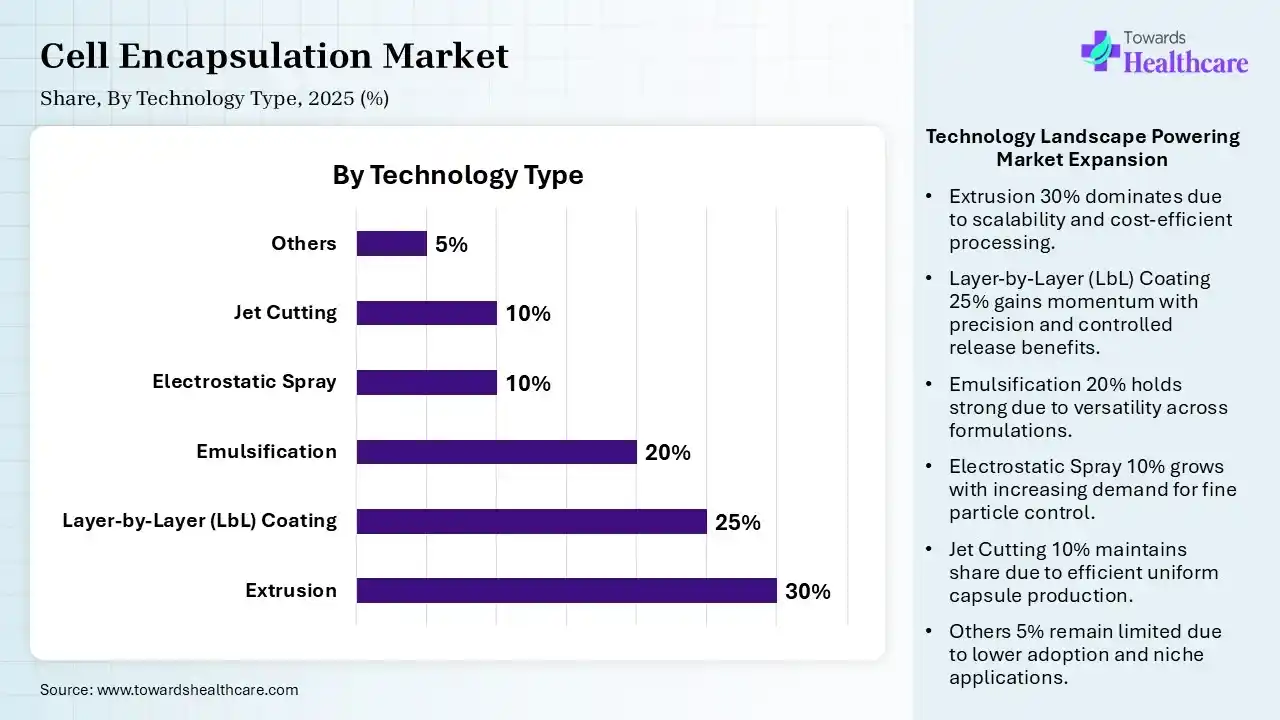

| Segments | Shares % |

| Extrusion | 30% |

| Layer-by-Layer (LbL) Coating | 25% |

| Emulsification | 20% |

| Electrostatic Spray | 10% |

| Jet Cutting | 10% |

| Others | 5% |

By technology, the extrusion segment dominated the cell encapsulation market with share of 30% in 2025. Cells are encapsulated by the physical process of extrusion, which uses hydrocolloids. Extrusion is a simple, inexpensive method that uses a sensitive procedure to create high cell viability without damaging cells. The technique doesn't require hazardous chemicals and may be applied in both aerobic and anaerobic settings.

By technology, the layer-by-layer (LbL) coating segment is expected to grow at the fastest CAGR of 16% in the cell encapsulation market during the forecast period. In cellular function engineering, layer-by-layer (LbL) encapsulation of cells with different polyelectrolytes has gained popularity. The LbL assembly method has been shown to be a straightforward, affordable, durable, flexible, and extremely adaptable bottom-up surface engineering technique for conformally coating a variety of surface types—from live cells to metallic implants; under moderate circumstances.

")

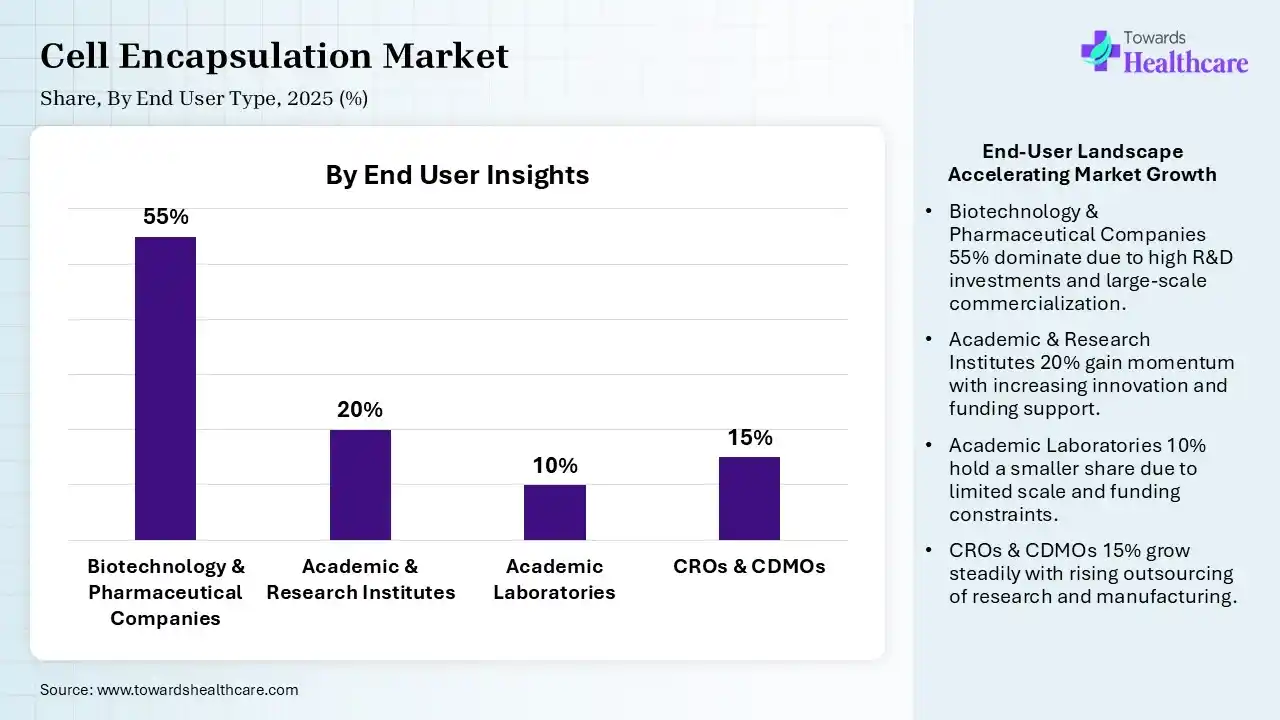

| Segments | Shares % |

| Biotechnology & Pharmaceutical Companies | 55% |

| Academic & Research Institutes | 20% |

| Academic Laboratories | 10% |

| CROs & CDMOs | 15% |

By end-user, the biotechnology & pharmaceutical companies segment dominated the cell encapsulation market with the share of 55% in 2025. Both drug delivery and regenerative medicine depend on pharmaceutical biotechnology, which employs state-of-the-art technologies to enhance drug efficacy and promote tissue regeneration. Drug delivery focuses on improving pharmaceutical properties, including bioavailability and targeted distribution, whereas regenerative medicine combines biomaterials and stem cells with advanced drug delivery methods to support tissue regeneration and repair.

By end-user, the academic & research institutes segment is expected to grow at the fastest CAGR of 14% in the cell encapsulation market during the forecast period. The process of cell encapsulation is essential for drug delivery systems, tissue engineering, and cell-based therapeutics. Through basic research, material development, and clinical translation, academic institutions and research are essential to the advancement of cell encapsulation technology.

")

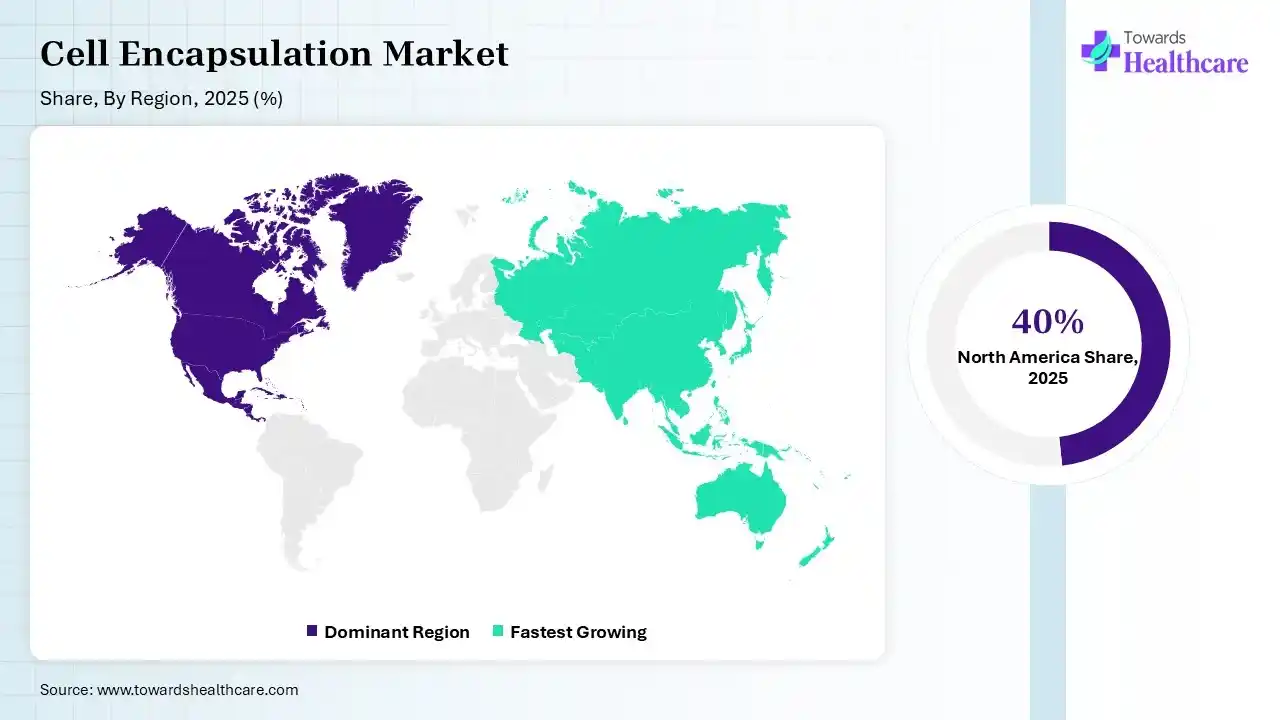

North America dominated the cell encapsulation market with share of 40% in 2025. A significant amount of development may be ascribed to favorable laws, more government help, and backing for private companies. The majority of the area's concentration is on drug discovery research, which drives business expansion. The presence of inventors and important industry players has increased the items' market share in the region. Industry players have a fantastic chance to produce innovative medicines using live cell encapsulation techniques because of increased research and development, as well as significant expenditures.

The U.S. Cell Encapsulation Market Trends

The promise of developing therapeutic solutions that repair organ, tissue, and cell functioning impacted by age, illness, or injury is presented by regenerative medicine technology. Someday, regenerative medicine could help the roughly 104,000 people in the U.S. who are waiting for an organ transplant, since there are significantly more people on the waiting list than there are available.

The Canada Cell Encapsulation Market Trends

In June 2025, the Stem Cell Network (SCN) announced a $13.5 million investment in 36 new clinical trials and research projects in regenerative medicine. With the help of 63 partner organizations that have provided more than $19.5 million in matching cash and in-kind support, this initiative has added $33 million to Canada's regenerative medicine ecosystem. The funded projects will advance creative research in 14 disease categories, including rare disorders like Rett syndrome and cystic fibrosis.

Asia Pacific is estimated to host the fastest-growing cell encapsulation market with share of 20% during the forecast period. The rapid ascent may be explained by advancements in the pharmaceutical and biotechnology industries of developing countries like China and India. Another element influencing the prosperous development of this region is the continuous government assistance provided to the pharmaceutical sectors in emerging countries. Furthermore, the region's sector is anticipated to grow greatly as a result of continuous research on cancer and infectious diseases.

The China Cell Encapsulation Market Trends

The number of stem cell clinical trials now underway in China demonstrates the country's rapid entry into the field. China now has the third-highest number of stem cell clinical trials worldwide, after the U.S. and Europe, with 164, according to the US National Institutes of Health. In terms of scientific production, China is likewise catching up quickly.

The India Cell Encapsulation Market Trends

Despite being a relatively new field in India, regenerative medicine is rapidly gaining popularity due to rising awareness and investment in healthcare innovation. The Indian government has launched a number of initiatives to promote innovation and entrepreneurship in the healthcare sector, including regenerative medicine. Advancells, Cryoviva Biotech, and Stempeutics Research are some of the leading companies in the Indian regenerative medicine market.

Europe is expected to grow significantly in the cell encapsulation market by 30% share during the forecast period. Growing funding for cell therapy and regenerative medicine research is driving the demand for encapsulation technologies. Additionally, the desire for more sophisticated treatment options as a result of the rising prevalence of chronic illnesses is driving the use of encapsulation methods for cell-based therapies. In Europe, financing programs and regulatory frameworks promote innovation and market growth. Collaborations among academic institutions, research teams, and industry players also promote technical innovation and commercial expansion.

The Germany Cell Encapsulation Market Trends

Germany is at the vanguard of a number of academic-industry partnerships that help move medications from laboratory to clinical settings, in addition to spearheading technological improvements. The ethical discussion around the use of stem cells is likewise becoming more heated in Germany. Experts are dedicated to upholding moral standards and furthering science in a regulated environment for stem cell research. Germany is at the forefront of the development and use of stem cell therapies.

The UK Cell Encapsulation Market Trends

Researchers in the UK have been working on regenerative medicine since its start, and it is one of the most exciting and promising areas of study. UK has the world's second-largest regenerative medicine ecosystem, with over 400 companies involved in the field. In the European market for advanced therapeutic medicines, about one in three small and medium-sized businesses (SMEs) are based in the United Kingdom.

| Company | Key Offerings |

| AUSTRIANOVA | Austrianova focuses on proprietary, GMP-grade technologies for live cell encapsulation, mainly using cellulose sulphate to safeguard, store, and deliver mammalian (Cell-in-a-Box®) and bacterial/yeast (Bac-in-a-Box®) cells. |

| Merck KGaA | Merck KGaA is a significant player in the sector, concentrating on supplying high-purity materials like alginate and chitosan for both micro- and macroencapsulation. They enhance cell therapy and drug delivery with their biopolymer knowledge. |

| Sphere Fluidics Ltd. | Sphere Fluidics, now known as Sphere Bio, is an important entity in the field. Their primary products are the Cyto-Mine® and Cyto-Mine Chroma platforms, which automate the encapsulation, screening, and sorting of millions of cells daily to speed up biologics discovery and cell therapy progress. |

| ViaCyte, Inc. | ViaCyte, Inc. is a prominent regenerative medicine firm in the industry. Their key products include PEC-01 (pancreatic progenitor cells) paired with specialized encapsulation devices like PEC-Direct and PEC-Encap. |

| Living Cell Technologies Ltd. | Living Cell Technologies Ltd. (LCT) offers products aimed at treating diabetes and neurodegenerative diseases by encapsulating cells to shield them from the host immune system while permitting the release of therapeutic factors. |

In March 2025, our CSS technology has already been utilized to encapsulate 20 distinct cell types, along with a wide variety of other biologics and small chemicals, according to Lisa Stehno-Bittel, president and co-founder of Likarda. In addition to having the potential to significantly enhance public health worldwide, this funding allows us to showcase the range of our technology and how it can help people with a wide range of illnesses in a number of settings.

Strengths

Weaknesses

Opportunities

Threats

By Polymer Type

By Encapsulation Method

By Application

By Technology

By End User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar