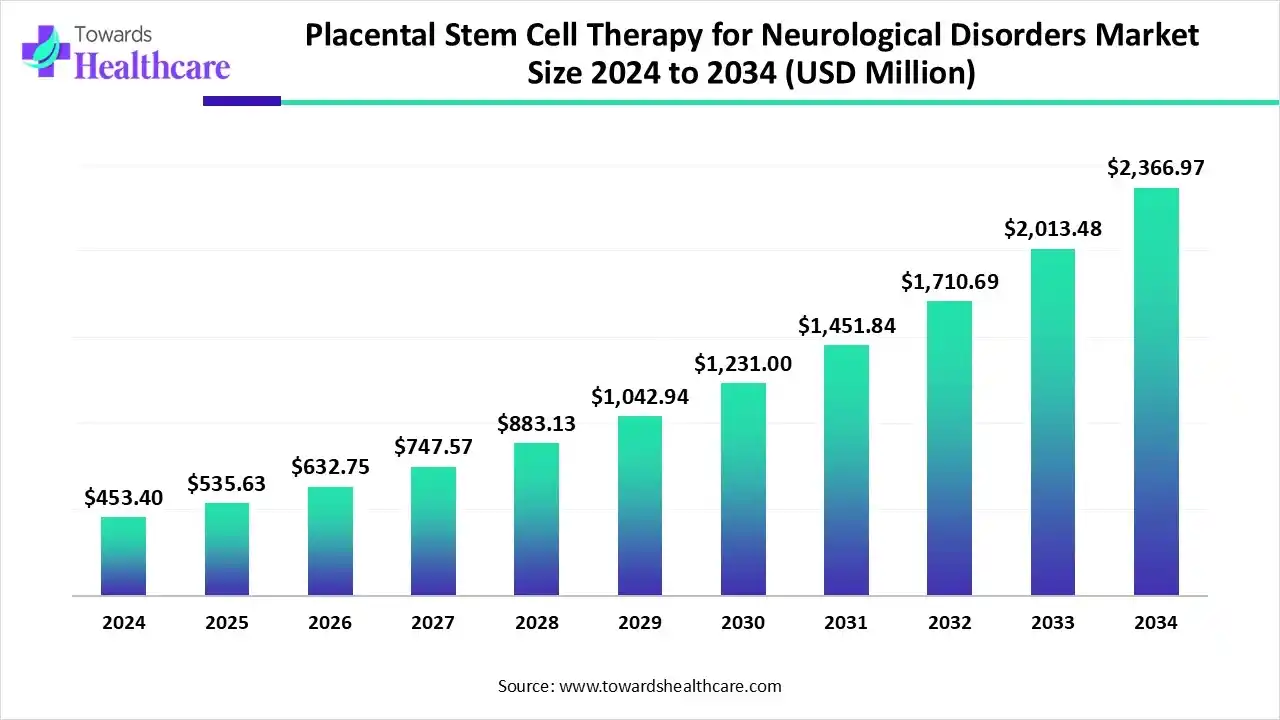

The global placental stem cell therapy for neurological disorders market size is calculated at US$ 535.65 million in 2025, grew to US$ 632.81 million in 2026, and is projected to reach around US$ 2836.93 million by 2035. The market is expanding at a CAGR of 18.14% between 2026 and 2035.

")

The placental stem cell therapy for neurological disorders market is rising as a result of the increasing prevalence of neurological disorders and the limitations of conventional therapies. Technological advancements such as improved techniques for cell isolation, proliferation, and differentiation are increasing the efficacy of therapies. Personalised medicine approaches that adapt treatments to each patient's requirements are gaining traction. The regulatory landscape continues to evolve as efforts are made to speed up approval processes without compromising patient safety.

The market is driven by increasing prevalence of neurological disorders, advances in regenerative medicine, and growing research on stem cell therapies’ efficacy and safety. The placental stem cell therapy for neurological disorders market involves the use of stem cells derived from human placenta for the treatment of neurological diseases, including Parkinson’s disease, Alzheimer’s disease, stroke, and spinal cord injuries. Placental stem cells are rich in mesenchymal and hematopoietic progenitors, offering regenerative, anti-inflammatory, and neuroprotective properties.

Key applications include neuronal regeneration, functional recovery, and neuroinflammation reduction. End-users include hospitals, research institutions, and biopharmaceutical companies. Market growth is fueled by clinical trials, regulatory approvals, and partnerships between biotechnology firms and academic centers globally across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Growing Neurological Disorders

There is a rise in the incidence of various neurological conditions, such as Parkinson’s, ALS, and stroke, which are increasing the demand and use of placental stem cell therapies, creating new opportunities for regenerative therapies.

Flourishing Regenerative Medicine

The growing advances in regenerative medicine for the treatment of neurological disorders are driving new opportunities for the development of cell proliferation, isolation, personalized therapy methods, and delivery systems.

Increasing R&D Activities

The companies are actively developing a wide range of placental stem cell therapies for the treatment of growing neurological disorders, where they are currently focusing on enhancing their applications for other therapeutic areas like autoimmune and musculoskeletal conditions.

Technological Advancements

The growing technological innovations are leading to their integration with stem cell selection, treatment optimization, and quality control to accelerate the placental stem cell therapies development, improve operational efficacy, and enhance treatment outcomes.

AI has great potential in transforming the placental stem cell therapy for neurological disorders market. To increase stem cell therapy's efficacy and efficiency in areas like cell selection, quality control, and delivery optimisation, artificial intelligence (AI) is being incorporated into the process. AI algorithms examine intricate data to assist in predicting therapeutic results, monitoring and regulating cell growth conditions, and choosing the best stem cells for a patient. Through improved research and the potential for more effective and individualised treatments for a range of illnesses, this combination advances regenerative medicine.

| Neurological Domain | Key 2024–2025 Data | Leading Companies (2024–2025) | Headquarters |

| All Neurological Disorders |

|

|

|

| Alzheimer’s & Dementia |

|

|

|

| Parkinson’s & Movement Disorders |

|

|

|

| Epilepsy |

|

| Table | Scope |

| Market Size in 2026 | USD 632.81 Million |

| Projected Market Size in 2035 | USD 2836.93 Million |

| CAGR (2026 - 2035) | 18.14% |

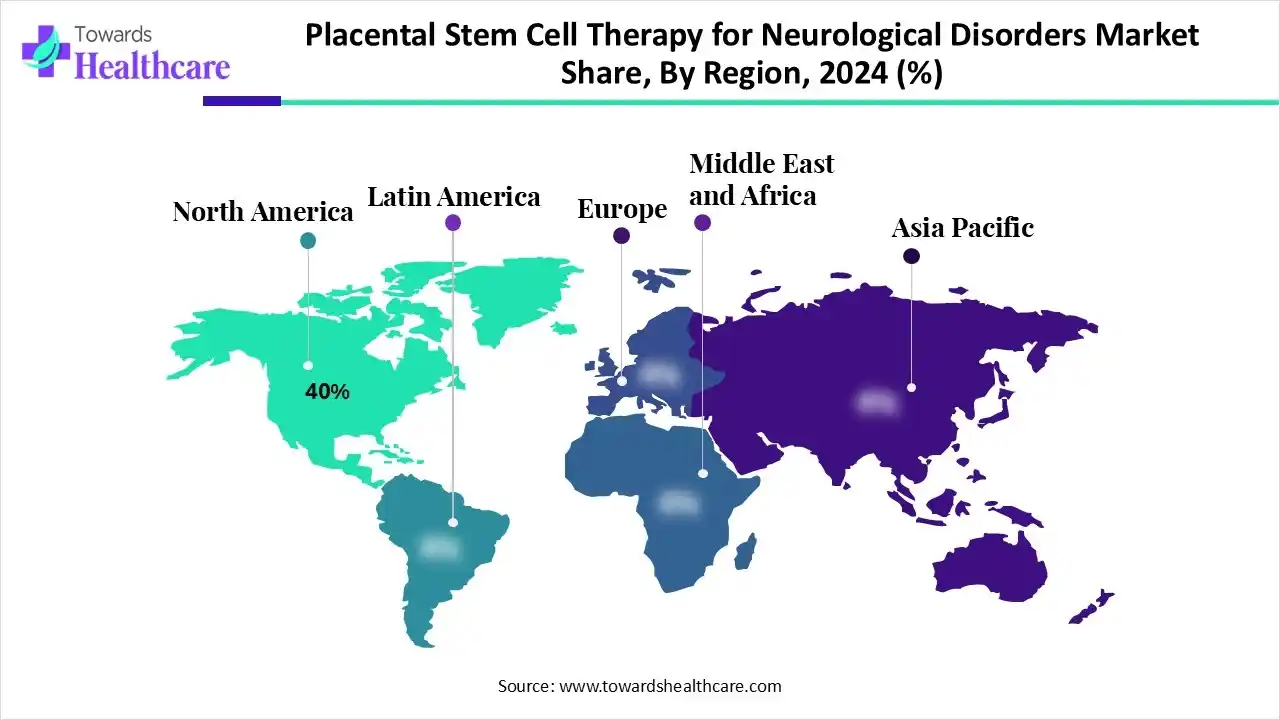

| Leading Region | North America by 40% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Cell Type/Lineage, By Application, By Product & Services, By Therapy Type, By End-User, By Region |

| Top Key Players | Pluristem Therapeutics, Celularity Inc., Medipost Co., Ltd., Stempeutics Research Pvt. Ltd., Osiris Therapeutics, Gamida Cell Ltd., Anterogen Co., Ltd., Neuroplast AS, AxoGen, Inc., FamiCord Group, Cytonet GmbH, ReNeuron Group Plc, BrainStorm Cell Therapeutics, Takeda Pharmaceutical Company, Lonza Group, BioTime Inc., Cytori Therapeutics, Celltex Therapeutics, Mesoblast Ltd., Evox Therapeutics |

")

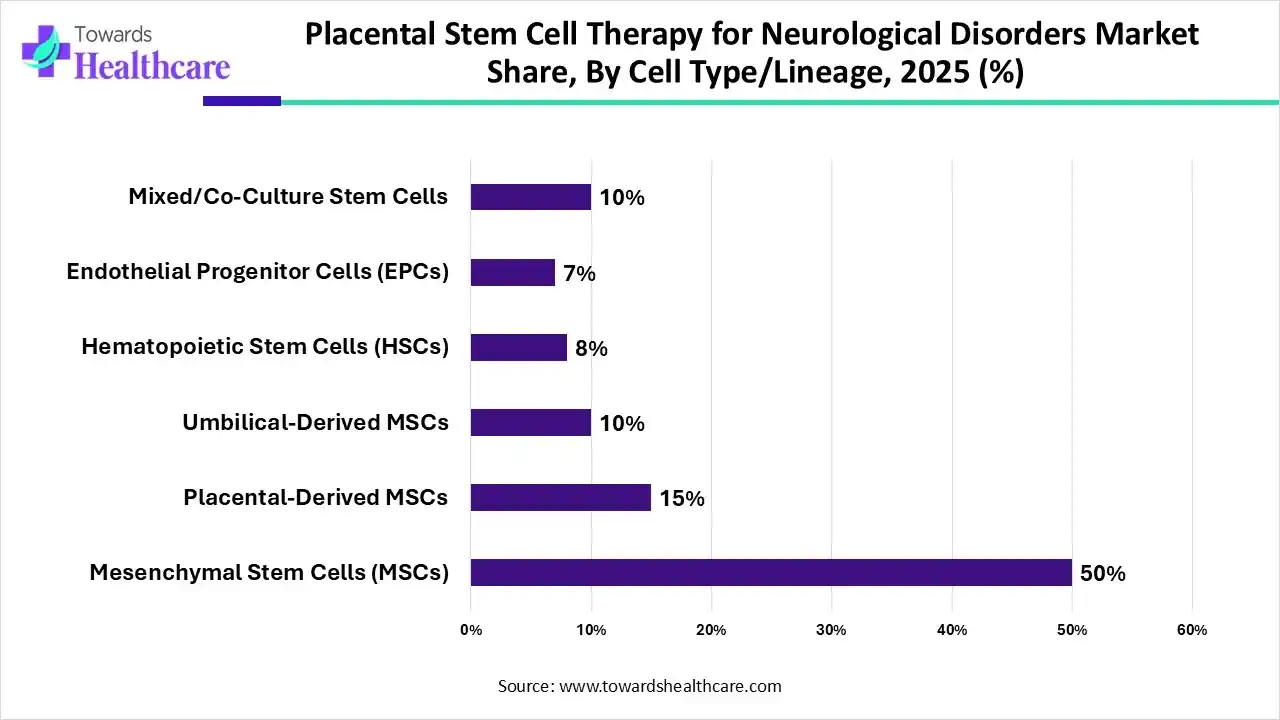

Which Cell Type/ Lineage Segment Dominated the Market in 2025?

By cell type/lineage, the mesenchymal stem cells (MSCs) segment held the largest share of the placental stem cell therapy for neurological disorders market in 2025, with a revenue of approximately 50%. Mesenchymal stem cells (MSCs) are one of the most sought-after cell sources due to their special qualities. The modulatory characteristics of MSCs as well as their engineering, labelling, and delivery strategies to the brain have been thoroughly investigated by researchers.

By cell type/lineage, the mixed/co-culture stem cells segment is anticipated to grow at the fastest CAGR during the forecast period. By simulating the intricate cellular interactions present in the brain, mixed or co-cultured stem cells are used to study neurological disorders. This enables researchers to look into the mechanisms underlying disease and screen medications. Compared to single-cell cultures, these systems offer a more physiologically accurate environment by frequently combining stem cell-derived neurones with other cell types such as astrocytes or oligodendrocytes.

| Segments | Shares 2025 % |

| Parkinson’s Disease | 30% |

| Alzheimer’s Disease | 12% |

| Stroke & Ischemic Injury | 10% |

| Acute Phase Therapy | 5% |

| Chronic Phase Therapy | 5% |

| Spinal Cord Injury | 6% |

| Multiple Sclerosis | 8% |

| Others | 24% |

Why was the Parkinson’s Disease Segment Dominant in the Market in 2025?

By application, the Parkinson’s disease segment held the largest share of the placental stem cell therapy for neurological disorders market in 2025, with a revenue of approximately 30%. Parkinson's disease (PD), the second most common neurodegenerative disease in 2024, affects more than 8.5 million people globally. As people age, the prevalence of Parkinson's disease (PD) increases significantly, especially in those over 60. Males are more likely than females to be affected by this neurological condition, which is believed to have the fastest rate of growth. According to a recent study, the global pooled prevalence was 1.51 cases per 1000 people, with rates higher in men and increasing with age and wealthier countries.

By application, the stroke & ischemic injury segment is eanticipated to grow at the fastest CAGR during the forecast period. The chance of stroke fatality is high. Around the world, 15 million people get a stroke every year. Five million of them pass away, and a further five million become chronically crippled, burdening families and communities.

Which Product & Service Segment Dominated the Market in 2025?

By product & service, the placental stem cell products segment held the largest share of the placental stem cell therapy for neurological disorders market in 2025, with a revenue of approximately 45%. Products of placental stem cells, such as placental mesenchymal stem cells (PMSCs), are being researched for neurological conditions like stroke, multiple sclerosis, and Parkinson's disease (PD). These stem cells' immunomodulatory and regenerative qualities make them promising.

By product & service, the cell delivery systems segment is anticipated to grow at the fastest CAGR during the forecast period. Techniques for delivering and maintaining therapeutic cells, including placental stem cells, to specific organs are known as cell delivery systems. In order to get across the blood-brain barrier and guarantee that cells reach the central nervous system (CNS), physicians employ a variety of delivery methods when treating neurological illnesses.

What Made the Allogeneic Therapy Segment Dominant in the Market in 2025?

By therapy type, the allogeneic therapy segment held the largest share of the placental stem cell therapy for neurological disorders market in 2025, with a revenue of approximately 55%. "Off-the-shelf" supply methods are crucial in emergency medical circumstances, and allogeneic solutions are especially well-suited for them. Utilising the cells of donors, these treatments enable preservation and instant access for the treatment of several patients. Time and resources can be saved as a result of avoiding the need for customised cell retrieval and preparation. Better scalability than autologous treatments is another benefit of allogeneic stem cell therapies, which might reduce patient and manufacturer costs while also improving accessibility.

By therapy type, the autologous therapy segment is anticipated to grow at the fastest CAGR during the forecast period. Includes uses in immuno-oncology and regenerative medicine. Using a patient's cells or tissues, this cutting-edge medical technique treats a variety of illnesses. Reducing the chance of immunological rejection and encouraging long-term recovery are two important benefits of autologous techniques.

Which End-User Segment Dominated the Market in 2025?

By end-user, the hospitals & specialty clinics segment held the largest share of the placental stem cell therapy for neurological disorders market in 2025, with a revenue of approximately 40%. Many clinics and hospitals, such Medanta and NeuroGen Brain and Spine Institute, specialise in employing autologous adult stem cells instead of placental ones for the treatment of neurological illnesses. Swiss Medica is a prominent worldwide choice, while Fortis, Apollo Hospital, and Cryoviva Biotech India are additional suppliers in India.

By end-user, the biopharmaceutical companies segment is anticipated to grow at the fastest CAGR during the forecast period. Most biomedical innovation is created by emerging biopharma (EBP) firms, many of which have never put a treatment on the market. These businesses eventually either successfully launch their goods onto the market or, more frequently, someone else buys their assets or entire businesses. The success of early-stage drug research is largely due to these EBP businesses.

")

North America dominated the placental stem cell therapy for neurological disorders market share by 40% in 2025. The demand for placental stem cell therapies has increased in North America due to growing knowledge of these treatments' potential advantages. The active search for alternative therapies by patients with neurological illnesses is fueling the market's expansion. Advances and accessibility have been fostered by partnerships among academic institutions, healthcare providers, and biotechnology businesses that have resulted in the establishment of specialised facilities for placental stem cell treatment in neurological illnesses.

What are the U.S. Market Trends?

By 2050, it is anticipated that 13 million Americans 65 and older will have Alzheimer's, up from an estimated 7.2 million in 2025. Nearly 12 million Americans unpaidly cared for individuals suffering from dementia in 2024. Nearly a million Americans suffer from Parkinson's disease, and the likelihood of developing the illness rises sharply with age. Other neurological conditions are not included in the data for 2024.

Rising Investment is Driving Canada

According to a May 2024 statement from the Government of Canada, up to one in three Canadians may have a neurological condition at some point in their lives. The expected number of dementia patients in Canada as of January 1, 2025, is 771,939.

In July 2025, the Canadian government, through the Canadian Institutes of Health Research (CIHR), has awarded $39.4 million to promote dementia and healthy ageing research. The funding comes from the CIHR Research Initiative on Brain Health and Cognitive Impairment in Ageing. The investment totals $44.8 million after an extra $5.4 million is contributed.

Asia Pacific is estimated to host the fastest-growing placental stem cell therapy for neurological disorders market during the forecast period. Major participants include China, India, and Japan, who are investing more in stem cell research and healthcare. The growing incidence of chronic illnesses and an ageing population are driving the need for stem cell therapies. Furthermore, a lot of Asia-Pacific nations are developing into clinical trial centres because of their sizable patient bases and reasonably priced medical care. The stem cell treatment market in Asia-Pacific is expected to develop significantly as awareness and healthcare infrastructure improve.

Europe is expected to grow significantly in the placental stem cell therapy for neurological disorders market during the forecast period, due to growing R&D activities. The presence of stringent regulation and an advanced healthcare system is also increasing the adoption of the placental stem cell therapies. The increasing investment and growing neurological disorders are also promoting the market growth.

UK Market Trends

The presence of well-developed healthcare infrastructure in the UK is increasing the adoption of placental stem cell therapies for the treatment of growing neurological disorders. The growing collaboration, R&D investment, and government funding are also increasing the development of new regenerative therapies for their effective treatment.

MEA is expected to grow significantly in the placental stem cell therapy for neurological disorders market during the forecast period, due to expanding industries, which are increasing the R&D activities focused on stem cell therapies. The growing healthcare investments, expanding healthcare, increasing neurological disorders, blooming medical tourism, and growing health awareness are also enhancing the market growth.

Saudi Arabia Market Trends

The growing government initiatives in Saudi Arabia are expanding the R&D activities focused on the development of regenerative medicines for the effective treatment of neurological disorders. The growing collaborations and manufacturing capacities are also increasing the innovations and adoption of the placental stem cell therapies for growing neurological disorders.

From initial discovery to human clinical trials, the development of placental stem cell therapies for neurological disorders proceeds through a multi-stage research and development (R&D) pipeline. Preclinical research, clinical trials, and cell sourcing and characteriszation are important phases.

Key companies include: Pluri Inc., Mesoblast Ltd., BrainStorm Cell Therapeutics, and Cynata Therapeutics.

A national regulatory agency, like the U.S. Food and Drug Administration (FDA), must supervise a multi-phase clinical trial process and conduct thorough preclinical research before placental stem cell therapy for neurological disorders can be approved an launched in the placental stem cell therapy for neurological disorders market.

Key companies include: Pluri Inc., Mesoblast Ltd., BrainStorm Cell Therapeutics, and Cynata Therapeutics.

From the first consultation through long-term follow-up care, a placental stem cell therapy programme for neurological disorders offers complete patient support and services. In order to promote recovery, the procedure places a strong emphasis on thorough patient qualification, thorough treatment planning, and continuous rehabilitation.

In August 2025, after a successful clinical study, Japanese pharmaceutical company Sumitomo Pharma said that it is requesting permission for a therapy for Parkinson's disease that involves transferring stem cells into a patient's brain. The company's therapy, which used induced pluripotent stem (iPS) cells, which can turn into any cell in the body, was safe and effective in reducing symptoms, according to a trial conducted by researchers from Kyoto University.

In August 2024, in order to meet the production needs of "medicinal products" in the ATMP category, Cryoviva Ltd., a stem cell bank with a cell expansion facility in its network, opens a "World Class" laboratory that triples in size from its initial facility size. It complies with GMP/PICS standards and can produce up to 500 billion cells annually.

By Cell Type/Lineage

By Application

By Product & Services

By Therapy Type

By End-User

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar