Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

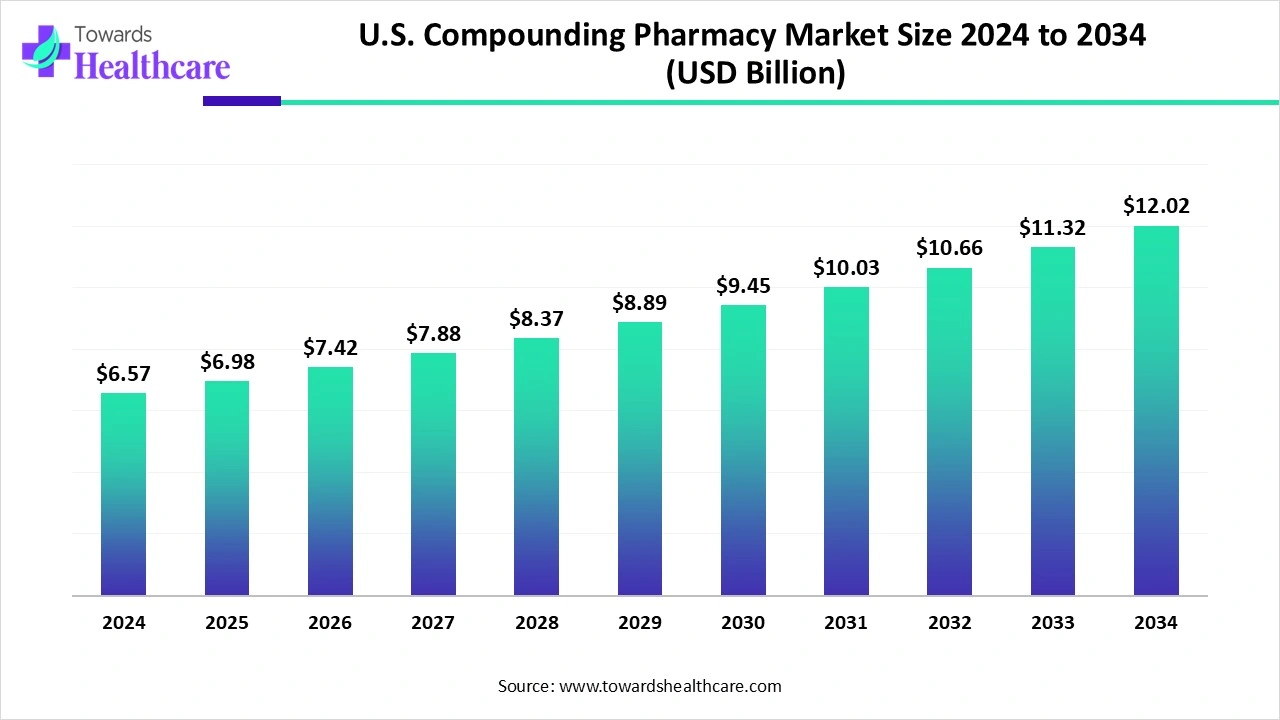

The U.S. compounding pharmacy market size in 2025 was US$ 6.98 billion, expected to grow to US$ 7.42 billion in 2026 and further to US$ 12.79 billion by 2035, backed by a robust CAGR of 6.24% between 2026 and 2035.

")

The U.S. compounding pharmacy market is expanding due to growing demand for personalized medications tailored to individual patient needs, including unique dosages, allergen-free formulations, and alternative delivery methods. Factors driving growth include the rising prevalence of chronic diseases, an aging population, and ongoing drug shortages, which increase reliance on compounded alternatives. Technological advancements in drug formulation and automation, along with regulatory support under the Drug Quality and Security Act, further enhance market efficiency. Patient-centered care approaches continue to boost market adoption.

A compounding pharmacy is a specialized type of pharmacy that prepares customized medications to meet the unique needs of individual patients, rather than providing standard, mass-produced drugs. These pharmacies create formulations tailored to dosage, strength, flavor, or delivery method, making medications more suitable for patients who cannot use commercially available products, such as children, the elderly, or those with allergies. Compounding pharmacies can produce creams, gels, capsules, liquids, or injectables, often combining multiple active ingredients into a single medication. They play a critical role during drug shortages, offering alternatives when standard drugs are unavailable. Regulated under the Drug Quality and Security Act, compounding pharmacies ensure safety, quality, and precision while supporting patient-centered care and personalized medicine approaches.

Investment and Funding Initiatives

Investment and funding initiatives are pivotal in propelling the growth of the market by enhancing operational capabilities, expanding service offerings, and fostering innovation. In 2025, notable developments underscore this trend:

Adoption of Inorganic Growth Strategies

Adopting inorganic growth strategies, such as mergers and acquisitions, has significantly propelled the U.S. compounding pharmacy market by enhancing service capabilities, expanding geographic reach, and integrating advanced technologies. These strategies enable companies to quickly scale operations, diversify service offerings, and access new patient populations, thereby accelerating market growth.

In January 2025, Revelation Pharma, a leading national network of 503A and 503B compounding pharmacies, acquired Cascade Specialty Pharmacy, a Washington-based provider specializing in ENT and animal health compounding. This acquisition not only expanded Revelation's service portfolio but also strengthened its nationwide presence, allowing for enhanced patient care and broader access to specialized compounded medications.

The U.S. compounding pharmacy market comprises pharmacies that prepare customised medications tailored to individual patients requirements when commercially available drugs are unsuitable because of dosage, formulation, ingredient sensitivities, or supply shortages. The market is expanding as demand for personalised medicine increases alongside the rising prevalence of chronic diseases and an aging population requiring specialised therapies. Growing drug shortages are encouraging healthcare providers to rely on compounding medications for uninterrupted patient care.

Technological advancements, including automated compounding systems, sterile manufacturing technologies, and digital prescription management, are improving accuracy, efficiency, and product quality. A key trend is the increasing adoption of 503B outsourcing facilities that supply hospitals with ready-to-use sterile compounded medications. Future opportunities lie in precision medicine, biologics-compatible compounding, pediatric and geriatric formulations, veterinary compounding, and integration of AI-driven quality assurance and workflow optimisation.

The U.S. compounding pharmacy market is influenced by a combination of internal capabilities and external healthcare trends. Internally, advances in sterile compounding technologies, automation, digital quality management systems, skilled pharmacists, and expanding 503B outsourcing facilities enhance efficiency, product quality, and production capacity. However, high operating costs, stringent quality standards, and workforce shortages remain key challenges. Externally, the market is driven by rising demand for personalised medicine, increasing chronic disease prevalence, an ageing population, and persistent drug shortages that require customised therapies. In addition, evolving FDA regulations, USP compliance requirements, active pharmaceutical ingredient (API) supply chain fluctuations, reimbursement policies, and competition from commercially manufactured drugs continue to influence market growth and operational strategies.

AI-Powered Specialty Compounding Expansions:

Integration of artificial intelligence (AI) can significantly enhance the market by improving precision, efficiency, and patient safety. AI-powered systems can assist in formulation optimization, predicting the most effective dosages and ingredient combinations for individualized medications. Automation through AI reduces human errors in compounding processes, ensures regulatory compliance, and streamlines workflow management. Additionally, AI can analyze patient data to forecast demand, manage inventory, and identify emerging trends in therapy needs. By enabling faster, more accurate, and personalized medication preparation, AI integration strengthens operational efficiency, enhances patient outcomes, and positions compounding pharmacies as innovative leaders in the healthcare sector.

Driver

Regulatory Support

Regulatory support plays a pivotal role in fostering the growth of the U.S. compounding pharmacy market by ensuring safety, enhancing public trust, and facilitating market expansion. Legislative measures not only address immediate healthcare needs but also establish a framework for sustainable growth in the compounding pharmacy sector. By aligning regulatory policies with market demands, these initiatives bolster the industry's capacity to deliver personalized and timely pharmaceutical solutions.

In 2025, significant legislative actions underscored this impact. The introduction of the Drug Shortage Compounding Patient Access Act of 2025 (H.R. 5316), supported by the Alliance for Pharmacy Compounding (APC), Congresswoman Diana Harshbarger, and Congressman Buddy Carter, aims to empower compounding pharmacies to address drug shortages effectively. This bipartisan initiative seeks to expand the scope of compounded medications during shortages, ensuring patient access to essential therapies.

Restraint

Quality and Safety Concerns & Competition from Standardized Pharmaceuticals

Past incidents of contamination and improper practices have raised concerns about the safety of compounded drugs, leading to stricter oversight and reduced trust. Availability of FDA-approved drugs often reduces reliance on compounded alternatives, especially when shortages ease.

Opportunity

Patient-Centric Approach

A shift toward patient-centric care models significantly enhances growth prospects for U.S. compounding pharmacies by aligning services more closely with individual patient needs and improving access, satisfaction, and outcomes. Under such models, pharmacies can offer tailored formulations altering active ingredient concentrations, excluding allergens, or changing delivery modes to better suit patients with specific health conditions, allergies, or lifestyle preferences. Focusing on patient-centric access (affordability, legal, certified compounds) strengthens trust in compounded therapies and drives demand. By putting patient experience at the core through personalized care, telehealth integration, and service flexibility, the compounding pharmacy market can grow more rapidly and sustainably.

In 2024, Hypermedica launched an initiative in partnership with certified compounding pharmacies and telehealth platforms to ensure continuous access to affordable compounded GLP-1 medications amid branded shortages and price surges.

| Table | Scope |

| Market Size in 2026 | USD 7.42 Billion |

| Projected Market Size in 2035 |

USD 12.79 Billion |

| CAGR (2026 - 2035) | 6.24% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Pharmacy Type, By Product Type, By End User, By Distribution Channel, By Region |

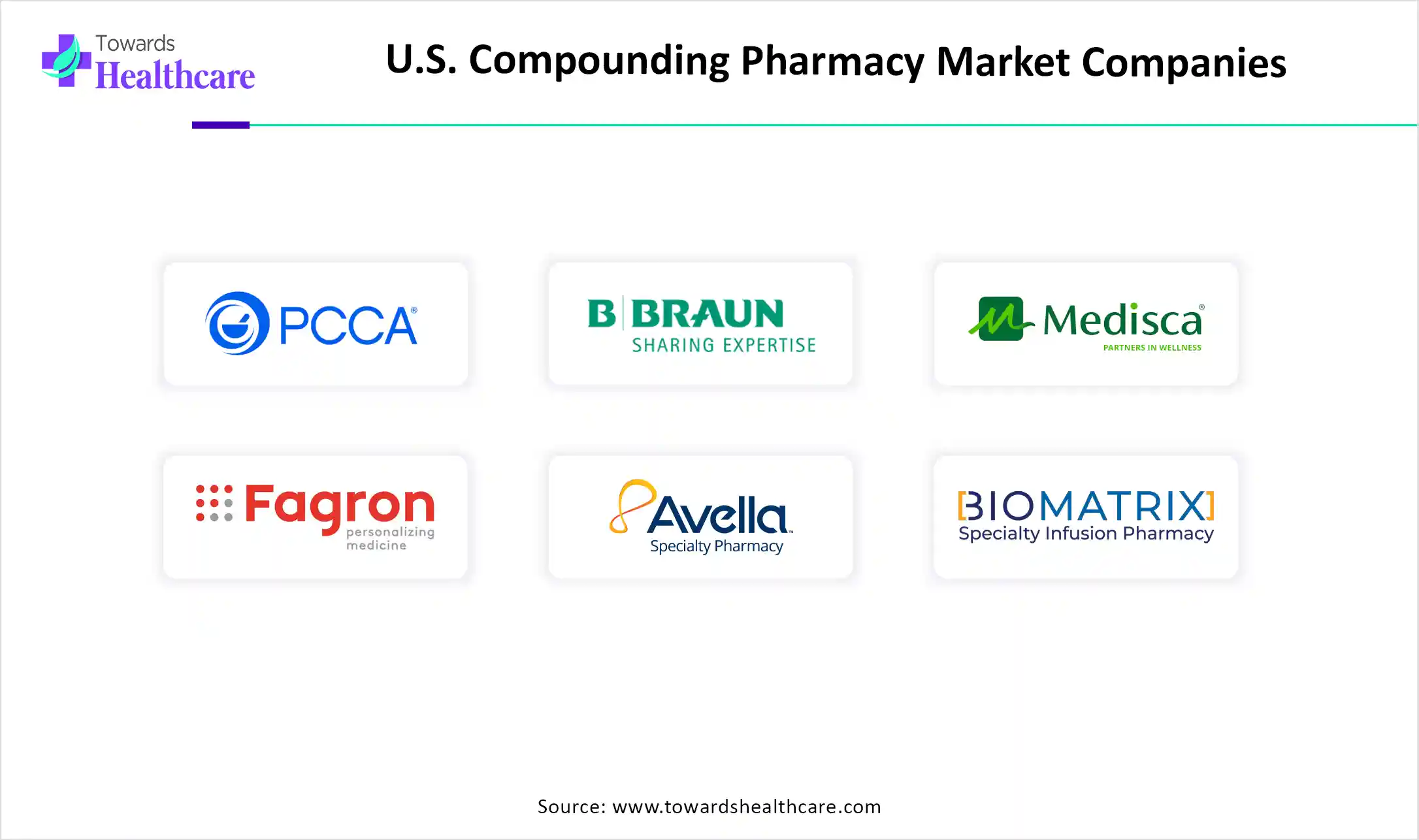

| Top Key Players | PCCA (Professional Compounding Centers of America), B. Braun Medical Inc., Medisca Inc., Fagron Inc, Wedgewood Pharmacy, Avella Specialty Pharmacy, NuVision Pharmacy, Diamond Pharmacy, Belmar Pharmacy, The Compounding Pharmacy of America, RXCrossroads (McKesson), PharMEDium (Fresenius Kabi), Central Pharmacy, CustomMed Pharmacy, BioMatrix Specialty Pharmacy, Epic Pharmacy, HealthLink Compounding Pharmacy, National Pharmaceutical Services (NPS), Kane Compounding Pharmacy, Sage Specialty Pharmacy |

")

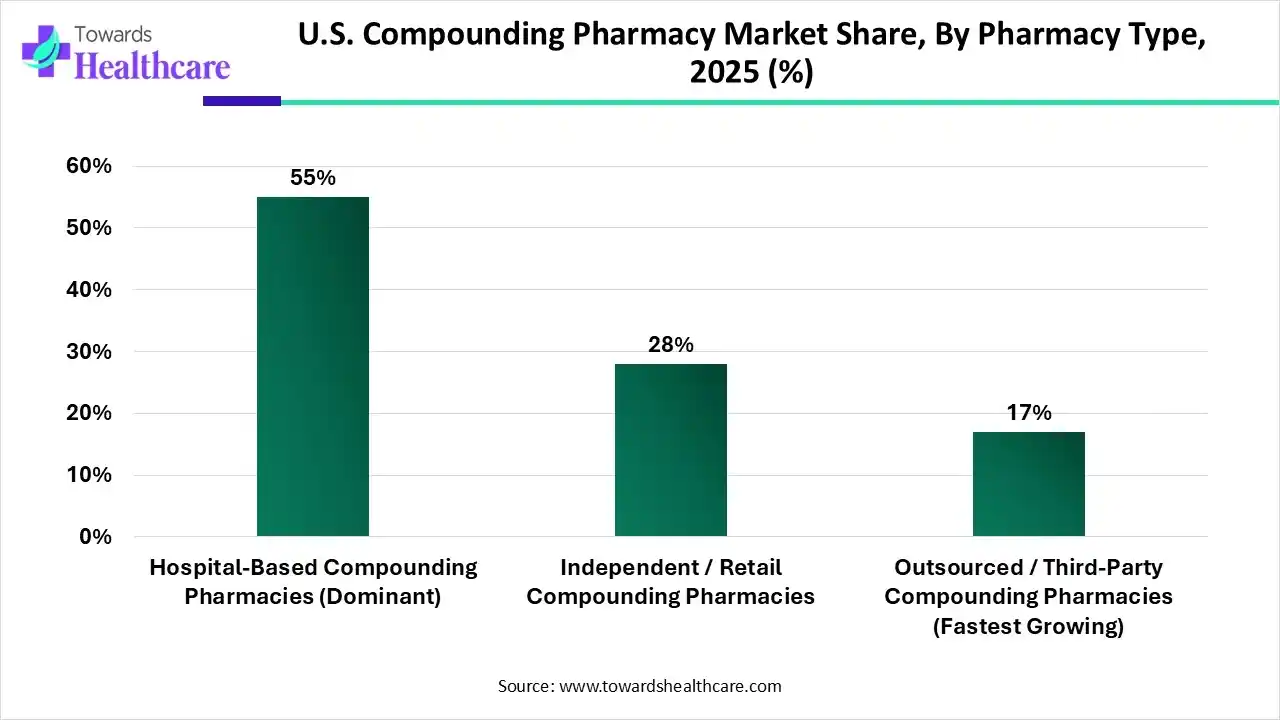

| Segments | Shares% |

| Hospital-Based Compounding Pharmacies (Dominant) | 55% |

| Independent / Retail Compounding Pharmacies | 28% |

| Outsourced / Third-Party Compounding Pharmacies (Fastest Growing) | 17% |

Explanation

Which Pharmacy Type Segment Dominated the U.S. Compounding Pharmacy Market?

The hospital-based compounding pharmacies segment dominates the market by 55% due to its ability to prepare sterile and complex formulations required for critical care, oncology, and surgical procedures. Hospitals ensure high safety standards, regulatory compliance, and immediate availability of customized drugs. Growing demand for parenteral nutrition, pain management, and chemotherapy preparations further strengthens their dominance in the healthcare ecosystem.

The outsourced/third-party compounding pharmacies segment is anticipated to be the fastest-growing in the U.S. compounding pharmacy market due to rising reliance on hospitals and clinics to meet the increasing demand for sterile and complex medications. By outsourcing, healthcare providers reduce internal workload, operational risks, and compliance challenges, while ensuring timely access to high-quality compounded drugs. The strict regulatory oversight of 503B outsourcing facilities under CGMP standards enhances safety and trust.

| Segments | Shares % |

| Sterile Compounded Medications (Dominant) | 60% |

| Non-Sterile Compounded Medications | 22% |

| Nutraceutical & Hormone Replacement Therapy (HRT) Products (Fastest Growing) | 10% |

| Veterinary Compounded Medications | 8% |

Explanation

Why Did the Sterile Compounded Medications Segment Dominate the U.S. Compounding Pharmacy Market?

The sterile compounded medications segment dominates the market by 60% because they are essential for critical treatments such as intravenous infusions, chemotherapy, ophthalmic preparations, and total parenteral nutrition. Hospitals and clinics rely heavily on sterile compounding to ensure patient safety and efficacy in sensitive therapies. Stringent regulations like USP <797> and FDA oversight of 503B facilities enhance credibility and quality assurance. Rising demand for injectable and infusible drugs, coupled with drug shortages, further strengthens the dominance of sterile compounded medications.

The nutraceutical & hormone replacement therapy (HRT) products segment is estimated to be fastest fastest-growing segment in the U.S. compounding pharmacy market due to rising awareness of hormonal imbalances such as menopause, andropause, and thyroid disorders, along with the growing preference for natural and preventive health solutions. Compounded bioidentical hormone therapies allow customized dosages and formulations tailored to patient needs, while nutraceuticals meet demand for wellness and disease prevention. The flexibility of compounding pharmacies, combined with easier access through telehealth and online platforms, further fuels the rapid growth of this segment.

| Segments | Shares % |

| Hospitals & Clinics (Dominant) | 50% |

| Individual Patients (Fastest Growing) | 30% |

| Veterinary Clinics & Pet Owners | 20% |

Explanation

How the Hospitals & Clinics Segment Dominated the Market?

The hospitals & clinics segment dominates the U.S. compounding pharmacy market by 50% because of their high reliance on customized medications for critical care, including sterile preparations, oncology drugs, pain management, and parenteral nutrition. These facilities require timely access to safe and effective compounded therapies that meet stringent regulatory and safety standards. The presence of in-house or outsourced compounding ensures a continuous supply during drug shortages. Additionally, the rising number of complex surgical procedures and chronic disease treatments further strengthens hospitals and clinics as the leading end-use segment.

The individual patients segment is anticipated to be the fastest-growing in the U.S. compounding pharmacy market due to rising demand for personalized medicines tailored to unique health needs. Patients increasingly seek customized dosages, allergen-free formulations, and alternative delivery methods not available in commercial drugs. Growth in chronic illnesses, pediatric requirements, and geriatric care supports this trend. Moreover, increasing awareness of bioidentical hormones, wellness products, and telehealth access further accelerates adoption, making individual patients a key driver of compounding pharmacy expansion.

| Segments | Shares% |

| Direct to Pharmacy / Hospital (Dominant) | 55% |

| Retail / Walk-In Pharmacies | 27% |

| Online / Mail-Order Services (Fastest Growing) | 18% |

Explanation

What Made Direct to Pharmacy/Hospital the Dominant Segment in the Market?

The direct-to-pharmacy/hospital segment is the dominant distribution channel in the U.S. compounding pharmacy market by 55% because it ensures faster, safer, and more reliable delivery of compounded medications directly to healthcare providers. This channel supports timely access to critical sterile preparations, oncology drugs, and customized therapies essential for patient care. Hospitals and pharmacies prefer direct procurement as it reduces dependency on intermediaries, minimizes supply delays, and maintains regulatory compliance.

The online/mail-order services segment is estimated to be the fastest-growing in the U.S. compounding pharmacy market due to the rising preference for convenience, accessibility, and privacy in obtaining customized medications. Patients increasingly turn to digital platforms for refills and consultations, especially for therapies like hormone replacement, nutraceuticals, dermatology solutions, and pediatric formulations. Telehealth integration further enhances this channel by enabling virtual consultations and direct prescription fulfillment. Mail-order services are particularly valuable for patients in remote or underserved areas, ensuring timely access to medications.

The South U.S. is the dominant region in the U.S. compounding pharmacy market due to its large population base, higher prevalence of chronic diseases, and significant demand for customized therapies. The region hosts a strong network of hospitals, specialty clinics, and compounding facilities that cater to rising healthcare needs. Favorable demographics, including a growing elderly population, further drive demand for personalized medications. Additionally, the South has seen increased investment in advanced compounding infrastructure, supporting sterile preparations and hormone replacement therapies, which reinforce its leading market position.

The Midwest U.S. is the fastest-growing region in the U.S. compounding pharmacy market due to increasing awareness and adoption of personalized medicine, coupled with a rising patient population requiring specialized treatments. The region faces a growing prevalence of chronic diseases, pediatric needs, and geriatric care, all fueling demand for customized formulations. Expanding healthcare infrastructure and investments in sterile compounding facilities also support growth.

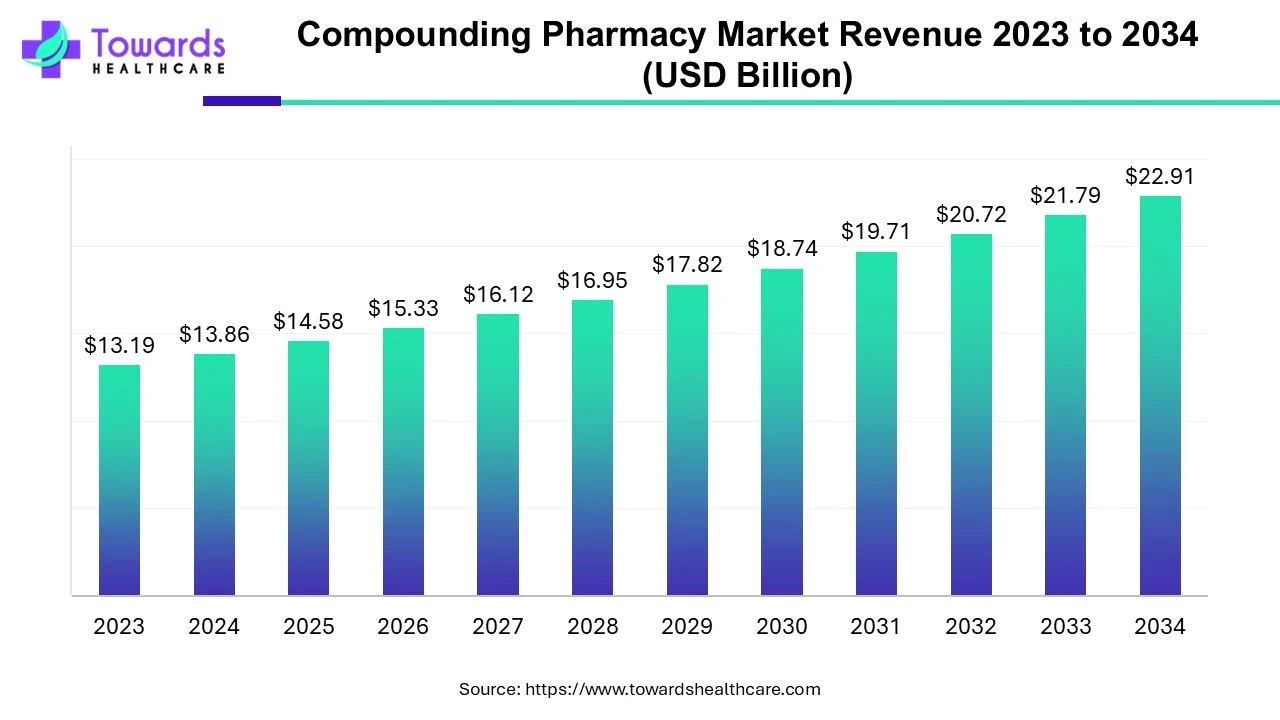

The global compounding pharmacy market was valued at approximately US$ 13.19 billion in 2023 and is expected to reach around US$ 22.91 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.15% between 2024 and 2034.

")

Research & Development (R&D)

Clinical Trial and Approval

Patient Support and Service

Strengths

Weaknesses

Opportunities

Threats

| Companies | Description |

| PCCA (Professional Compounding Centers of America) | The company is a premier supplier for independent, specialized compounding pharmacies in the U.S. and globally, providing high-quality chemicals, equipment, training, and software. |

| B. Braun Medical Inc. | The company is a significant player, offering a combination of automated compounding technology, sterile manufacturing services, and specialized pharmacy services through its subsidiaries. |

| Medisca Inc. | In 2024, the company opened a "MAZ Lab" in Arizona, an innovation and customer resource center focused on compounding technology. |

| Fagron Inc | The company is a leading provider of high-quality pharmaceutical raw materials, specialized vehicles, and innovative compounding tools in the U.S. market, focusing on personalized medicine. |

| Wedgewood Pharmacy | The portfolio focuses on animal health, offering custom medications for veterinarians and pets, including flavored solutions, treats, and transdermal gels. |

| Avella Specialty Pharmacy | The company specializes in therapeutic areas including oncology, pain management, dermatology, and fertility, offering tailored dosages and specialized formulations for patient needs. |

| HealthLink Compounding Pharmacy | The portfolio includes oral (highest share), topical, and sterile preparations, with top therapeutic areas focused on pain management and hormone replacement. |

| Diamond Pharmacy | The company is the largest correctional pharmacy provider in the U.S., specializing in unit-dose blister card medication dispensing. |

| Belmar Pharmacy | The company is a major player in the U.S. compounding pharmacy market in bioidentical hormone replacement therapy (BHRT), integrative medicine, and nutritional therapies. |

| The Compounding Pharmacy of America | The portfolio focuses on products designed for pain management, hormone replacement therapy (HRT), anti-aging/skin care, and customized nutritional supplements. |

In May 2025, the Chairman and CEO of LifeMD, stated that LifeMD, Inc., a leading virtual primary care provider has announced a special US$299 introductory bundle for new self-pay patients who are prescribed Wegovy (semaglutide). This bundle includes both the prescription drugs and the ability to use LifeMD's online weight-loss program. In light of April, LifeMD announced a partnership with Novo Nordisk to offer Wegovy at a discounted price of US$199. An extra US$100 will cover LifeMD's clinical care, onboarding, and maintenance.

By Pharmacy Type

By Product Type

By End User

By Distribution Channel

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar