Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

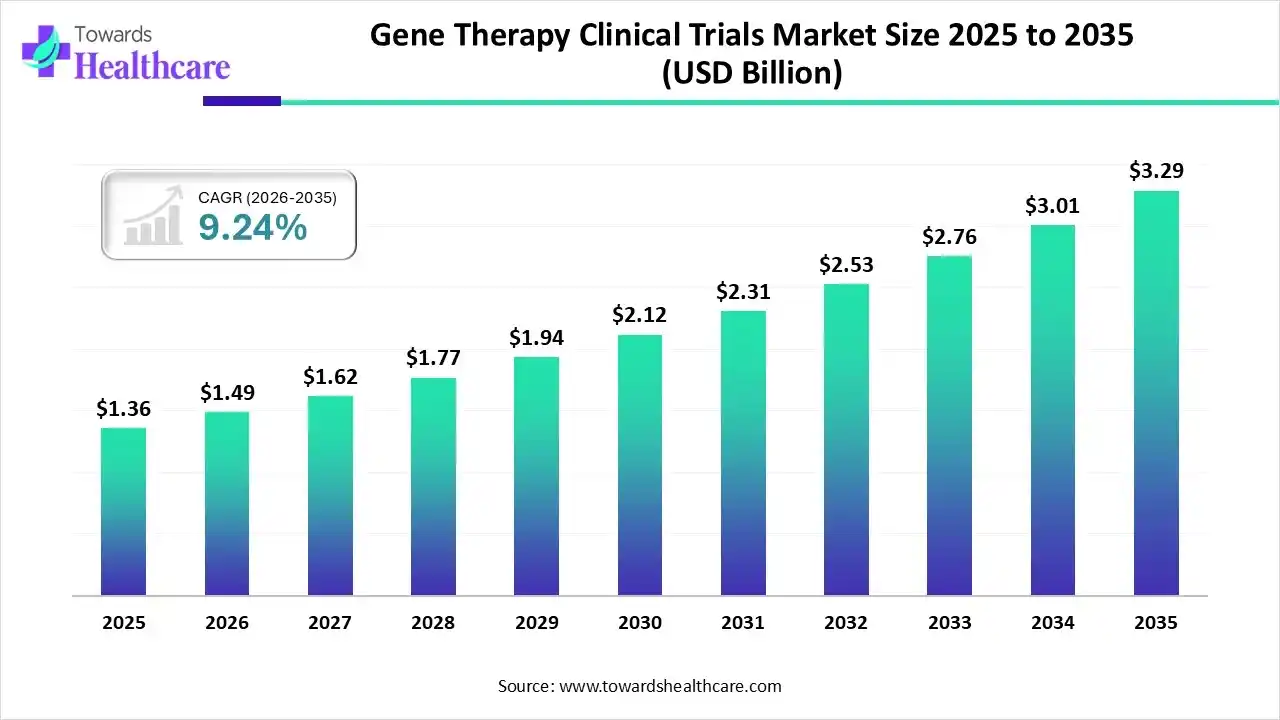

The gene therapy clinical trials market size was valued at US$ 1.36 billion in 2025 and is projected to grow to 1.49 billion in 2026. Forecasts suggest it will reach approximately US$ 3.29 billion by 2035, registering a CAGR of 9.24% during the period.

")

The gene therapy clinical trials market is primarily driven by the increasing need for personalized medicines and growing research and development activities. The rising prevalence of genetic and rare disorders potentiates the demand for gene therapy. Government organizations support the development of gene therapy through several initiatives and funding. Prominent players collaborate to access advanced technologies and develop innovative products. Artificial intelligence (AI) streamlines the entire clinical trial process and aids in data analysis. The future is promising, with the advancements in genomic technologies.

The gene therapy clinical trials market covers sponsored studies that evaluate in vivo and ex vivo gene delivery to treat or prevent disease using viral vectors (AAV, lentivirus, adenovirus, HSV), non-viral platforms (plasmid DNA, lipid nanoparticles), genome editing (CRISPR/Cas, ZFN, TALEN), and cell-based gene therapies (e.g., CAR-T, engineered T/NK, HSC). It spans trial planning, site activation, vector and cell handling logistics, manufacturing for clinical supply, and data/biomarker operations. Growth is driven by expanding pipelines, maturing regulatory pathways, better vector engineering and manufacturing capacity, and strong investment in rare diseases, oncology, and ophthalmology.

Increasing Collaboration: Major players collaborate to access advanced technologies and expand their geographical presence. Companies use each other’s expertise to develop innovative products and accelerate time-to-market approval.

AI and machine learning (ML) algorithms can transform the complex clinical trial process by assisting in patient selection, real-time monitoring, and toxicity prediction. AI introduces automation in clinical trials, saving time and costs for healthcare professionals and sponsors. AI and ML can analyze vast amounts of data and predict potential outcomes of a particular gene therapy. They can help researchers in screening large numbers of candidates rapidly and select designs that fulfill the desired criteria, similar to their use in target identification. AI and ML enhance the efficiency and accuracy of clinical trials.

Demand for Gene Therapy

The major growth factor for the gene therapy clinical trials market is the growing demand for gene therapy. Gene therapy is widely preferred as it directly cures a disease from its root cause. The rising prevalence of cancer, neurological, genetic, and rare disorders increases the need for gene therapy. Unlike small molecules, gene therapy provides targeted treatment, which is beneficial to patients, resulting in fewer side effects. Regulatory agencies necessitate the conduct of clinical trials to assess a product’s safety and efficacy before market approval. As of 15th August 2025, the U.S. Food and Drug Administration has approved 46 cell and gene therapy products.

Lack of Access

The advanced gene therapy in clinical trials is generally inaccessible to people from rural areas. Rural areas lack skilled professionals with experience in executing gene therapy clinical trials and access to tools that can pre-emptively assess the risk to patients based on data.

What is the Future of the Gene Therapy Clinical Trials Market?

The market future is promising, driven by the advancements in genomic technologies. Innovative genomic techniques, such as CRISPR-Cas9, are widely adopted to revolutionize gene therapy development. The CRISPR-Cas9 technique offers specific modifications of target genes, resulting in high accuracy and efficiency. Prime editing and approaches involving CRISPR-Cas effectors present future opportunities for researchers as they are more versatile and efficient tools for manipulating genetic material. This technique offers unprecedented precision in genome editing. It guides Cas9 to the target DNA and provides the necessary template for the insertion, deletion, or conversion of specific DNA sequences.

| Table | Scope |

| Market Size in 2026 | USD 1.49 Billion |

| Projected Market Size in 2035 | USD 3.29 Billion |

| CAGR (2026 - 2035) | 9.24% |

| Leading Region | North America by 46% |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Therapy Modality, By Vector/Delivery Platform, By Therapeutic Area, By Clinical Phase, By Route of Administration, By Region |

| Top Key Players | Novartis, Roche/Genentech, Pfizer, Biogen, Regeneron, Sarepta Therapeutics, Bluebird bio, CRISPR Therapeutics, Editas Medicine, Intellia Therapeutics, Verve Therapeutics, Sana Biotechnology, Beam Therapeutics |

")

| Segments | Shares % |

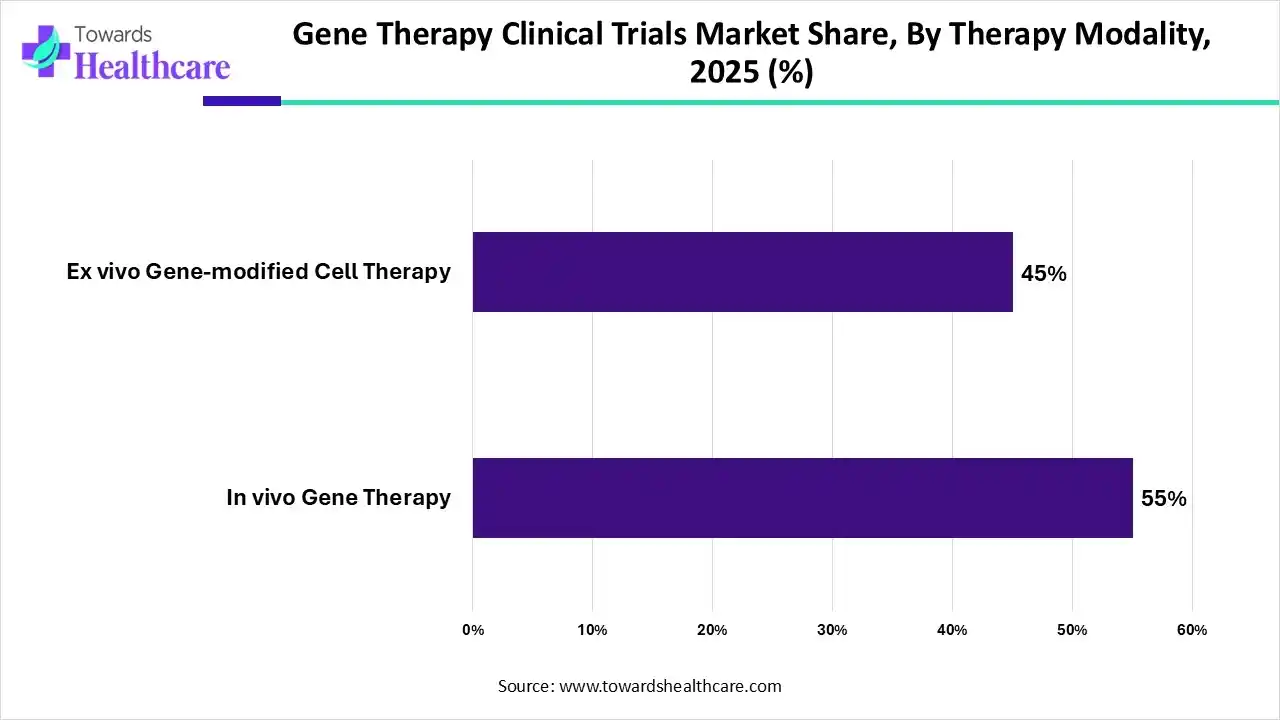

| In vivo Gene Therapy | 55% |

| Ex vivo Gene-modified Cell Therapy | 45% |

Explanation

Which Therapy Modality Segment Dominated the Gene Therapy Clinical Trials Market?

By therapy modality, the in vivo gene therapy segment held a dominant presence in the market by 55% in 2025. This is due to the high simplicity and efficiency of the in vivo process. The in vivo refers to the direct delivery of genetic material into the patient’s body through the parenteral route. The genetic material is transferred using a vector, aiding in its targeted delivery. Advancements in vector technology and cost-effectiveness potentiate the demand for in vivo gene therapy.

By therapy modality, the ex vivo gene therapy segment is expected to grow at the fastest CAGR in the market during the forecast period. Ex vivo gene therapy involves removing specific cells from a person, genetically altering them in a laboratory, and transplanting them back into the person. This technique enables researchers to develop gene therapy against a wide range of disorders as they can modify the genetic material based on a patient’s needs.

| Segment | Share 2025 (%) |

| AAV (Adeno-Associated Virus) | 45% |

| Lentiviral Vectors | 25% |

| Adenoviral/Oncolytic & Others | 15% |

| Non-viral (plasmid DNA, LNP/mRNA) | 10% |

| Genome Editing (CRISPR, ZFN, TALEN) | 5% |

Explanation

How the AAV (Adeno-Associated Virus) Segment Dominated the Gene Therapy Clinical Trials Market?

By vector/delivery platform, the AAV (adeno-associated virus) segment held the largest revenue share of the market by 45% in 2025. This segment dominated because AAV vectors are non-pathogenic and can be engineered to carry specific genes into target cells. These vectors do not cause any harm or illness to humans. They can directly target the cause of a disease and change the way a cell functions. AAV vectors are highly preferred as they are non-integrating, i.e., they do not insert their DNA into the cell’s genome. They can persist within a patient’s body even for a lifetime.

By vector/delivery platform, the genome editing segment is expected to grow with the highest CAGR in the market during the studied years. Certain genome editing techniques, such as CRISPR, ZFN, TALEN, and AAV/LNP, facilitate gene delivery within patients. These techniques enable researchers to knock out faulty genes and insert correct genes. They provide targeted treatment to recognize specific DNA sequences. CRISPR-based genome-scale screening methods can overcome numerous technical hurdles associated with other contemporary screening technologies.

| Segments | Shares% |

| Oncology | 35% |

| Rare/Genetic & Metabolic Disorders | 19% |

| Ophthalmology (retinal) | 15% |

| Hematology (hemoglobinopathies, coagulation) | 10% |

| Neurology/CNS | 4% |

| Cardiovascular Diseases | 10% |

| Infectious Diseases | 4% |

| Others | 3% |

Explanation

Why Did the Oncology Segment Dominate the Gene Therapy Clinical Trials Market?

By therapeutic area, the oncology segment contributed the biggest revenue share of the market by 35% in 2025. This is due to the rising prevalence of cancer and the need for personalized treatment. Many tumors are caused by genetic mutations, which lead to abnormal cell growth. Gene therapy alters the genetic material of a patient that causes cancer, ultimately curing the cancer from its root cause. As of August 2025, 1,472 studies are registered related to gene therapy in cancer on the clinicaltrials.gov website.

By therapeutic area, the neurology/CNS segment is expected to expand rapidly in the market in the coming years. Ongoing efforts are made to develop gene therapy for expanding applications, such as neurological disorders. Government organizations encourage the general public to screen for and aid in the early diagnosis of neurological disorders. This creates a new wave for the therapeutic development of gene-targeted therapies, offering hope for modifying the natural course of the disease.

| Segments | Shares % |

| Phase I/I/II | 60% |

| Phase II | 20% |

| Phase III & Pivotal/Confirmatory | 15% |

| Post-marketing/Long-term Follow-up (LTFU) | 5% |

Explanation

Which Clinical Phase Segment Led the Gene Therapy Clinical Trials Market?

By clinical phase, the phase I/ I/II segment led the global market by 60% in 2025. This is due to the need to establish a new drug’s safety and dose range. Phase I clinical trials are conducted at a small scale, usually involving 20-100 healthy volunteers. If a treatment is found safe in a phase I clinical trial, a phase 2 clinical trial is conducted on a larger patient population. Phase II trials help to determine the effectiveness of a therapeutic.

By clinical phase, the Phase III & pivotal/confirmatory segment is expected to witness the fastest growth in the market over the forecast period. Phase III trials are conducted on a much larger scale, involving hundreds to thousands of patients, to assess a drug’s efficacy. Only 25-30% of drugs reach Phase III trials. The results of a Phase III trial are essential as regulatory agencies approve a product based on the efficacy and safety required to be approved and commercialized.

| Segments | Shares % |

| Intravenous/Systemic | 40% |

| Intravitreal/Subretinal | 15% |

| Intrathecal/Intracerebroventricular | 10% |

| Intratumoral/Regional | 10% |

| Hepatic-targeted, Intramuscular & Others | 25% |

Explanation

What Made Intravenous/Systemic the Dominant Segment in the Gene Therapy Clinical Trials Market?

By route of administration, the intravenous/systemic segment accounted for the highest revenue share of the market by 40% in 2025. Gene therapy is commonly administered through the intravenous route, allowing it to circulate throughout the body and reach the target site. It is widely preferred due to its faster onset of action and high bioavailability. The demand for minimally invasive gene delivery and the need to avoid the complexities of direct injection into multiple tissues make the intravenous route a suitable choice.

By route of administration, the intrathecal/intracerebroventricular segment is expected to show the fastest growth over the forecast period. The intrathecal/intracerebroventricular route is generally used for patients with neurological disorders. This helps healthcare professionals to deliver the gene therapy directly into the CNS. This route provides targeted treatment and reduces systemic side effects.

")

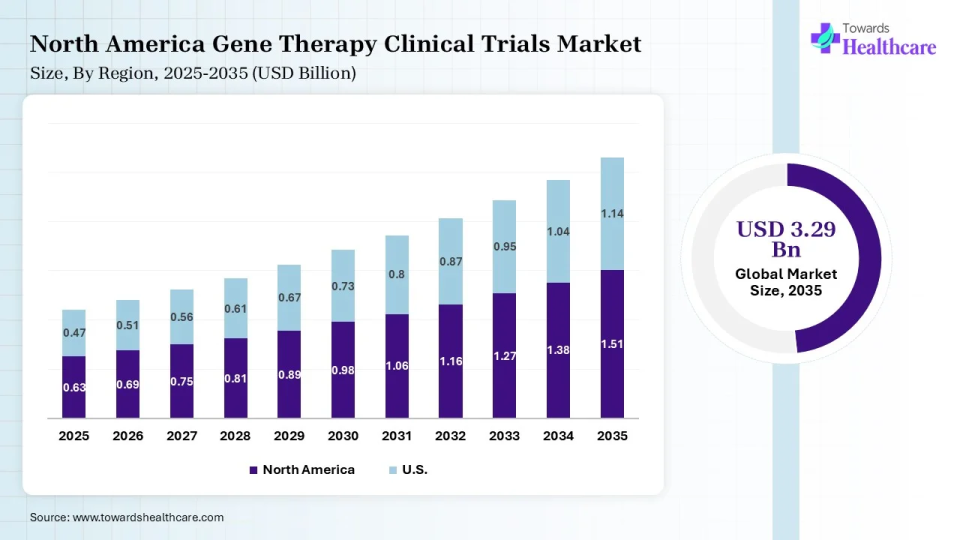

North America dominated the global market in 2025. The presence of key players, the availability of a favorable clinical trial infrastructure, and increasing investments are the major growth factors of the market in North America. The region has an expanding manufacturing capacity, favoring commercial-scale manufacturing of gene therapy. Government organizations launch initiatives to support clinical trials and the development of novel gene therapy products.

U.S. Market Trends

Key players, such as Pfizer, Inc., Biogen, and Regeneron Pharmaceuticals, are the major contributors to the market in the U.S. The American Society of Gene & Cell Therapy (ASGCT) reported that 79 trials were initiated in Q1. About 12 start-ups collectively raised approximately $304.5 million in Q1 seed and Series A funding.

Canada Market Trends

The Canadian Institutes of Health Research (CIHR) provides funding for bringing rare disease gene therapies to clinical readiness as part of the National Strategy for Drugs for Rare Diseases. In 2023, it announced investments of up to $1.5 billion over three years. In August 2024, Ocugen, Inc. announced that Health Canada approved a “No Objection Certificate” to initiate the OCU400 Phase 3 clinical trial in Canada.

Asia-Pacific is expected to grow at the fastest CAGR in the gene therapy clinical trials market during the forecast period. The rapidly expanding clinical trial infrastructure and affordable services encourage foreign investors to conduct their clinical trials in Asia-Pacific countries, like China, Japan, and India. The increasing number of local sponsors and collaborations among key players fosters market growth. The growing research and development activities and the rising adoption of advanced technologies contribute to market growth.

China Market Trends

As of August 2025, a total of 494 clinical trials were registered in China related to gene therapy. In December 2024, Bayer announced that it had entered into agreements with Epigenic Therapeutics (Shanghai) Biotechnology Co., Ltd., Shanghai Immunocan Biotech Co., Ltd., and AccurEdit Therapeutics Co., Ltd. as resident companies. This will enable the companies to access worldwide resources and expertise, accelerating breakthrough innovations in CGT.

India Market Trends

In India, 24 clinical trials related to gene therapy are registered as of August 2025. Government agencies promote the indigenous development of gene therapy through “Make in India” and “Atmanirbhar Bharat” initiatives. In April 2024, the President of India launched India’s first home-grown gene therapy for cancer at IIT Bombay.

| Company | Key Offerings | Contributions | Other Details |

| Novartis | Gene therapies, CAR-T | Advanced cell and gene therapy trials | Strong global R&D |

| Roche / Genentech | Genomic medicines | Expands gene therapy research | Focus on oncology and rare diseases |

| Pfizer | Viral vector therapies | Invests in gene therapy manufacturing | Broad clinical trial pipeline |

| Biogen | Neurological gene therapies | Develops treatments for rare disorders | Strong neuroscience expertise |

| Regeneron | Genetic medicine platforms | Integrates genomics with drug discovery | Expanding gene therapy programs |

| Sarepta Therapeutics | Muscular dystrophy therapies | Leads gene therapy trials in DMD | Focus on rare diseases |

| bluebird bio | Lentiviral gene therapies | Pioneers in treatments for genetic diseases | Focus on hematologic disorders |

| CRISPR Therapeutics | CRISPR-based therapies | Develops genome editing treatments | Strong clinical collaborations |

| Editas Medicine | CRISPR therapeutics | Advances in vivo gene editing | Focus on inherited diseases |

| Intellia Therapeutics | CRISPR gene therapies | Develops in vivo editing treatments | Expanding rare disease trials |

Michael Culme-Seymour, Regional Vice President for APAC at Cencora, commented that the percentage of clinical trials in the APAC region is tremendously increasing, from 8% in 2013 to 29% in 2023. The company expands and strengthens its capabilities to meet the growing demand for premium specialty logistics services as more companies establish clinical trials. There are more than 650 cell and gene therapy (CGT) clinical trials underway in the region.

By Therapy Modality

By Vector/Delivery Platform

By Therapeutic Area

By Clinical Phase

By Route of Administration

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar