Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

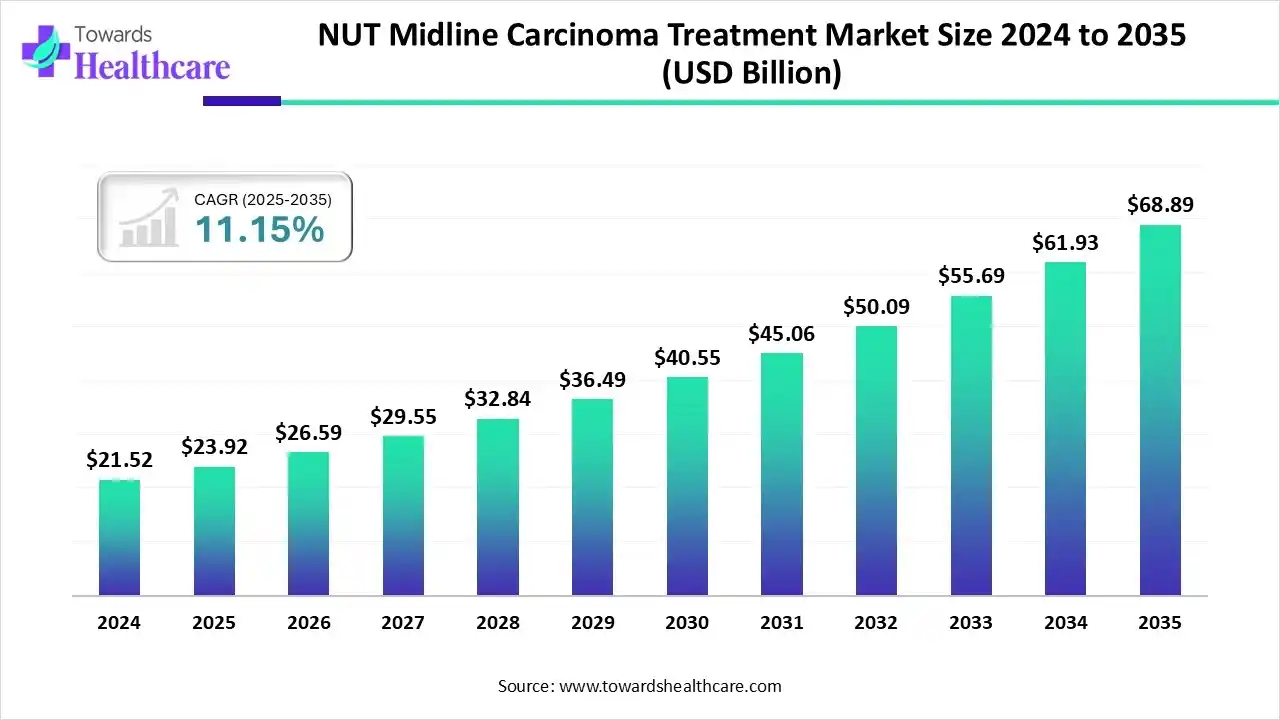

The global NUT midline carcinoma treatment market size is estimated at US$ 23.92 billion in 2025, grew to US$ 26.59 billion in 2026, and is expected to reach approximately US$ 68.89 billion by 2035. The market is expanding at a CAGR of 11.15% from 2026 to 2035.

Companies are developing various treatment options for NUT midline carcinoma, with AI technologies being leveraged to optimize and accelerate drug development. Expanding healthcare infrastructure, robust industry growth, increasing R&D activities, funding, and awareness are driving adoption across regions. Additionally, the launch of targeted therapies is further propelling market growth.

| Table | Scope |

| Market Size in 2025 | USD 23.92 Billion |

| Projected Market Size in 2035 | USD 68.89 Billion |

| CAGR (2026 - 2035) | 11.15% |

| Leading Region | North America |

| Market Segmentation | By Treatment, By Route Of Administration, By End Use, By Region |

| Top Key Players |

Zenith Epigenetics, Merck & Co., Inc., GSK plc, Pfizer Inc, C4 Therapeutics, Inc., Ipsen Biopharmaceuticals, Inc., Novartis AG, Sanofi S.A. |

The NUT midline carcinoma treatment market is fueled by a growing shift toward novel targeted therapies, increasing diagnostic advancements, and rising awareness. Treatments for NUT midline carcinoma include various options such as chemotherapy, radiotherapy, as well as emerging targeted and immunotherapies, with personalized and more effective treatments also being developed. These therapies help control tumor progression, shrink tumors, or remove them, providing targeted action that enhances patient outcomes.

AI is transforming the NUT midline carcinoma treatment market by enabling precise diagnosis and genomic profiling, which helps identify the specific BRD4-NUT fusion mutations driving the cancer. It facilitates the development of personalized therapies by predicting which treatments are most likely to be effective for individual patients. Additionally, AI aids in drug discovery by forecasting drug targets, interactions, and potential toxicities, accelerating the creation of optimized treatment options. Overall, AI enhances treatment precision, reduces development timelines, and improves patient outcomes in this rare and aggressive cancer segment.

| Sub-Segment | Market Share (%) |

| Chemotherapy | 45% |

| Targeted Therapy | 25% |

| Immunotherapy | 15% |

| Radiation Therapy | 10% |

| Others | 5% |

Explanations:

Which Treatment Segment Holds the Dominant Share of the NUT Midline Carcinoma Treatment Market in 2024?

The chemotherapy segment held the dominant market share in 2024 due to its status as the primary first-line therapy for aggressive cancers. Its systemic effects allow it to target rapidly progressing tumors, while its broad-spectrum activity addresses multiple cancer pathways. Additionally, the widespread availability and established clinical use of chemotherapy drugs have contributed to their preference among healthcare providers, reinforcing their leading market position.

The targeted therapy segment is expected to grow at the highest CAGR during the projection period, as it offers target-specific action, thereby increasing effectiveness and promoting its use. At the same time, fewer side effects associated with targeted therapies are boosting adoption rates, improving survival rates, and encouraging further innovation. Additionally, increasing research, regulatory approvals, and adoption of novel targeted drugs by oncology centers contribute to segmental growth.

The immunotherapy segment is expected to grow at a significant rate in the near future, as it helps boost the body's immune system. This enhances the natural defense mechanism by targeting tumor cells. Personalized therapies are also increasingly being used due to their higher success rates, often combined with other treatment options to improve patient outcomes.

| Sub-Segment | Market Share (%) |

| Intravenous (IV) | 70% |

| Oral | 25% |

| Other | 5% |

Explanations:

What Made Intravenous the Dominant Segment in the Market in 2024?

The intravenous segment dominated the NUT midline carcinoma treatment market in 2024, due to its systemic delivery that provides rapid action. It also offers high bioavailability, which enhances the therapeutic effect of treatment options and increases their use in emergency situations. Additionally, various chemotherapy agents, which are unstable in the digestive tract, are administered through this route.

The oral segment is expected to register the highest CAGR during the forecast period, as this route offers easy administration, which helps improve patient convenience. Additionally, they are the preferred method for long-term cancer treatment, which is driving the development of oral formulations. Furthermore, self-administration trends are increasing their use.

| Sub-Segment | Market Share (%) |

| Hospitals | 65% |

| Specialty Clinics | 25% |

| Other | 10% |

Explanations:

How Does the Hospitals Segment Dominate the NUT Midline Carcinoma Treatment Market in 2024?

The hospitals segment dominated the market by holding the largest share in 2024 due to the availability of various treatment options. At the same time, the presence of experienced professionals in these settings helps in effectively delivering complex therapies to patients. Moreover, the high usage of continuous patient monitoring and increased adoption of advanced therapies are attracting more patients to these settings.

The specialty clinics segment is expected to grow at the fastest rate in the coming years, due to the presence of skilled personnel, which helps in providing personalized treatment options. At the same time, they also offer shorter waiting times, which improve patient adherence to treatment. Additionally, they provide advanced, targeted therapies that are attracting patients.

| Region | Market Share (%) |

| North America | 40% |

| Europe | 27% |

| Asia-Pacific | 22% |

| Latin America | 6% |

| Middle East & Africa | 5% |

Explanations:

North America led the NUT midline carcinoma treatment market in 2024, capturing the largest share, driven by the presence of a large number of market players that accelerated the development of novel therapies. Significant growth in R&D investments further encouraged innovation across both industry and academic institutions. Advanced healthcare infrastructure and high adoption rates of cutting-edge treatments also supported market expansion. Additionally, favorable regulatory frameworks and growing awareness among healthcare professionals strengthened the region’s leadership in the market.

There is significant growth in R&D activities across U.S., supported by government funding and private investment, which is driving clinical trials. Additionally, the rising incidence of NUT midline carcinoma is increasing the adoption of advanced and personalized therapies. For instance, according to Nature Reviews Clinical Oncology, the total number of NUT carcinoma cases in the U.S. is estimated at 1,400 per year.

Asia Pacific is expected to grow at the fastest rate in the NUT midline carcinoma treatment market during the forecast period, driven by the expanding oncology sector. This, in turn, is increasing interest in the development of NUT carcinoma diagnosis and treatment, which are backed by healthcare investments. Additionally, expanding healthcare and increasing awareness are driving earlier diagnosis and greater use of various treatment options. Additionally, supportive government initiatives and growing private-sector participation are accelerating the availability of innovative therapies, further strengthening the region’s market position.

Expanding healthcare infrastructure in India, including hospitals and specialty clinics, is driving increased demand for NUT carcinoma treatments. Concurrently, the growing oncology sector is fostering innovation and collaborations among companies, accelerating clinical trials. Additionally, government initiatives are enhancing treatment affordability and improving patient outcomes, further supporting market growth in the region.

Europe is expected to experience notable growth in the NUT midline carcinoma treatment market during the forecast period, driven by a robust R&D infrastructure that supports the development of complex therapies, new combinations, and other innovative treatment options. Rising awareness about rare cancers and favorable regulatory frameworks are encouraging the development and adoption of targeted and personalized therapies. Additionally, collaborations between biotech companies, academic institutions, and government bodies are accelerating innovation and improving access to novel treatment options across the region.

The UK’s advanced pharmaceutical and biotech industries are actively developing therapies for NUT carcinoma. Regulatory incentives, such as fast-track and orphan drug designations, are fostering innovation and accelerating clinical trials. Additionally, the well-established healthcare system is supporting the growing adoption of personalized and targeted treatments.

South America is witnessing an opportunistic rise in the NUT midline carcinoma treatment market due to increasing healthcare infrastructure investments and growing awareness of rare cancers. Expanding healthcare infrastructure is increasing the detection of these cancers, driving demand for earlier and more effective treatment. The growing awareness of a range of cancers is also driving their diagnosis, thereby increasing the demand for advanced therapies and oral formulations. Additionally, rising government initiatives and partnerships with global pharmaceutical companies are facilitating the adoption of targeted and personalized treatments across the region.

There is growing awareness in Brazil about NUT carcinoma as a rare and aggressive cancer, driving the adoption of genetic testing and treatment services. Additionally, the expanding healthcare sector is increasing the use of immunotherapies, chemotherapy, and targeted therapies. Collaborations among companies are fostering clinical trials, supported by investments from multiple sources.

The market in the Middle East and Africa (MEA) is expected to grow during the forecast period, driven by increased early diagnosis through government-led awareness and screening campaigns. Concurrently, rising healthcare investments are expanding oncology centers, boosting the adoption of various treatment options. Additionally, growth in medical tourism and ongoing innovations are further enhancing market expansion.

Saudi Arabia is witnessing a rise in government initiatives that promote cancer research and development while improving access to novel therapies. Concurrently, advancements in the oncology sector are driving the adoption of molecular testing and enhanced treatment capabilities for managing NUT carcinoma. Additionally, companies are focusing on developing precision medicines alongside more affordable cancer treatment options.

The R&D of NUT midline carcinoma treatment focuses on developing targeted therapies to inhibit the BRD4-NUT fusion protein that drives the cancer, along with combining treatment approaches to improve patient outcomes.

Key Players: Bristol-Myers Squibb Company, Merck & Co., Inc., Pfizer Inc., F. Hoffmann-La Roche Ltd.

The clinical trials and regulatory approval process for NUT midline carcinoma treatments includes assessing efficacy endpoints such as overall response rate (ORR), overall survival (OS), and progression-free survival (PFS).

Key Players: Bristol-Myers Squibb Company, Merck & Co., Inc., Pfizer Inc., GSK plc, F. Hoffmann-La Roche Ltd.

The formulation and final dosage preparation of NUT midline carcinoma treatment involve balancing the use of traditional intravenous chemotherapy with the development of more patient-friendly oral targeted therapies.

Key Players: Bristol-Myers Squibb Company, Merck & Co., Inc., Pfizer Inc., GSK plc, F. Hoffmann-La Roche Ltd.

The packaging and serialization of the NUT midline carcinoma treatment ensure compliance with standard pharmaceutical supply chain regulations, traceability requirements, and proper packaging for safe administration.

Key Players: Bristol-Myers Squibb Company, Merck & Co., Inc., Pfizer Inc., F. Hoffmann-La Roche Ltd.

Patient support and services for NUT midline carcinoma treatment include emotional support networks, financial assistance, genetic counseling services, and access to clinical trials.

Key Players: Bristol-Myers Squibb Company, Merck & Co., Inc., Pfizer Inc., GSK plc, F. Hoffmann-La Roche Ltd.

Corporate Information

Business Overview

BMS is a global biopharmaceutical company focused on discovering, developing, and delivering innovative medicines for serious diseases such as oncology, hematology, immunology, cardiovascular issues, and fibrosis. Regarding NUT midline carcinoma, a rare and aggressive cancer caused by chromosomal rearrangements involving NUTM1 and BRD family proteins, BMS is exploring epigenetic and BET inhibitor therapies that target the underlying molecular fusion proteins (e.g., BRD4-NUT).

Business Segments / Divisions

Geographic Presence

BMS operates globally, with commercial operations, R&D and manufacturing across the Americas, Europe, AsiaPacific, Middle East & Africa. For example, its India affiliate includes commercial, businessinsights and R&D entities in Mumbai, Hyderabad and Bangalore.

Key Offerings

SWOT Analysis

Corporate Information

Business Overview

Zenith Epigenetics is a clinical-stage biotechnology company focused on discovering and developing novel epigenetic therapies, especially bromodomain and extra-terminal domain (BET) inhibitors for oncology indications with high unmet medical needs. Its strategic goal is to translate epigenetic biology into effective cancer treatments, with particular attention to rare and aggressive cancers like NUT carcinoma.

Business Segments / Divisions

Geographic Presence

Zenith Epigenetics operates globally in terms of clinical development and licensing. Although headquartered in Canada, it has additional offices in the U.S. (San Francisco) and conducts clinical trials in the U.S. and internationally. Its development and licensing activities include territories such as Asia (via partnerships) and global trial sites for rare cancers.

Key Offerings

SWOT Analysis

| Companies | Headquarters | Key Strength | Products |

| Zenith Epigenetics | Calgary, Canada | Focuses on the development of potent and selective BET protein inhibitors | ZEN-3694 |

| Merck & Co., Inc. | New Jersey, U.S. | A global leader in oncology | Keytruda |

| GSK plc | Middlesex, UK | Focuses on specific medication development | Molibresib |

| Pfizer Inc | New York, U.S. | Deep and diverse oncology pipeline and various treatment modalities | Chemotherapies |

| C4 Therapeutics, Inc. | Massachusetts, U.S. | Expertise in targeted therapies and fusion-oncoprotein inhibitors | CFT7455 |

| Ipsen Biopharmaceuticals, Inc. | Paris, France | Strong rare oncology focus | BET inhibitors |

| Novartis AG | Basel, Switzerland | Robust rare-cancer pipeline | Epigenetic therapies |

| Sanofi S.A. | Paris, France | Immuno-oncology and rare cancer collaborations | Targeted therapies |

| AbbVie Inc. | Illinois, U.S. | Rare-disease and oncology expertise | Investigational NMC therapies |

| Amgen Inc. | California, U.S. | Biologics and pipeline expansion for rare cancers | Investigational therapies |

| F. Hoffmann-La Roche Ltd | Basel, Switzerland | Strong diagnostics and precision medicine capabilities | Molecular profiling and oncology drugs |

The NUT midline carcinoma treatment market is poised for rapid evolution as the convergence of precision oncology and orphandisease incentives draws expanding R&D interest and commercial ambition. With the disease’s molecular hallmark, a BRD4-NUTM1 fusion, serving as a defined target, the transition from conventional chemotherapy to BET inhibitors, fusion protein degraders, and combination regimens is accelerating. Diagnostic advancements, including next-generation sequencing and fusion detection, are increasing case identification and expanding the treatment pool. These scientific and diagnostic enablers create a compelling market-entry window for novel therapeutic players in this high-unmet-need rare oncology segment.

Geographically, while North America remains the most established region, owing to its advanced healthcare infrastructure, early access frameworks, and favorable orphandrug regulatory regimes, the most attractive growth vectors reside in AsiaPacific and emerging geographies. These regions benefit from scalable oncology infrastructure buildout, increasing public and private investment in rare cancer care, and improving access to molecular diagnostics and targeted therapies. Strategic partnerships and licensing deals in lowerpenetrated markets offer incumbent and newentrant companies the ability to establish leadership in whitespace territories before saturation, thereby capturing disproportionate value.

From a commercialization perspective, this market presents a differentiated highvalue niche within the broader oncology landscape. Competitive advantage will accrue to companies that can combine precision diagnostics, targeted therapeutics, and outcomebased care models, particularly those incorporating digital/AI tools, biomarkerguided patient stratification and servicebundled care delivery. Opportunities include modular business models centred on therapy plus diagnostics, earlymover access into underserved regions, and premium pricing justified by the rarity and aggressiveness of NMC. However, success will require navigating diagnostic adoption, clinical trial scale limitations and reimbursement complexities inherent in ultrarare cancer markets.

By Treatment

By Route Of Administration

By End Use

By Region

Principal Consultant

Shivani Zoting is a dedicated research analyst specializing in the healthcare industry. With a strong academic foundation, a B.Sc. in Biotechnology and an MBA in Pharmabiotechnology, she brings a unique blend of scientific understanding and strategy.

Learn more about Shivani Zoting

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar