Pipeline Programs

CGT Companies Tracked

Manufacturing Facilities

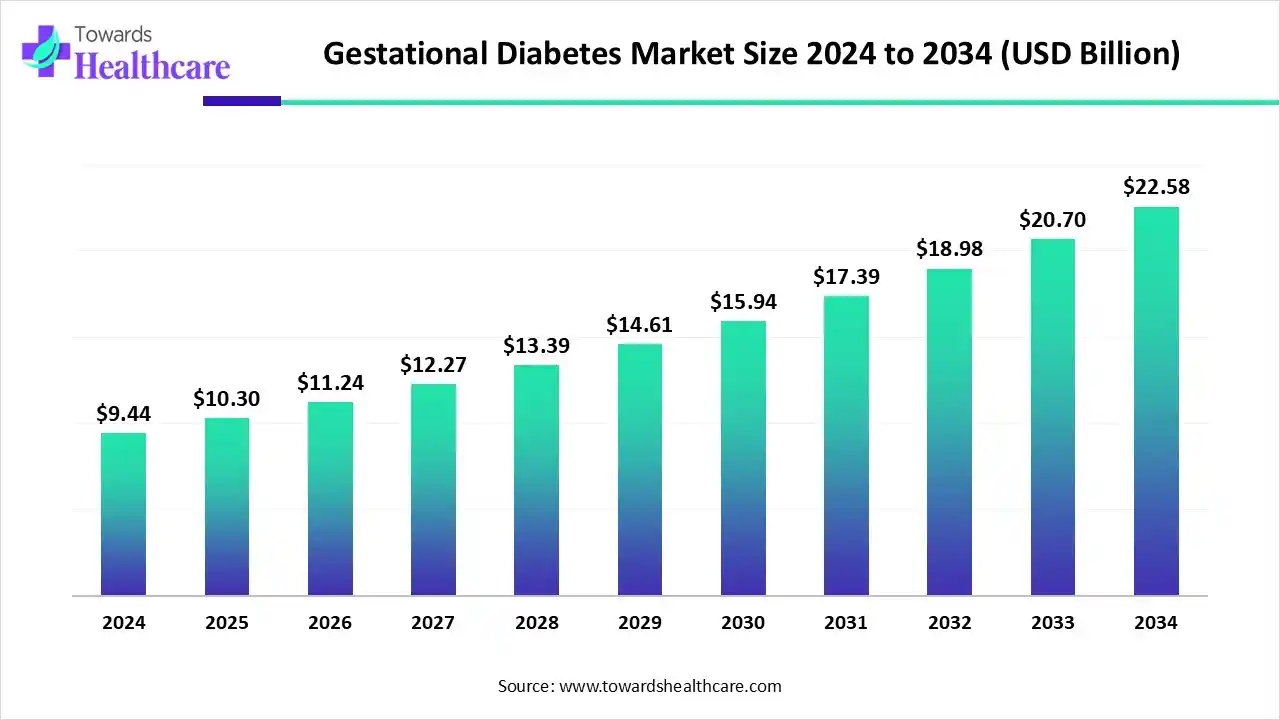

The global gestational diabetes market size is calculated at USD 10.3 billion in 2025, grew to USD 11.24 billion in 2026, and is projected to reach around USD 22.58 billion by 2034. The market is expanding at a CAGR of 9.15% between 2024 and 2034.

")

The gestational diabetes market is primarily driven by the increasing risk of gestational diabetes, especially in obese patients or those with a family history of diabetes. Government organizations launch initiatives to encourage pregnant women to undergo screening tests, thereby avoiding possible complications. Artificial intelligence (AI) revolutionizes the diagnosis and monitoring of gestational diabetes. Novel therapeutic innovations and effective management strategies drive the market’s future.

| Table | Scope |

| Market Size in 2025 | USD 10.3 Billion |

| Projected Market Size in 2034 | USD 22.58 Billion |

| CAGR (2025 - 2035) | 9.15% |

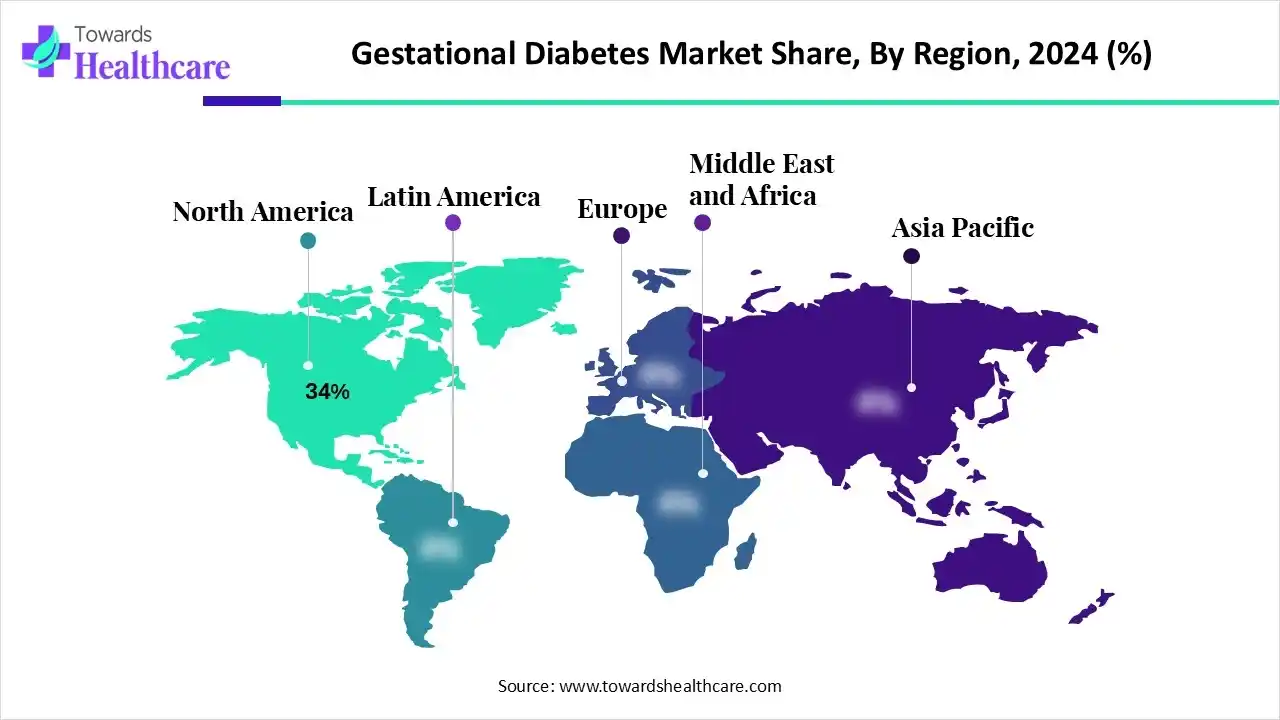

| Leading Region | North America by 34% |

| Market Segmentation | By Treatment Type, By Product/Drug Formulation, By Dosage Form/Delivery Device, By Diagnostic & Monitoring Method, By End-User/Care Provider, By Distribution Channel, By Region |

| Top Key Players | Novo Nordisk, Abbott Laboratories, F. Hoffmann-La Roche Ltd., Biocon Limited, Johnson & Johnson, Merck & Co., Inc., AstraZeneca plc, Boehringer Ingelheim GmbH, Becton, Dickinson and Company (BD), Ascensia Diabetes Care, Insulet Corporation, Tandem Diabetes Care, Inc., Ypsomed Holding AG, Thermo Fisher Scientific, Sun Pharmaceutical Industries Ltd., Nipro Diagnostics |

The gestational diabetes market is experiencing robust growth, driven by favorable screening programs, growing awareness of maternal-fetal risks, and technological innovations. It comprises products and services used to detect, monitor and manage glucose intolerance first identified during pregnancy, including screening and diagnostic tests (OGTT kits, point-of-care glucose tests), blood glucose monitoring devices (glucometers, test strips, continuous glucose monitors), therapeutics (insulins and approved oral agents used in pregnancy), digital/telehealth care and pregnancy-specific care programs, and related clinical services.

AI plays a crucial role in advancing gestational diabetes care, improving prediction, screening, and management. AI and machine learning (ML) algorithms facilitate early risk prediction, continuous glucose monitoring, and insulin-dosing recommendations. They analyze vast amounts of data and predict potential treatment outcomes for individual patients. They enhance the efficiency and accuracy of gestational diabetes diagnosis and treatment. Leveraging AI in telemedicine enables healthcare professionals to provide remote monitoring, eliminating the need for patients to visit healthcare organizations.

Which Treatment Type Segment Dominated the Gestational Diabetes Market?

The lifestyle & medical nutrition therapy (MNT) segment held a dominant presence in the market with a share of 45% in 2024, due to the growing demand for natural products and increasing awareness of a healthy lifestyle. Plant-based diets can improve insulin sensitivity and increase its secretion. Therapeutics derived from natural products also provide antioxidant effects. Regular exercise has also been proven to be beneficial.

Insulin Therapy

The insulin therapy segment is expected to grow at the fastest CAGR in the gestational diabetes market during the forecast period. Insulin therapy is beneficial in restoring glycemia in women with gestational diabetes. Ongoing efforts are made to evolve insulin analogs and study their long-term effects on maternal and child health.

Oral Anti-Diabetic Agents

The oral anti-diabetic agents segment is expected to grow at a notable rate. Metformin and sulfonylureas (glyburide) are the most widely prescribed anti-diabetic medications as they are comparatively safer and cost-effective. They have lower adverse effects, like pre-eclampsia and neonatal hypoglycemia.

How the Insulin Injectables Segment Dominated the Gestational Diabetes Market?

The insulin injectables segment held the largest revenue share of 40% in the market in 2024, due to the need for insulin therapy among pregnant women. Commercial prefilled pens, cartridges, and vials are available for patients, eliminating the need for skilled healthcare professionals for insulin delivery. The demand for insulin injectables is increasing as it is estimated that 15% to 30% of women require insulin therapy.

Glucose Monitoring Devices & Consumables

The glucose monitoring devices & consumables segment is expected to grow with the highest CAGR in the gestational diabetes market during the studied years. Government organizations encourage patients to monitor glucose during pregnancy at regular intervals. Advanced monitoring devices can also send real-time alerts to providers. This helps healthcare professionals to make proactive clinical decisions.

Oral Tablets

The oral tablets segment is expected to witness significant growth. Oral tablets are more cost-effective and easier to administer, enhancing patient convenience. They regulate blood glucose levels and can be used as alternatives to insulin.

Why Did the Prefilled Pens/Pen Cartridges Segment Dominate the Gestational Diabetes Market?

The prefilled pens/pen cartridges segment contributed the biggest revenue share of 45% in the market in 2024, due to advances in drug delivery systems and the increasing integration of advanced technologies. Prefilled pens/cartridges deliver insulin into the subcutaneous tissue. They are available in various forms, including disposable, reusable, and smart pens.

CGM Sensors/Consumables

The CGM sensors/consumables segment is expected to expand rapidly in the gestational diabetes market in the coming years. Sensors are embedded in CGM devices to accurately monitor blood glucose levels in pregnant women. The two different types of sensors include disposable and implantable sensors, which are inserted under the skin and placed inside the body, respectively.

Vials

The vials segment is expected to show lucrative growth in the coming years. Vials offer a more flexible dosing option, allowing healthcare professionals to provide tailored dosages. This is particularly useful for patients with fluctuating needs or specialized dosing instructions.

Which Diagnostic & Monitoring Method Segment Led the Gestational Diabetes Market?

The oral glucose tolerance test (OGTT) segment led the market with a share of 45% in 2024, due to the ability of the test to find problems with the way the body handles sugar after a meal. OGTT measures the body’s response to sugar. This test is usually conducted between 24 and 28 weeks of pregnancy.

CGM (Real-Time & Intermittent)

The CGM (real-time & intermittent) segment is expected to witness the fastest growth in the gestational diabetes market over the forecast period. CGM devices provide more precise and accurate results as they are measured in real-time. They help empower women to manage their diabetes during pregnancy, improving their pregnancy experience.

Self-Monitoring Blood Glucose (SMBG)

The self-monitoring blood glucose (SMBG) segment is expected to show notable growth over the upcoming years. People are becoming more aware of monitoring their blood glucose levels. SMBG during pregnancy is feasible and acceptable, improving maternal and neonatal health outcomes.

What Made Hospitals & Maternity Centers the Dominant Segment in the Gestational Diabetes Market?

The hospitals & maternity centers segment accounted for the highest revenue share of 40% in the market in 2024, due to the increasing number of patient admissions and the presence of skilled professionals. Skilled professionals provide multidisciplinary expertise to patients. Efforts are made to enhance accessibility to maternity care services across diverse geographical locations.

Home Care/Self-Management

The home care/self-management segment is expected to show the fastest growth in the gestational diabetes market over the forecast period. Home care and self-management of gestational diabetes include managing blood sugar through diet and regular exercise. Non-pharmacological treatment offers superior benefits, including fewer side effects, enhanced patient comfort, and long-term benefits.

Outpatient Clinics/Diabetes Clinics

The outpatient clinics/diabetes clinics segment is expected to show remarkable growth. The increasing number of dedicated clinics and the availability of specialized equipment boost the segment’s growth. Skilled professionals in outpatient clinics and diabetes clinics provide personalized care to patients.

How the Retail Pharmacies Segment Dominated the Gestational Diabetes Market?

The retail pharmacies segment held a major revenue share of 40% in the market in 2024, due to the availability of favorable infrastructure and suitable capital investments. Retail pharmacies offer numerous benefits, including free home delivery, 24/7 services, and special discounts.

Direct-to-Patient/Home Delivery

The direct-to-patient/home delivery segment is expected to account for the highest growth in the forecast period. Numerous e-commerce platforms, manufacturers, and retail pharmacies offer home delivery services to patients. This helps patients to order appropriate medications or devices in the comfort of their homes.

Hospital/Institutional Procurement

The hospital/institutional procurement segment is expected to grow significantly. Hospital/institutional procurement is essential as hospitals can provide advanced care to patients. The hospital procurement process covers various aspects, from the initial investment request from clinical staff to the final decision to purchase.

")

North America dominated the global market share by 34% in 2024. The availability of state-of-the-art research and development facilities, the presence of key players, and the increasing prevalence of gestational diabetes are the major factors that contribute to market growth in North America. Government organizations launch initiatives and provide funding to accelerate research related to gestational diabetes.

Key players, such as Eli Lilly and Company, Abbott Laboratories, and Johnson & Johnson, are the major contributors to the market in the U.S. The International Diabetes Federation (IDF) reported that the prevalence rate of gestational diabetes in the U.S. was 21.4% in 2024. The U.S. has a well-established clinical trial infrastructure, accounting for 259 studies related to gestational diabetes as of October 2025.

Asia-Pacific is expected to grow at the fastest CAGR in the market during the forecast period. The burgeoning healthcare sector and the growing research and development activities boost the market. Sedentary lifestyles and a family history of diabetes are the major risk factors for developing gestational diabetes in women living in the Asia-Pacific. Favorable screening programs and campaigns encourage pregnant women to screen for diabetes.

The Indian government is at the forefront of providing advanced maternal care through the “Pradhan Mantri Surakshit Matritva Abhiyaan (PMSMA)” initiative that aims to prevent maternal and newborn deaths and provide high-quality maternal care with dignity and respect. The program provides assured, comprehensive, and quality antenatal care, free of cost, universally to all pregnant women on the 9th of every month.

Europe is expected to grow at a notable CAGR in the gestational diabetes market in the foreseeable future. The increasing investments and the rising prevalence of gestational diabetes augment the market. According to a recent meta-analysis, the average prevalence rate of gestational diabetes in Europe is 10.9%. Favorable government support and increasing healthcare expenditure contribute to market growth. The growing awareness of maternal health enables healthcare professionals to provide early intervention.

The Scottish Government announced an additional funding of up to £8.8 million for diabetes technology to the Diabetes Scotland organization. The National Health Service (NHS) England recently launched the “artificial pancreas” initiative to offer an artificial pancreas to women with type 1 diabetes who are either pregnant or planning to become pregnant. The UK reported the third-highest prevalence rate of gestational diabetes in Europe, representing 23.1%.

The gestational diabetes market in South America is expanding steadily, supported by increasing maternal health awareness, improved diagnostic access, government-led prenatal screening initiatives, and rising adoption of digital glucose monitoring and nutrition management solutions across Brazil, Argentina, and Chile.

In Brazil, the gestational diabetes landscape is increasingly visible, with recent national data estimating a prevalence of around 14 % among pregnant women. Driven by rising maternal age, obesity, and the expansion of prenatal screening programs, care efforts are scaling to engage education, digital monitoring tools, and integrated nutrition-and-exercise support across public and private maternity services.

The Middle East & Africa are considered to be a significantly growing area in the gestational diabetes market, due to the increasing adoption of advanced technologies and the growing risk of obesity, which propels market growth. People are becoming aware of the early detection and management of gestational diabetes. Several government and private organizations conduct seminars and conferences to share the latest updates about diabetes monitoring and management in pregnant women.

The Egyptian government announced that approximately 7 million Egyptians have undergone medical examinations as part of the Pre-Marriage Health Screening and Caring for the Health of Mothers and Newborns initiatives since February 2023. The government also formed an initiative to improve maternal and child health through a new mobile app.

SWOT Analysis

Recent News and Updates

Announced job cuts of about 9,000 employees (~11% of workforce) to save ~DKK 8 billion by end-2026 amid competitive pressure in the obesity market. Also announced a major licensing deal worth up to US$2.1 billion with biotech Omeros Corporation for the MASP-3 inhibitor in rare diseases.

Industry Recognitions / Awards

Recognized widely for innovation in diabetes/obesity care and leadership in metabolic disease therapeutics.

SWOT Analysis

Recent News and Updates

In July 2025, Abbott’s stock dropped over 8% after it cut its full-year revenue growth guidance to 7.5-8.0% due to headwinds in China's diagnostic volumes. In October 2025, analysts at UBS and Benchmark reiterated Buy ratings, highlighting strong MedTech growth and solid fundamentals.

Press Releases

Q1 2025 results (April) announced ~ US$1.7 billion CGM revenue growth and full-year guidance reaffirmed. Q3 2025 results (October) posted 6.9% sales growth and reaffirmed full-year guidance.

Industry Recognitions / Awards

Frequently recognized for innovation and strong device/technology leadership in diabetes care and medical devices.

Read Further how top manufacturers are transforming the global Gestational Diabetes market: https://www.towardshealthcare.com/companies/gestational-diabetes-companies

By Treatment Type

By Product/Drug Formulation

By Dosage Form/Delivery Device

By Diagnostic & Monitoring Method

By End-User/Care Provider

By Distribution Channel

By Region

Principal Consultant

Rohan Patil is a seasoned market research professional with over 5+ years of focused experience in the healthcare sector, bringing deep domain expertise, strategic foresight, and analytical precision to every project he undertakes.

Learn more about Rohan Patil

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar