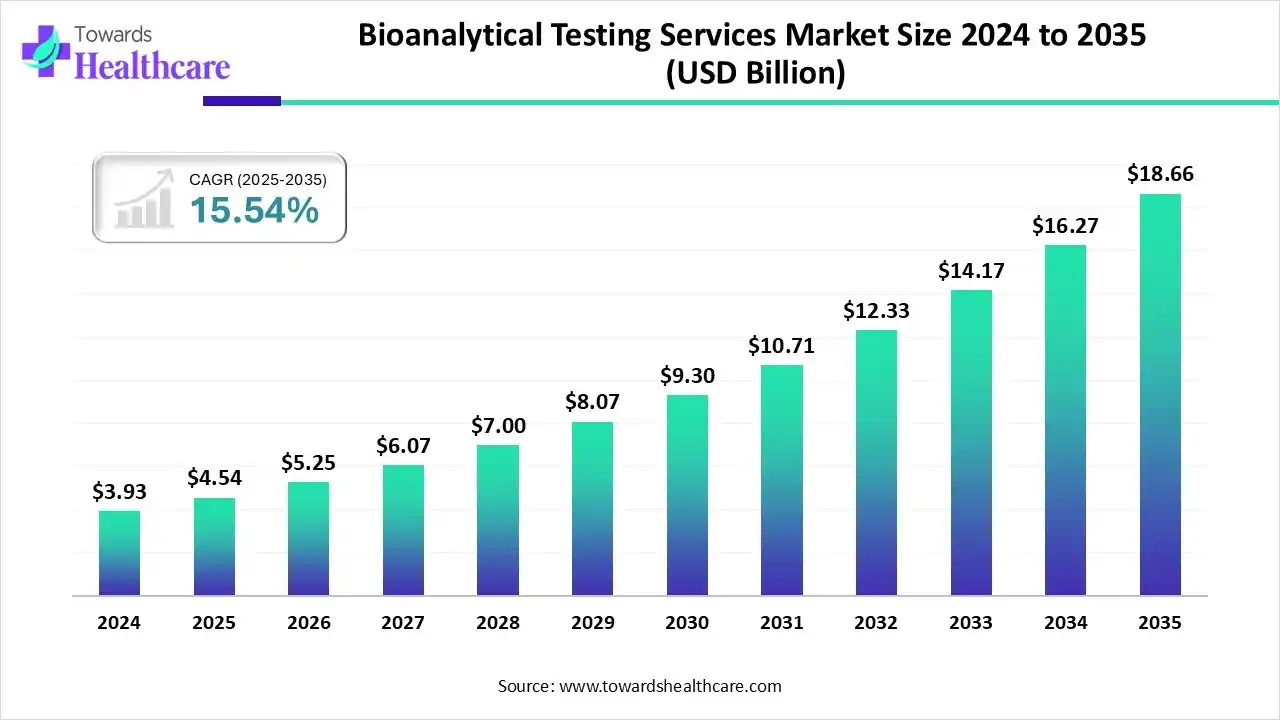

The global bioanalytical testing services market size is calculated at USD 4.54 billion in 2025, grew to USD 5.25 billion in 2026, and is projected to reach around USD 18.66 billion by 2035. The market is expanding at a CAGR of 15.54% between 2026 and 2035.

The bioanalytical testing services market is primarily driven by growing research and development activities and stringent regulatory policies. The growing awareness of the significance of bioanalytical testing potentiates its demand. Increasing R&D investments and the rising complexity of therapeutics boost the market. Artificial intelligence (AI) automates the testing procedures to enhance accuracy and reduce the timelines. Technological innovations, such as ultra-high-performance liquid chromatography (UHPLC) and next-generation sequencing, drive the future of bioanalytical testing services.

The bioanalytical testing services market is experiencing robust growth, driven by growing drug discovery and development research, technological innovations, and the increasing number of preclinical and clinical trials. It encompasses services for the identification and quantification of drugs and metabolites in biological matrices, including blood, plasma, serum, cerebrospinal fluid, saliva, and urine.

Bioanalytical testing data help researchers move their drug development program from discovery to investigational new drug (IND) submission and beyond. They are applied in discovery, preclinical, and clinical stages. Bioanalytical testing is conducted for various applications, such as chromatographic bioanalysis, molecular biology, immunology, biomarkers, and non-GLP discovery bioanalysis.

Bioanalytical testing services involve the quantitative and qualitative analysis of drugs, metabolites, biomarkers, and biological samples to support drug discovery, preclinical studies, clinical trials, and regulatory approvals. The bioanalytical testing services market is expanding due to the increasing development of biologics, biosimilars, and personalized medicines, coupled with rising clinical trial activities worldwide. Growing outsourcing by pharmaceutical and biotechnology companies to specialized contract research organizations is further accelerating demand. A key trend is the integration of AI-driven data analysis, laboratory automation, and high-resolution analytical technologies such as LC-MS/MS and next-generation sequencing, improving testing accuracy and efficiency. Future opportunities lie in cell and gene therapy bioanalysis, decentralized clinical trials, and companion diagnostics. Additionally, stringent regulatory requirements, increasing investments in pharmaceutical R&D, and the growing focus on biomarker-based drug development continue to drive sustained market growth.

AI introduces automation in bioanalytical testing services, enabling service providers to perform multiple experiments simultaneously, at a faster rate and with greater precision. Integrating AI and machine learning (ML) algorithms in analytical instruments reduces manual errors and enhances accuracy. AI-enabled robots ensure superior quality control, including visual assessments and high reproducibility. This leads to enhanced productivity and service quality for clients. Thus, AI and ML have been instrumental in achieving remarkable outcomes in analytical testing.

| Month, Year | Company | Collaborator | Purpose |

| June, 2025 | Emery Pharma | Fortrea | To provide rapid testing of rifampin for impurities and conduct drug-drug interaction studies |

| March, 2025 | Emery Pharma | Centivax | To leverage Emery’s expertise in developing an IND-enabling GLP-compliant potency release assay for GMP batches of the Centivax pan-influenza vaccine, Centi-Flu |

| October, 2025 | AstraZeneca BioVenture Hub | PPD | To enhance R&D using chromatography, molecular genomics, and proteomics to drive innovation and strengthen the life science ecosystem |

| May, 2024 | KCAS Bio | Crux Biolabs | To provide harmonized spectral flow cytometry across the U.S., Europe, and Australia to support the global needs of clinical research |

| Table | Scope |

| Market Size in 2026 | USD 5.25 Billion |

| Projected Market Size in 2035 | USD 18.66 Billion |

| CAGR (2026 - 2035) | 15.54% |

| Leading Region | North America |

| Historical Data | 2020 - 2023 |

| Base Year | 2025 |

| Forecast Period | 2026 - 2035 |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Molecule, By Test, By Workflow, By End-Use, By Region |

| Top Key Players | BioAgilytix, Eurofins Scientific, Precision for Medicine, Illumina, Bio-Rad Laboratories, Altasciences, QPS, SpinoS Life Science, IntoxLab, Thermo Fisher Scientific, Syneos Health |

")

| Segments | Shares % |

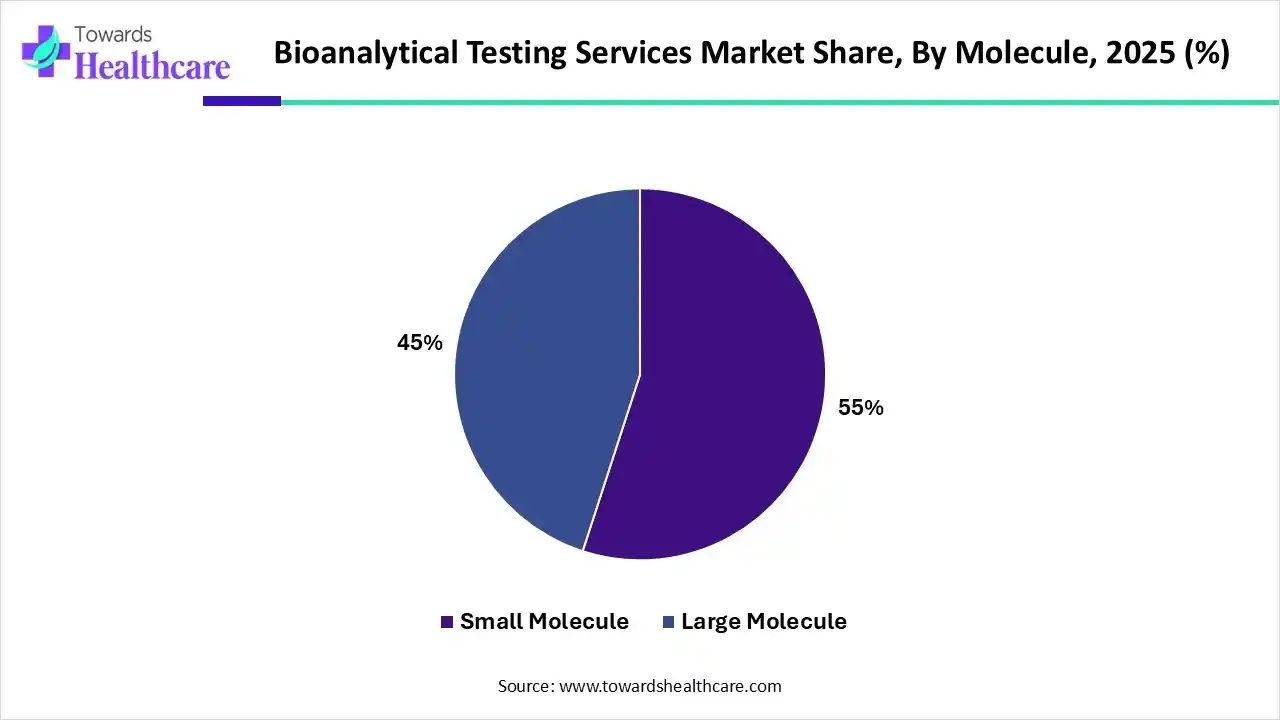

| Small Molecule | 55% |

| Large Molecule | 45% |

Explanation

Which Molecule Segment Dominated the Bioanalytical Testing Services Market?

The small molecule segment held a dominant presence in the market by 55% in 2025, due to the growing demand for small-molecule drugs and the need to assess the ADMET properties of small molecules. The development of small-molecule drugs does not require complex research pathways, allowing researchers to create more such drug candidates. Bioanalytical testing is essential for small molecules to analyze their DMPK profile from discovery, preclinical, GLP toxicology, and clinical studies.

Large Molecule

The large molecule segment is expected to grow at the fastest CAGR in the market during the forecast period. Large molecules or biologics offer superior benefits compared to small-molecule drugs, such as targeted treatment and reduced systemic side effects. They undergo complex pathways and require specialized equipment for their development and testing. As more and more large-molecule products are being developed, large-molecule bioanalysis has become increasingly more common.

| Segments | Shares % |

| Bioavailability | 40% |

| Bioequivalence | 30% |

| ADME | 10% |

| Pharmacokinetics (PK) | 7% |

| Pharmacodynamics (PD) | 4% |

| Biomarker Testing | 3% |

| Cell-based Assay | 4% |

| Virology Testing | 2% |

| Other Tests | 0% |

Explanation

Why Did the Bioavailability Segment Dominate the Bioanalytical Testing Services Market?

The bioavailability segment held the largest revenue share of the market in by 40% 2025, due to the need for the development of more efficacious and potent drugs. Bioavailability (BA) refers to the rate and extent to which the active ingredient is absorbed from the drug product and distributed to the site of action. BA testing is essential in the development phase to reveal disadvantageous properties and the possible technological interventions. This enables researchers to modify the properties of drugs and develop more effective products.

Bioequivalence

The bioequivalence segment is expected to grow with the highest CAGR in the market during the studied years. Bioequivalence (BE) refers to the study of the rate and extent to which an active substance of pharmaceutical equivalents reaches the target site. The growing demand for generic drugs and biosimilars potentiates their development. As of October 2025, the U.S. Food and Drug Administration (FDA) has approved 76 biosimilars for different indications.

ADME

The ADME segment is expected to grow at a notable CAGR. Absorption, distribution, metabolism, and excretion (ADME) properties are essential to determine at the early stage of drug development. ADME properties can be determined either through in silico, in vitro, or in vivo procedures. Poor ADME properties are estimated to account for 40% of drug failures in clinical trials. Thus, regulatory agencies necessitate researchers to provide ADME data for drug approval.

| Segment | Share 2025 (%) |

| Sample Analysis | 50% |

| Sample Collection and Preparation | 30% |

| Other Processes | 10% |

| Method Development and Validation | 10% |

Explanation

How the Sample Analysis Segment Dominated the Bioanalytical Testing Services Market?

The sample analysis segment contributed the biggest revenue share of the market by 50% in 2025. This segment dominated because sample analysis is the most vital step in bioanalytical testing. Sample analysis is of prime importance during preclinical and clinical testing. The availability of advanced technologies, such as automation, simplifies data analysis for researchers. AI and ML reduce manual errors in sample analysis and lead to higher accuracy results.

Sample Collection and Preparation

The sample collection and preparation segment is expected to expand rapidly in the market in the coming years. Sample collection and preparation involve careful, standardized processes for collecting biological matrices. Samples are also required to be transported and stored properly to maintain analyte stability. Sample preparation is considered the bottleneck step, as the biological matrix has its own unique challenges and complexity.

Method Development and Validation

The method development and validation segment is expected to grow significantly. Method development and validation aim to ensure that the methods used to measure the identity, purity, potency, and stability of drugs are accurate, precise, and reliable. This is a crucial step to determine that the procedures and tests evaluate the method’s performance characteristics. Moreover, it also assists researchers in selecting appropriate analytical techniques.

| Segments | Shares % |

| Pharma & Biopharma Companies | 60% |

| CDMO | 15% |

| CRO | 20% |

| Others | 5% |

Explanation

Which End-Use Segment Led the Bioanalytical Testing Services Market?

The pharma & biopharma companies segment led the market by 60% in 2025, due to the availability of a favorable infrastructure and suitable capital investments. Capital investments enable companies to purchase advanced equipment and expand their infrastructure. Numerous pharma & biopharma companies offer bioanalytical testing services through their in-house facilities, thereby generating more revenue. Pharma & biopharma companies work on multiple projects simultaneously, necessitating them to outsource their services.

CRO

The CRO segment is expected to witness the fastest growth in the market over the forecast period. Contract research organizations (CROs) have desirable facilities and equipment to provide specialized laboratory services, including method development, transfer, qualification, validation, and sample analysis. CROs provide these services under stringent regulatory guidelines to ensure data accuracy and reliability for regulatory submissions.

CDMO

The CDMO segment is expected to grow in the coming years. Contract development and manufacturing organizations (CDMOs) specialize in the research and manufacturing of drug candidates. They ensure drug stability, safety, and efficacy throughout the entire drug development and manufacturing process.

North America dominated the global market in 2025. The availability of state-of-the-art research and development facilities, a strong presence of pharmaceutical and biotech companies, and favorable regulatory support are the major growth factors of the market in North America. Government organizations actively support biotech research through funding and initiatives. Companies from North America aim to become global leaders in drug development and serve a larger patient population.

U.S.: The Powerhouse of Pharma Innovation

The U.S. is home to over 5,000 pharmaceutical companies and more than 3,000 biotech companies. This increases the development of novel drugs, especially biologics and cell & gene therapies, requiring bioanalytical testing services. The increasing number of new drug approvals also propels the market. In 2024, the FDA approved 50 new drugs, and as of October 2025, it approved 34 new drugs.

Canada Emerges as a High-Growth Hub for Bioanalytical Testing Services

Canada's bioanalytical testing services market is witnessing significant growth due to its robust pharmaceutical and biotechnology ecosystem, expanding clinical research activities, and strong government support for life sciences innovation. Increasing investments in biologics, biosimilars, precision medicine, and cell and gene therapy are driving demand for advanced bioanalytical testing. Additionally, the adoption of cutting-edge analytical technologies and regulatory-compliant testing services is strengthening the country's position as a leading bioanalytical research hub.

Asia-Pacific is expected to grow at the fastest CAGR in the market during the forecast period. The burgeoning biopharmaceutical sector and the increasing demand for new drug discovery boost the market. The growing awareness of personalized medicines, driven by rapidly changing demographics, promotes the development of novel drugs. China and India encourage foreign direct investments (FDI) in the biotech fields. They also have suitable infrastructure, enabling foreign companies to set up their testing facilities in the Asia-Pacific countries.

Global Capital Fuels India’s Pharma Growth

The FDI inflow for the pharmaceutical sector in India has rapidly evolved over the last decade. Approximately 3% of the total FDI inflow is related to the pharma sector. In 2024, the FDI inflow was Rs 7,500 crore. In February 2025, India hosted the 9th International Symposium on Current Trends in Drug Discovery Research at CSIR-Lucknow to focus on international cooperation, quantum computing, and AI to accelerate drug discovery.

China Strengthens Its Position in Bioanalytical Testing Services

China's bioanalytical testing services market is growing notably due to rapid expansion of its pharmaceutical and biotechnology industries, increasing drug discovery and clinical trial activities, and rising investments in innovative biologics. Government support for biopharmaceutical development, expanding contract research organizations (CROs), and the adoption of advanced analytical technologies are enhancing testing capabilities, making China a key destination for global bioanalytical research and development.

Europe is expected to grow at a significant CAGR in the upcoming period. The presence of key players and the rising adoption of advanced technologies augment the market. The growing collaboration among key players to leverage advanced technologies and develop novel products contributes to market growth. Countries like Germany, the UK, and France are at the forefront of expanding their research and clinical trial infrastructure, opening doors for numerous opportunities for foreign researchers.

Key Players Powering Innovation in the UK

Key players, such as Chimera Biotec GmbH, Intertek, and SGS United Kingdom, provide bioanalytical testing services in the UK. The UK ranks second for share of government spending on health R&D and joint third for charitable R&D funding. The Department for Science, Innovation, and Technology (DSIT) recently announced an investment of £55 billion for R&D, improving lives and growing the UK’s economy.

UK Expands as a Leading Bioanalytical Testing Services Hub

The UK bioanalytical testing services market is expanding notably due to its strong clinical research infrastructure, growing biopharmaceutical innovation, and increasing investments in precision medicine and advanced therapeutics. The presence of leading contract research organizations (CROs), collaborations between academia and industry, and the adoption of advanced analytical technologies are enhancing bioanalytical capabilities, positioning the UK as a key center for global drug development and clinical research.

South America: Strengthening Clinical Research Infrastructure

South America’s bioanalytical testing market grows as governments modernize research facilities, expand public–private clinical programs, and adopt GLP-certified labs to support rising drug discovery, pharmacokinetic studies, and regulatory-compliant testing capabilities region-wide.

Brazil: National Drive for Advanced Bioanalysis

Brazil’s growing pharmaceutical R&D investments and ANVISA’s accelerated drug-approval reforms are fueling demand for validated assays, biomarker quantification, and biosimilar characterization through local CROs and newly established bioanalytical laboratories.

Germany Accelerates Innovation in Bioanalytical Testing Services

Germany's bioanalytical testing services market is growing significantly due to its strong pharmaceutical manufacturing base, advanced life sciences research, and increasing investments in biologics and precision medicine. Rising demand for high-quality bioanalytical testing in clinical trials, supportive regulatory standards, and the adoption of advanced analytical platforms are strengthening the country's role as a leading European hub for drug development and bioanalysis.

The Middle East and Africa witness rapid bioanalytical expansion, propelled by government-funded biotech parks, WHO-backed vaccine projects, and regional initiatives enhancing bioequivalence testing, immunogenicity assessments, and pharmaceutical quality-control networks.

GCC: Strategic Biotech and CRO Partnerships

GCC nations boost bioanalytical testing via national biotech strategies, Saudi Arabia’s Vision 2030 healthcare goals, and UAE partnerships with global CROs establishing advanced labs for biologics, biosimilars, and clinical-trial analysis.

Company Overview : Charles River Laboratories is a leading global contract research organization (CRO) providing essential products and services to help pharmaceutical, biotechnology, medical device companies, and academic/government institutions accelerate their research and drug development efforts. It is a full-service, early-stage CRO.

Corporate Information (Headquarters, Year Founded, Ownership Type)

Key Milestones/Timeline

Business Segments/Divisions

Key Offerings

End-Use Industries Served

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Continued strategic focus on integrated service models, offering clients end-to-end support from discovery to commercial manufacturing.

Product Launches/Innovations

Capacity Expansions/Investments

Regulatory Approvals

Maintains key global accreditations and compliance standards, including FDA and EMA compliance, and AAALAC International Accreditation.

Distribution channel strategy

Primarily direct sales through dedicated global sales and scientific teams, emphasizing integrated, end-to-end solutions, particularly for early-stage development clients.

Technological Capabilities/R&D Focus

Core Technologies/Patents

Research & Development Infrastructure

Extensive global network of state-of-the-art research and testing facilities.

Innovation Focus Areas

Competitive Positioning

Strengths & Differentiators

Market Presence & Ecosystem Role

SWOT Analysis

Recent News and Updates

Press Releases

Industry Recognitions/Awards

Information not explicitly found in recent, concise news snippets, but generally recognized as a leading global CRO.

Company Overview: Labcorp Drug Development, formerly Covance, is a global contract research organization providing a full suite of drug development services, from preclinical testing and clinical trials to commercialization. It is a key segment of the larger Labcorp life sciences company.

Key Milestones/Timeline

Business Segments/Divisions

Key Offerings

End-Use Industries Served

Key Developments and Strategic Initiatives

Mergers & Acquisitions

Partnerships & Collaborations

Product Launches/Innovations

Capacity Expansions/Investments

Regulatory Approvals

Distribution channel strategy

Leverages its extensive network of patient-service centers and laboratories for diagnostics, while the Drug Development segment utilizes a direct sales model for CRO services to biopharma clients.

Technological Capabilities/R&D Focus

Core Technologies/Patents

Research & Development Infrastructure

Extensive global laboratory infrastructure, including its central lab and specialized testing facilities.

Innovation Focus Areas

Competitive Positioning

Strengths & Differentiators

Market presence & ecosystem role

SWOT Analysis

Recent News and Updates

Press Releases

Industry Recognitions/Awards

Information not explicitly found in recent, concise news snippets, but generally recognized as a global leader in laboratory and drug development services.

Top Companies & Their Offerings in the Bioanalytical Testing Services Market

By Molecule

By Test

By Workflow

By End-Use

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar