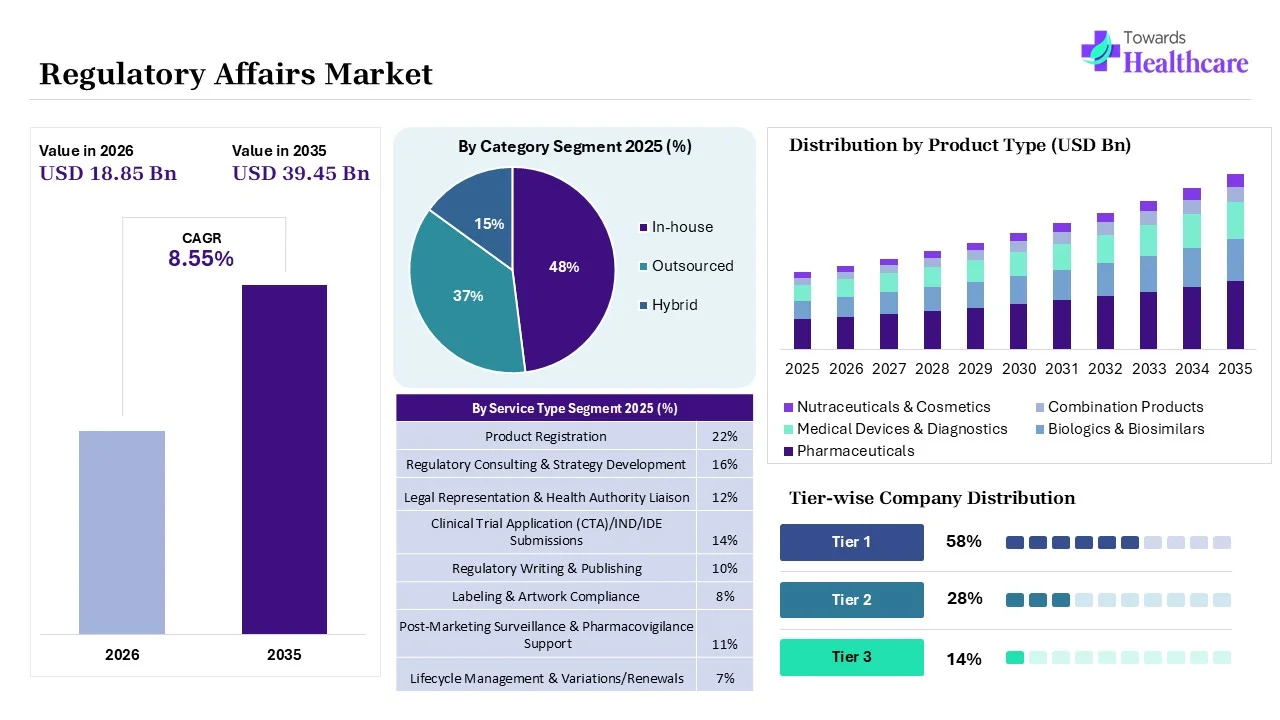

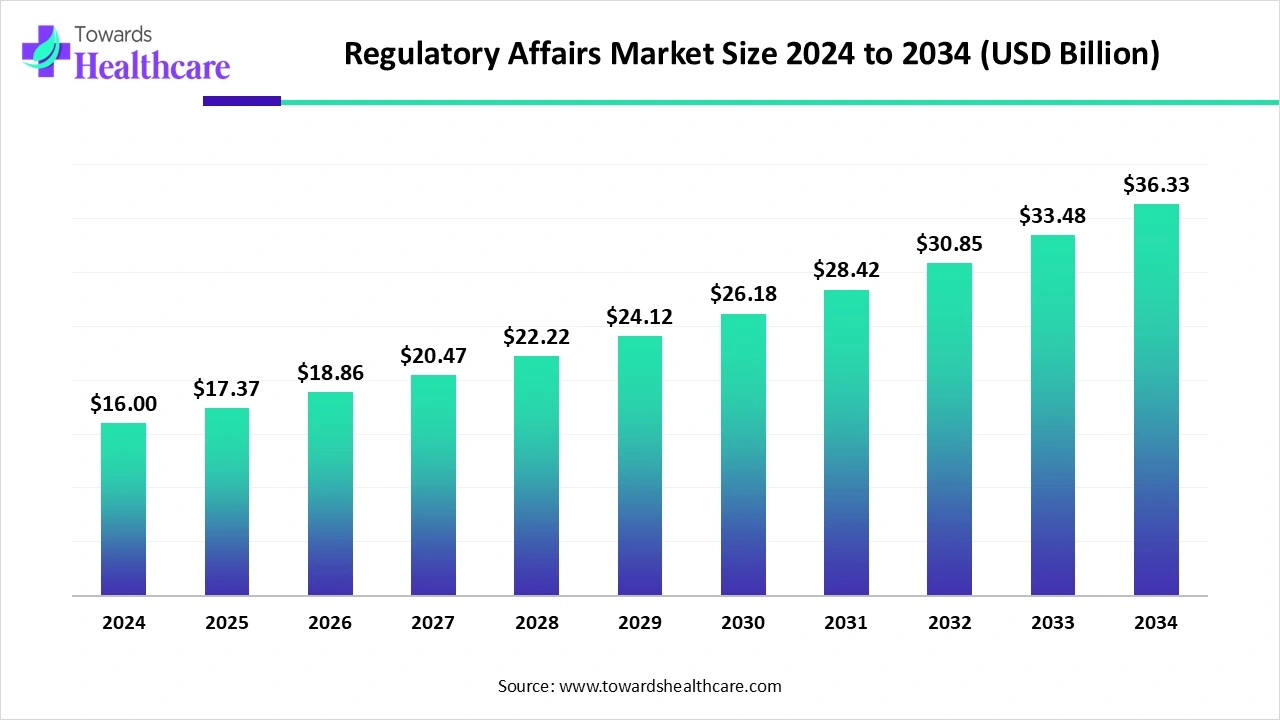

The global regulatory affairs market size is calculated at US$ 17.37 billion in 2025, grew to US$ 18.85 billion in 2026, and is projected to reach around US$ 39.45 billion by 2035. The market is expanding at a CAGR of 8.55% between 2026 and 2035.

")

An aging population is experiencing a huge burden of chronic and rare diseases, like cancers, diabetes, and neurological issues, which are boosting the development of drug molecules and personalized treatments. This further expands the emergence of a strong regulatory landscape for monitoring, evaluating the safety, efficacy of these evolving drugs. The regulatory affairs market is imposing the widespread adoption of digital solutions, like AI tools and other cloud-based software for faster and efficient regulatory submissions to agencies, like the FDA &EMA.

The regulatory affairs market encompasses professional services, technology platforms, and outsourced solutions that support pharmaceutical, biotechnology, and medical device companies in complying with evolving health authority regulations worldwide. This market covers activities across clinical development, product registration, labeling, lifecycle management, and post-marketing compliance. Offerings include in-house functions, outsourced consulting and CRO partnerships, and software platforms for regulatory information management (RIM). The market is driven by stringent regulatory frameworks, global harmonization needs, faster drug/device approvals, and increasing reliance on digital systems for compliance documentation and submissions.

Diverse pharmaceutical and biopharmaceutical companies are focusing on R&D enhancements, expansion of their facilities is fueling the respective market growth.

Currently, AI-powered approaches are playing a crucial role in diverse markets, including the regulatory affairs sector. Nowadays, researchers are applying generative AI for intelligent assistants and regulatory co-pilots for automating documentation and submissions, boosting Regulatory Intelligence (RI) by aligning with real-time data and trends. This further allows more effective and proactive compliance monitoring.

For instance,

Regulatory affairs is the discipline responsible for ensuring that pharmaceuticals, biotechnology products, medical devices, and other healthcare products comply with national and international regulatory requirements throughout their lifecycle. The regulatory affairs market is expanding due to increasing product approvals, evolving global regulatory frameworks, and the growing complexity of healthcare innovations. Advancements in AI-driven regulatory intelligence, cloud-based Regulatory Information Management (RIM) systems, predictive analytics, automated dossier preparation, and digital compliance platforms are transforming regulatory operations.

Future opportunities are driven by global regulatory harmonization, increasing adoption of real-world data and evidence in submissions, and the expansion of digital health and advanced therapies requiring specialized regulatory expertise. Rising outsourcing of regulatory services, growing investments in compliance technologies, and continued innovation in electronic submission are further accelerating market growth, enabling organizations to streamline approvals, improve compliance efficiency, and accelerate product commercialization across global markets.

The regulatory affairs market is influenced by a combination of internal and external factors. Internally, advancements in Regulatory Information Management (RIM) systems, AI-powered regulatory intelligence, electronic submissions (eCTD), automation of compliance workflows, skilled regulatory professionals, and robust quality management systems are enhancing operational efficiency and accelerating product approvals. Externally, evolving global regulatory frameworks, increasing pharmaceutical and medical device innovation, rising demand for faster product commercialization, expanding clinical research, and regulatory harmonization initiatives are driving market growth. However, changing compliance requirements, regional regulatory variations, lengthy approval timelines, and increasing documentation complexity continue to present key challenges for industry stakeholders.

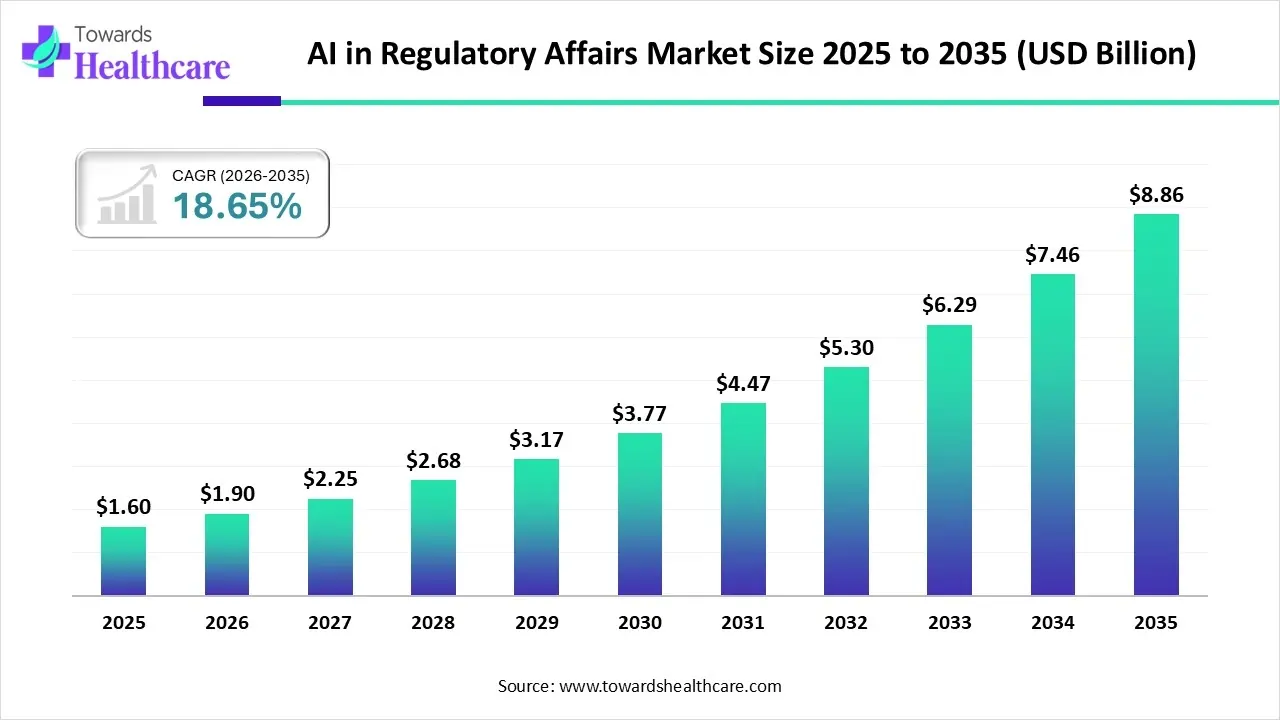

The global AI in regulatory affairs market size is calculated at US$ 1.6 in 2025, grew to US$ 1.9 billion in 2026, and is projected to reach around US$ 8.86 billion by 2035. The market is expanding at a CAGR of 18.65% between 2026 and 2035.

")

Driver

Emerging Demand and Regulatory Framework

Day by day, the pharma area is transforming due to several ongoing advances, such as AI-powered drug development, digital health, and customized medicine, which further merge with newer regulatory complexities. So this raises wider investments in regulatory professionals and overall regulatory affairs market services. Alongside, developing companies, like small and mid-sized ones, are highly demanding for outsourcing regulatory affairs, which facilitates specialized professionals, lowers expenses, and maintains focus on core business activities. Consistent modifications in regulatory frameworks and guidelines around various areas and for numerous product types are boosting demand for regulatory intelligence and expertise.

Restraint

QC and Intellectual Property Issues

The growing requirements in regulatory affairs outsourcing are facing barriers regarding the preservation of their proprietary information and intellectual property. Also, the market has been impacted by the need for maintenance of continuous quality control and adherence among outsourcing partners for all regulatory standards, which possibly results in non-compliance.

Opportunity

Regulatory Harmonization in Dx and Blockchain Technology

The worldwide rise of digitization is mainly fueling the emergence of newer regulatory requirements in the coverage of digital therapeutics (Dx). Along with this, the regulatory affairs market will have revolutionary opportunities in mobile health apps and remote monitoring tools to improve their safety, efficacy, and data security. Additionally, innovations in blockchain technology will enable ensuring the traceability and security of clinical data throughout the drug development process. Furthermore, harmonized regulatory landscapes will be helpful in approving tailored medicines that are customized to individual genetic markers.

| Table | Scope |

| Market Size in 2026 | USD 18.85 Billion |

| Projected Market Size in 2035 | USD 39.45 Billion |

| CAGR (2026 - 2035) | 8.55% |

| Leading Region | North America |

| Key Applications | Regulatory submissions (eCTD, IND, NDA, MAA), labeling compliance, pharmacovigilance integration, regulatory intelligence, lifecycle management, compliance tracking |

| Primary End Users | Pharmaceutical companies, biotech firms, medical device manufacturers, CROs, CDMOs, regulatory consultants |

| Key Growth Drivers | Increasing global drug approvals, regulatory complexity, globalization of clinical trials, digital transformation in pharma, AI-driven regulatory intelligence |

| Measurable Values | USD Millions/Units/Volume |

| Market Segmentation | By Service Type, By Category, By Product Type, By End-User/Client Segment, By Delivery Mode/Technology Enablement, By Region |

| Top Key Players | Accenture, ArisGlobal, Bioclinica, Certara, Charles River Associates, Covance, Deloitte, Freyr Solutions, ICON plc, IQVIA, Parexel International, PharmaLex, ProPharma Group, PPD, Veeva Systems |

| Segments | Shares % |

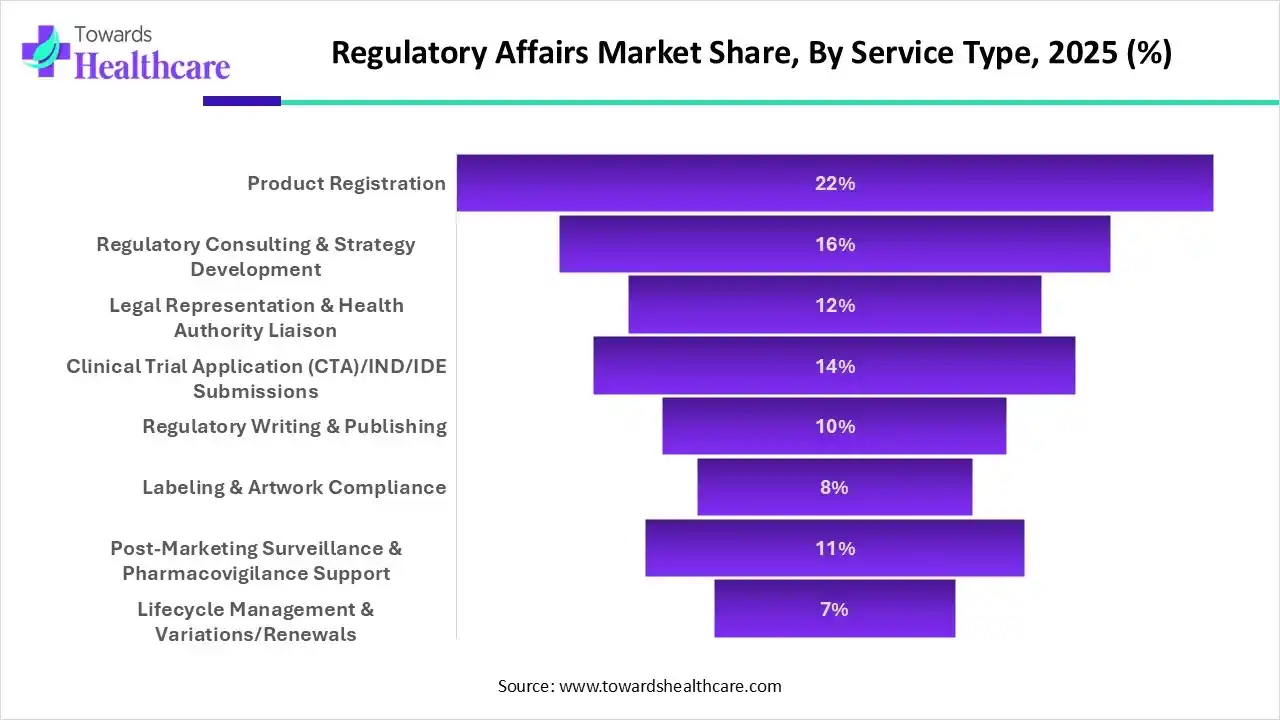

| Product Registration | 22% |

| Regulatory Consulting & Strategy Development | 16% |

| Legal Representation & Health Authority Liaison | 12% |

| Clinical Trial Application (CTA)/IND/IDE Submissions | 14% |

| Regulatory Writing & Publishing | 10% |

| Labeling & Artwork Compliance | 8% |

| Post-Marketing Surveillance & Pharmacovigilance Support | 11% |

| Lifecycle Management & Variations/Renewals | 7% |

")

Which Service Type Held a Major Share of the Regulatory Affairs Market in 2025?

The product registration segment dominated with the biggest share of the market by 22% in 2025. The segment is driven by the accelerating clinical trials, especially for new biologics and gene therapies, and more drug approvals are enhancing the requirements for regulatory submissions and market authorization. In this era, the growing applications of AI and ML in regulatory operations to simplify submissions and analysis, along with an emphasis on regional regulatory harmonization, are propelling the segmental developments. Also, consistent post-market surveillance is assisting in ensuring ongoing compliance.

Moreover, the post-marketing surveillance & pharmacovigilance support segment is estimated to witness the fastest expansion. Developing novel drug molecules is propelling the efforts in the detection of rare adverse events, the growth of regulatory bodies' requirements, and escalating patient populations with complex comorbidities are supporting the push in PMS. These robust PMS/PV services necessitate strong coordination among regulatory affairs, manufacturing, and other departments, along with higher engagement with healthcare providers and consumers, which helps the comprehensive collection and reporting of safety information.

| Segments | Shares % |

| In-house Regulatory Affairs Departments | 48% |

| Outsourced | 37% |

| Hybrid | 15% |

How did the In-House Regulatory Affairs Departments Segment Lead the Market in 2025?

In 2025, the in-house regulatory affairs departments segment accounted for the largest share of 48% share of the regulatory affairs market by 48%. The segment is fueled by the establishment of internal teams by highly developed companies for managing complex and high-stakes submissions, including BLAs and INDs, ensuring feasible integration with R&D and clinical departments. Global companies are stepping into structured, electronic submissions, which streamlines monitoring, updating, and reviewing documents with lower time and expenditures.

And, the outsourced segment is predicted to expand rapidly during 2026-2035. The combination of factors, like the expanding oncology developments, widespread digital transformations, is fueling the effective outsourcing approaches. Currently, the raised focus on strategic, end-to-end partnerships with Contract Development and Manufacturing Organizations (CDMOs) and Contract Research Organizations (CROs) which are propelled by spending pressures, the growth of biologics and injectables, and the integration of digital technologies.

| Segments | Shares % |

| Pharmaceuticals (Small Molecules) | 39% |

| Biologics & Biosimilars | 24% |

| Medical Devices & Diagnostics | 21% |

| Combination Products | 9% |

| Nutraceuticals & Cosmetics | 7% |

Which Product Type Dominated the Regulatory Affairs Market in 2025?

The pharmaceuticals segment captured the dominant share of the market by 39% in 2025. Across the globe, there is a huge burden of chronic illness cases, particularly cancers, heart issues, and diabetes are boosting the development of novel treatments with a robust regulatory landscape. Involvement of complexities of small molecules strongly emphasizes deeper CMC (Chemistry, Manufacturing, & Controls) data, which comprises impurity determination, stability studies, and method validation, to meet global standards. Ongoing expiration of patents of branded molecules is introducing new opportunities in the progress and sale of inexpensive generic small molecule drugs.

Whereas the biologics & biosimilars segment is estimated to expand rapidly in the coming era. Primarily, the expanding healthcare expenditures and the need for highly cost-effective treatments are driving the demand for biosimilars, which give more comparable versions of reference biologics at an affordable price. A wide range of efforts by regulatory bodies, mainly the FDA, are involved in the increasing number of approvals of biosimilars, coupled with the acquisition of interchangeability designations, enabling them to be automatically substituted for the reference product.

| Segments | Shares % |

| Large Multinational Pharmaceutical & Biotech Companies | 44% |

| Mid-sized Pharma/Biotech | 21% |

| Start-ups & Emerging Biopharma | 15% |

| Medical Device & Diagnostics Firms | 13% |

| CROs & CMOs | 7% |

How did the Large Multinational Pharmaceutical & Biotech Companies Segment Lead the Market in 2025?

The large multinational pharmaceutical & biotech companies segment held a major share of 44% of the regulatory affairs market by 44% in 2025. Nowadays, the pharmaceutical hub is focusing on enhancing patient safety and highly efficacious treatments for rare diseases (orphan drugs) and other specialty therapies, which drives the requirements for specialized regulatory assistance to meet unique demands. A significant emphasis on cybersecurity of emerging devices, including pacemakers and insulin delivery systems, which utilize cloud and Bluetooth, regulatory affairs must play a vital role in data security and anti-hacking regulations to protect patients.

Eventually, the start-ups & emerging biopharma segment is anticipated to witness rapid growth. Factors, like leveraging digital solutions, the number of clinical pipelines, and enhanced demand for immunotherapies and other crucial treatments, are revolutionizing the developments in these start-ups and emerging biopharma companies. Various startups should incorporate regulatory planning from the early stages of development, many times collaborating with specialized consultancies or employing global capability centers in hubs, particularly India, to handle complex submissions and ensure patient safety and product quality.

| Segments | Shares % |

| Regulatory Information Management (RIM) Software Platforms | 34% |

| Document Management & eCTD Publishing Tools | 22% |

| Cloud-based RA Solutions | 18% |

| AI/Automation in Regulatory Intelligence | 14% |

| Manual / Consulting-driven Delivery | 12% |

Which Delivery Mode/Technology Enablement dominated the Regulatory Affairs Market in 2025?

The regulatory information management (RIM) software platforms segment captured the biggest share of the market by 34% in 2025. These types of platforms provide a single, centralized repository for all regulatory data, further supporting real-time visibility and better decision-making. The market encompasses sophisticated platforms, like DDiSmart and Freyr Digital, which expand trends consisting of AI, cloud computing, and predictive analytics to leverage proactive compliance and simplified workflows for life sciences and medical device companies.

Although the AI/automation in the regulatory intelligence segment will register the fastest growth, the use of AI helps in scanning regulatory databases, health authority portals, and industry publications for updates, new demands, and changes to present rules. Whereas NLP supports in extracting key information from large volumes of regulatory documents, translations, and submissions to detect related modifications and insights, ultimately minimizing manual review time. The emergence of cloud-based platforms, mainly RegIntel, uses advanced AI to continue complex global regulations into streamlined, actionable insights and intelligence for regulatory teams.

In the regulatory affairs market, North America accounted for a major share in 2025. As this region is the largest area that imposes the FDA-centric demands, and also possesses a robust CRO hub. Alongside the growing number of complex clinical trials and groundbreaking products (comprising biologics and personalized medicine), this results in a significant demand for specialized expertise to navigate strict regulations from agencies, like the FDA.

For instance,

U.S. Regulatory Affairs Market Trends

In November 2024, Quantiphi, an AI-first digital engineering company, and DDReg, a global company in regulatory expertise, partnered with a focus on addressing regulatory limitations faced by pharmaceutical, biotechnology, medical device, and cosmetics manufacturers.

Canada Regulatory Affairs Market Trends

The Canadian market comprises the execution of a new biocide regulatory landscape for disinfectants and sanitizers, with strong efforts toward outsourcing, and global trends, such as the adoption of AI, data integration, and IDMP standards within the pharmaceutical and health product sectors. A huge support of the official website, like Canada.ca, acts as a prominent source for regulatory updates and notices related to drug and health product regulations.

During 2025-2034, the Asia Pacific is predicted to register rapid growth in the regulatory affairs market. Primarily, this region is experiencing a major transformation in biopharma companies, clinical trials, and harmonization of regulations. This further impels the broader adoption of digitalization and AI algorithms in application screening, safety monitoring, and the complete effectiveness, especially in India, Singapore, Japan, and China. The co-regulator, like AI, supports the regulatory approval process, including granting and monitoring, to make processes quicker and greater data-driven.

Singapore Regulatory Affairs Market Trends

In August 2025, Singapore and Hong Kong signed a memorandum of understanding that fosters cooperation among their regulatory agencies to handle concerns regarding health products, like pharmaceuticals, medical devices, advanced therapy products, and traditional medicines.

Japan Regulatory Affairs Market Trends

In June 2025, Mitsubishi Research Institute, Inc. and Astellas Pharma Inc. entered into a memorandum of understanding to offer drug-discovery startups in Japan support in their efforts to go global.

The European regulatory affairs market is experiencing a notable expansion. A rise in negotiations supporting for evolution of a novel legislative framework, which will optimize access, cost-effectiveness, and supply of medicines across the EU. Thus, the other approaches by the European Medicines Agency (EMA) are unveiling a new platform that will assist in monitoring and managing medicine shortages and issuing the latest guidelines for companies.

For this market,

UK Regulatory Affairs Market Trends

The growing R&D activities and clinical trials across the UK are increasing the demand for various regulatory services. The UK also consists of robust regulatory agencies, which are also responsible for the approval of the products, where the growing regulatory complexities in the medical device development are also increasing the demand for their expertise.

MEA is expected to grow significantly in the regulatory affairs market during the forecast period, due to the rapid healthcare expansion, which is increasing the demand for regulatory requirements. The growing pharmaceutical manufacturing capabilities and clinical trials are also increasing their demand, which is enhancing the market growth.

Saudi Arabia Regulatory Affairs Market Trends

Saudi Arabia consists of robust regulatory authorities that oversee the regulatory compliance of products developed, which is increasing the demand for regulatory expertise in the industries. The growing innovations, expanding hospitals, and increasing clinical trials are also increasing their demand.

South America is expected to show lucrative growth in the regulatory affairs market during the forecast period, due to expanding pharmaceutical and biotechnology industries, and there is a growth in the regulatory requirement for the growing R&D activities and clinical trials. The growing development of medical devices and generic products are also increasing their demand, promoting the market growth.

Brazil Regulatory Affairs Market Trends

Brazil is experiencing a growth in the pharmaceutical industry, where it is promoting the development of medical devices, generics, and biosimilars, increasing regulatory submissions. The presence of stringent regulations and expanding healthcare systems is also increasing their demand for expertise.

|

Category

|

Key Players | Role in Ecosystem |

| Technology Providers | IQVIA, Veeva Systems, Oracle Health Sciences | Provide regulatory data platforms, submissions tools, and RIM systems |

| Product Manufacturers | Pfizer, Roche, Novartis (internal RA divisions) | Generate regulatory submissions for drug/device approvals |

| Service Providers | Parexel, ICON plc, Labcorp Drug Development | Offer regulatory consulting, submission support, compliance strategy |

| Platform Providers | Veeva Vault RIM, Oracle Argus, MasterControl | Centralized regulatory information management platforms |

| CROs/CDMOs | IQVIA, Parexel, Syneos Health | Provide end-to-end clinical + regulatory support services |

| Software Vendors | ArisGlobal, Ennov, Extedo | Specialized regulatory submission and document management software |

| Research Institutions | DIA (Drug Information Association), FDA collaborations, EMA research bodies | Provide regulatory frameworks, training, policy development |

| End-User Industries | Pharma, Biotech, Medical Devices, Diagnostics | Primary consumers of regulatory affairs services |

R&D

Clinical Trials and Regulatory Approvals

Formulation and Final Dosage Preparation

Packaging and Serialization

Patient Support and Services

| Tier 1 | Tier 2 | Tier 3 | |

| Typical Market Influence | 58% | 28% | 14% |

| Tier 1 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| Veeva Systems Inc. | Pleasanton, California, USA | United States | Global leader in life sciences cloud software with dominant Regulatory Information Management (RIM) systems | Veeva Vault RIM, Vault Submissions, Regulatory document management |

| IQVIA Holdings Inc. | Durham, North Carolina, USA | United States | Major global CRO and data analytics leader with strong regulatory intelligence and submissions support | Regulatory consulting, submission services, real-world data analytics |

| Oracle Corporation (Life Sciences Division) | Austin, Texas, USA | United States | Enterprise-grade clinical and regulatory software provider used in pharma compliance workflows | Oracle Argus Safety, Oracle Clinical One, regulatory data systems |

| Tier 2 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| ArisGlobal LLC | Miami, Florida, USA | United States | Specialized regulatory technology vendor focused on life sciences automation | LifeSphere RIMS, regulatory workflow automation |

| Ennov | Paris, Île-de-France, France | France | Strong mid-sized regulatory and quality management software provider | eCTD publishing, regulatory document management systems |

| Extedo GmbH | Munich, Bavaria, Germany | Germany | Leading European regulatory software provider specializing in eCTD submissions | eCTDmanager, regulatory submission publishing tools |

| Tier 3 | ||||

| Company Name | Headquarters | Country | Why Relevant to This Market | Key Products/Services |

| MasterControl Inc. | Salt Lake City, Utah, USA | United States | Quality and regulatory document management software provider for life sciences | QMS, document control, regulatory compliance software |

| Sparta Systems (Honeywell Life Sciences) | Princeton, New Jersey, USA | United States | Strong QMS and regulatory compliance platform provider | TrackWise Digital QMS, regulatory workflows |

In January 2025, Medical Regulation Gate (MRG) and the Regulatory Affairs Professionals Society (RAPS) announced a new collaboration to address the growing and emerging regulatory training requirements of Saudi Arabia and the broader Middle East region. Mohsen Al Muslimani, Chief Executive Officer of Medical Regulation Gate (MRG), stated that this accelerates the growth of the largest global organization of professionals involved in regulatory and quality assurance for healthcare products, enhancing offerings and support for this vital community of professionals.

By Service Type

By Category

By Product Type

By End-User/Client Segment

By Delivery Mode/Technology Enablement

By Region

Principal Consultant

Payal Rabde is a Healthcare Market Research Analyst at Towards Healthcare Research & Consulting with 4+ years of experience in pharmaceuticals, biotechnology, medical devices, and life sciences.

Learn more about Payal Rabde

Reviewed By

Aditi Shivarkar is a seasoned professional with over 14 years of experience in healthcare market research. As a content reviewer, Aditi ensures the quality and accuracy of all market insights and data presented by the research team.

Learn more about Aditi Shivarkar